Rheinmetall Q1 2026: When the Factory Outruns the Bureaucracy

The sovereign dependency thesis survived its first throughput test. Q2 decides whether the governor is temporary or structural.

TL;DR

The thesis moved from funding to throughput. Q4 proved sovereign customers would pre-fund Rheinmetall’s capacity; Q1 asks whether that funded capacity can turn into accepted deliveries, cash flow, and delivery credibility fast enough.

The moat is intact, but the governor is visible. Demand and funding are not the issue; the bottleneck is the conversion layer, customer acceptance, lot testing, procurement timing, inventory-to-revenue mechanics, and management bandwidth across Naval, Air Defence, Digital, autonomy, and deep strike.

At ~€1,207, the price finally makes the debate investable. The stock is no longer pricing most of the bull case, but Q2 is the proof point: if inventory converts and Q2 revenue validates management’s >50% growth claim, the flywheel works; if not, the “sovereign infrastructure” thesis starts looking like industrial overreach.

Rheinmetall reported Q1 sales of €1.94 billion, operating result of €224 million, an 11.6% operating margin, operating free cash flow of -€285 million, Rheinmetall Nomination of €4.87 billion, and backlog of €73.0 billion. That is the earnings recap. It is also the least useful way to understand the quarter.

The right place to start is with our own evolution. In Q3, we worried that Rheinmetall’s story was running into industrial physics: backlog was enormous, but cash burn and ammunition margin pressure suggested that being indispensable did not automatically mean being cash-generative. In Q4, we changed our view. The important discovery was not that free cash flow improved; it was how it improved. Sovereign customers were prepaying because they needed Rheinmetall’s capacity more than Rheinmetall needed incremental orders. We upgraded the moat from regulatory entrenchment to sovereign dependency: governments were financing the industrial capacity they could not replace.

Q1 does not reverse that conclusion. It makes it more precise. The funding debate is no longer the center of the thesis. The throughput debate is.

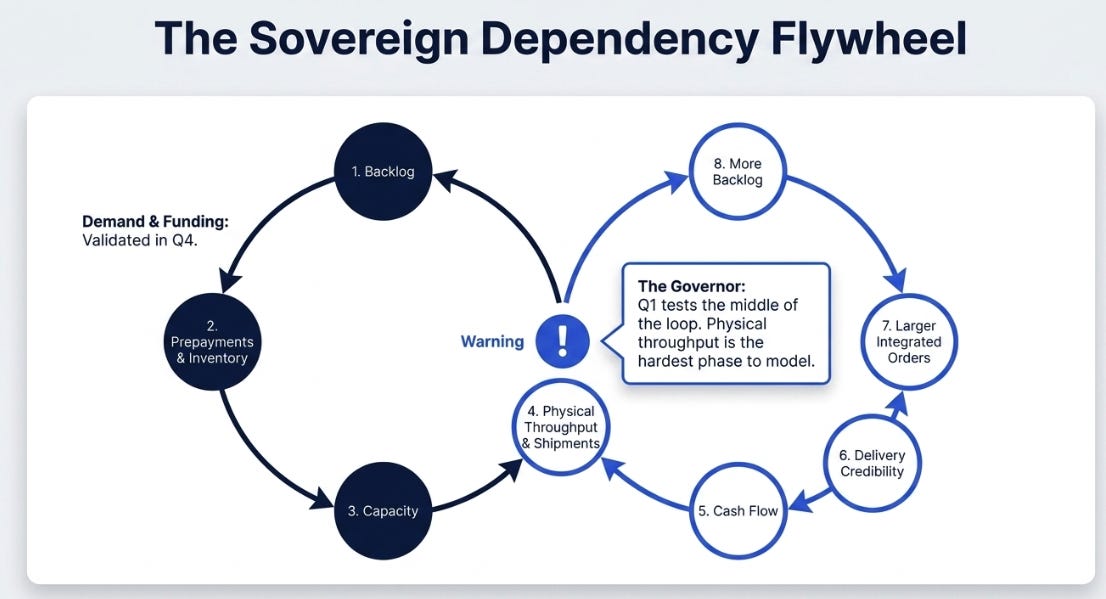

Q4 proved Rheinmetall’s customers would fund the moat. Q1 asks whether Rheinmetall can operate it.

The Factory Outran the Bureaucracy

The sell-side version of Q1 is easy: sales growth disappointed, cash flow was negative, and the company promised a stronger Q2. That is true, but too shallow.

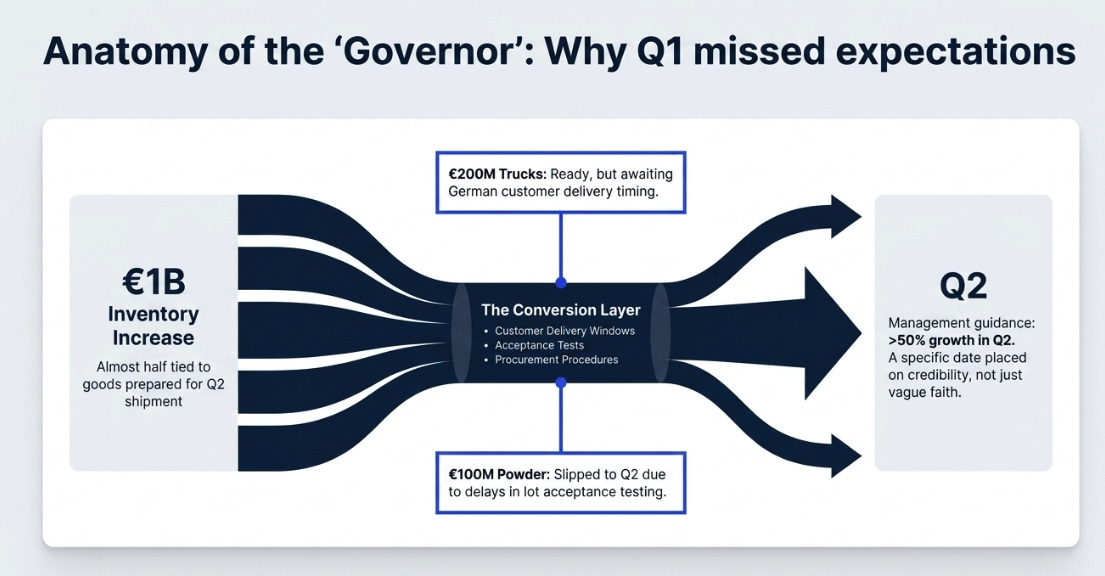

Management’s explanation was unusually specific. Around €200 million of trucks were ready but awaiting German customer delivery timing; another €100 million of powder-related revenue slipped because lot acceptance testing pushed delivery into Q2. Papperger therefore guided to Q2 growth of more than 50%.

That is the key point: not the miss, but the specificity of the test. A vague “second-half recovery” is management asking for faith. “More than 50% growth in Q2” is management putting a date on credibility.

The quarter’s core tension is that the factory appears to be scaling faster than the conversion layer around it: customer delivery windows, acceptance tests, procurement procedures, and inventory-to-revenue mechanics. CFO Klaus Neumann said roughly €0.5 billion of inventory went into finished and pre-finished goods ready for Q2 shipment; almost half of the €1 billion inventory increase was tied to goods prepared for Q2.

If that inventory ships, Q1 was the balance-sheet shadow of growth. If it does not, Q1 was the first warning that the capacity flywheel has a governor.

The Mechanism Is Intact, Not Yet Confirmed

The fundamental question is whether Rheinmetall can turn customer-funded capacity into a durable sovereign infrastructure role. Europe has moved from a just-in-time defense model to a just-in-case security model. In the old world, budgets were the bottleneck. In the new world, budgets are increasingly visible; the bottleneck is deliverable industrial capacity.

Rheinmetall’s core capability is not “making tanks” or “making shells.” It is capacity credibility: powder, ammunition, propulsion, vehicles, air defense, digital systems, autonomy, and now naval, assembled into something governments can actually procure, deploy, and maintain.

That mechanism compounds if backlog and prepayments fund capacity, capacity improves delivery credibility, credibility wins larger integrated orders, and those orders deepen Rheinmetall’s role as sovereign defense infrastructure. It breaks if inventory does not convert, if acceptance delays become structural, if Weapon & Ammunition margins normalize faster than volume scales, or if Naval and Digital absorb capital without proving platform economics.

Q1 gave us evidence that the mechanism is still working. It did not prove it.

Operating profit grew 17% on 8% sales growth. Vehicle Systems grew only 3%, but margin improved to 9.6%. Weapon & Ammunition was flat on sales, but held 19.4% margin. Digital Systems grew 16%, with margin rising to 5.2%. Air Defence was the standout: more than 30% growth, with margin expanding from 12.5% to 15.6%. Naval contributed its first month at €77 million of sales and roughly 10% profitability.

That is not a broken quarter. It is an unfinished quarter.

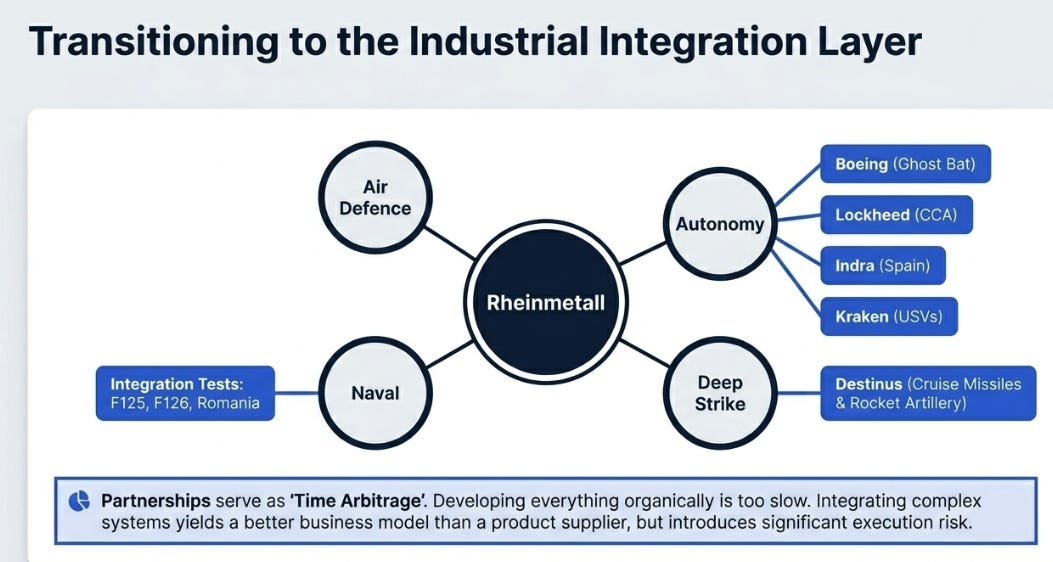

The Integration Layer

The most important strategic development in Q1 was not in the income statement. It was in the widening of the architecture.

Naval closed in February. Management said the first month was in line with expectations, at about €80 million of sales and 10% EBIT, with profitability expected to move over time toward 15%. F125, F126, and Romania are the first tests of whether this becomes a real Sea domain or merely an expensive shipyard acquisition.

The same logic applies to autonomy and deep strike. Rheinmetall is not trying to invent everything internally. It is using partnerships as time arbitrage: Boeing for Ghost Bat, Lockheed for CCA cooperation, Indra for Spain, Kraken for unmanned surface vessels, Destinus for cruise missiles and ballistic rocket artillery. Papperger’s point was explicit: partnerships are faster than development programs, and Germany does not have time to wait for organic development of every new capability.

Viewed individually, each initiative can be justified. Viewed collectively, they reveal both the bull case and the risk. Rheinmetall is trying to become the industrial integration layer across vehicles, ammunition, air defense, ships, drones, missiles, sensors, and command systems. That is a better business than a product supplier. It is also a harder business to execute.

The company is becoming more important because it is becoming broader. It is becoming riskier for the same reason.

Variant Perception: Rearmament Is Not the Edge

The market already understands that European defense spending is going up. That is not the variant perception.

The better question is whether Rheinmetall is becoming the sovereign infrastructure layer that converts budgets into capability. The loop is:

backlog → prepayments and inventory → shipments → cash → capacity → delivery credibility → larger integrated orders → more backlog.

Q1 matters because it tests the middle of the loop. Demand is visible. Funding was validated in Q4. Now comes the harder-to-model part: physical throughput.

At €1,542 after Q4, we argued that the business had improved but the entry had not. The ceiling rose, but much of the upgraded thesis was priced. At roughly €1,207 now, the setup is different. The stock is no longer asking investors to pay for most of the bull case. It is closer to paying for the base case while preserving upside if Q2 proves the governor is bureaucratic rather than structural.

That does not mean the stock is obvious. It means the debate is finally worth having.

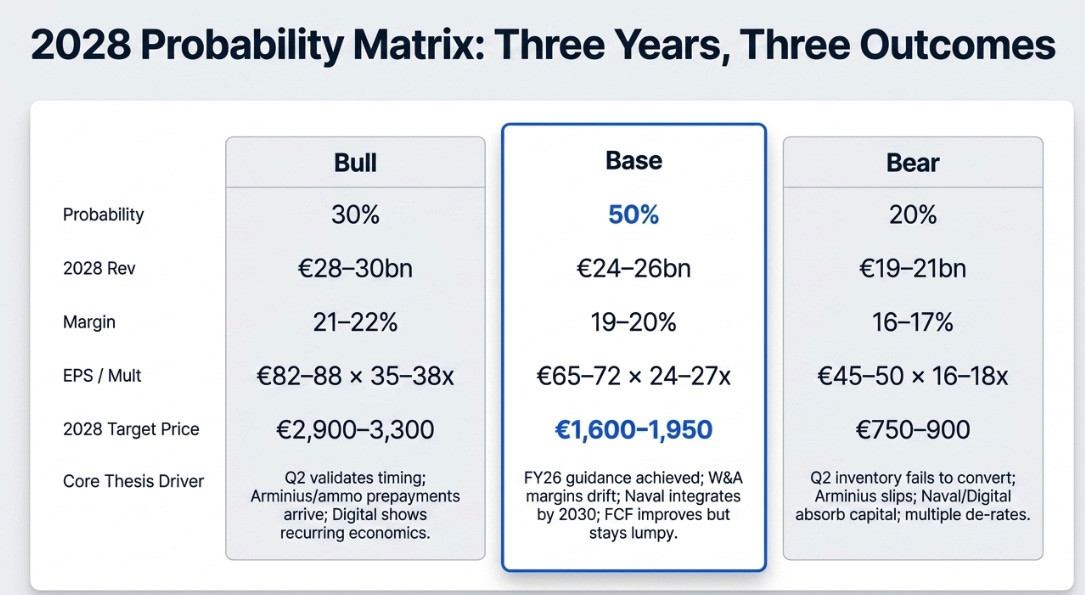

Three Years, Three Outcomes

By 2028, this should be clear. Capacity will either translate into output or it will not. Digital will either show platform economics or remain project revenue. Naval will either integrate or absorb management time. Arminius, ammunition, Air Defence, and Middle East demand will either convert or stay in procurement fog.

Assuming a current price around €1,207:

The probability-weighted value lands roughly in the high-€1,700s to low-€1,800s before dividends. That is a materially better setup than at €1,542. But it is still not a sleepy value stock. You are being compensated for execution risk, not spared from it.

What Has to Happen Next

The thesis is now unusually measurable.

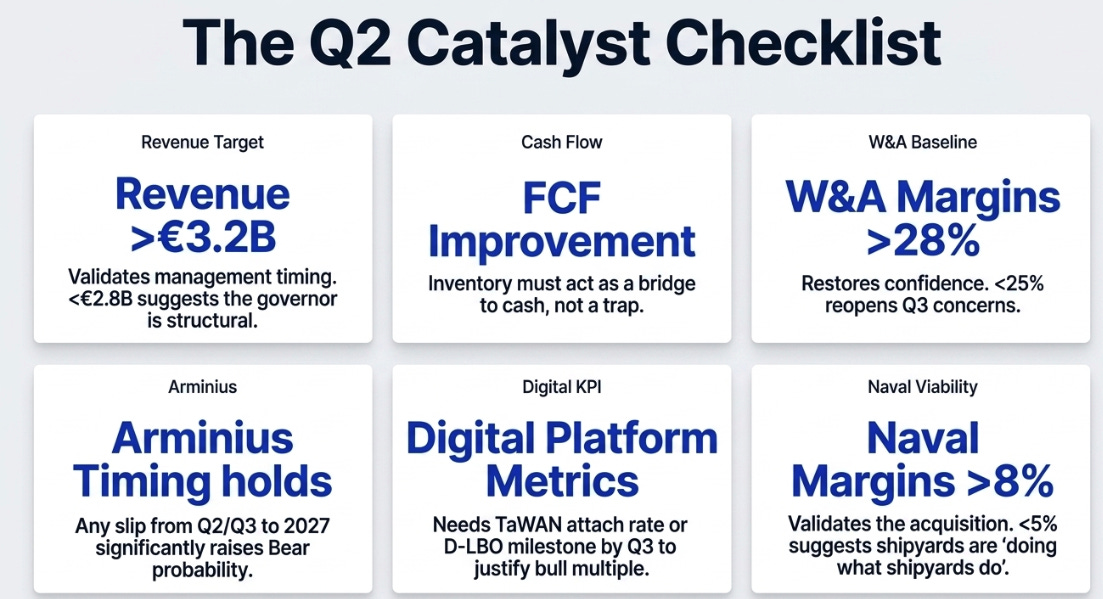

First, Q2 revenue needs to validate management’s timing explanation. Above €3.2 billion would be a strong signal; below €2.8 billion would suggest the governor is more structural than bureaucratic. Second, operating free cash flow must improve in Q2 and H2; inventory has to be a bridge, not a trap. Third, Weapon & Ammunition margins need a clean baseline under the new structure; 28%+ would restore confidence, while below 25% would reopen the Q3 concern. Fourth, Arminius language matters: any move from Q2/Q3 to 2027 raises the bear probability. Fifth, Digital Systems needs at least one platform KPI by Q3, software or services mix, TaWAN attach rate, D-LBO milestone, lifecycle revenue, because without it the bull multiple is narrative, not evidence. Sixth, Naval margins above 8% through the year would suggest the acquisition works; below 5% would suggest shipyards are doing what shipyards often do.

What Changed

Our view did not reverse after Q1. It became more precise.

Q3 warned that backlog could run into industrial physics. Q4 showed sovereign customers would finance the capacity they could not replace. Q1 now asks the next and harder question: can Rheinmetall turn funded capacity into delivered capability fast enough to make the dependency permanent?

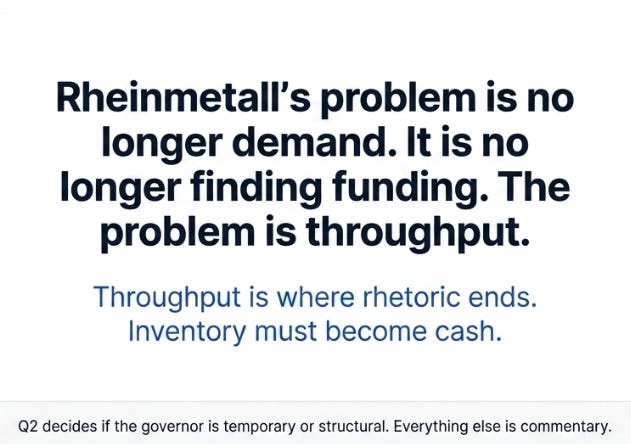

Rheinmetall’s problem is no longer finding demand. It is no longer, at least for now, finding funding. The problem is throughput.

Throughput is where rhetoric ends. Trucks must be accepted. Powder must be qualified. Naval programs must be integrated. Digital systems must prove recurring economics. Air defense conversations must become contracts. Inventory must become cash.

At €1,207, the price finally acknowledges some of that risk. Whether the business validates the price arrives in Q2. Everything else is commentary.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.