Rolls-Royce 2H25 Earnings: The Toll Booth Compounds

Rolls-Royce didn’t just prove the turnaround worked. It revealed a monopoly-like engine annuity with most of the cash still to come, and a geopolitical selloff briefly handed investors a cheaper entry

TL;DR

· Rolls-Royce’s FY2025 results suggest this is no longer a simple recovery story: Civil Aerospace margins hit 20.5%, free cash flow reached £3.27bn, and management raised mid-term targets while announcing a multi-year buyback.

· The key new insight is in LTSA economics: management showed the cash value of long-term service agreements has more than quadrupled since 2022, with roughly 75% of the incremental value still unrealised by 2028.

· The article’s variant view is that the market still treats Rolls-Royce like a cyclical industrial, when it increasingly looks like a mission-critical installed-base compounder whose pricing power, durability gains, fleet growth, and cost efficiency reinforce each other over time.

What We Said, What Happened, What Changed

In January, we published The Physics of Pricing Power, arguing that Rolls-Royce had completed one of the most remarkable transformations in industrial history. The thesis was straightforward: Rolls-Royce had spent a decade buying exclusivity on the A350 and A330neo, locking airlines into TotalCare contracts they could not exit, and then, under Tufan Erginbilgic, had finally exercised the pricing power it had spent twenty years refusing to use. The turnaround wasn’t cost-cutting. It was monetising switching costs.

We believed every word of that thesis. We also said the stock, at 1,273p, left no room for error. Our probability-weighted return was negative. The opportunity, we wrote, “lies not in the thesis but in patience.”

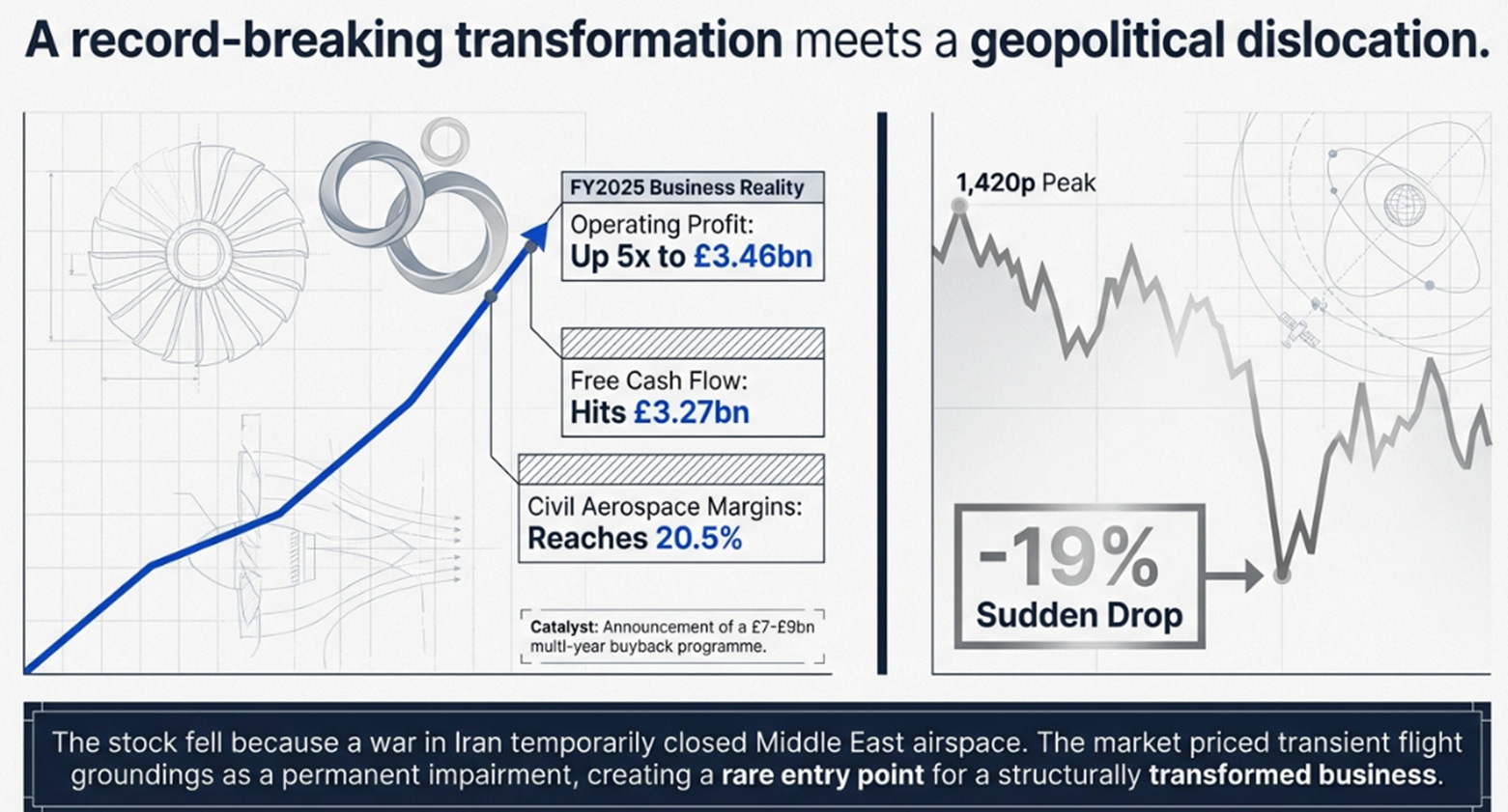

On 26 February, Rolls-Royce published the best results in its 120-year history. Operating profit reached £3.46 billion, five times the 2022 level. Free cash flow hit £3.27 billion. Civil Aerospace margins reached 20.5 percent. Every mid-term target was raised by 25 to 40 percent. A £7 to £9 billion buyback, the first multi-year programme in the company’s history, was announced. The stock hit an all-time high of 1,420p.

Then a war started in Iran, Middle East airspace closed, and the stock fell 19 percent in three weeks.

We got the business right and the stock setup wrong, or rather, we got it wrong for approximately four hours before geopolitics corrected the price for us. The entry point we said to wait for arrived, but not because the business disappointed. It arrived because a conflict 4,000 miles away temporarily grounded some flights.

That is interesting. But it is not the most interesting thing that happened. The most interesting thing was a chart that Erginbilgic showed during the earnings presentation, a chart that was not in the press release, not in the financial tables, and that most analysts have still not fully incorporated into their models. That chart is the reason our view has changed.

The Annuity Reveals Itself

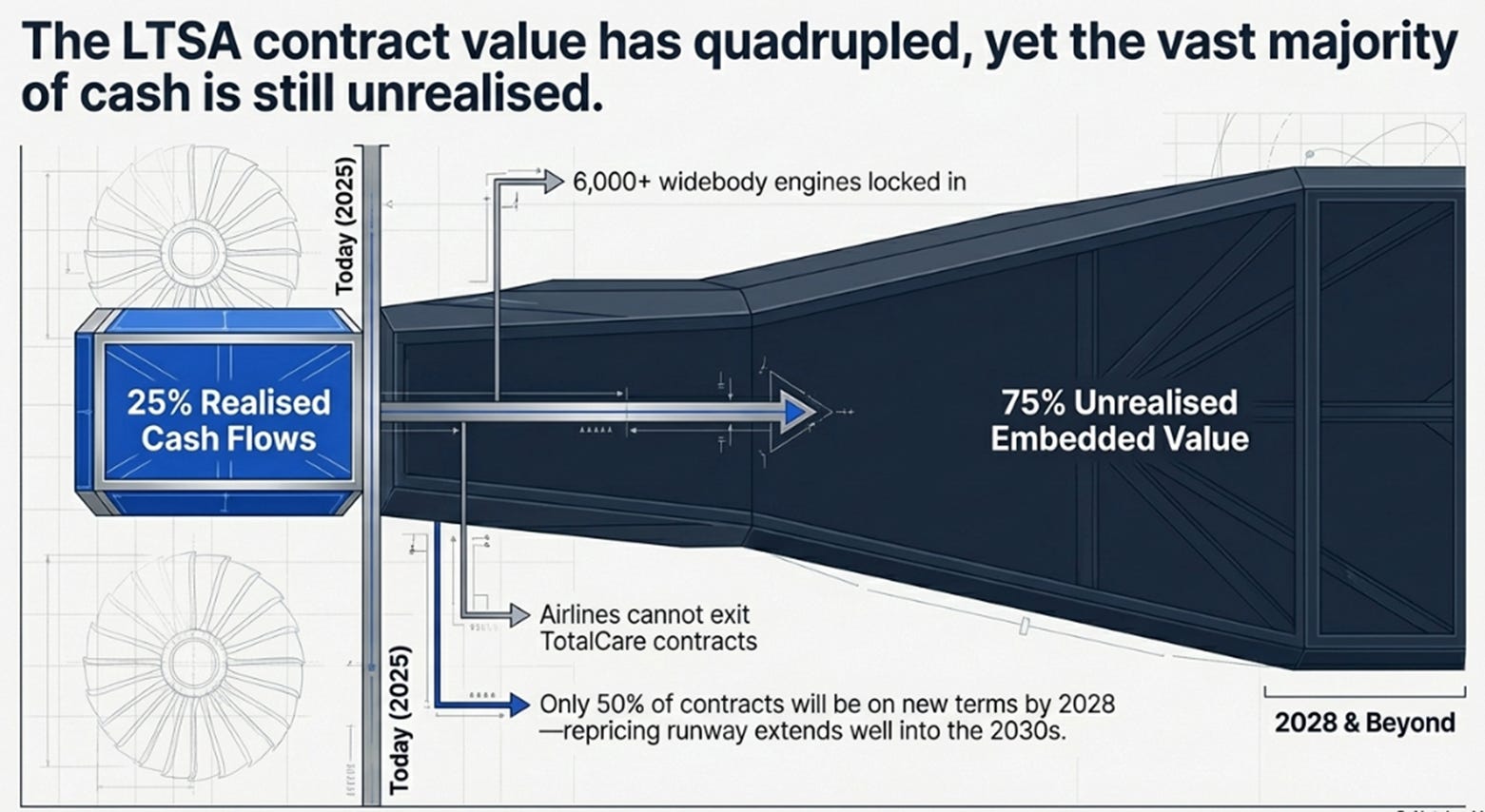

The chart showed that the cash value of Rolls-Royce’s LTSA contracts, the long-term service agreements under which airlines pay per engine flying hour, has more than quadrupled since 2022. More than two-thirds of that increase came from management actions: contract renegotiations, time-on-wing engineering improvements, and EFH rate optimisation. Volume recovery contributed less than a third.

By 2028, only 25 percent of the incremental cash associated with those improved contracts will have been realised.

Read that again. The installed base of 6,000-plus widebody engines, flying under contracts that airlines cannot exit, on aircraft where no alternative engine exists, has been re-priced so aggressively that the embedded future cash flows have quadrupled, and three-quarters of that value has not arrived yet. Moreover, only half of LTSA contracts will be on new terms by 2028, meaning the re-pricing runway extends well into the 2030s.

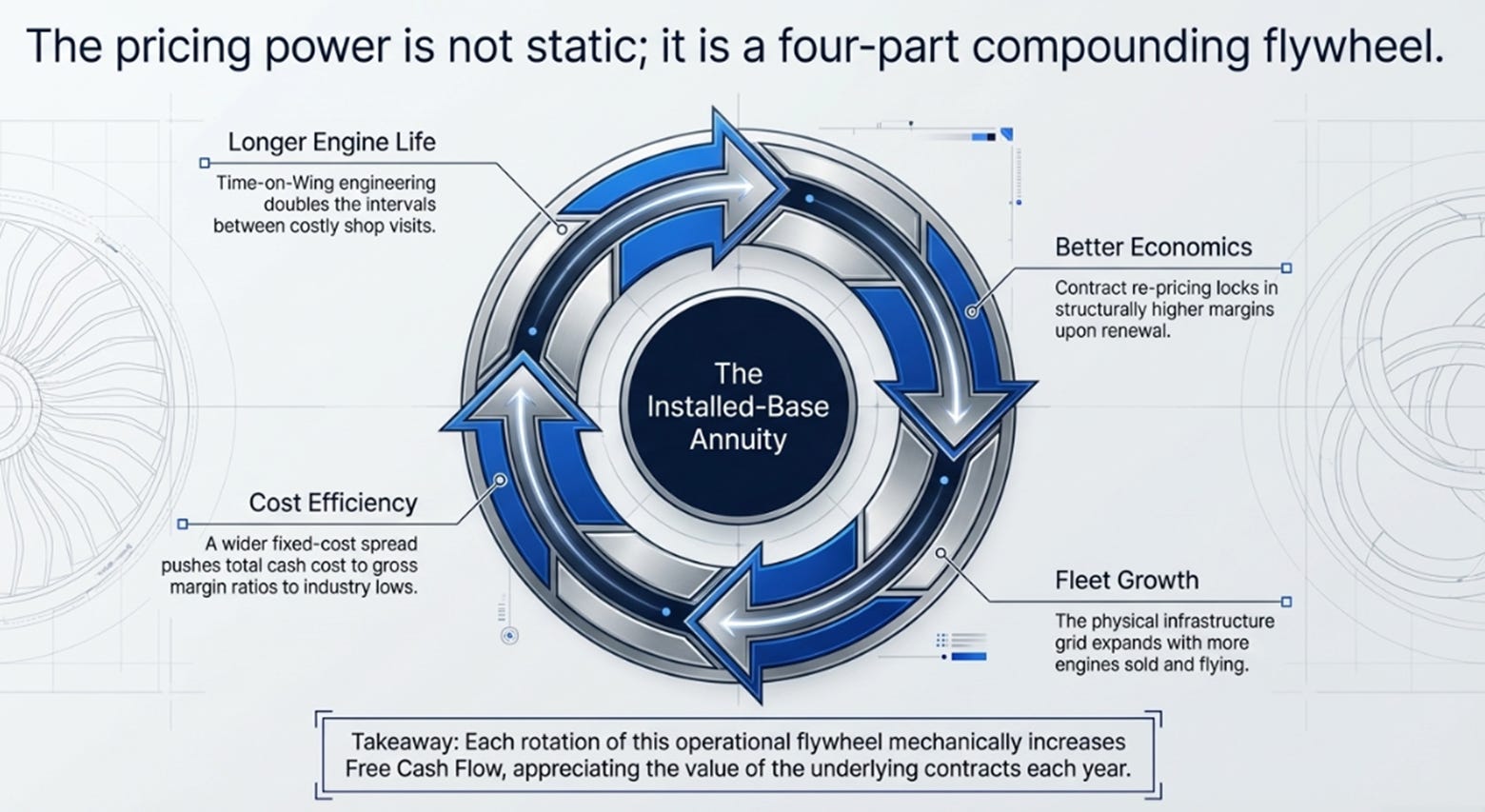

Our January piece described Rolls-Royce’s economics correctly. We called it a toll booth. What we missed was that the toll booth was still being expanded. We treated the pricing power as a static advantage, the company had monopoly positions and was finally charging for them. The FY2025 disclosure revealed it is a compounding advantage, a flywheel with four interlocking elements that reinforce each other at scale.

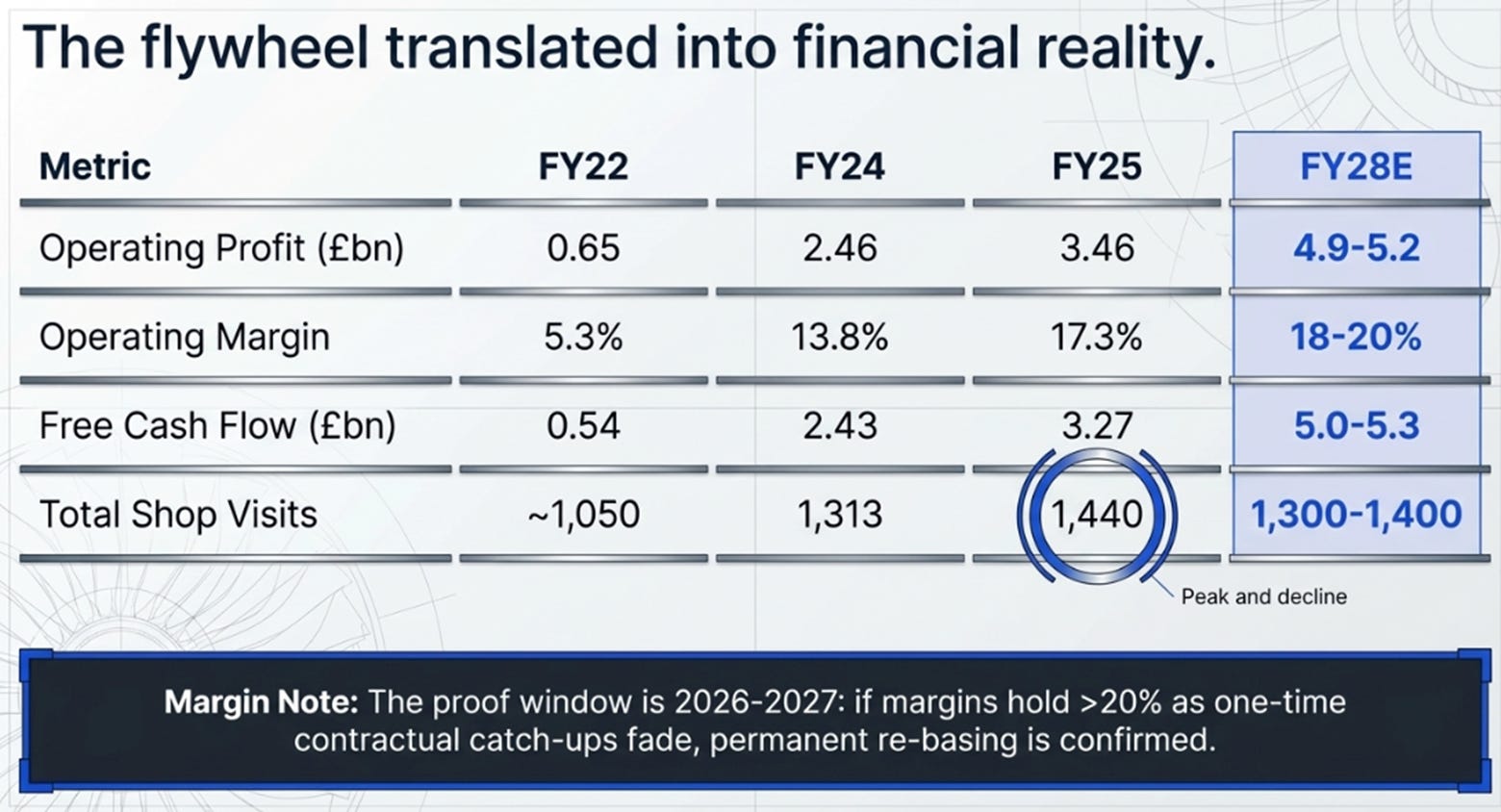

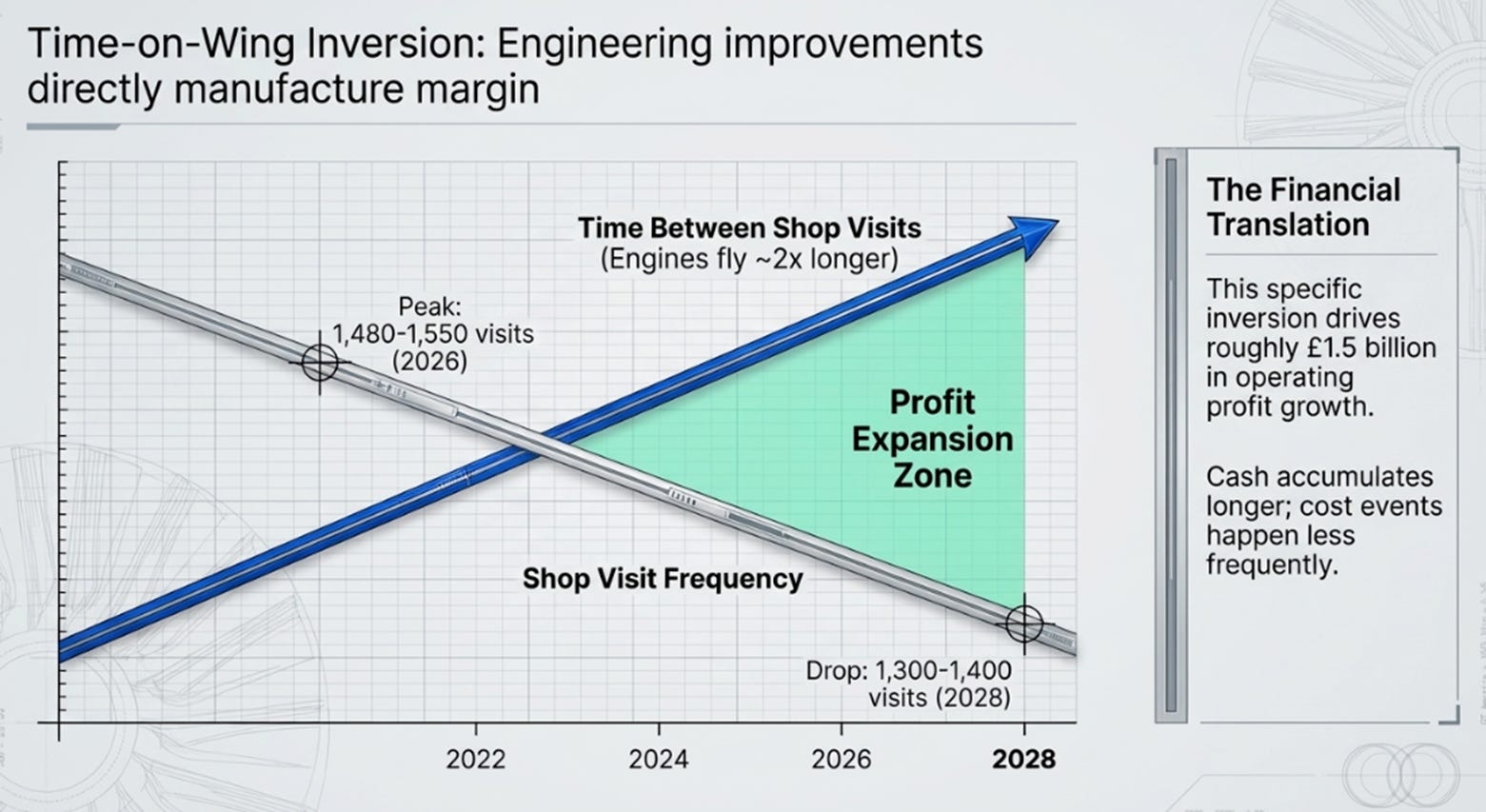

The first element is time-on-wing. Rolls-Royce has now raised its durability target to more than 100 percent improvement across in-production Trent engines, with more than half already delivered. The Trent XWB-84 life extension programme completes in 2026. The practical consequence is that engines now fly roughly twice as long between shop visits. During those extended intervals, the airline pays per flying hour under the LTSA. Cash accumulates longer before the next cost event. The cost event itself is cheaper because visit frequency falls. Management quantified the result: shop visits peak in 2026 at 1,480 to 1,550, then decline to 1,300 to 1,400 by 2028. Over the same period, operating profit grows by roughly £1.5 billion.

Fewer shop visits. Higher profitability. That inversion is not a recovery. It is the flywheel made visible in the guidance.

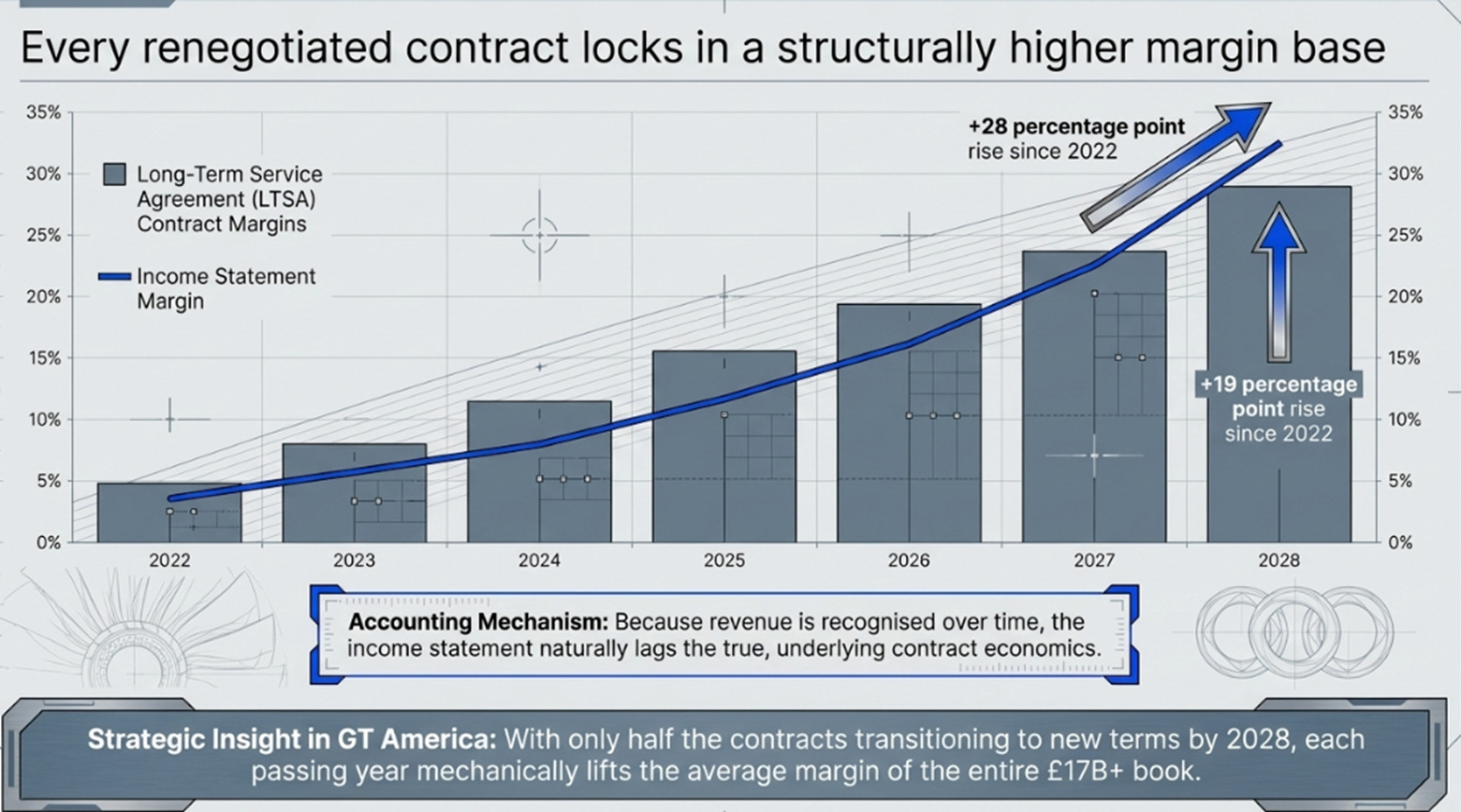

The second element is contract re-pricing. Each LTSA that renews or renegotiates comes in at higher margins than its predecessor. Management disclosed that LTSA contract margins have risen 19 percentage points since 2022, while the income statement margin, which lags because revenue is recognised over time, has risen 28 points. Since only half of contracts will be on new terms by 2028, each year that passes lifts the average margin of the entire book as more contracts flip to the new economics.

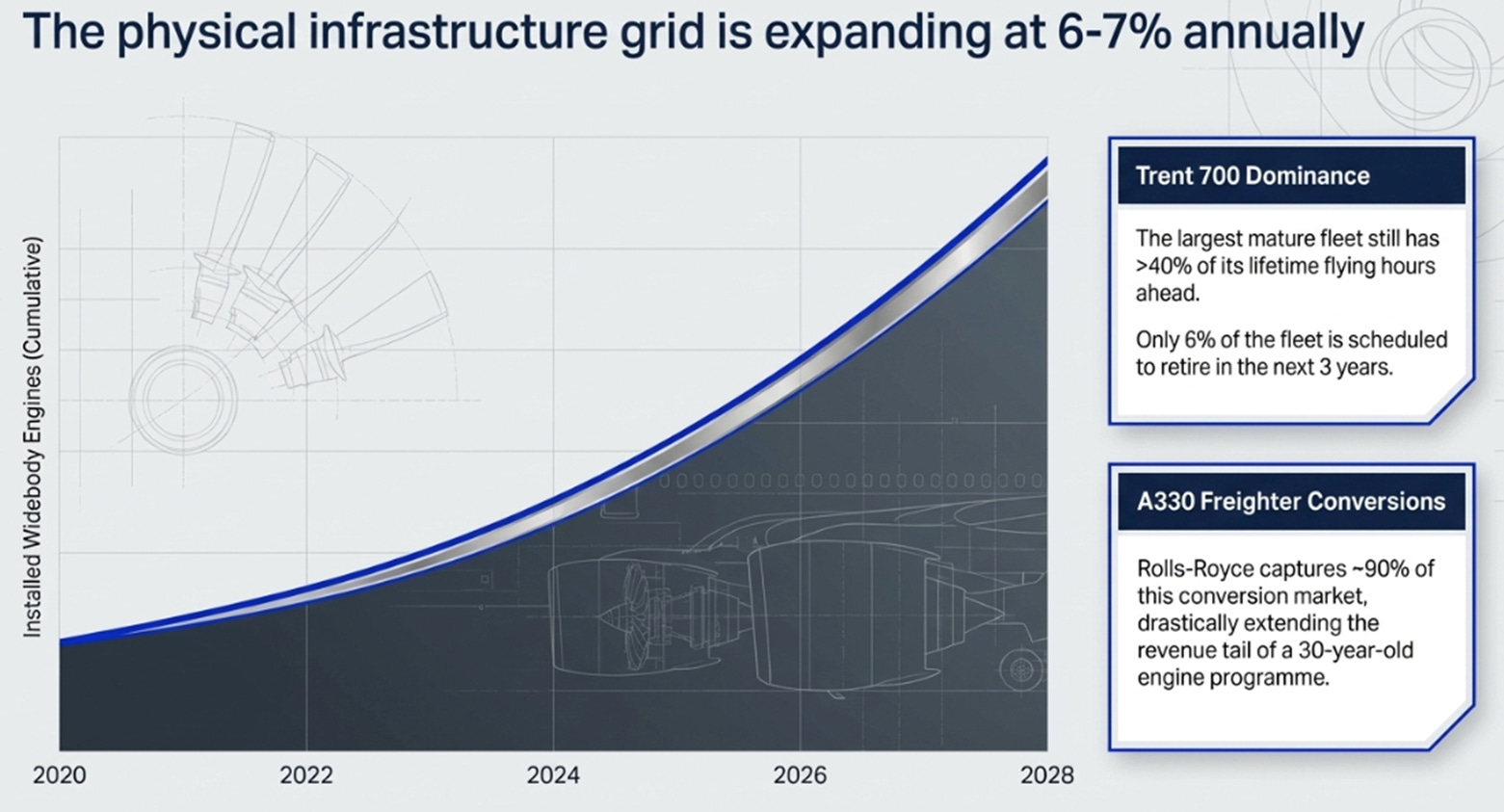

The third element is fleet growth. The installed widebody engine base is expanding at 6 to 7 percent annually. Each new engine arrives with a new LTSA, contracted at the higher margin. The Trent 700, the largest mature fleet, still has more than 40 percent of its total lifetime flying hours ahead, with only 6 percent retired in three years. The A330 freighter conversion market, where Rolls-Royce captures roughly 90 percent of conversions, extends the revenue tail of a thirty-year-old engine programme further still.

The fourth element is cost efficiency. The total cash cost to gross margin ratio has fallen from 0.80x in 2022 to 0.36x in 2025, best-in-class in the industry. This is the quiet compounder: the fixed cost base spreads across more engines, more flying hours, and more aftermarket revenue with each passing year.

The engine is the physical infrastructure. The LTSA is the subscription. Time-on-wing is the churn reduction programme. Together they produce economics that resemble a contracted annuity more than a manufacturing business, except the contract duration is measured in decades, and the annuity appreciates rather than depreciates with each passing year.

There is a tension worth naming. Management says the contribution from contractual improvements, the onerous releases and catch-ups that added £392 million in FY2025, will be reduced by 2028. If margins compress as that tailwind fades, the flywheel thesis weakens from “permanent re-basing” to “one-time repricing with partial reversion.” If margins hold above 20 percent without that support, the thesis is confirmed. The proof window is 2026 to 2027.

The Second Business and the Category Question

There is a quieter development that most coverage treats as a footnote but that may matter as much as the LTSA disclosure over a three-year horizon.

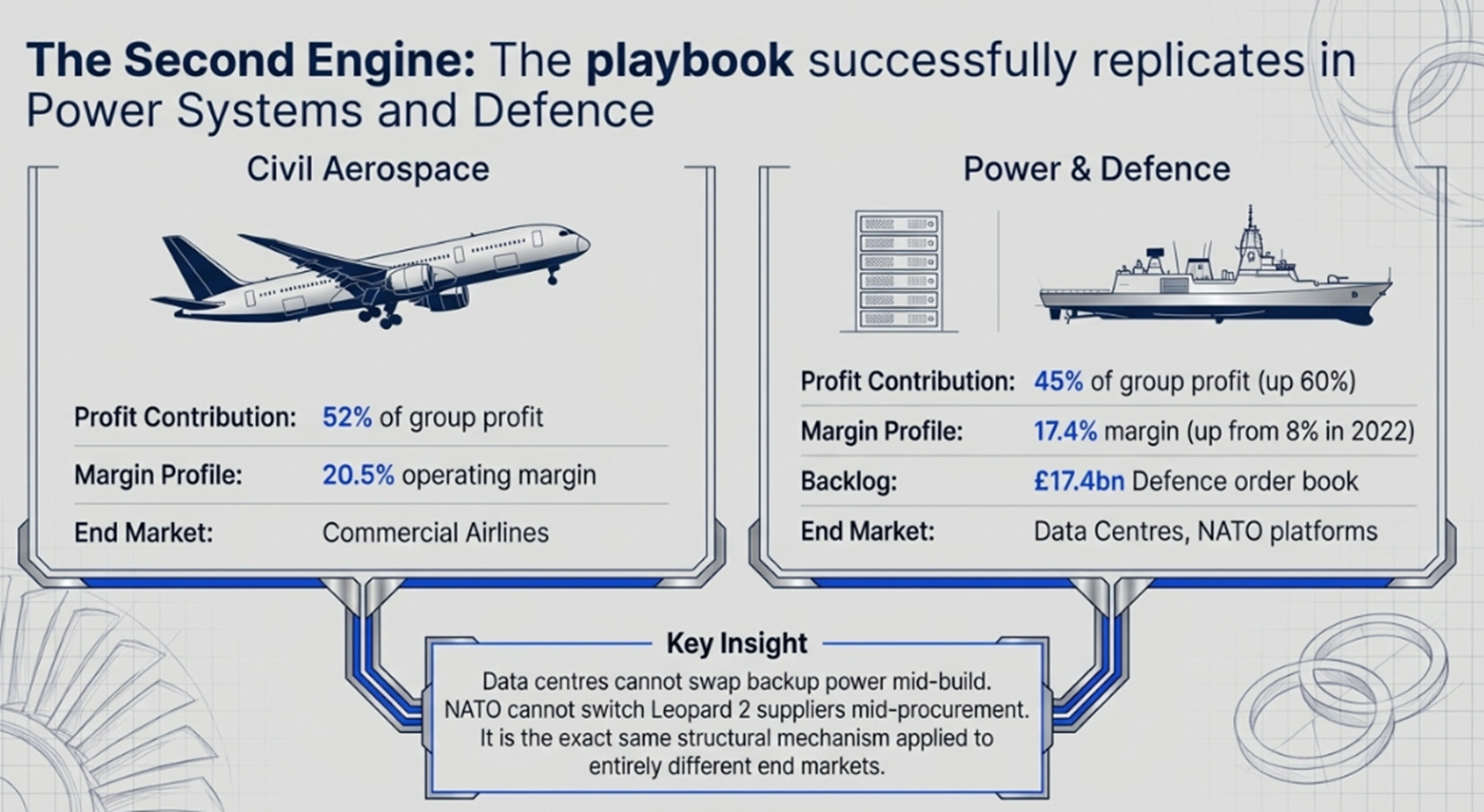

Rolls-Royce is no longer one business. Civil Aerospace generated 52 percent of group operating profit in FY2025 and absorbs 90 percent of investor attention. But Power Systems, backup power generators for data centres, engines for NATO land and naval platforms, battery energy storage, delivered £852 million of operating profit, up 60 percent, on 17.4 percent margins. Defence contributed £689 million on a £17.4 billion order backlog representing more than three years of revenue. Together, these two divisions now account for 45 percent of group earnings, and both are growing.

The temptation is to frame Power Systems as an “AI data centre play.” Data centre revenue did grow 35 percent, and management targets 20 percent annual growth in power generation to 2028. But wrapping diesel and gas generators in hyperscaler language is partly narrative engineering. Data centres are 5 to 7 percent of group revenue. That does not transform the category alone.

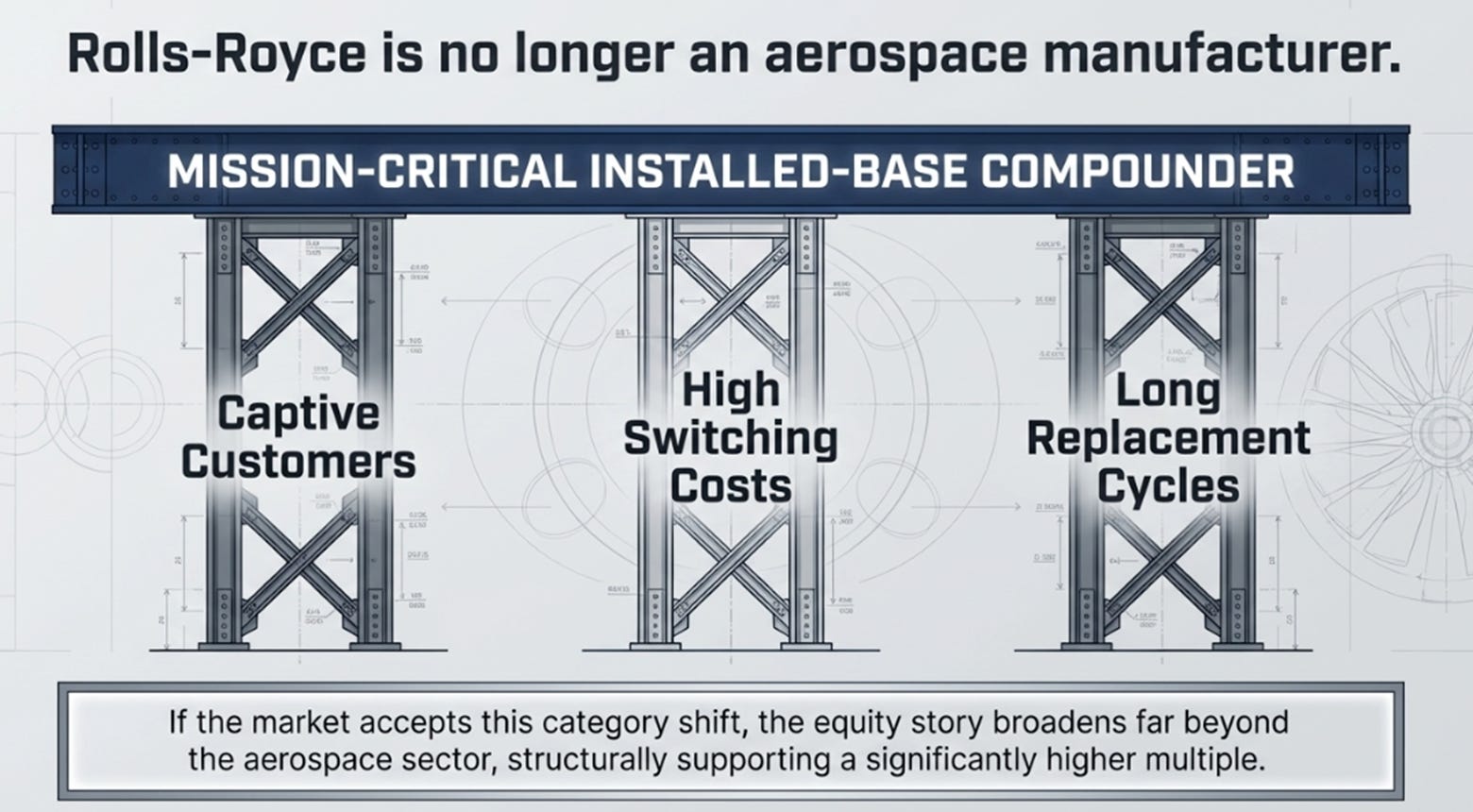

The more important insight is structural. Rolls-Royce’s pricing power formula, captive customers operating mission-critical infrastructure with high switching costs and long replacement cycles, is not unique to civil aviation. Data centres cannot easily swap backup power providers mid-build. NATO armies cannot switch Leopard 2 engine suppliers mid-procurement. The commercial optimisation playbook that produced 20.5 percent margins in Civil Aerospace is now producing 17.4 percent margins in Power Systems, up from 8 percent in 2022. Same mechanism, different end market.

If Power Systems sustains 18 to 20 percent margins and Defence maintains its £17 billion-plus backlog, the equity story broadens from “civil aerospace aftermarket” to “mission-critical installed-base compounder.” That category shift, if the market accepts it, supports a structurally higher multiple than the aerospace sector alone would warrant.

The Variant Perception and the Iran Dislocation

The consensus view of Rolls-Royce is now favourable. Thirteen of eighteen analysts rate the stock a Buy. The average price target is approximately 1,400p. The transformation is respected.

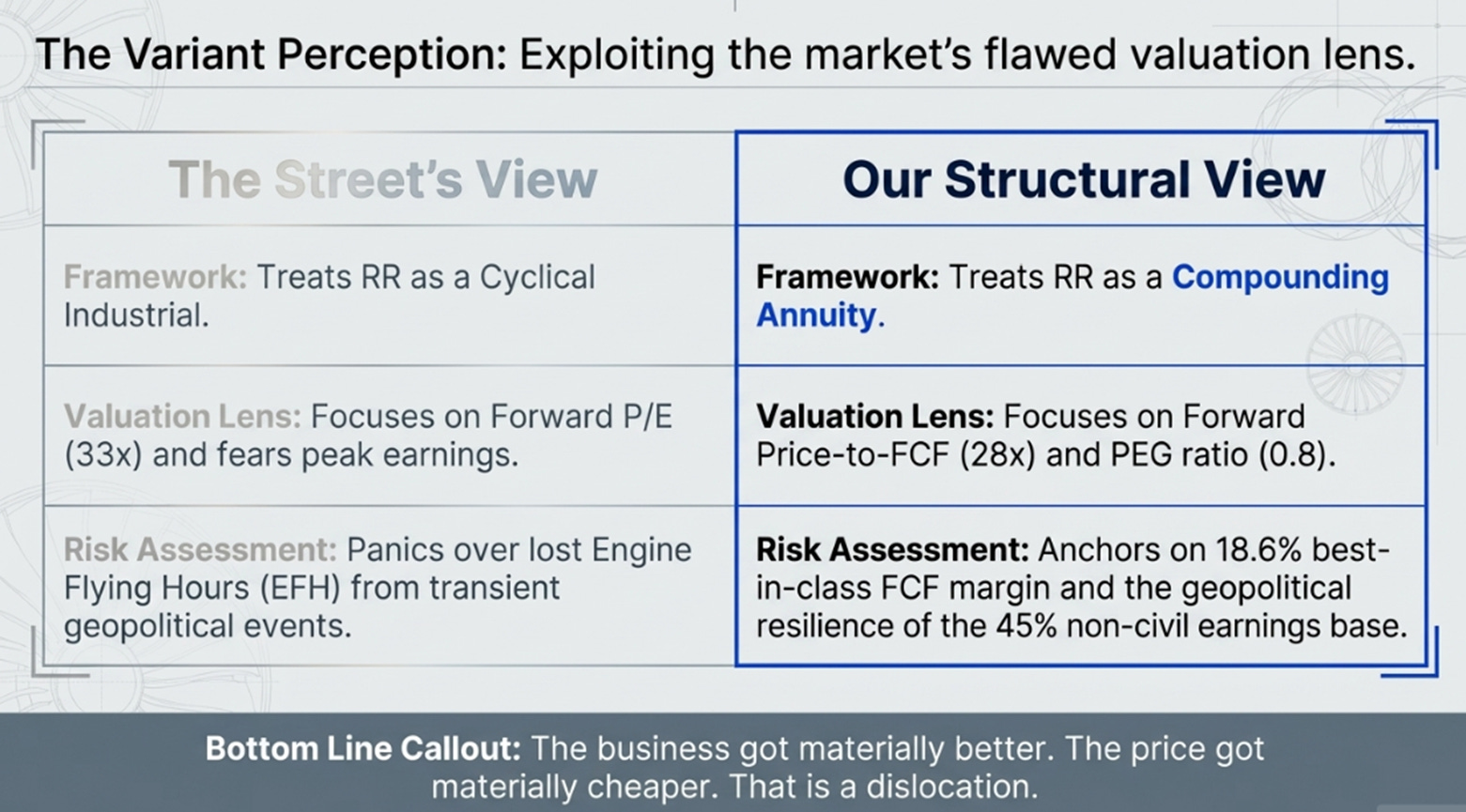

But the consensus still frames Rolls-Royce as a cyclical industrial trading at a full multiple. The trailing P/E of 17x looks optically cheap because it includes non-recurring statutory gains; the forward P/E of 33x looks expensive because the market values each year of earnings as if it might be the peak. The sell-side worries about margin normalisation as contractual catch-ups fade. It discounts each quarter of EFH data as if the current flying hour rate is the permanent one.

Our variant view is different. The correct valuation lens is forward price-to-free-cash-flow, which stands at 28x, and the PEG ratio, which is 0.8. An FCF margin of 18.6 percent, best-in-class among global aerospace peers, applied to a business growing earnings at 17 percent with net cash on the balance sheet and a massive buyback compressing the denominator does not screen as expensive on any quality-compounder framework. It screens as cheap.

The Iran war made the disconnect vivid. A temporary grounding of Middle East flights, affecting 15 to 20 percent of widebody traffic for a period of months, triggered a 19 percent stock decline. The market priced each lost flying hour as if it were permanent. It ignored the fact that COVID collapsed engine flying hours by 57 percent and the LTSA contracts survived intact. It ignored the 75 percent of contracted future cash that sits beyond 2028. It ignored that Defence and Power Systems, 45 percent of earnings, are either neutral or positively exposed to geopolitical instability.

The business got materially better. The price got materially cheaper. That combination has a name: dislocation.

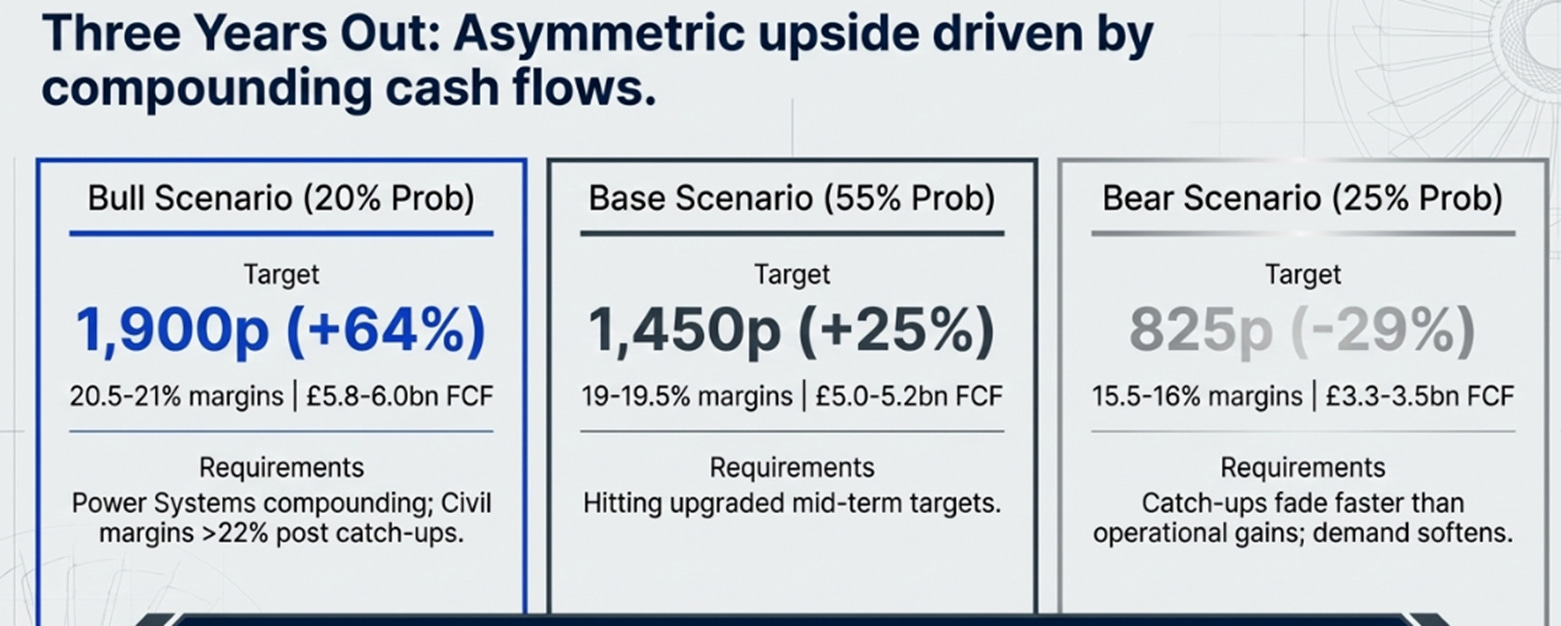

Three Years Out

The three scenarios below are three different answers to one strategic question: is Rolls-Royce a turnaround ending, or an annuity beginning to compound?

The probability-weighted value is approximately 1,340p, implying 16 percent upside and an annualised return of 9 to 10 percent including dividends. The buyback mechanically retires 600 to 700 million shares over the period, lifting earnings per share by 3 to 4 percent annually regardless of which scenario unfolds.

What to Watch, and What We Would Do

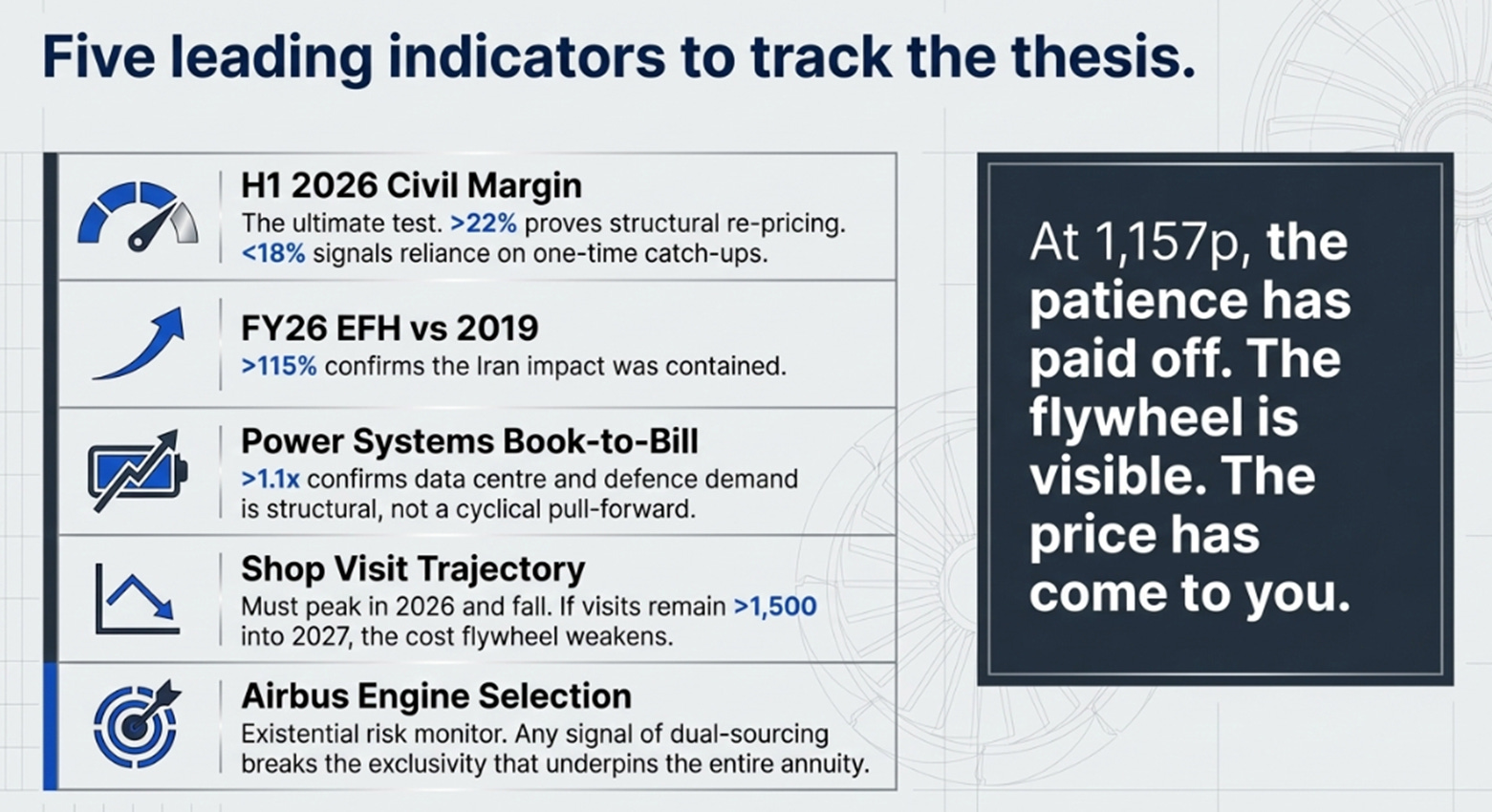

Five things determine which scenario wins.

First, Civil Aerospace operating margin in H1 2026. Above 22 percent confirms the flywheel is self-sustaining without contractual catch-ups. Below 18 percent means the catch-up benefit was the margin story, not structural re-pricing. This is the single most important data point.

Second, FY2026 engine flying hours relative to 2019. Above 115 percent means the Iran conflict’s impact was contained. Below 108 percent implies a demand impairment that delays the mid-term earnings trajectory.

Third, Power Systems book-to-bill. Above 1.1x confirms structural demand from data centres and defence. Below 0.9x suggests the growth was a cyclical pull-forward, and the 18 to 20 percent margin target is at risk.

Fourth, shop visit trajectory. Management says visits peak in 2026 then fall. If they remain stubbornly above 1,500 into 2027, the time-on-wing engineering is lagging the timeline, and the flywheel’s cost leg weakens.

Fifth, Airbus engine selection signals. The existential long-term risk is not recession, Iran, or supply chains. It is Airbus opening a future widebody programme to competitive engine selection, breaking the exclusivity that underpins the entire annuity. Any signal of dual-sourcing, at Farnborough, in Airbus capital markets days, or in airline lobbying, demands immediate reassessment of terminal value.

In January we argued that Rolls-Royce had become a toll booth. The FY2025 results proved something we did not fully appreciate: the toll booth compounds. Each year, the installed base is worth more than the year before, through longer engine life, higher contract margins, fleet growth, and cost efficiency that reinforces itself at scale. Management disclosed this for the first time in a form that makes the economics measurable rather than theoretical.

At 1,157p, you are paying 28 times forward free cash flow for the highest FCF margin in aerospace, a compounding installed base with three-quarters of its value still ahead, a £2.5 billion annual buyback shrinking the denominator, and the cleanest balance sheet in the company’s 120-year history. The January piece said the opportunity lay in patience. The patience paid off. The flywheel is visible. The price has come to you.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.