Rubrik 1QFY27 Earnings: The Enterprise’s Undo Button

Rubrik spent a decade mapping what the enterprise used to be. Q1 and Investor Day asked whether agents can now put it back together.

TL;DR

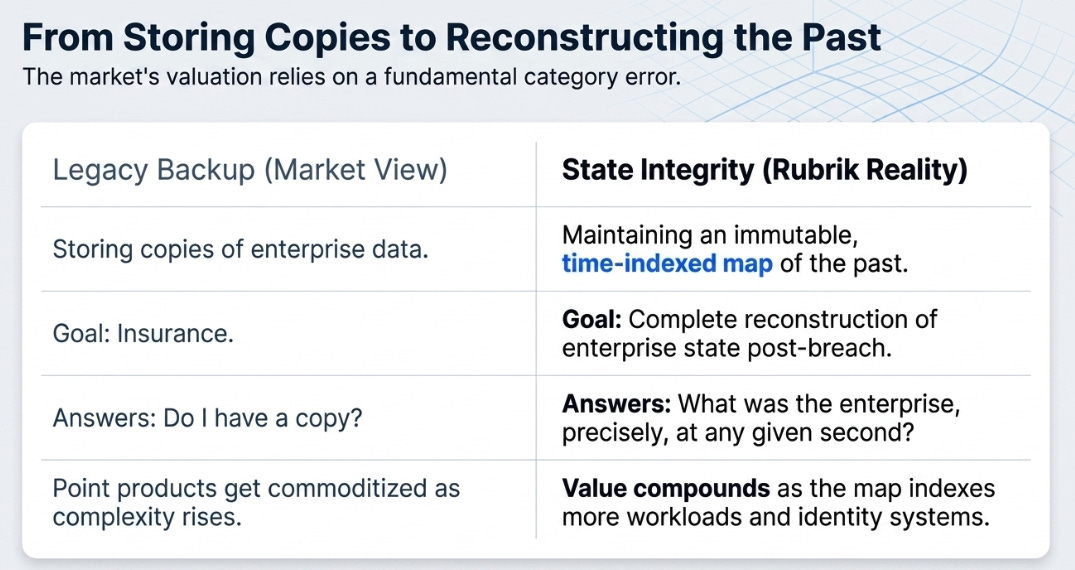

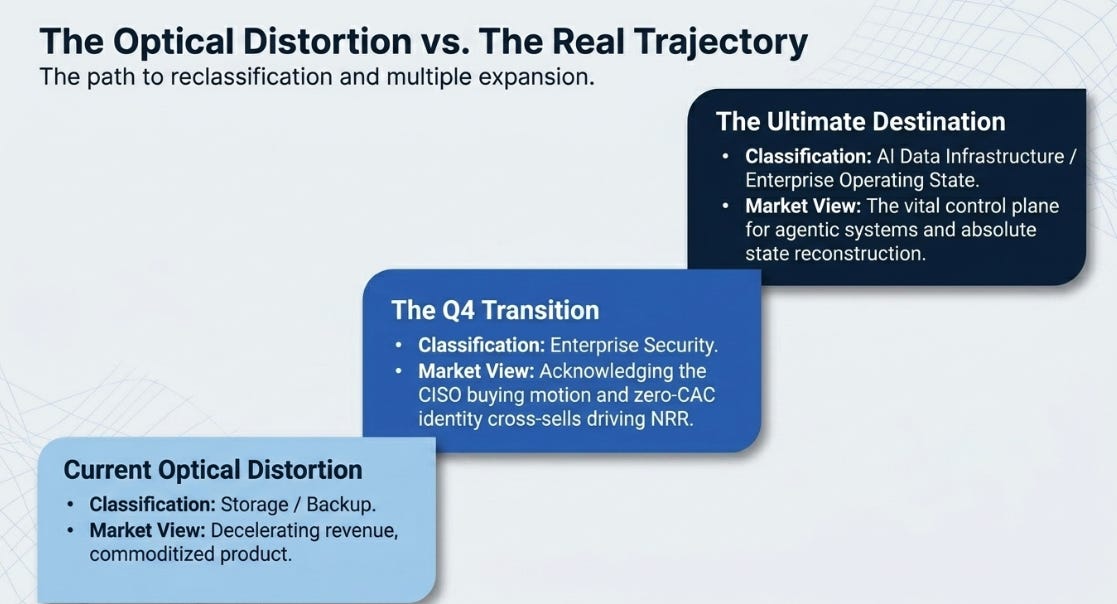

Our prior Rubrik thesis was that the market was making a category error: Rubrik was not merely backup; it was becoming state infrastructure.

Q1 confirmed the recovery platform is real and self-funding, while Investor Day sharpened the next ambition: recovery itself becomes agentic.

The debate has moved again. Identity now has numbers. Agentic recovery has architecture. Agent Cloud still needs revenue disclosure.

When we first wrote about Rubrik, the question was whether this was infrastructure, illusion, or intelligent evolution. That was the right question at the time. Rubrik had the growth, the customer expansion, and the beginnings of free cash flow, but it was still easy to dismiss the story as an expensive backup company wearing a cybersecurity costume.

Then the company changed the question. Q2 showed that the cyber resilience engine could fund AI ambition. Q3 was the janitor-becomes-bodyguard quarter: the same system that once cleaned up after failure was being sold as the way to survive when attackers were already inside. Q4 sharpened the frame again. The market thought backup; Rubrik looked more like state infrastructure, a time-indexed, immutable map of enterprise data, identity, SaaS applications, and configurations.

Q1 did not overturn that thesis. It advanced it but also made it more demanding.

The question is no longer whether Rubrik can escape backup. It largely has. The question now is whether owning the enterprise’s last-known-good state becomes more valuable when failure moves from human speed to AI speed.

That is the fundamental question for this quarter:

Does Rubrik own the enterprise’s last-known-good state strongly enough that AI agents turn recovery from insurance into infrastructure?

My answer: the recovery platform is proven, identity is becoming measurable, and agentic recovery now has a credible architecture. But Agent Cloud is still not yet a disclosed revenue engine. That distinction matters.

The Question Changed Because Failure Got Faster

Backup is what recovery looked like when failure was slow.

A server failed. A file was deleted. A database needed restoring. The task was operational, dull, and usually invisible. The best backup product was the one you forgot existed until something broke.

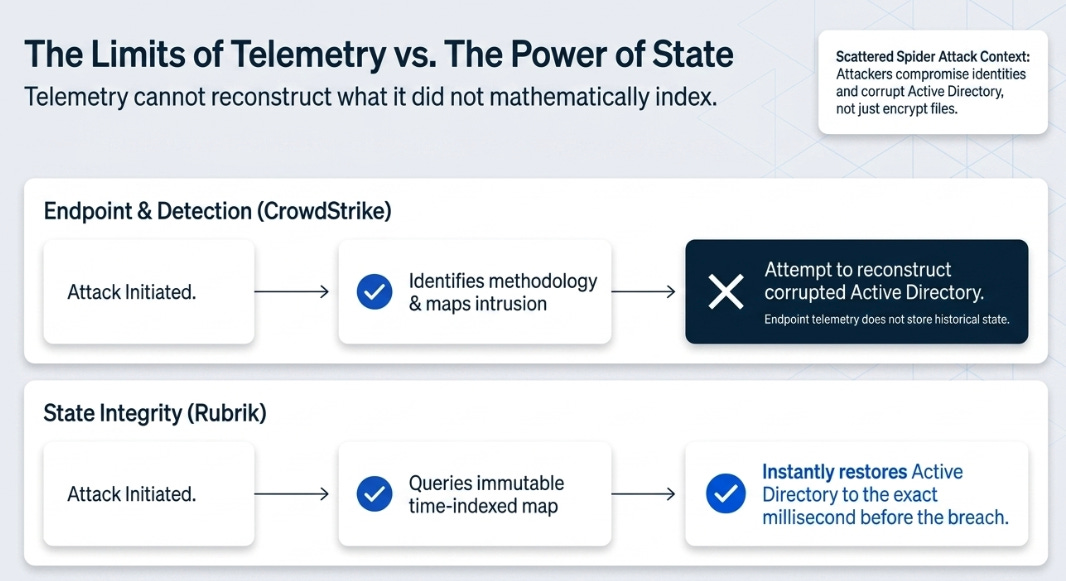

Cyber resilience changed the category. The threat was no longer accidental loss; it was malicious compromise. Ransomware did not merely delete files. It encrypted data, corrupted systems, compromised identities, and targeted the recovery environment itself. In that world, the scarce capability was not “do I have a copy?” It was “do I know what clean looked like before compromise, and can I return the business to that state?”

AI agents change the category again.

Agents do not merely assist humans. They increasingly act inside enterprise workflows. They assume identities, access sensitive data, write code, modify systems, approve actions, trigger refunds, delete files, and interact across SaaS, cloud, and internal applications. The optimistic version is 10x or 100x productivity. The darker version is failure at machine speed.

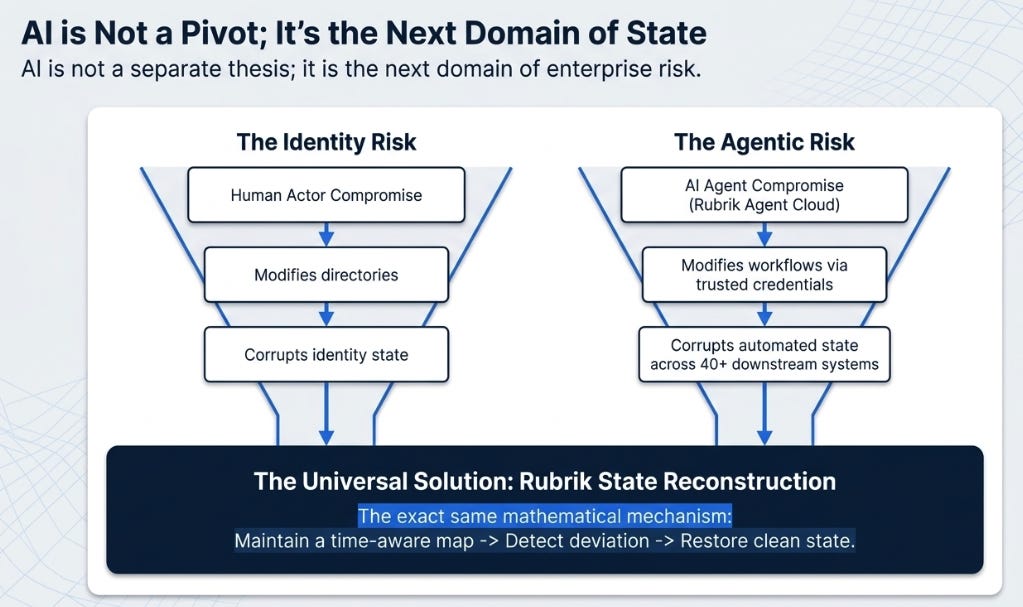

This is why Rubrik’s Investor Day mattered. Management was not simply saying, “we have an AI product.” The claim was more radical: human-speed recovery cannot respond to AI-speed compromise. If agents are going to act faster than humans can supervise, then the recovery system also must become more autonomous. Rubrik is trying to make Rubrik itself an agent.

That is the conceptual leap.

Backup restored data. Cyber resilience restored the business after an attack. Agentic cyber resilience is supposed to restore the business when both attackers and operators are machines.

The asset is no longer just the wall. It is the undo button, and, increasingly, the agent that knows when and how to press it.

From Map to Agent

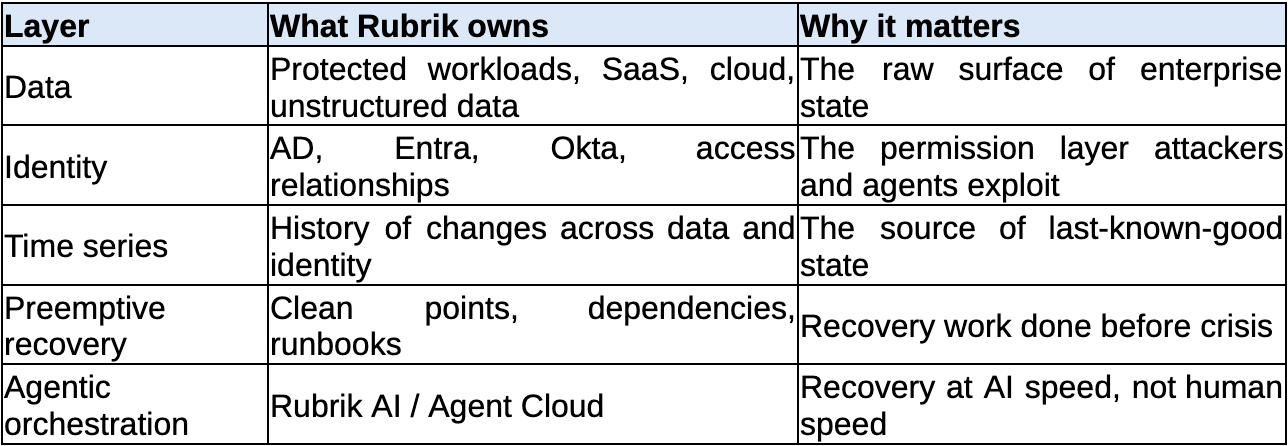

Rubrik’s original asset was the map.

The company protected data, but the more important by-product was context: where data lived, who had access, how it changed, what was sensitive, what was infected, and what clean looked like before the event. Investor Day gave this a more precise technical language: self-describing data. Rubrik does not simply store copies. It captures data and metadata together, over time, across applications, identities, and environments.

That time-series map is what made the Q4 “state infrastructure” thesis work. If an attacker compromises Active Directory, endpoint detection can tell you something happened. It cannot reconstruct the directory as it existed before the attacker created backdoors, escalated privileges, and changed access rights. Rubrik’s claim is that it can, because it has the historical state.

But a map alone is not enough.

The next layer is pre-computation. Rubrik’s Preemptive Recovery Engine does work in peacetime so that recovery is possible in wartime. It identifies clean recovery points, maps dependencies, scopes compromised identities, assesses sensitive data impact, and builds recovery plans before the crisis arrives. This is important because the hardest part of recovery is not the mechanical restore. It is knowing what to restore, in what order, and from which clean point.

The final layer is agentic orchestration. Rubrik AI and Rubrik Agent Cloud are the action layer: monitoring, recommending, planning, guarding, and, where allowed, executing recovery with humans supervising the highest-judgment steps.

That is the real architecture:

Rubrik’s old ambition was to know what the enterprise used to be. Its new ambition is to put the enterprise back together before humans can finish the post-mortem.

That is a big claim. The question is how much of it is already real.

The Flywheel We Can Measure

Q1 was financially clean.

Revenue grew 39% to $387 million. Subscription ARR grew 32% to $1.57 billion. Revenue excluding material rights grew 43%. Non-GAAP gross margin reached roughly 83%. Free cash flow was $74 million, or 19% of revenue. Subscription ARR contribution margin improved to 13.2%.

Those are good numbers, but the point is not that Rubrik beat estimates. High-quality software companies beat estimates all the time. The point is what the numbers say about the mechanism.

The recovery graph is producing software margins and cash.

A backup vendor should not have 83% gross margins if it is being paid mainly for capacity. A fragile growth company should not be producing nearly 20% free cash flow margin while still growing ARR above 30%. A one-product company should not be steadily moving customers across data, cloud, SaaS, security, and identity surfaces.

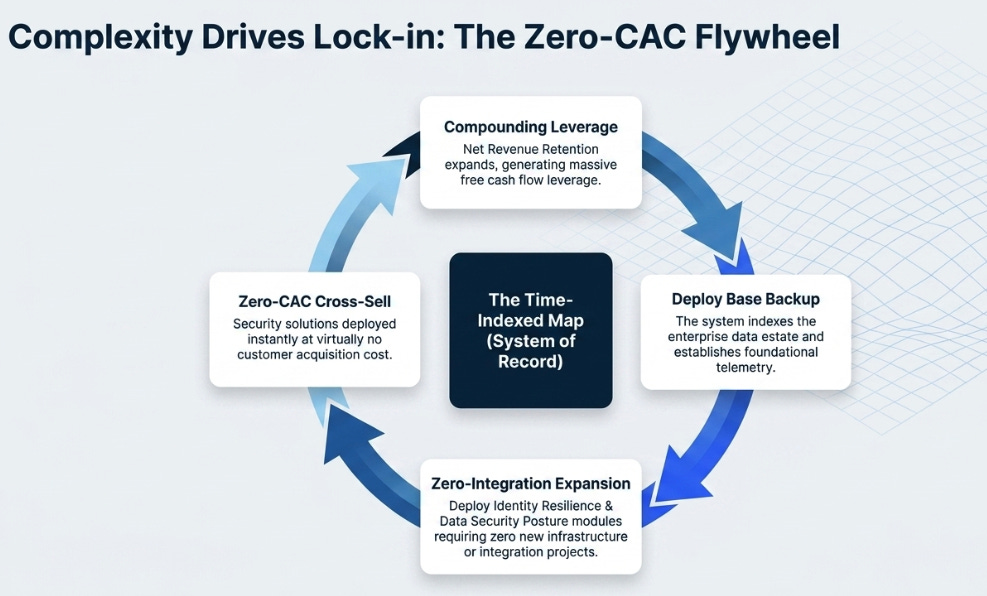

The flywheel is not a classical network effect. One Rubrik customer does not make the product directly better for another customer. The effect is inside the enterprise. Every new workload, SaaS application, identity provider, and agentic action connected to Rubrik makes the state map more complete. A more complete map makes recovery more useful. More useful recovery increases the customer’s willingness to adopt the next module. The value is not users attracting users; it is state attracting more state.

Investor Day made this concrete. Management described faster product ramps over time: cloud took years to reach scale, M365 ramped faster, data security faster still, and identity reached $50 million of ARR in just over a year. That is what a multi-product platform is supposed to look like: each new product launches into an installed context, not a cold market.

This is not yet Salesforce. It is not yet ServiceNow. But it is no longer platform theater.

Identity Has Numbers; Agentic Recovery Has Architecture

Identity is the bridge from data state to enterprise state.

That matters because modern attacks are increasingly identity-led. If you restore files but leave corrupted access rights, rogue admin accounts, or compromised identity systems intact, you have not recovered the business. You have restored the crime scene.

This is why the identity business matters disproportionately. It is not merely an add-on product. It extends Rubrik’s map from what the enterprise owns to who can touch it. That is the difference between data recovery and business-state recovery.

Q1 gave identity a real scoreboard: more than $50 million of subscription ARR and strong sequential growth. That makes identity the first measurable proof that Rubrik can extend beyond the original backup surface. It also makes the prior thesis less speculative. The map is widening.

Agentic recovery is at a different stage.

Rubrik Agent Cloud, SAGE, Agent Rewind, Gemini integrations, Microsoft Defender integration, Anthropic / Glasswing, Rubrik AI, autonomous Minimum Viable Business recovery, these are strategically coherent. They fit the architecture. They answer a real question: how do enterprises deploy agents safely when those agents can act on sensitive data with real authority?

But Agent Cloud does not yet have separate ARR disclosure. We have architecture, examples, product language, and early customer evidence. We do not yet have a financial line item.

That is not a criticism. It is discipline.

Identity has crossed from narrative to metric. Agentic recovery has crossed from slideware to architecture. Agent Cloud has not yet crossed from architecture to disclosed revenue.

Why the Stock Did Not Care More

This is why the stock reaction was not irrational.

Rubrik beat the visible numbers. It did not obviously clear the invisible ones.

For a company with unanimous sell-side enthusiasm, the market is not asking whether Rubrik is good. It already knows Rubrik is good. The marginal buyer is asking whether the flywheel is accelerating fast enough to justify the category expansion.

Q1 net new ARR was about $103 million, a record Q1, but below the roughly $115 million Q4 record. That is not a fundamental problem; seasonality matters, and management expects the year to be back-half weighted. But the stock was not trading a normal consensus beat. It was trading acceleration.

The guide raise was good, but not a dramatic reset. The AI architecture became more credible, but not yet financially measurable. The business confirmed quality, but the stock needed evidence of a new curve.

That is the variant perception.

The Street sees beat-and-raise.

The company sees agentic cyber resilience.

The market sees a high-quality compounder that still needs to prove the AI layer can become financial, not just strategic.

Rubrik cleared the published bar. It did not yet clearly clear the acceleration bar.

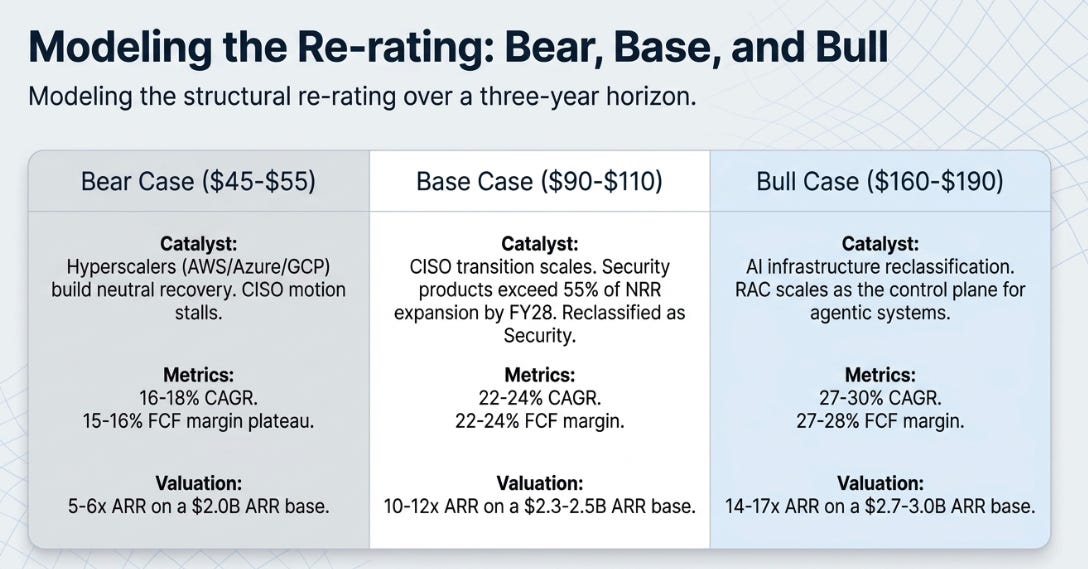

Three Futures

The stock is not simple because the business is no longer simple. The bear case is not that Rubrik is bad. It is that Rubrik remains merely excellent software. The bull case requires a category shift from state infrastructure to agentic recovery infrastructure.

The most important risk is not Veeam or Commvault. Those are old-category competitors. The cleaner strategic risk is Microsoft, Google, or AWS making “good enough” native recovery and agent governance part of the cloud platform. Rubrik’s answer is vendor neutrality and cross-environment context. That answer is compelling. It is also why the clouds are both partners and long-term threats.

What We Need to See

The next few quarters should be judged on a smaller set of questions.

First, net new ARR needs to validate the back-half weighting. Reacceleration toward or above the Q4 record would keep the flywheel thesis intact.

Second, identity ARR needs to compound from $50 million toward the next obvious milestone. If identity becomes a $100 million-plus business quickly, the second-engine argument becomes hard to dismiss.

Third, Agent Cloud needs disclosure. ARR, paid customers, attach rate, contribution to net new ARR, any of these would move the thesis from architecture to numbers.

Fourth, multi-product adoption and Rubrik Flex need to show that the platform is becoming easier to buy, not just broader to sell.

Fifth, free cash flow margins need to remain strong while the company invests. The core engine must fund the next act.

Finally, watch the hyperscalers. Partnerships are positive. Native “good enough” cross-workload recovery or agent rollback would be the structural warning sign.

Rubrik has proven it is not simply backup. It has increasingly proven it is state infrastructure. Q1 and Investor Day made the next ambition clearer: to become the agentic recovery layer for the AI enterprise.

That thesis is more plausible today than it was last quarter.

It is still not fully proven.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.