Rubrik’s 4QFY26: The Market Thinks It’s Backup. It’s Actually State Infrastructure

A record quarter confirmed Rubrik’s transition from data storage to enterprise state integrity, yet the stock trades like a slowing backup vendor.

TL;DR

Q4 proved the shift is real: identity recovery is exploding (400 → 900 customers) and security now drives nearly half of expansion revenue.

Rubrik’s moat is architectural: it maintains a time-indexed map of enterprise state, something detection vendors and hyperscalers cannot easily replicate.

The opportunity is a category error: the market values Rubrik like storage while the business is compounding like security infrastructure.

In our last piece, we called Rubrik the janitor who became the bodyguard. The janitor spent a decade storing copies of enterprise data as insurance, unremarkable work, mostly invisible, occasionally essential. The bodyguard, we argued, was emerging: the same immutable data archive that powered backup was becoming the only mathematical way to restore a business to the exact second before a breach. The mechanism was right. What Q4 revealed is that we were describing a transition that was already further along than we knew, and asking a question that Q4 has now largely answered, which means the interesting question has moved.

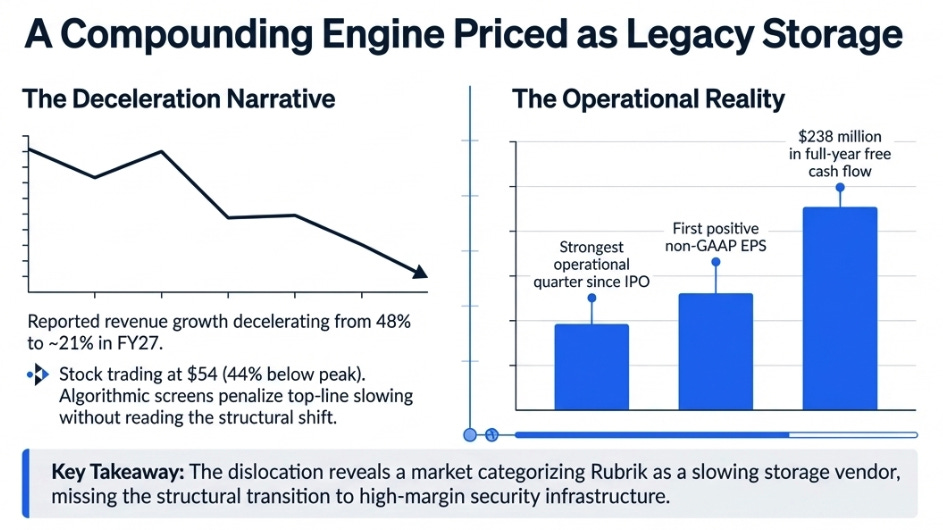

The market, meanwhile, is arguing about a different question entirely. Rubrik reported its strongest operational quarter since going public, record net new ARR, first positive non-GAAP EPS, $238 million in full-year free cash flow, and the stock sits at $54, 44% below its peak. The explanation is not complicated: reported revenue growth will decelerate from 48% to roughly 21% in FY27, and algorithmic screens do not read footnotes. But the explanation, while accurate, is not the point. The point is what the dislocation reveals about how the market is categorizing this company, and why that categorization is wrong in a way that matters for the next three years.

The Wrong Category

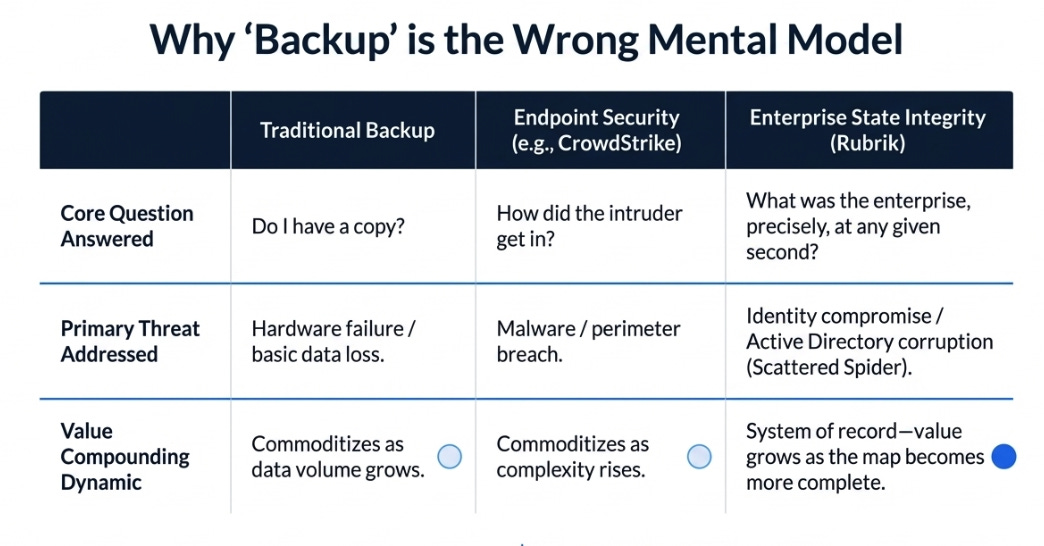

Backup is about storing copies. That is what Rubrik was built to do and what most investors still think it does. The market’s mental model has updated to “backup company with a security story,” which is better than “backup company” but still wrong in a structural sense.

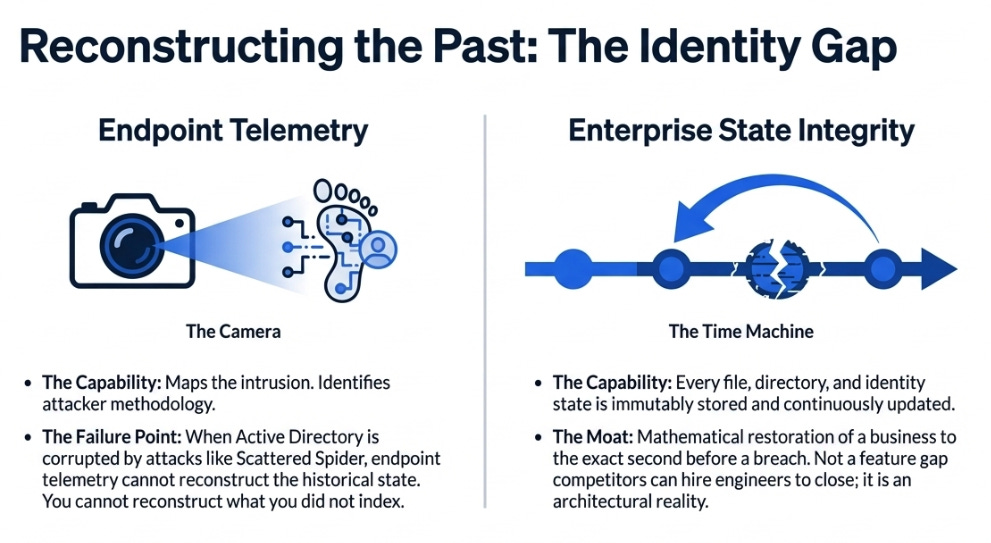

What Rubrik actually maintains is an enterprise’s relationship with its own past. Every file, every directory, every identity state, every configuration, indexed, immutably stored, continuously updated, queryable across time. This is not semantically equivalent to backup. Backup answers “do I have a copy?” Rubrik’s system answers “what was the enterprise, precisely, at any moment in its history?” The distinction sounds philosophical until you understand what cyber attacks actually target.

The Scattered Spider attacks that have dominated enterprise security discussions over the past two years did not encrypt files. They compromised identities, corrupted Active Directory, and locked administrators out of the systems they needed to respond. CrowdStrike can tell you this happened. It can identify the attacker’s methodology and map the intrusion. What it cannot do is reconstruct the Active Directory as it existed before the attack, because endpoint telemetry does not store the historical state of the enterprise. Rubrik does. This is not a feature gap CrowdStrike can close by hiring more engineers. It is an architectural reality: you cannot reconstruct what you did not index.

The shift from perimeter defense and endpoint detection to identity-based attacks and assumed breach means the scarce capability in enterprise security is no longer detecting what happened, it is knowing what the enterprise used to be and being able to get back there. That is a different product category than backup, and it is a different product category than traditional cybersecurity. It is, for lack of an established term, state integrity. And Rubrik is the only company with the architecture to own it at enterprise scale.

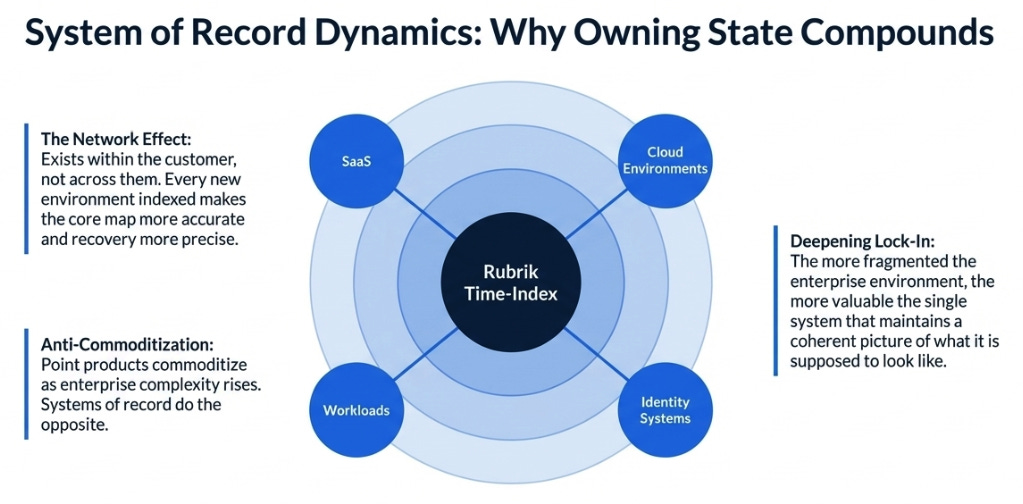

Why Owning State Compounds

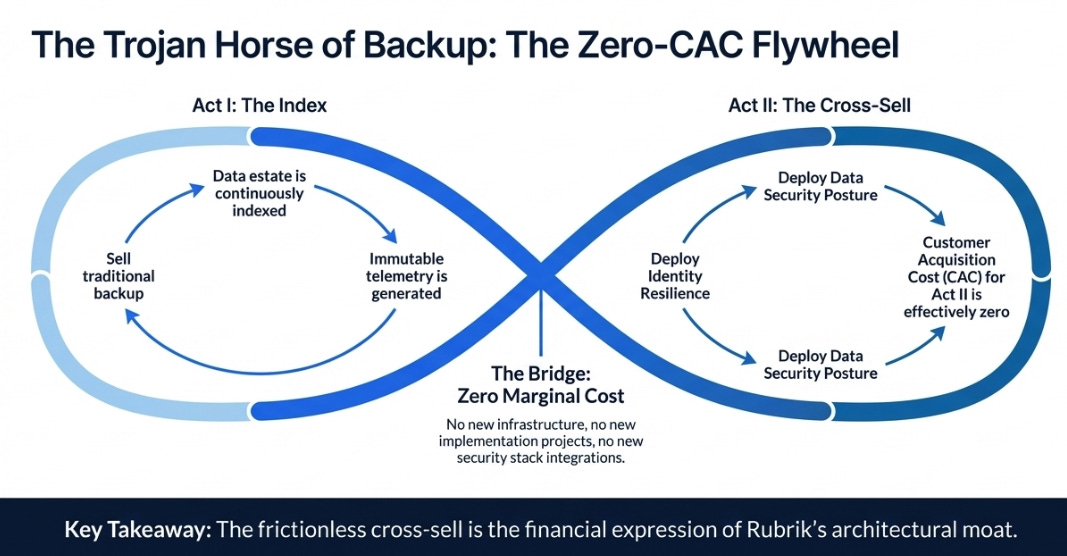

The reason this matters beyond a single product category is that Rubrik’s value grows with the completeness of its map. Every additional workload, identity system, SaaS application, and cloud environment that Rubrik indexes makes its map more accurate, its recovery more precise, and its governance more relevant. This is a network effect, not across customers, but within them. Each enterprise Rubrik serves becomes a progressively more locked-in customer not because switching costs are high in the traditional sense, but because the value of the map grows with its coverage.

This is the structural dynamic that the “backup company” frame misses entirely. Point products get commoditized as complexity rises, the more fragmented the enterprise environment, the harder it is for any single security tool to maintain relevance. System-of-record products do the opposite. The more fragmented the environment, the more valuable the system that maintains a coherent picture of what that environment is supposed to look like. Rubrik gets stronger as enterprises get more complex. That is not true of most software companies, and it is certainly not true of backup vendors.

The zero-marginal-cost cross-sell is the financial expression of this dynamic. Once Rubrik has indexed an enterprise’s data estate, which happens in the course of selling backup, deploying an identity resilience module or a data security posture product requires no new infrastructure, no new implementation project, no new security stack integration. The telemetry already exists. The customer acquisition cost for Act II is, in the limit, zero. This is why $238 million in free cash flow is not an aberration. It is what the Trojan Horse looks like when it opens.

Q4 as Proof, Not Update

We argued in prior pieces that identity and security products were the plausible next adjacency. Q4 closed that debate.

Identity customers grew from 400 to more than 900 in a single quarter, the fastest product growth in company history. More importantly, 40% of those new identity customers were net-new logos: enterprises that came to Rubrik specifically for identity recovery, not as a cross-sell from backup. That means the CISO buying motion is real and it is self-sustaining. Rubrik is winning in security evaluations against security vendors, on security criteria, in the security budget. Security products now account for more than 45% of net revenue retention expansion, up from 34% a year ago and from essentially zero three years prior.

These are not incremental data points. They are evidence that the compounding mechanism has activated beyond backup. The map is extending into identity. The zero-CAC cross-sell is working. The buyer has shifted. When we said the janitor was becoming the bodyguard, we were describing a hypothesis. Q4 makes it a fact.

The deferred revenue balance makes the durability concrete: $1.845 billion in contracted, already-signed revenue against $1.316 billion in trailing twelve-month revenue. The pipeline covers more than a year of recognized revenue with zero new bookings. Rubrik’s contracted future is larger than its recent past. That is not a statistic you associate with a category in decline.

The FCF as Fingerprint

There is a precise financial signature for a company whose second act is monetizing infrastructure it built in its first act at near-zero marginal cost. Revenue grows at a meaningful pace. Free cash flow grows much faster. Margins expand structurally rather than cyclically. The GAAP-to-non-GAAP reconciliation narrows as stock-based compensation normalizes.

Rubrik’s FY26 financials are this fingerprint. Full-year free cash flow of $238 million on $1.316 billion in revenue, an 18% FCF margin, against $22 million and 2% in FY25. ARR contribution margin swung from negative 12% in FY24 to positive 12% in FY26. Non-GAAP EPS turned positive in Q4 for the first time. These are not the numbers of a backup vendor straining to grow. They are the numbers of a platform in the early innings of a compounding expansion loop.

The one caveat worth stating clearly: FY27 free cash flow guides to only $265-275 million, or roughly 14% growth despite the structural leverage. Management is investing the incremental dollar rather than dropping it to cash, capex tripled in Q4. That is not a red flag, but it warrants watching. The question is whether the investment is building capacity for the next S-curve or filling gaps in the existing one.

AI Is Not the Thesis. It Is the Destination of the Same Mechanism.

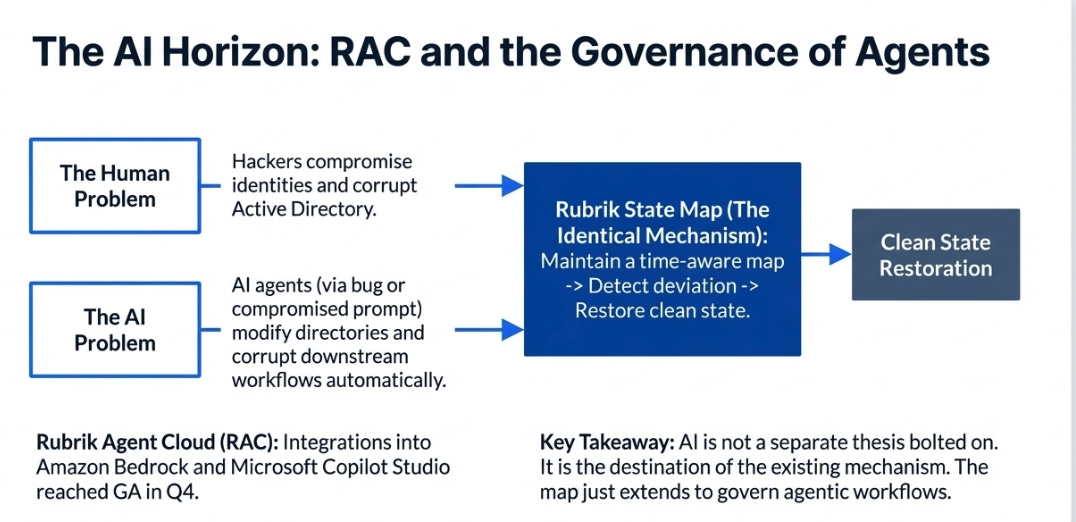

Rubrik Agent Cloud reached general availability in Q4 with integrations into Amazon Bedrock and Microsoft Copilot Studio. No paying customers were disclosed. The AI chapter is not open yet.

But understanding why RAC exists matters for understanding what Rubrik is becoming. AI agents access data, modify directories, and make decisions inside production environments with trusted credentials. When one behaves incorrectly, through a bug, a compromised prompt, a misconfigured policy, the damage is not a file. It is a workflow. It might propagate across forty downstream systems before anyone notices. The enterprise needs to know what state it was in before the agent acted, and it needs to be able to get back there.

This is the same problem Rubrik already solves for human attackers who compromise identities. The mechanism is identical: maintain a time-aware map of enterprise state, detect deviation, restore clean state. The only difference is the actor, human versus agent. RAC is not a new thesis bolted onto Rubrik’s platform. It is the existing mechanism applied to the next domain of enterprise risk.

That is why AI is the destination rather than a separate bet. The same architecture that makes Rubrik valuable for identity recovery makes it valuable for agent governance. The map just needs to extend. And the more the enterprise deploys AI agents, the more complete and more valuable the map becomes. This is the loop extending into its next iteration.

What It Is Worth

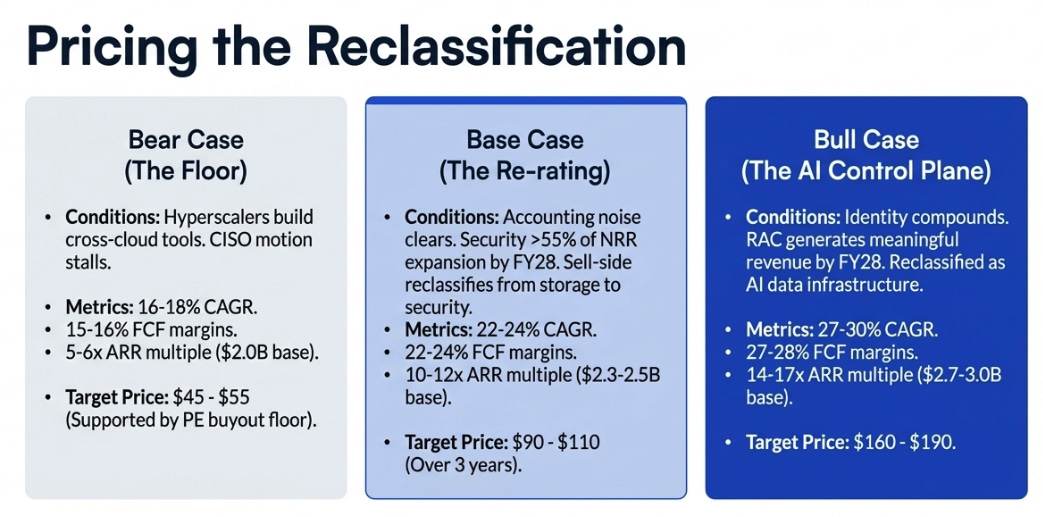

The market is pricing RBRK at roughly 7x forward ARR as a decelerating backup vendor. The question is which misperception clears first, and when.

In the bear case, it never does. Cloud providers, AWS, Azure, GCP, build credible cross-cloud identity recovery and governance tools that enterprises accept as good enough. The CISO buying motion stalls. Rubrik remains a premium recovery company with excellent economics but a capped multiple. Revenue grows at a 16-18% CAGR through FY29, FCF margins plateau at 15-16%, and the stock trades at 5-6x ARR on a $2.0 billion ARR base. Call it $45-55. It is still a fine business. Private equity notices at this price. That creates a floor, not a recovery.

In the base case, the accounting noise clears, the CISO transition continues, and identity becomes a scaled second engine. Security products exceed 55% of NRR expansion by FY28. Revenue grows at a 22-24% CAGR. FCF margins expand toward 22-24% as the cross-sell loop matures. The multiple re-rates from 7x to 10-12x ARR as sell-side analysts are forced to reclassify the company from storage to security. On a $2.3-2.5 billion ARR base at those multiples, the stock reaches $90-110 over three years.

In the bull case, identity continues compounding and AI begins contributing. RAC generates meaningful revenue by FY28. The company gets reclassified not as security but as AI data infrastructure, the control plane for enterprise operating state in a world of agentic systems. Revenue grows at a 27-30% CAGR. FCF margins approach 27-28%. The multiple expands to 14-17x ARR on a $2.7-3.0 billion ARR base. The stock reaches $160-190.

The base and bull cases are not dependent on management executing perfectly. They are dependent on the mechanism being real, which Q4 confirmed, and on the market eventually valuing it correctly. The bear case is dependent on hyperscalers solving a problem that runs counter to their incentives: vendor-neutral, cross-cloud recovery that works as well on AWS as on Azure as on GCP. Their incentive is lock-in. Rubrik’s value proposition is the opposite.

What to Watch

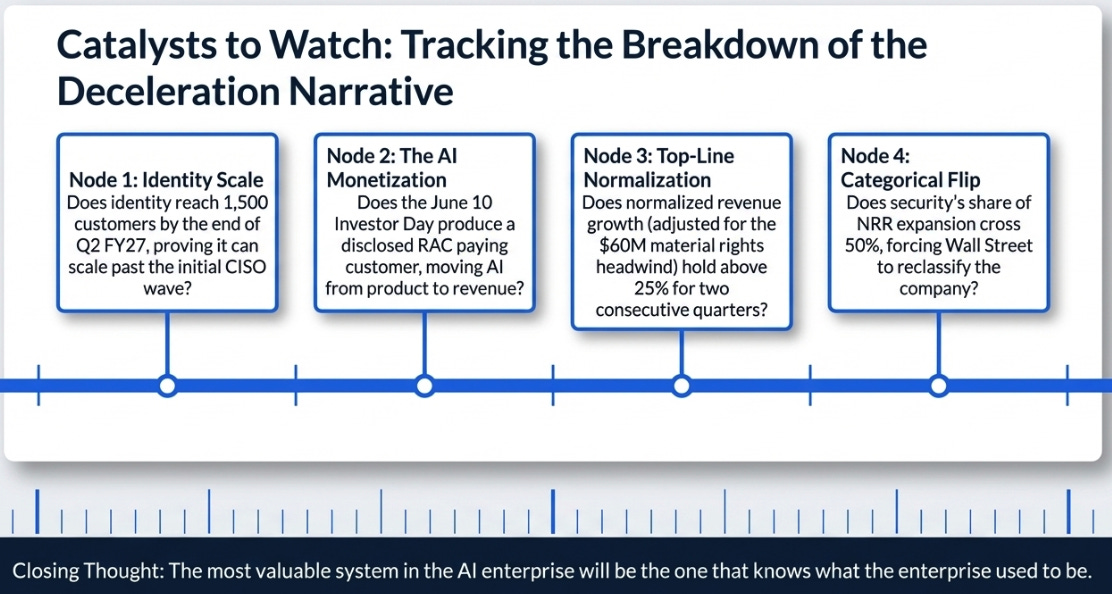

Four questions will determine which scenario unfolds. Does identity reach 1,500 customers by the end of Q2 FY27, or does it plateau after the initial CISO wave? Does the June 10 Investor Day produce a disclosed RAC paying customer, or does AI remain a product without revenue? Does normalized revenue growth, adjusted for the $60 million material rights headwind, hold above 25% for two consecutive quarters, collapsing the deceleration narrative? And does security’s share of NRR expansion cross 50%, forcing a categorical reclassification?

The answers will arrive over the next four to six quarters. The optical distortion will make every quarter look like deceleration to anyone reading headlines. That gap, between what the screener sees and what the mechanism is doing, is the opportunity.

The most valuable system in the AI enterprise may turn out to be the one that knows what the enterprise used to be. Rubrik spent a decade building that system while the market thought it was building backup. Q4 was the quarter the system proved it extends beyond backup. The question now is not whether that matters. It is how large the surface area becomes.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.