Saab 4Q25 Earnings: The Fighter Jet Nobody Wanted

Saab spent 30 years building Europe’s sovereignty stack. The market just showed up.

TL;DR:

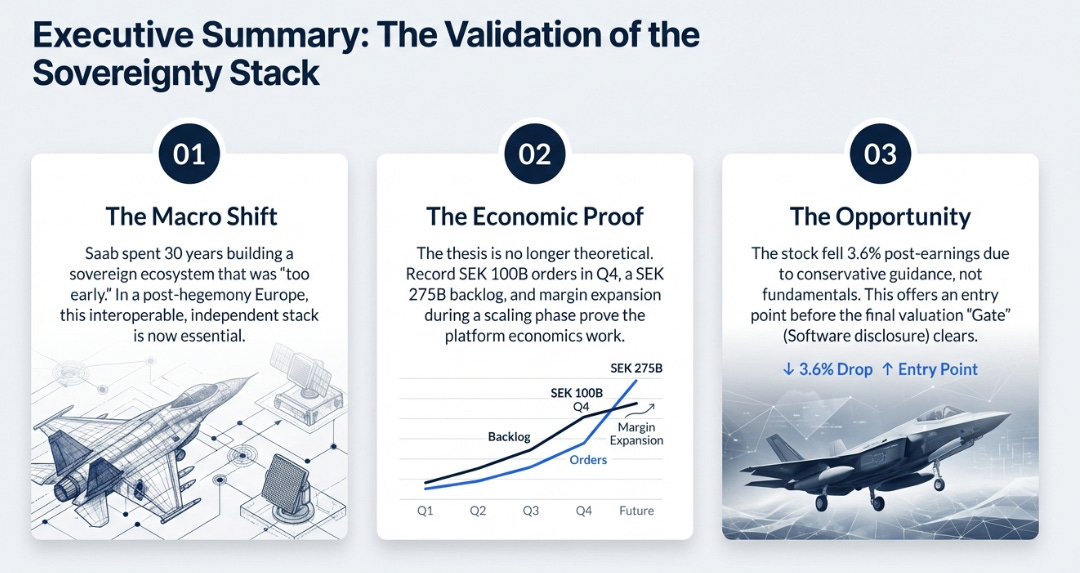

Saab was early, not wrong: the company spent three decades building an affordable, interoperable, sovereign defense ecosystem that only makes sense in a post-American-hegemony Europe, and that world has finally arrived.

This quarter proved it economically: record SEK 100B orders, SEK 275B backlog, and continued margin expansion show Saab is scaling a platform, not just shipping hardware.

The stock fell because the story isn’t finished: execution and megadeals are largely clearing; software disclosure at CMD is the last gate between “expensive defense stock” and “European defense platform.”

In 1993, Saab rolled out the Gripen, a lightweight, single-engine fighter jet designed by a neutral country of 9 million people. The Western defense establishment was politely uninterested. The Americans had the F-16. The French had the Mirage, and later the Rafale. The British and Germans were building the Eurofighter. Why would any self-respecting air force buy a Swedish fighter?

The answer, for nearly two decades, was that they wouldn’t. Saab’s export campaigns failed with dispiriting regularity through the 1990s and 2000s. The one meaningful win, South Africa, was mired in corruption scandals. The Czech Republic leased Gripens rather than bought them, which is the procurement equivalent of being asked to prom as a friend. Meanwhile, Saab’s car division went bankrupt in 2011, and the defense side was widely regarded as a subscale Nordic niche player building clever equipment for a country that wasn’t even in NATO.

Fast-forward to February 2026. Saab just reported SEK 100 billion in order bookings in a single quarter. Colombia bought Gripen. France bought GlobalEye. Poland selected Saab’s submarines. Ukraine signed a letter of intent for fighters. Canada is in discussions. The backlog stands at SEK 275 billion. The company that nobody took seriously is now the fastest-growing major defense company in the West.

What changed wasn’t Saab, it was the world. Saab spent three decades building exactly the kind of defense ecosystem that a post-American-hegemony Europe now desperately needs: affordable, interoperable, sovereign, and not dependent on Washington’s goodwill. The Gripen wasn’t too small or too Swedish. It was too early. Sweden’s insistence on doing everything itself, fighters, submarines, radar, missiles, electronic warfare, looked like stubbornness when America was the assumed guarantor of European security. It looks like foresight now that European nations have been told, in no uncertain terms, to take care of themselves.

That’s the story. Now let me show you what this quarter says about whether the world has truly caught up to what Saab built.

On to the Update:

The Best Quarter Nobody Rewarded

From Bloomberg:

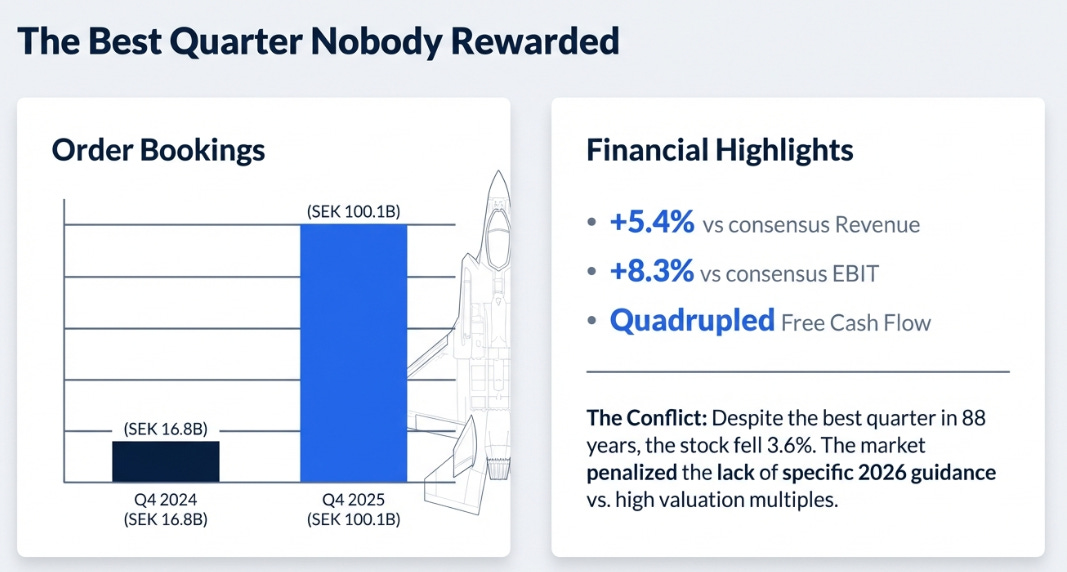

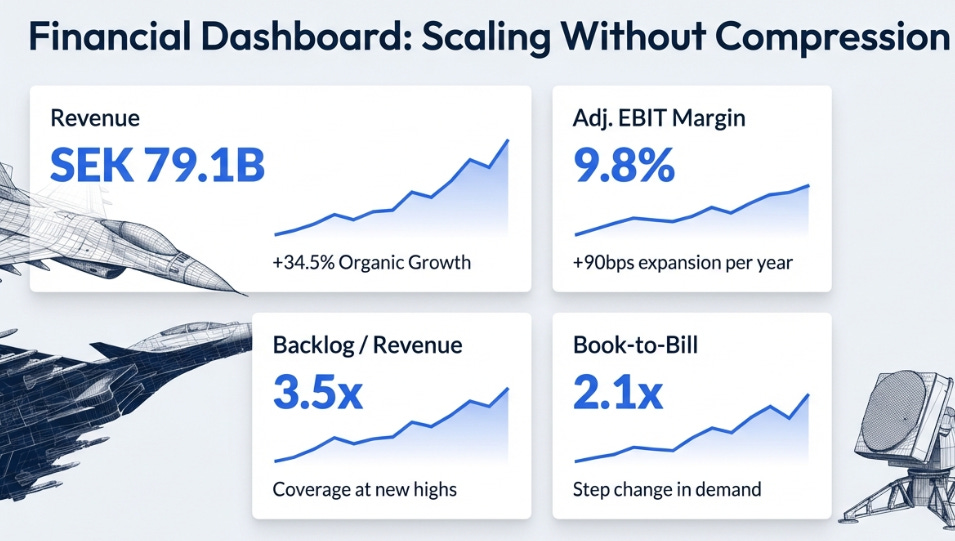

Swedish defense group Saab AB reported fourth-quarter revenue of SEK 27.7 billion, beating analyst estimates of SEK 26.3 billion, driven by a surge in order bookings to SEK 100.1 billion, the highest quarterly intake in the company’s history. Organic growth of 34.5% and adjusted operating profit of SEK 2,925 million both exceeded consensus. For the full year, Saab reported revenue of SEK 79.1 billion, adjusted EBIT of SEK 7,730 million, and free cash flow of SEK 4.2 billion. The company raised its medium-term organic growth CAGR to approximately 22% from 18%. Shares initially rose 4.6% before reversing to close down 3.6%.

I want to sit with that last sentence. The best quarter in 88 years of corporate history, and the stock fell. Revenue beat by 5.4%. Profit beat by 8.3%. Orders were nearly six times the year-ago quarter. Free cash flow quadrupled. And investors sold.

The reason is simple: at 48 times trailing earnings, you don’t get credit for what you did, you get judged on what you promise. And CEO Micael Johansson, in a move that I think is strategically deliberate but that the market found infuriating, promised almost nothing. The growth upgrade to ~22% was already consensus. No 2026 margin guidance. No extension of targets beyond 2027. When pressed, Johansson was blunt:

“You won’t get sort of a specific number or a range or anything. You have to unfortunately live with the guidance that we’ve given on growth of EBIT.”

Compare this to Rheinmetall’s Armin Papperger, who gives investors margin targets, product-level breakdowns, and multi-year profitability roadmaps. Papperger tells you where the destination is. Johansson tells you to enjoy the drive. At 15 times earnings, that’s charming. At 48 times, it’s a problem.

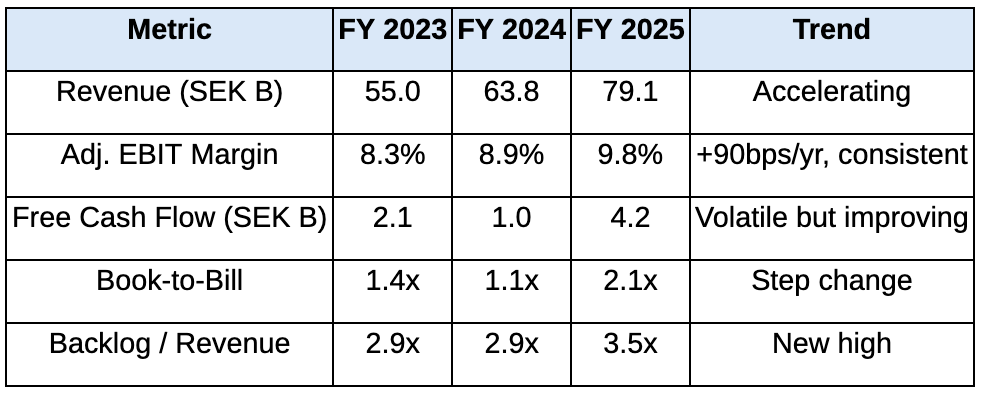

The trend I keep returning to is the margin line. Ninety basis points of expansion per year, for three consecutive years, during a period of 20-25% revenue growth. Defense companies are not supposed to do this. When you scale a project-based business this fast, hiring thousands, ramping new programs, managing larger and more complex contracts, margins typically compress. Saab’s are expanding. That tells you something about the nature of the revenue being added.

What the Sell-Side Sees vs. What’s Actually Happening

The market sees an expensive defense contractor that delivered a great quarter but won’t guide on margins. I think this misses three things.

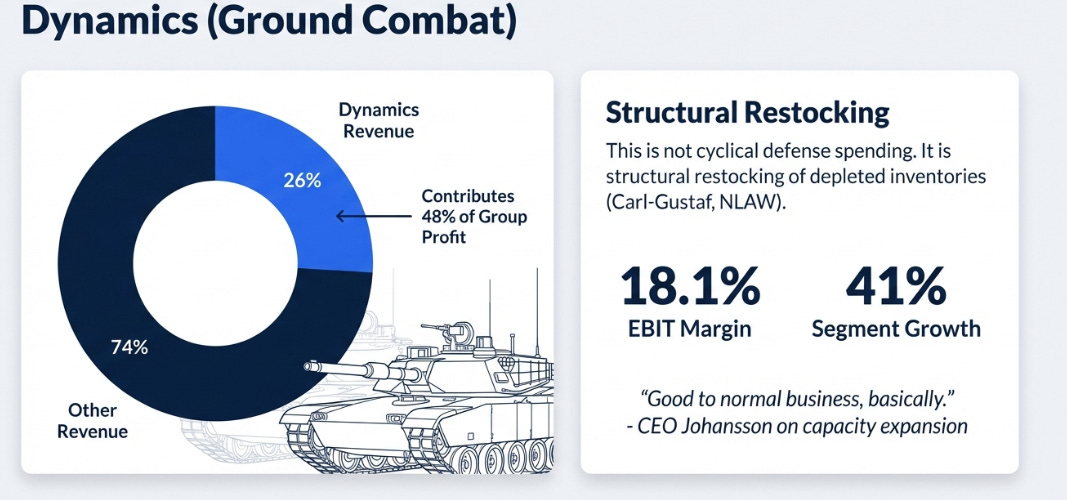

First, Saab’s ammunition and ground combat business, called Dynamics, is not a typical defense segment. It grew 41% last year with an 18.1% EBIT margin. It now contributes 48% of group operating profit on just 26% of revenue. The backlog is SEK 90 billion. And the demand is not discretionary. Carl-Gustaf recoilless rifles, AT4 anti-tank weapons, RBS 70 air defense missiles, NATO countries must continuously replenish these. European inventories were depleted by decades of underinvestment and then by transfers to Ukraine. The restocking cycle is structural, not cyclical. When asked whether new factories in Michigan and India would disrupt profitability, Johansson was almost dismissive: “Good to normal business, basically.” He’s telling you this isn’t a growth phase, it’s a steady state at 18% margins.

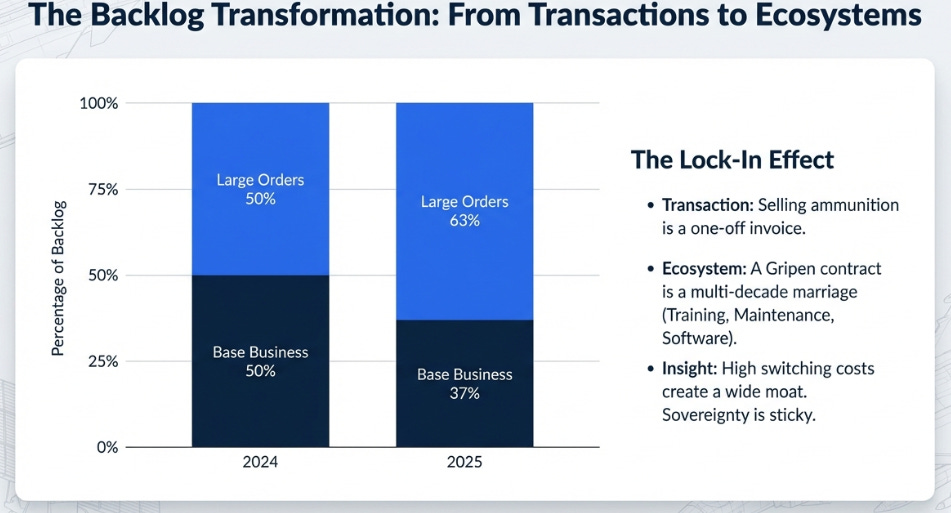

Second, the backlog changed in kind, not just size. Large orders, Gripen fighters, GlobalEye surveillance aircraft, A26 submarines, comprised 63% of 2025 bookings, up from 50% in 2024. An ammunition order is a transaction: it ships, you invoice, you need another order. A Gripen contract with Colombia is a multi-decade relationship: training, maintenance, software updates, spare parts, and a political commitment that makes switching to another fighter effectively impossible. The pilots train on it. The ground crews specialize in it. The electronic warfare libraries, the sensor fusion, the weapons integration, all of it is Saab’s. Switching costs aren’t just financial; they’re generational. The backlog isn’t a number. It’s a measure of how many countries have made Saab their sovereign choice.

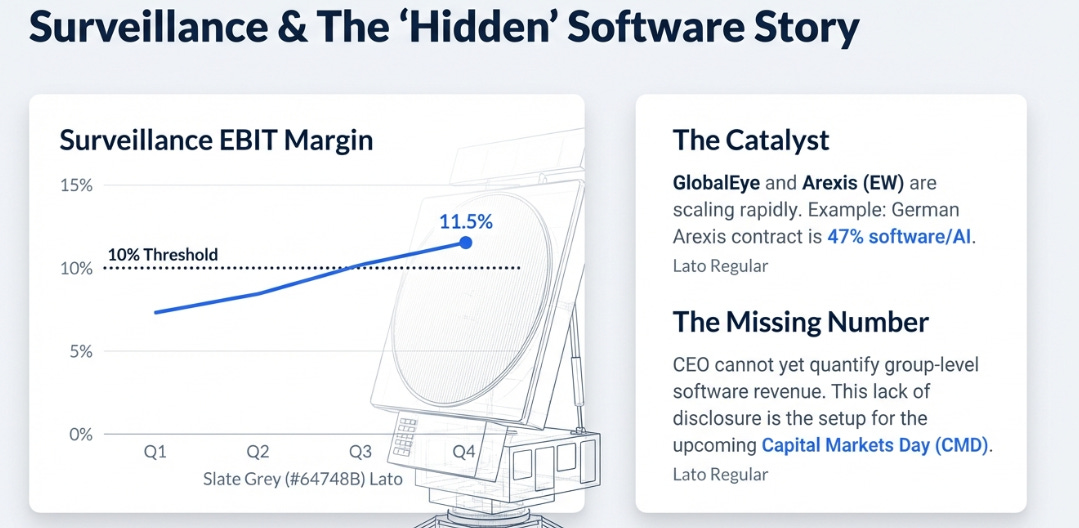

Third, Surveillance, Saab’s largest segment, crossed a margin threshold I’ve been watching. Adjusted EBIT went from 8.9% to 10.0% for the year, with Q4 hitting 11.5%. This happened while loss-making legacy contracts are still being cleaned up:

“We have taken steps to either mitigate loss-making business or making sure that we have a crossroad decision on whether that business should be within Surveillance or not. But we’re not done yet.”

“Crossroad decision” is polite Swedish for “we’re going to divest or shut it down.” He’s telling you 10% is the floor. With GlobalEye and the Arexis electronic warfare system (where 47% of a recent EUR 549 million German contract was software and AI) both scaling, 11-12% is realistic once the cleanup is done.

The thesis isn’t without complications. The T-7 trainer program with Boeing got worse, profitability pushed to 2028-2029, from a previous expectation of mid-2027. Aeronautics is posting a 6.2% margin despite 15% revenue growth, the entire Gripen improvement is being consumed by T-7 losses. And the software question remains open: when asked to quantify group-level software revenue, Johansson said “I can’t do that today.” Not “it’s immaterial.” He can’t do it today. I believe this is staging for a Capital Markets Day disclosure, but until that day comes, the most important number for the thesis doesn’t exist.

Where Our Thesis Stands, What Changed and What Didn’t

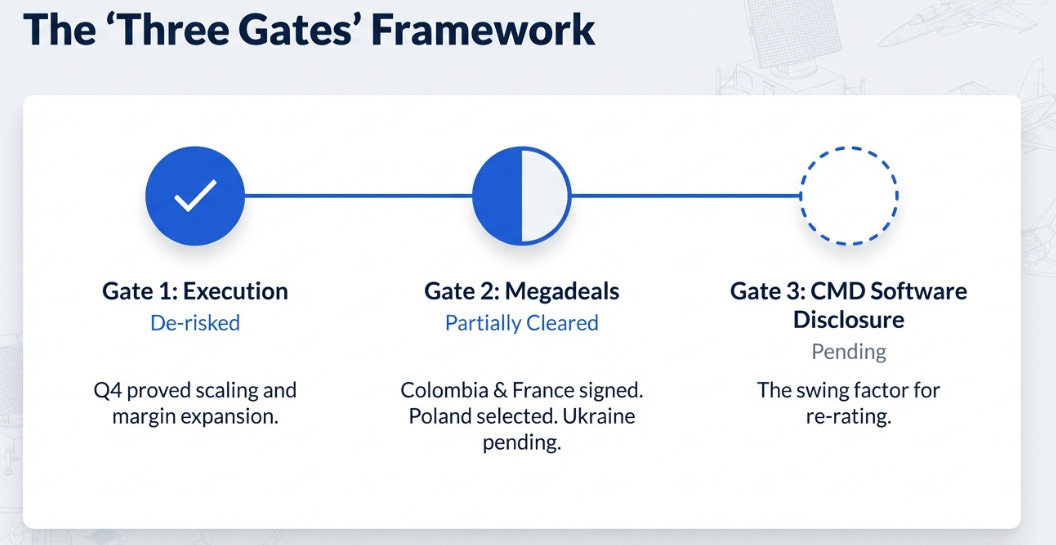

In November, after the Arexis contract made the software economics visible for the first time, I laid out three gates that would determine whether this story works: the CMD software disclosure, mid-2026 execution evidence, and megadeal conversion. Here’s where we are.

Gate 2, execution, is substantially de-risked. Q4 showed Saab can convert a massive backlog into revenue at scale while expanding margins. Not fully cleared, 2026 will be the real test with new factories and thousands of hires, but the trajectory is right.

Gate 3, megadeals, is partially cleared. In November, Poland, France, and Colombia were all still in various campaign stages. Today, Colombia is signed. France is signed. Poland is selected and Johansson expects the ~SEK 30 billion contract to be finalized this year. Ukraine and Canada remain unsigned, but the backlog is already SEK 275 billion without them.

Gate 1, the CMD software disclosure, remains the swing factor. This is the one that determines whether Saab re-rates or stays range-bound.

The honest assessment is that the fundamentals are materially better than in November across almost every dimension, backlog up 47%, margins expanding, free cash flow inflecting, sovereign lock-in deepening with each signed contract, while the stock has moved only modestly. The risk/reward has improved. Here’s how I think about the scenarios now:

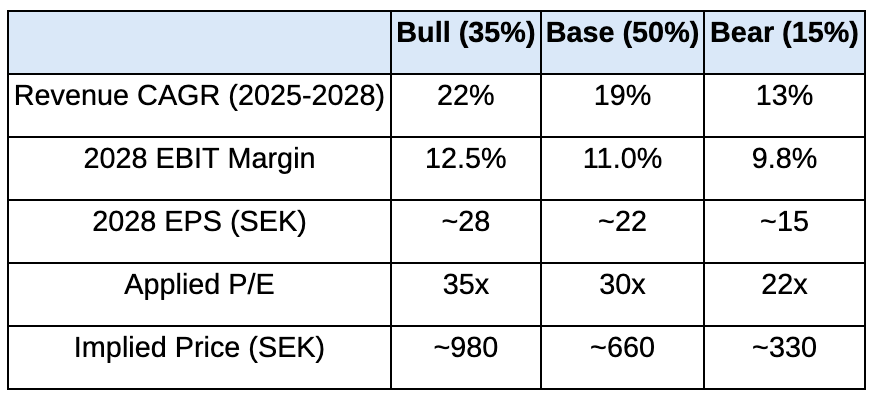

Two things changed from November. First, I nudged the bull probability from 30% to 35% because two of three gates have partially cleared, that’s evidence, not hope. Second, and more importantly, the bear case floor moved up. In November I had SEK 450-500 as the downside; I’m now at ~330 using 2028 numbers. But the real floor is higher than the math suggests, because the locked-in backlog, SEK 275 billion of contractual commitments, with 79% of 2026 revenue already covered, means Saab doesn’t deserve a commodity defense multiple even in the downside. An 18x P/E on depressed earnings ignores that France, Colombia, and Sweden are already embedded in Saab’s ecosystem and aren’t leaving. A 22x floor multiple reflects that structural reality.

The probability-weighted expected value is roughly SEK 680, about 27% above current. This isn’t a screaming buy. But it’s a favorable skew, and the confidence behind the base case is meaningfully higher than it was three months ago because we now have Q4 data confirming the trajectory rather than extrapolating from Q3.

What the Gripen Story Tells You

In 1993, Saab was building a fighter jet for a country too small and too neutral to need one. The export campaigns failed because the world didn’t want what Saab was selling. What Saab was selling was sovereignty, the ability to operate a complete defense ecosystem without depending on a superpower’s supply chain, technology transfer restrictions, or geopolitical mood swings. For thirty years, that was a product with no market. Then the market arrived all at once.

Here’s what I’m watching to see how the story evolves. Surveillance margins, do they hold above 10% through Q1, the seasonally weakest quarter? Poland submarines, does the ~SEK 30 billion contract convert from selection to signature in the first half? The Capital Markets Day, does Johansson finally quantify software revenue? That’s the single most important catalyst. Aeronautics margins, do they break 7%, or does T-7 keep eating the Gripen improvement? And European defense spending, do the 2% of GDP commitments survive the next election cycle?

In 1993, nobody wanted the Gripen. In 2026, countries are lining up to enter Saab’s ecosystem, and once they’re in, they don’t leave. The company that was too small, too Swedish, and too stubborn to build what the world wanted spent three decades building what the world would eventually need. Whether the stock catches up depends on one man at a podium, pointing at a slide, saying a number he’s been carefully not saying for two years.

Johansson knows which number. The market is waiting. I think the wait is almost over.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.