Saab Q1 2026 Earnings: The Number That Didn’t Come

We were waiting for Saab to disclose software revenue. Q1 suggests the platform may reveal itself first in the architecture customers are buying.

TL;DR

The proof may not come as a software revenue line: We were waiting for Johansson to disclose Saab’s software/integration economics, but Q1 suggests the platform is first becoming visible in product architecture, especially C-UAS, where sensors, command-and-control, effectors, and upgrades are sold as one integrated system.

Saab’s real flywheel is sovereign architecture: The bull case is not simply that Saab sells more defence equipment; it is that each radar, C2 layer, Gripen system, naval combat system, or counter-drone deployment makes the next Saab product easier to adopt by deepening training, doctrine, interoperability, maintenance, and political switching costs.

Q1 strengthened the base case, not the victory lap: Organic growth, EBIT leverage, Surveillance strength, and operational cash flow all support the thesis, but free cash flow was still negative, Aeronautics remains a drag, and software disclosure is still missing, so Saab remains an “own and verify” stock, not a thesis fully proven.

I ended the last Saab piece waiting for a number.

Not a revenue number. Not an EBIT number. Not another backlog number. Saab already had those. I was waiting for the number that would either vindicate or embarrass the thesis we had been building for a year: how much of Saab is really software, systems integration, electronic warfare, data links, combat management, AI, and upgrade economics hiding inside a company still reported like a traditional defence contractor?

Q1 did not give us that number.

That should have been a problem. Instead, it made the story more interesting.

Our prior Saab arc was straightforward. Saab was no longer just a Swedish defence contractor. It was becoming Europe’s “sovereign stack”: a company whose value came not merely from selling fighters, radars, missiles, or submarines, but from connecting those systems into a NATO-compatible architecture that countries could operate and upgrade with greater independence. The missing proof point was disclosure. At some point, we expected Micael Johansson to point to a slide and say: here is the software layer, here are the margins, here is why Saab should not be valued like a normal defence contractor.

He still has not said it.

There are two ways to respond to that. The easy way is to say the thesis remains unproven. The better way is to ask whether we were looking for proof in the wrong place.

What If Software Is Not a Segment?

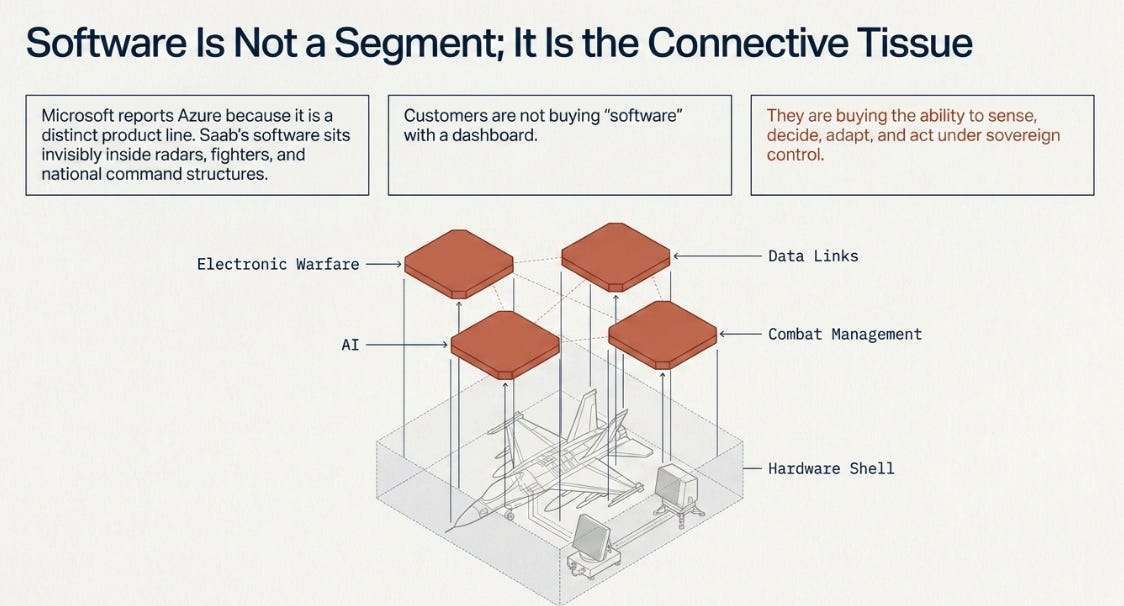

The mistake may be importing a software-company disclosure expectation into a defence architecture business.

Microsoft can report Azure because Azure is a product line. Adobe can report subscription revenue because the business model makes the software line visible. Saab is different. Its software is not consumed separately by a procurement officer with a credit card and a dashboard. It sits inside radars, fighters, electronic-warfare systems, combat-management systems, counter-drone architectures, naval platforms, training routines, command structures, and national doctrine.

The customer is not buying “software.” The customer is buying the ability to operate a defence system that can sense, decide, adapt, and remain under sovereign control.

That is why the software number still matters, but may not be the first place the truth appears. If Saab is right, the economics will show up first in how customers buy: not isolated equipment, but architectures. Not a radar, then a separate command system, then a separate effector, but an integrated chain from detection to decision to action. Not one national project, but a series of adjacent procurements that become easier because the country is already inside the Saab architecture.

The question after Q1, then, is not “where is the software disclosure?” It is: are customers behaving as if Saab’s integration layer is becoming the product?

Q1’s answer was not definitive. But it was suggestive.

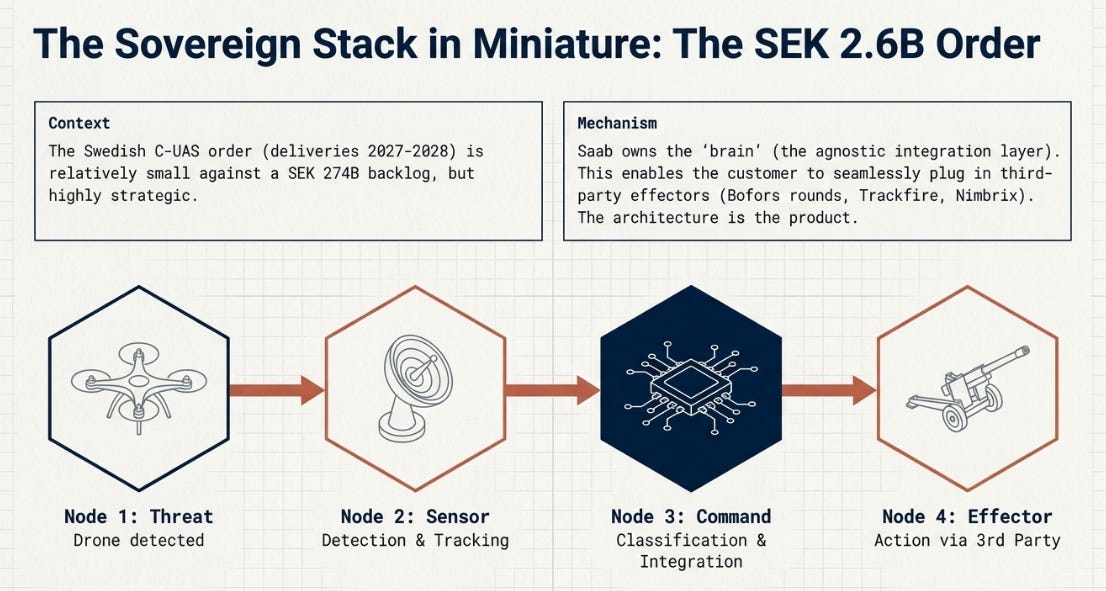

The SEK 2.6 Billion Order That Matters More Than Its Size

The most important order in Q1 was not large enough to move the model.

Sweden’s Counter-UAS order was worth SEK 2.6 billion, with deliveries planned for 2027-2028. In a company with a SEK 274 billion backlog, that number is not the point. The architecture is the point.

Saab described the system as an integrated Counter-UAS solution, from “sensor to shooter,” modular, adaptable to evolving drone threats, built with Saab and selected third-party technologies, and including further development and integration.

That is the sovereign stack in miniature.

A drone appears. A sensor detects it. A command system classifies it. An effector is selected. The architecture adapts as the threat evolves. The customer does not simply buy a radar, a cannon, a missile, or a vehicle. The customer buys the system that makes all of those pieces work together.

On the call, Johansson described the system as flexible and effector-agnostic — able to work with different effectors, from Bofors rounds to Trackfire and eventually Nimbrix. That is the right kind of agnostic. Saab does not need to own every fist if it owns the brain that decides where the fist lands.

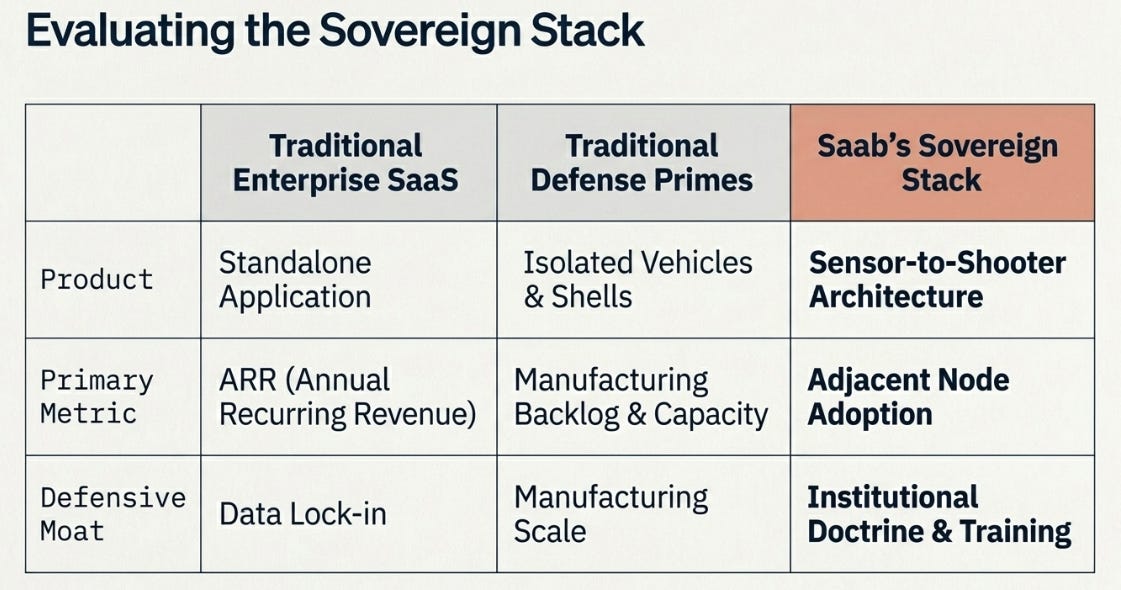

This is where Saab differs from the usual European rearmament story. Rheinmetall’s question is capacity: can it produce enough shells, vehicles, and land systems into a shortage? Saab’s question is architecture: can it become the integration layer for countries that want NATO-compatible capability without total dependence on any one superpower or prime contractor?

Capacity still matters. But for Saab, capacity is the cost of the thesis, not the thesis itself.

The Flywheel Is Boring, Which Is Why It Works

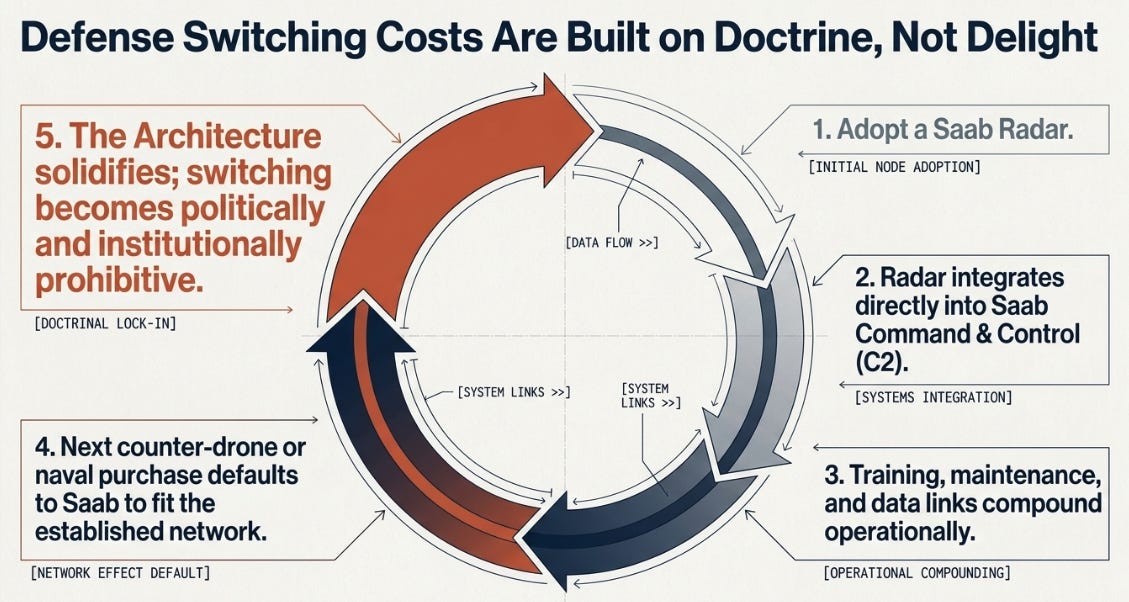

Defence switching costs are not created by delight. They are created by doctrine.

A country buys a Saab radar. That radar connects into Saab command-and-control. The next counter-drone system is easier to buy from Saab because the sensor layer already exists. The next naval system is easier if the combat-management layer is trusted. The next aircraft, electronic-warfare package, or upgrade becomes less like a fresh procurement and more like an extension of the architecture already in place.

This is not a social network effect. No one is posting selfies on Giraffe 1X. It is slower, more political, more bureaucratic, and much harder to see. But in defence, those features can make it more durable.

Training compounds. Maintenance routines compound. Data links compound. Local industrial participation compounds. Software upgrade paths compound. Operational trust compounds. The switching costs are not just financial; they are institutional.

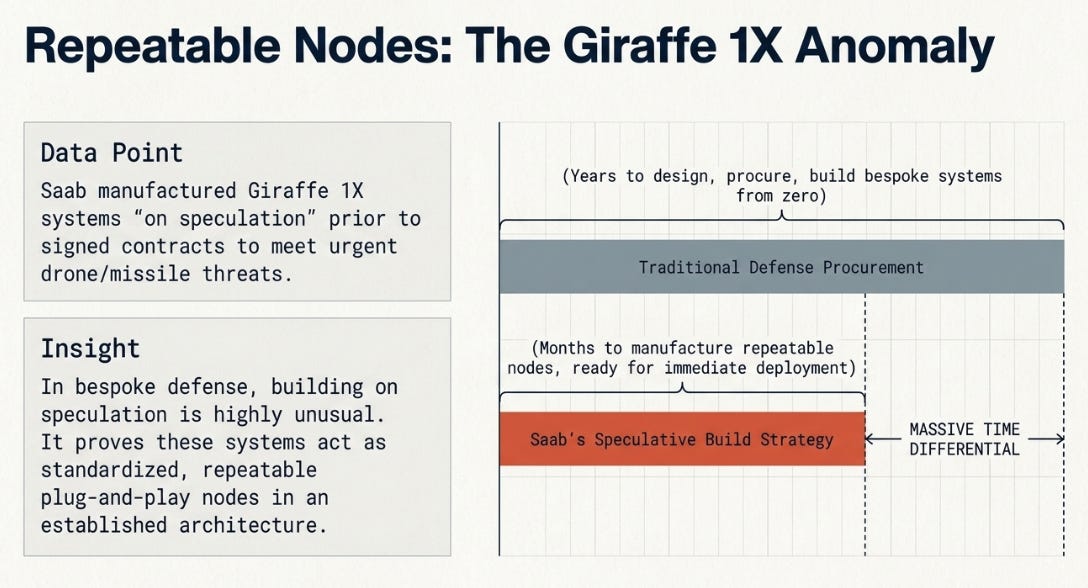

That is why Q1’s Giraffe 1X commentary mattered. Johansson said Saab had manufactured some Giraffe 1X systems partly “on speculation,” rather than only waiting for signed contracts, which enabled fast deliveries to customers facing urgent missile and drone threats. In a bespoke defence world, that is an unusual posture. It suggests some Saab systems are becoming repeatable nodes in an architecture, not one-off national projects that begin from zero every time.

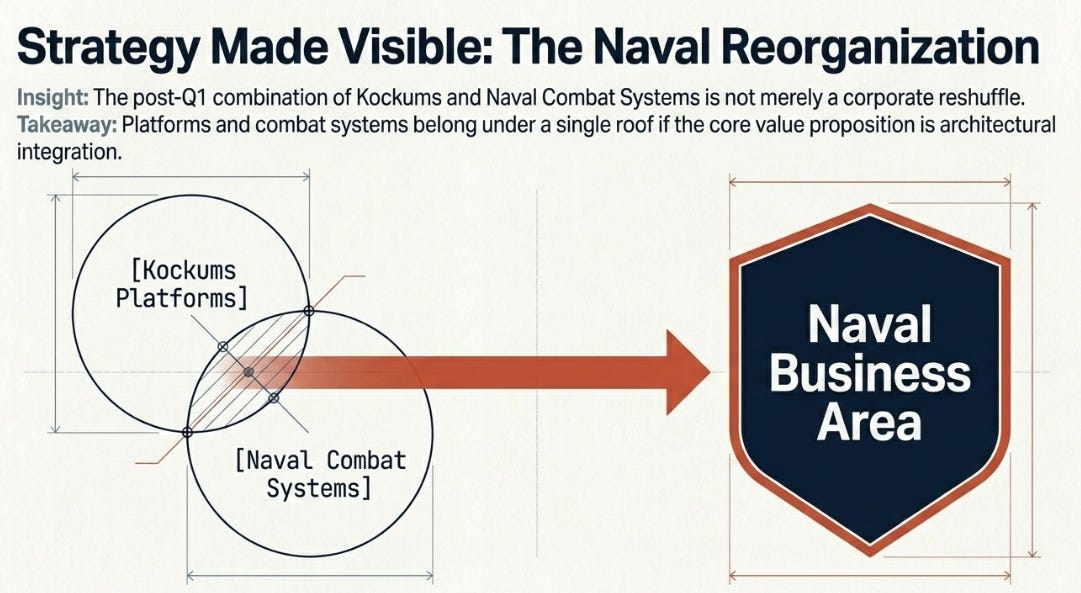

Naval points in the same direction. Saab’s new Naval business area, formed after the quarter, combines Kockums with Naval Combat Systems. That is not just reorganization. It is strategy made visible: platforms and combat systems belong together if the value is integration.

The Quarter After the Fireworks

Only now do the Q1 numbers matter.

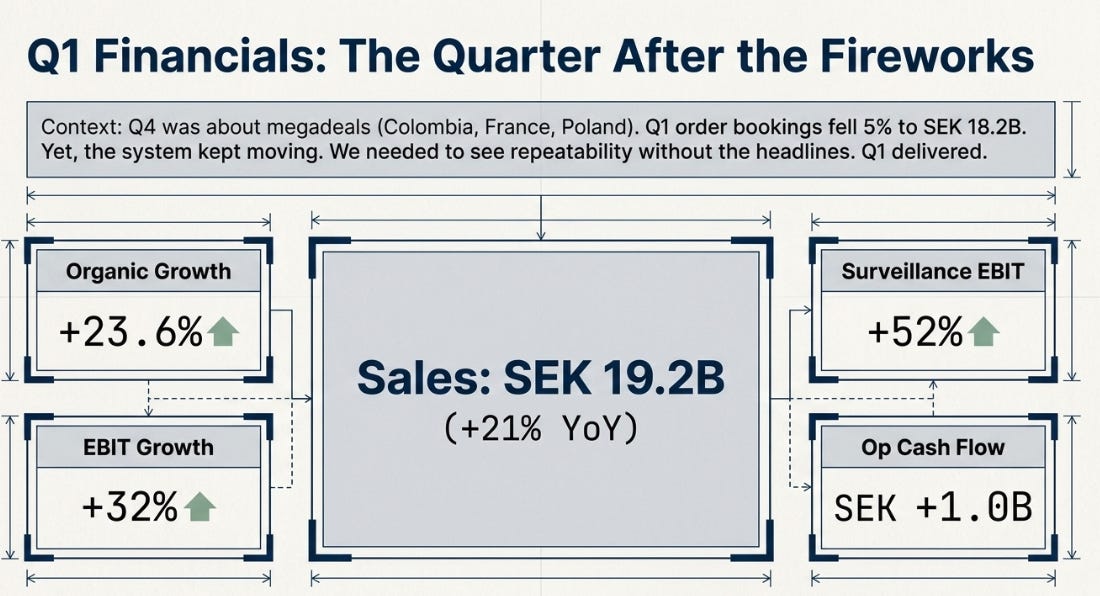

Q4 was the fireworks quarter: Colombia Gripen, France GlobalEye, Poland submarines selected, Ukraine letter of intent, record orders, and a backlog that made the sovereign-stack thesis feel almost too neat. Q1 was quieter. Order bookings fell 5% to SEK 18.2 billion, and book-to-bill was below 1x. A sell-side recap would start there.

If this were merely a defence-cycle story, that would matter more. If it is an architecture story, the more interesting fact is that the system kept moving without another megadeal.

Sales rose 21% to SEK 19.2 billion, organic growth was 23.6%, EBIT rose 32%, and operational cash flow improved to SEK 1.0 billion. All business areas and Combitech delivered double-digit sales growth. Surveillance grew sales 32% and EBIT 52%, helped by Giraffe 1X deliveries and C-UAS. Dynamics remained the profit engine, with a 17.5% margin.

That is what we needed to see. Not perfection. Repeatability.

Saab did not need a giant new order to grow faster than 20%. It did not need a software disclosure slide to show operating leverage. It did not need a fighter headline for Surveillance to look increasingly like the place where sensors, software, command-and-control, and threat adaptation collapse into one business.

This is what I mean by the architecture becoming observable.

The Part That Still Bothers Me

This is where I do not want to let the thesis get too elegant.

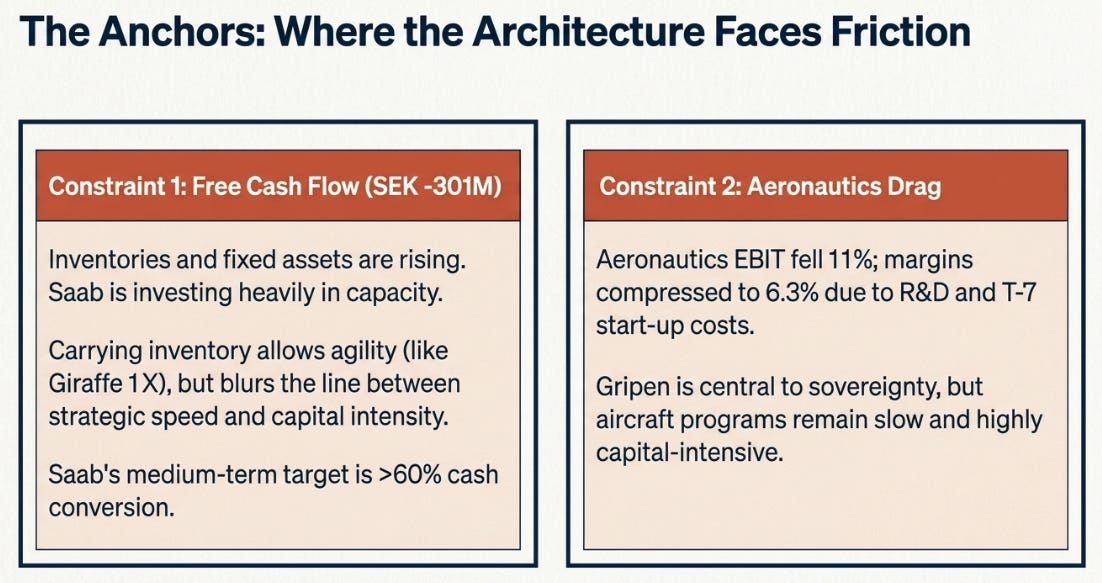

Free cash flow was still negative SEK 301 million. Inventories rose. Tangible fixed assets rose. Saab is investing heavily in capacity, inventory, suppliers, and facilities because architecture still has to be manufactured.

Some of that is exactly what we want. If speed wins defence orders, and if customers need systems now, then carrying inventory can be strategic. The Giraffe 1X example suggests Saab is willing to take working-capital risk where it has demand visibility.

But there is a line between strategic inventory and bad inventory, and the income statement will not tell you where that line is. Cash will.

Saab’s medium-term target is cumulative cash conversion above 60%. Q1 moved in the right direction, but one quarter does not answer the funding question. If Saab’s architecture story requires too much capital to scale, the platform multiple will have a ceiling.

Aeronautics is the second constraint. Sales grew 15%, but EBIT fell 11%, and the margin compressed to 6.3%, hurt by R&D amortization, currency, and T-7 start-up costs. Gripen is central to the sovereignty narrative, but aircraft programs remain slow, complex, and capital-intensive. The base case can tolerate that. The bull case cannot ignore it.

What Changed in My View

Before Q1, I thought software disclosure was the next decisive gate. After Q1, I still think it matters, but I no longer think it is the only gate.

The cleanest proof would be a number. The earlier proof may be customer behaviour.

If C-UAS exports follow Giraffe 1X installations, if Naval shows better economics after combining platforms with combat systems, if Surveillance sustains margins above 10%, if countries that buy one Saab node return for adjacent nodes, then the architecture thesis will be proving itself before accounting catches up.

That is the update. We were waiting for Saab to separate software from hardware. Q1 suggests customers may increasingly be buying the place where software and hardware become inseparable.

Variant Perception

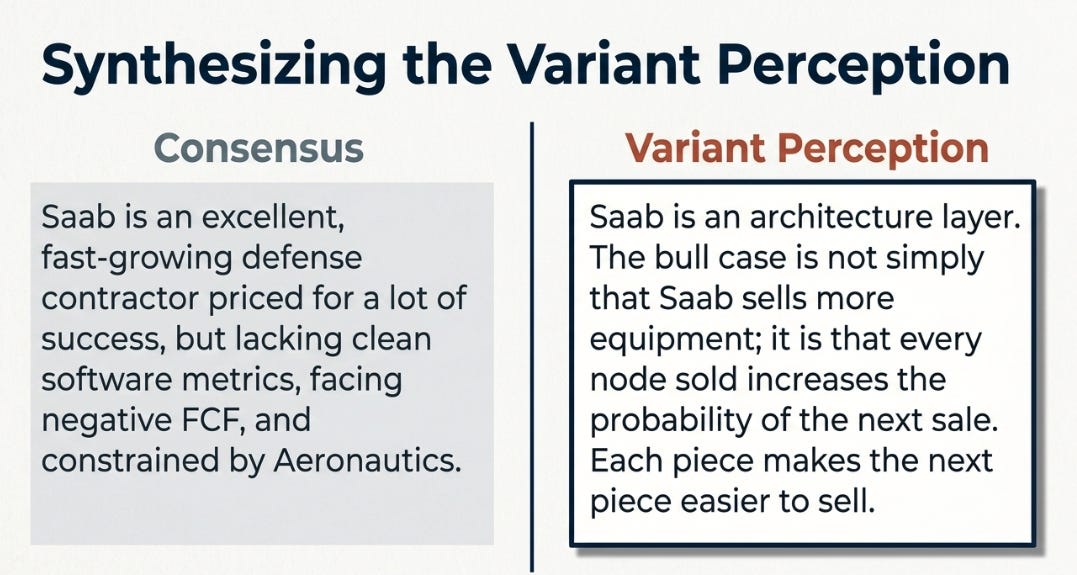

The consensus view is reasonable: Saab is an excellent European defence company, growing rapidly, but priced for a lot of success. Order intake was down, free cash flow was negative, Aeronautics disappointed, and the software number still does not exist.

The variant perception is not to dismiss those issues. It is to say they are not the central issue.

The central issue is whether Saab is becoming an architecture layer. If it is, every system sold increases the probability that the next system is also Saab. A radar creates pull-through for C2. C2 creates pull-through for counter-drone. Counter-drone creates pull-through for effectors. Gripen creates decades of training, maintenance, upgrades, weapons integration, and electronic-warfare dependence. Naval combat systems can do the same at sea.

The bull case is not that Saab sells more equipment. The bull case is that each piece of equipment makes the next piece easier to sell.

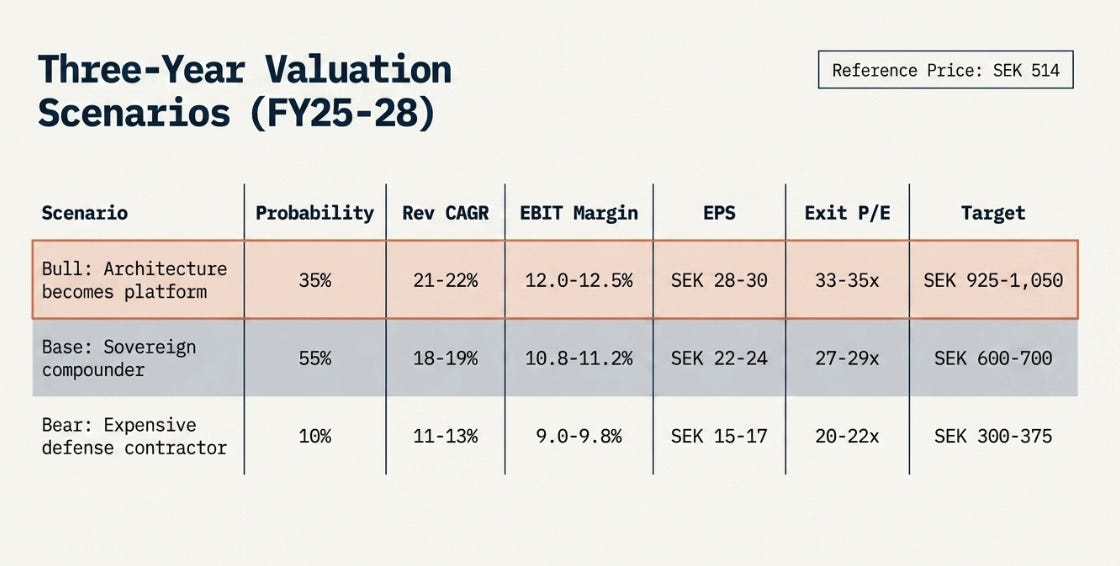

Three-Year Scenarios

Using a reference price around SEK 514, the setup is attractive but not obvious.

I would not raise the bull probability yet. Q1 did not give us software disclosure, a major new platform award, or clean free cash flow. What it did give us was a stronger base case and a lower probability that Q4 was merely order-book euphoria.

This remains an “own and verify” stock. The expected value is attractive, but the proof points still matter.

What To Watch

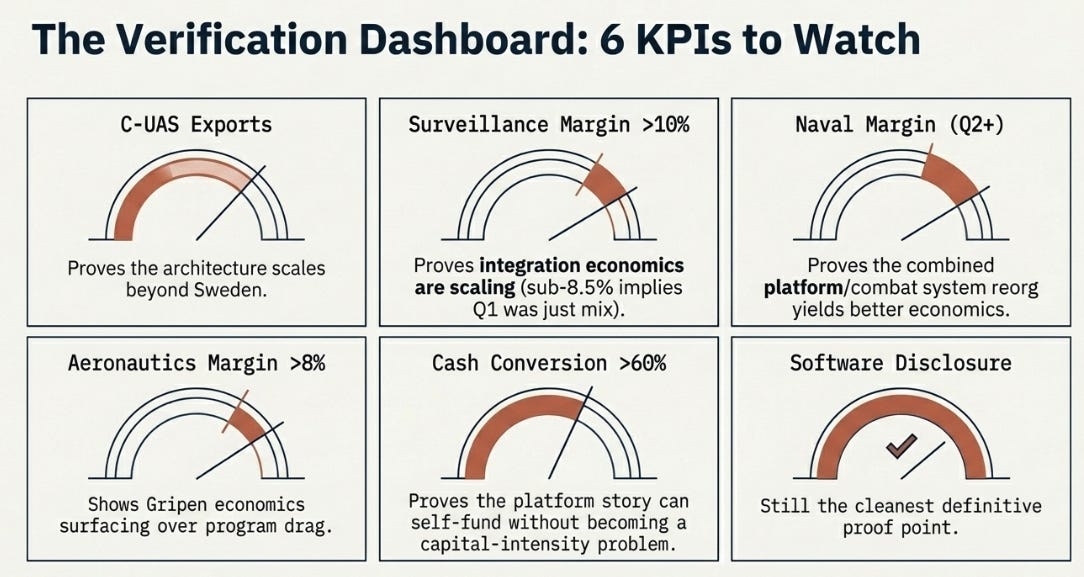

The first proof point is C-UAS exports. Sweden proves the concept; export orders prove the architecture.

The second is Surveillance margin. Above 10% sustained suggests integration economics are scaling. Below 8.5% suggests Q1 was mix.

The third is Naval margin from Q2 onward. The reorganization only matters if platforms plus combat systems produce better economics than platforms alone.

The fourth is Aeronautics margin. Above 8% would show Gripen economics surfacing. Below 6% would mean T-7 and program drag are still eating the story.

The fifth is cash conversion. Above 60% keeps the thesis self-funded. Below 50% turns the platform story into a capital-intensity problem.

And yes, the sixth is still software disclosure. It is no longer the only proof. It remains the cleanest one.

The Number Can Wait. The Architecture Can’t.

Q1 did not answer the question we asked. It suggested a better question.

We wanted Saab to prove the software layer by disclosing it. Instead, Q1 showed the software layer becoming visible in the architecture customers are buying: Giraffe 1X into C-UAS, C-UAS into command-and-control, Naval into combat systems, Surveillance into the integration layer.

That is not yet disclosed software economics. It is not durable free cash flow. It is not permission to ignore valuation.

But it is the right kind of evidence.

Saab is no longer trying to prove that countries want sovereignty. Q4 did that. Q1 asked whether sovereignty compounds when the headlines go quiet.

The answer is not final. But it is getting harder to dismiss.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.