SanDisk 3QFY26 Earnings: From Thesis to Test

The warm-storage thesis has been validated. The next question is whether contracts can turn a violent NAND upcycle into durable earnings power.

TL;DR

The AI storage bottleneck is now real, not theoretical. Datacenter is already a quarter of revenue, enterprise SSD demand is being pulled directly by inference, KV cache, RAG, longer context windows, and agentic workloads.

Q3 proved SanDisk has pricing power — maybe too much pricing power. Revenue, EPS, gross margin, and free cash flow all exploded, but the quarter was heavily ASP-led, which keeps cyclicality risk front and center.

The investment case has shifted from demand to durability. The key variable is no longer whether SanDisk can earn extraordinary EPS; it is whether NBM coverage, contract guarantees, and margin floors can hold through the next downcycle.

The Thesis Has Been Walked

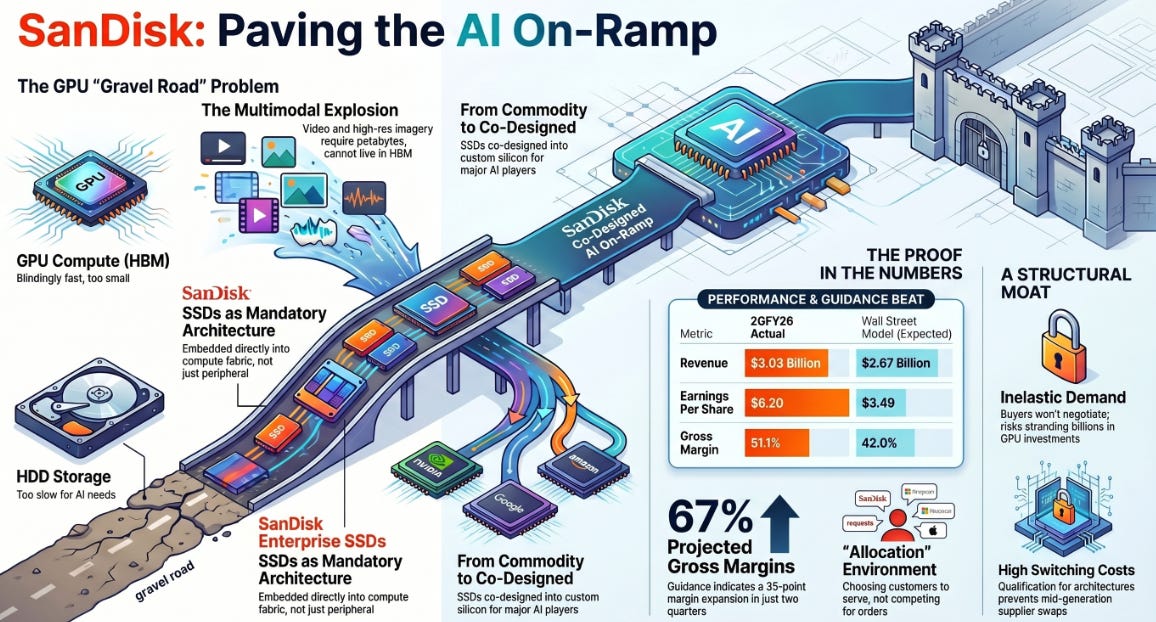

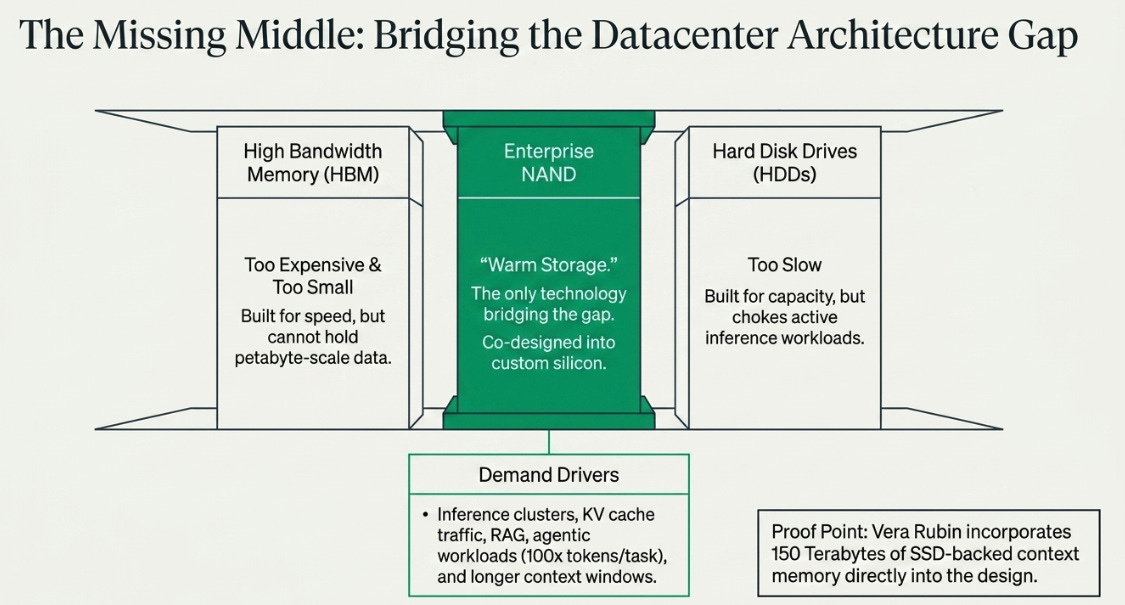

When I initiated SanDisk at $244, the argument was simple: NVIDIA had built the twenty-lane GPU highway, but the on-ramps were still gravel roads. AI infrastructure had a missing middle, High Bandwidth Memory was too expensive for petabyte-scale data, hard drives were too slow for active workloads, and the only technology that filled the gap was high-capacity enterprise NAND. I called it warm storage and argued it was becoming mandatory infrastructure, not a commodity input. My bull case was $450.

After Q2, at $539, I wrote that Jensen Huang had effectively confessed the problem on stage at CES. He described context memory that no longer fit inside HBM, KV cache traffic choking inference clusters, and 150 terabytes of SSD-backed context memory designed directly into Vera Rubin. Three weeks later SanDisk’s earnings confirmed the demand. ASPs were up 35-57% sequentially, gross margins were guided to 65-67%, and the company was operating in allocation, choosing which customers to serve rather than competing for orders. I set a new bull case at $1,200 and wrote that “the next 2x may be harder, but the path is visible.”

The stock is now $1,127. The path has been substantially walked. My original bull case has been exceeded by 2.5 times while we are still in fiscal 2026.

The awkward part about being right on direction is that it does not mean being right on magnitude. My framework for the architectural bottleneck was correct: datacenter is now a quarter of revenue, enterprise SSDs are being co-designed into custom silicon, and pricing power has transferred from buyer to seller. But my imagination for how violently SanDisk would capture the economics of that bottleneck was far too small. That makes this update harder than the previous two. This is not a victory lap. It is a framework reset forced by a stock that has outrun the thesis.

Q3: Numbers That Force a Reset

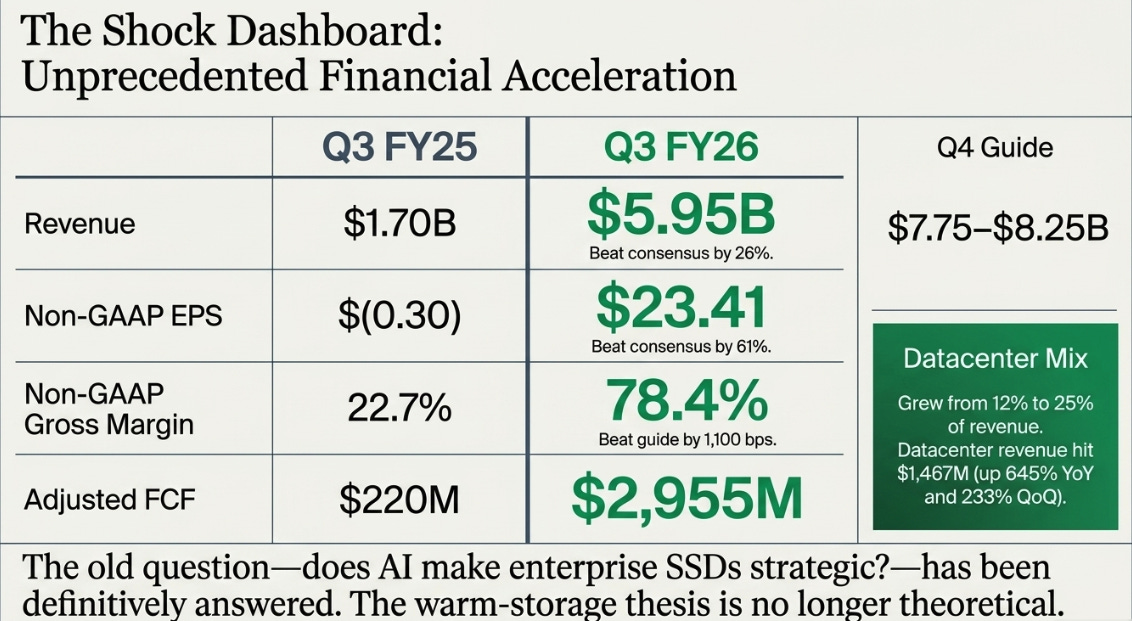

The numbers almost defy annotation.

Source: SanDisk press releases and earnings presentations.

Revenue beat consensus by 26%. EPS beat by 61%. Gross margin beat the company’s own guide by eleven hundred basis points. Datacenter revenue grew 233% sequentially and 645% year-over-year. Q4 was guided roughly 30% above what the sell side had penciled in.

The old question, does AI make enterprise SSDs strategic?, has been answered. Datacenter is a quarter of the business, not a future slide. Management explicitly tied NAND demand to inference, reasoning, agentic AI, KV cache, RAG, longer context windows, and token generation. The warm-storage thesis is no longer theoretical.

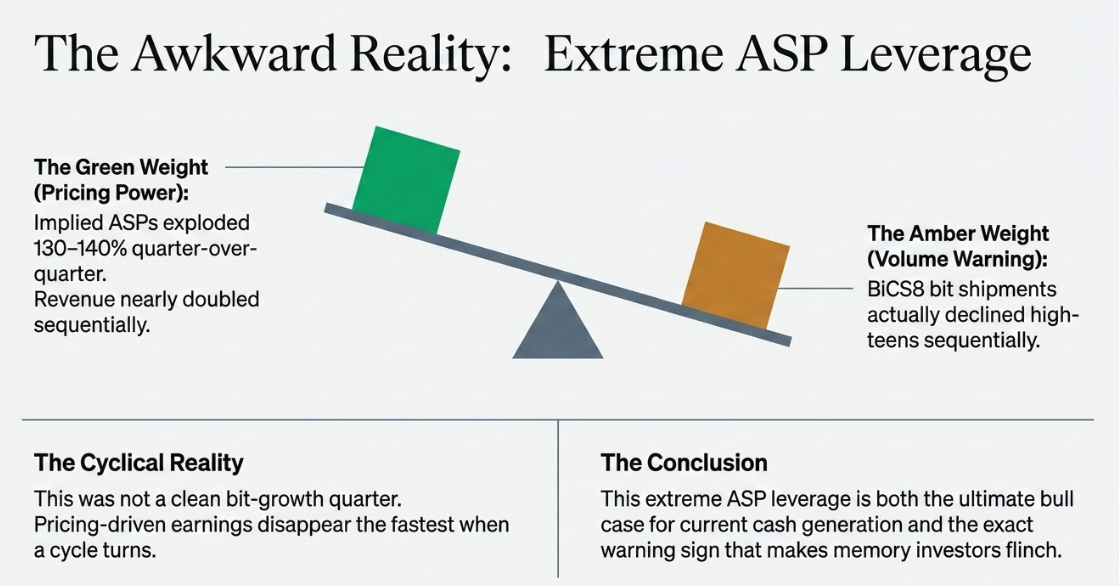

But this was not a clean bit-growth quarter. Revenue nearly doubled while BiCS8 shipments were down high-teens sequentially, implying ASPs exploded roughly 130-140% quarter-over-quarter. That is both the bull case and the warning sign. Pricing-driven earnings are the ones that disappear fastest when the cycle turns, which is exactly why memory investors flinch even when the numbers are extraordinary.

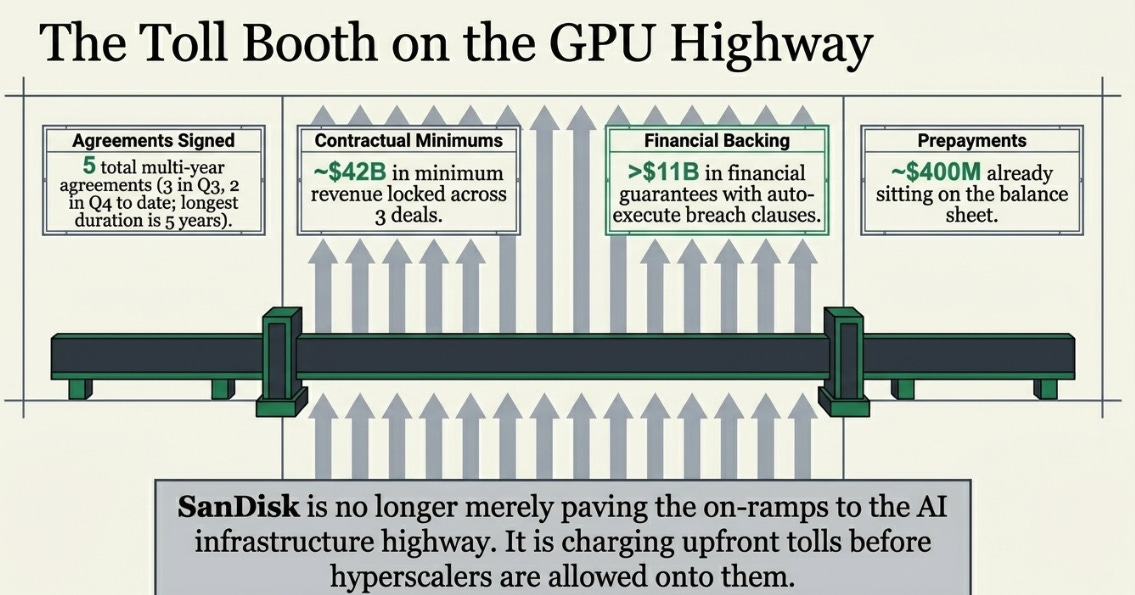

The Toll Booth Emerges

The more important disclosure than the headline beat is what SanDisk is doing with its leverage.

Source: SanDisk Q3 FY26 earnings call and press release.

In the initiation, I argued SanDisk could be valuable as the “intentional fifth wheel”, a strategically necessary supplier that hyperscalers would preserve to avoid Samsung/SK Hynix concentration. That framing was right but incomplete. It described why SanDisk had value. It did not describe how SanDisk would capture it.

Q3 supplied the mechanism: contracts. Five multi-year agreements with prepaid collateral and auto-execute breach clauses, backed by third-party financial instruments. SanDisk is no longer merely paving the on-ramps to the GPU highway. It is charging tolls before customers are allowed onto them.

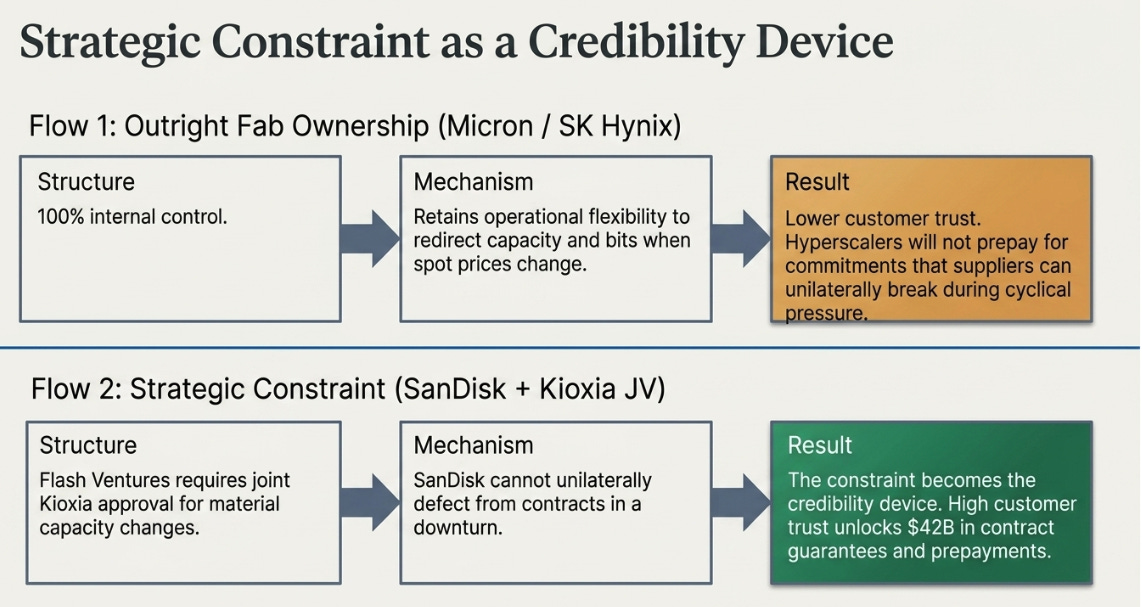

There is an underappreciated structural reason why customers signed with SanDisk specifically. SanDisk’s joint venture with Kioxia, historically the biggest analytical knock on the company, prevents SanDisk from unilaterally redirecting capacity in a downturn. Flash Ventures requires Kioxia’s joint approval for material capacity changes. Customers will pre-fund commitments with a supplier that cannot defect from contracts under cyclical pressure. They will not pre-fund the same commitments with Micron or SK Hynix, who own their fabs outright and retain the operational flexibility to redirect bits whenever the math changes. The constraint became the credibility device. The credibility device enabled the toll booth.

But toll booths are not magic. The notes following the print captured a nuance the bulls were underweighting: NBMs improve multiple durability but may cap peak-cycle upside. If customers lock supply at fixed or semi-fixed terms near current pricing, SanDisk may be trading some peak-cycle optionality for a more durable base. That is good for the multiple. It is potentially bad for the most aggressive EPS scenarios. Durability has a price, and the price is participation if NAND keeps ripping above contracted levels.

The Problem With Being Right

My Q2 bull case was $1,200 with 25% probability. The stock is at $1,127, within 6% of the scenario I assigned one-in-four odds. Either my Q2 probabilities were wrong and the bull case deserved higher weight, or the stock has moved faster than the evidence supports. Both readings lead to the same conclusion: the analytical framework needs to be rebuilt around different variables.

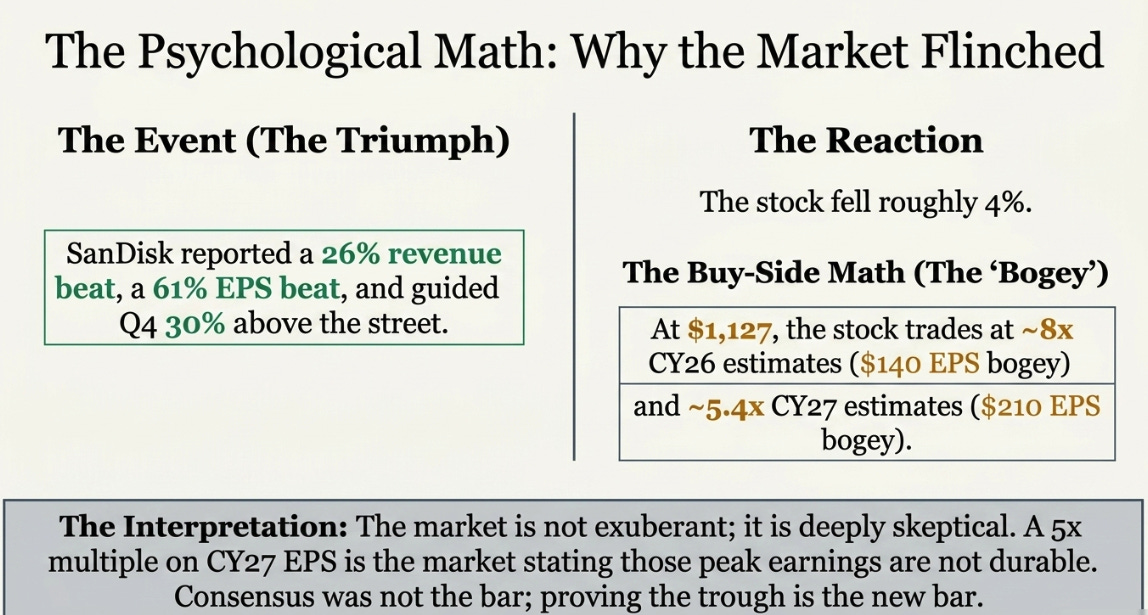

The stock reaction confirms this. SanDisk fell roughly 4% on a quarter that beat consensus by 26% on revenue and 61% on EPS, with a Q4 guide 30% above the street. That is not irrational. It is revealing. Consensus was not the bar; buy-side bogeys were. The most aggressive investors were already underwriting CY26 EPS around $140 and CY27 EPS above $210. At $1,127, the stock trades at roughly 8x CY26 and 5.4x CY27 on those bogeys.

The market is not exuberant. It is skeptical. A 5x multiple on CY27 EPS is the market saying those earnings may not be durable. The market has the thesis. It is waiting for proof that the floor holds.

The New Bear Case Is Margin Durability

The demand picture is as strong as it has ever been for any semiconductor subsector. Big 5 hyperscaler capex went from $620 billion to $720 billion in three months. All five guided higher for CY27. Token consumption is growing exponentially. Agentic AI, multi-agent systems that consume 100x or more tokens per task compared to single-shot inference, is in its first year. KV cache, RAG, longer context windows, and reasoning workloads are all NAND-hungry, not HBM-hungry. The demand side of the warm-storage thesis is not just intact; it is accelerating faster than I modeled at initiation.

The bear case is no longer about demand. The bear case is about margin durability on the uncontracted portion of the book. NBMs currently cover just over one-third of FY27 bits. That means roughly two-thirds of SanDisk’s output remains exposed to spot pricing. If ASPs roll over, because Samsung eventually responds, because Micron pivots back from HBM, because hyperscalers hit a digestion cycle in late 2027, the uncontracted book gets hit. NBMs cushion the trough. They do not repeal cyclicality.

The question is no longer whether SanDisk can earn extraordinary EPS. It obviously can. The question is whether the gross-margin floor is 55%, 45%, or 30%. The answer to that question determines whether the stock is cheap, fair, or expensive at $1,127, and the answer depends almost entirely on whether NBM coverage scales past 50% and whether the variable-pricing components in years three through five of those contracts hold through a downturn.

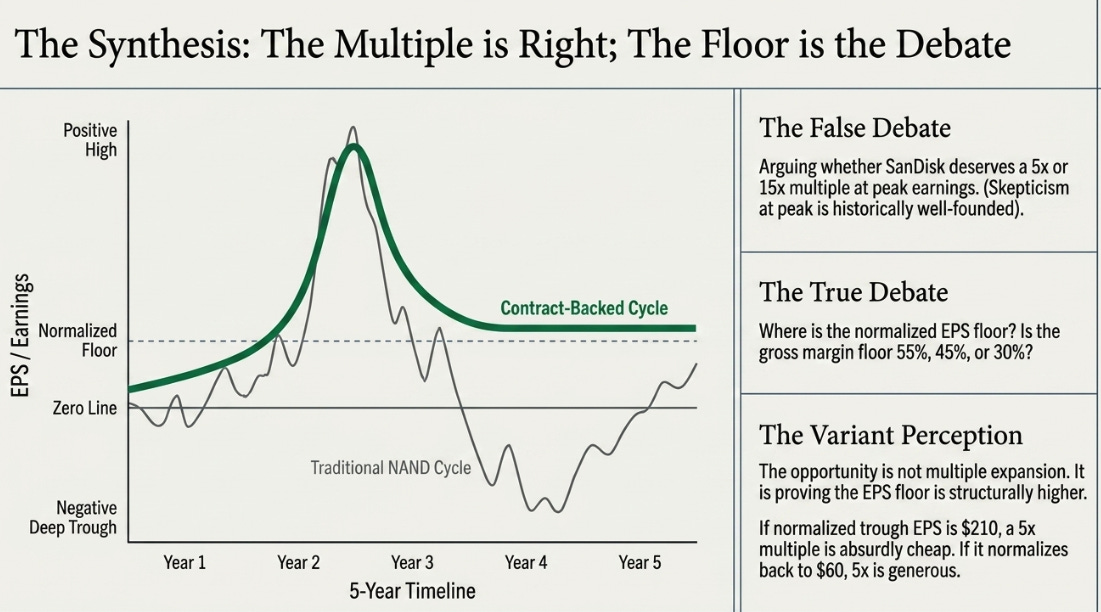

Variant Perception: The Debate Is The EPS Floor

The consensus view is that SanDisk is in the greatest NAND upcycle in history, with AI demand providing structural support, but earnings are probably near peak and the cycle will resolve as cycles always have.

The bull view is that NBMs and AI architecture integration have changed the earnings profile permanently, that contracts convert commodity pricing spikes into infrastructure-like cash flows, and the stock deserves a multiple closer to differentiated semis than to cyclical memory.

My view is that both sides are arguing about the wrong variable. The multiple is roughly right, 5-8x near-peak earnings is what a skeptical market pays for memory at the top of the cycle, and that skepticism is historically well-founded. The debate is not about the multiple. It is about whether normalized EPS is $210 (in which case 5x is absurdly cheap) or $60 (in which case 5x is generous). The opportunity is not multiple expansion. It is proving that the EPS floor is structurally higher than old-cycle investors assume. That proof requires NBM coverage scaling, and we are at one-third, not one-half.

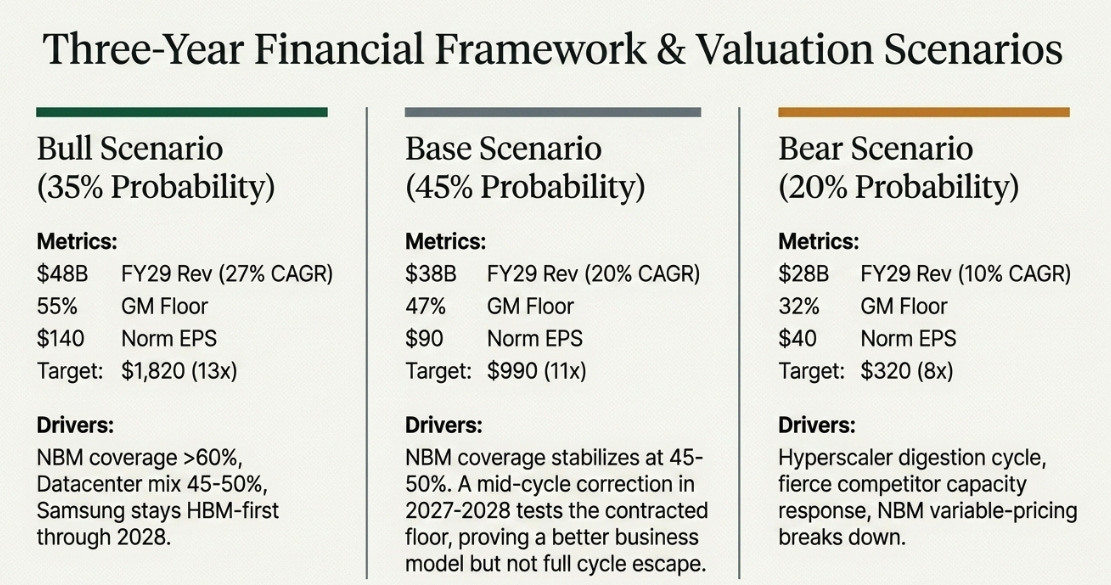

Three-Year Framework

The bull case requires NBM coverage above 60%, datacenter mix at 45-50%, HBF contributing revenue by FY29, and Samsung maintaining HBM-first capital allocation through 2028. The demand backdrop, $720B of hyperscaler capex rising into CY27, agentic workloads in year one, makes this more plausible than it was three months ago.

The base case requires NBM coverage stabilizing at 45-50%, margins normalizing well above historic NAND levels but well below 78%, and a mid-cycle correction in 2027-2028 that tests the contracted floor. This is the scenario where SanDisk proves it is a better business than old NAND without proving it has fully escaped the cycle.

The bear case requires a hyperscaler digestion cycle, competitor capacity response, and NBM variable-pricing components resetting lower in years three through five. Even here, the floor is higher than the $140 bear I wrote at initiation, the contracted base provides genuine protection that did not exist in prior cycles.

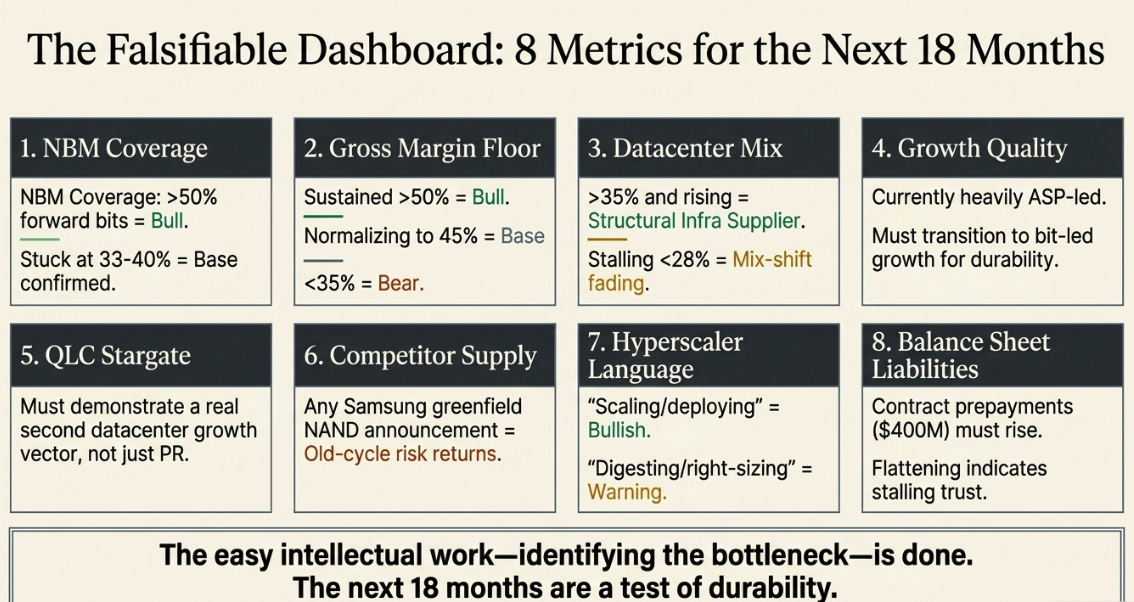

What We Track

Eight items, with falsifiable thresholds:

NBM coverage, above 50% of forward-year bits strengthens bull case; stuck at 33-40% confirms base

Gross-margin floor, sustained above 50% = bull; normalizing to 45% = base; below 35% = bear

Datacenter mix, above 35% and rising = infrastructure supplier; stalling below 28% = mix-shift fading

ASP vs bit decomposition, pricing-led is the current story; bit-led growth needed for durability

QLC Stargate ramp, must become a real second datacenter growth vector, not just a press release

Competitor supply, Samsung greenfield NAND announcement = old-cycle risk returns

Hyperscaler language, “scaling” and “deploying” remain bullish; “digesting” and “right-sizing” are warnings

Contract liabilities on balance sheet, should rise if NBM prepayments are real; flattening = stalling

From Thesis to Test

The first article asked whether AI needed a warm-storage layer between HBM and hard drives. The second article showed that NVIDIA’s architecture confirmed the problem. This article has to ask a harder question: can SanDisk turn that problem into durable economics?

SanDisk has not become software. It has not escaped memory cyclicality. But it has found a mechanism, contracts, guarantees, committed bits, a JV structure that makes those commitments credible, that could make part of the cycle contract-backed. Whether that mechanism scales from one-third to one-half of bits, whether the margin floor holds through the next downturn, and whether the demand from agentic workloads and inference scaling sustains the capex cycle through 2028, those are the questions the next 18 months will answer.

At initiation, SanDisk was a thesis. After Q2, it was a confirmation. After Q3, it is a test. The easy intellectual work, identifying the bottleneck, explaining why warm storage matters, understanding why the fifth wheel has strategic value, is done. What remains is watching whether the toll booth collects, and at what price.

The GPU highway is twenty lanes wide and full to capacity. SanDisk paved the on-ramps faster than I expected and built toll booths I did not anticipate. Whether the tolls hold through the next cycle is the only question that matters now.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.