Sea Limited 4Q25 Earnings: The Choice Not to Harvest

Unit economics are improving, but Sea is choosing scale over margins to deepen its ecosystem advantage.

TL;DR

Shopee’s margins remain low because Sea is deliberately reinvesting growing transaction surplus into infrastructure.

Cross-business integration: from SPayLater to VIP subscriptions, is creating measurable ecosystem advantages.

If those advantages persist, Sea’s current valuation assumes a profitability ceiling that likely isn’t real.

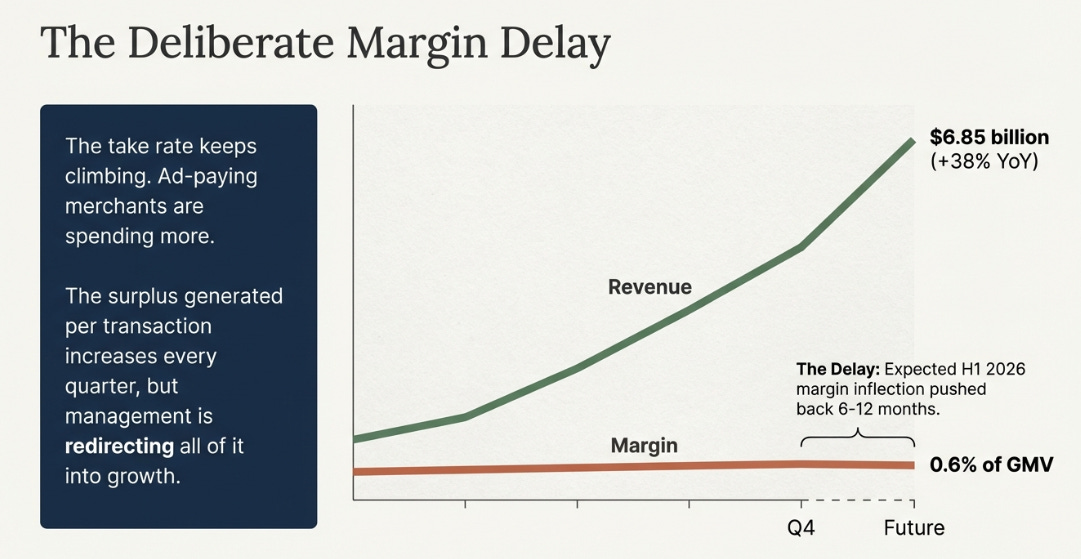

“Sea Limited reported fourth-quarter revenue of $6.85 billion, up 38% year-on-year. The company guided for 2026 Shopee GMV growth of approximately 25% with adjusted EBITDA ‘no lower than’ 2025 levels.”, Bloomberg

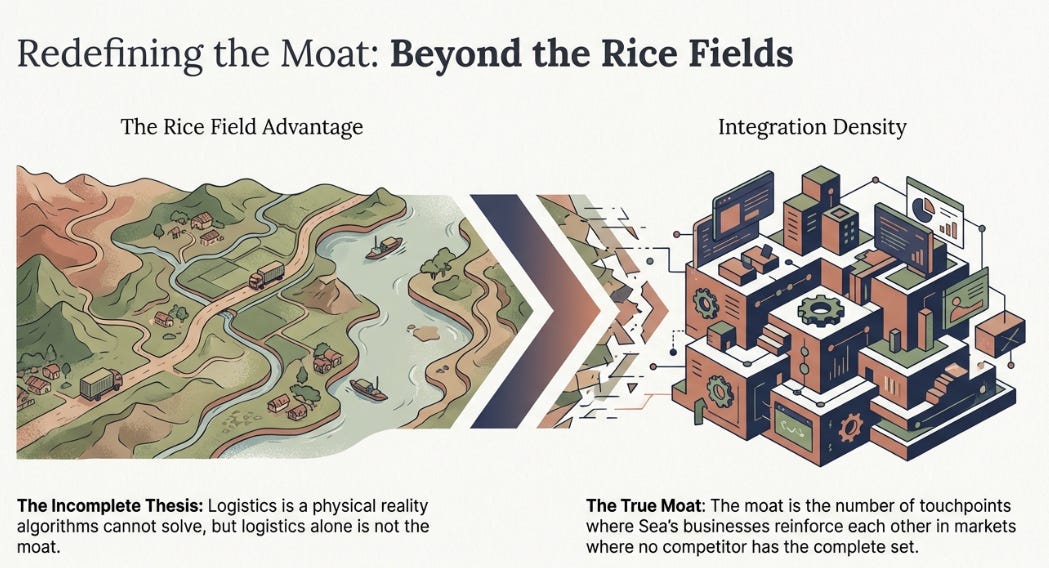

In November I wrote about Sea Limited’s “Rice Field Advantage”, the argument that years of building logistics infrastructure across rural Southeast Asia and urban Brazil had created an operational moat that asset-light competitors could not replicate. Delivering packages through rice fields and across rivers was a physical reality no algorithm could solve, and Sea had accumulated this capability one village at a time, in a way that could not be purchased or fast-followed.

The question was whether Shopee margins would inflect upward from the 0.6% of GMV level that spooked markets after Q3. They did not.

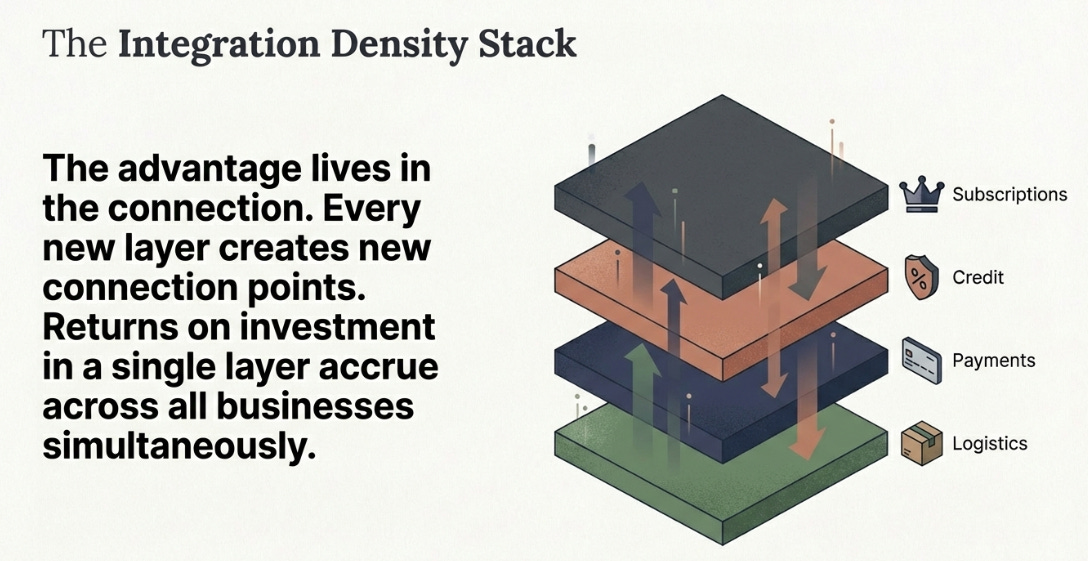

That non-event is what matters about this quarter, not because it invalidates the thesis, but because it clarifies what kind of company Sea is becoming. The rice field framing was wrong, or rather, incomplete. I described a logistics moat. What Q4 revealed is that the moat is integration density, the number of touchpoints where Sea’s businesses reinforce each other. Logistics was the first and most visible layer. It is not the moat itself. The moat is what happens when you stack logistics, payments, credit, and subscriptions on top of each other in markets where no one else has all four.

The Deliberate Delay

I got the timing wrong. I expected margin inflection to begin in the first half of 2026. Management pushed the timeline to the second half at earliest, possibly 2027. That is a six-to-twelve month delay.

The reason it didn’t arrive is what changes the interpretation. The unit economics improved, meaningfully. Core marketplace revenue grew at nearly twice the rate of GMV. Sea has pricing power it is choosing not to exercise. The take rate keeps climbing. Ad-paying merchants are spending more. The surplus generated per transaction is increasing every quarter.

Management is redirecting all of it into growth.

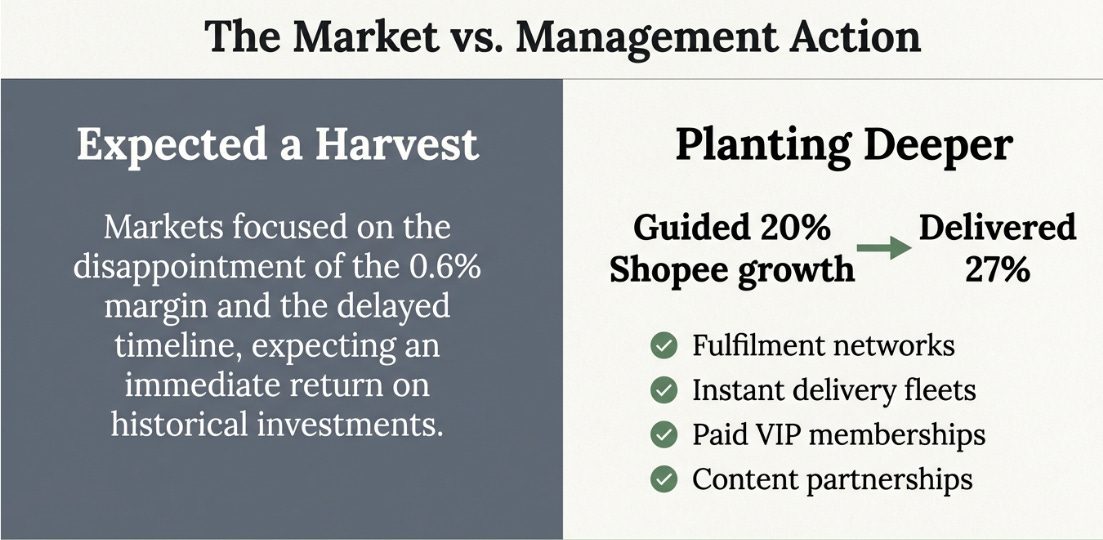

Chris Feng was remarkably direct on the call. They had guided for 20% Shopee growth at the start of 2025. Over the year, “we realized that there are areas we are able to drive the market to grow, and we also learned that there are different levers that we can pull.” They delivered 27%. Now they want to keep pulling.

The levers are all physical: fulfillment networks, instant delivery fleets, a paid VIP membership, content ecosystem partnerships. Feng described these as having “clear investment cycles”, time-limited, not permanent. He said margins should expand by end of 2026 and that the 2-3% long-term target “is well achievable.”

I believe him because the unit economics confirm it, not because CEO promises are inherently credible. A business whose high-margin revenue grows at twice the rate of its volume is generating margin. It is deploying it elsewhere. The question is whether the deployment is wise, and that depends on what the infrastructure produces once built.

Integration Density

I described the rice field moat as logistics, Sea can deliver where others cannot. That was right but incomplete.

What Q4 showed is that logistics is the foundation for interlocking advantages that create value no individual business could produce alone. The VIP program makes this concrete.

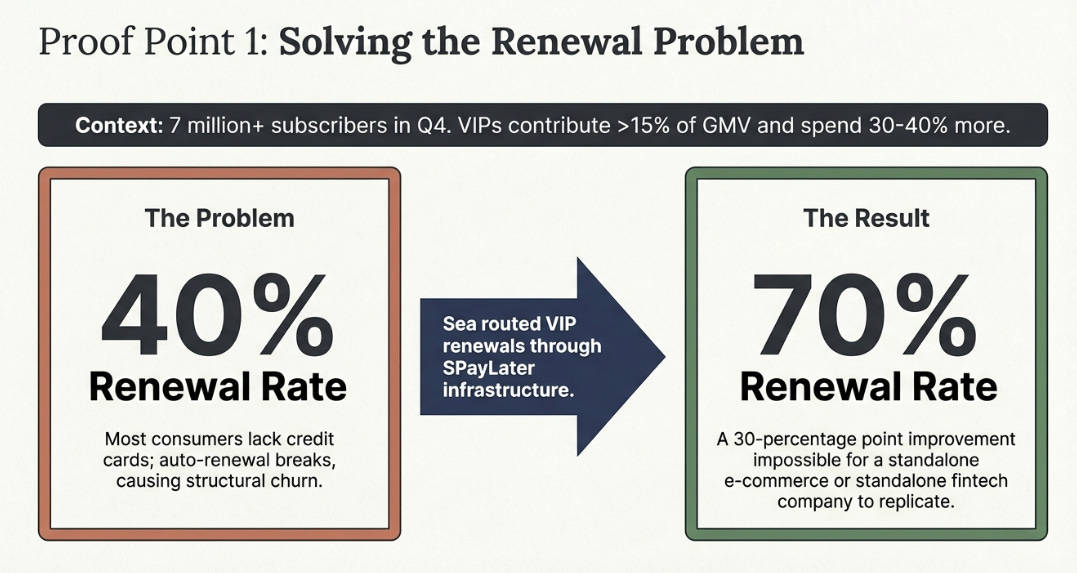

Sea launched a paid membership, free shipping, vouchers, exclusive discounts, that surpassed 7 million subscribers in Q4, more than double the prior quarter. In some markets VIP members contribute over 15% of GMV and spend 30-40% more after joining. Interesting, but not unique. Every e-commerce platform has tried loyalty programs.

The hard part in Southeast Asia is payment failure on renewal. Most consumers don’t have credit cards. Auto-renewal breaks. The renewal rate was 40%, most subscribers churned every month not because they wanted to leave, but because the payment couldn’t process.

Sea routed VIP renewals through SPayLater. The renewal rate in Indonesia went from 40% to 70%.

A standalone e-commerce company cannot replicate this without building its own financial services arm. A standalone fintech cannot replicate it without building its own marketplace. The advantage lives in the connection between two businesses, and it widens as both grow. More subscribers generate more payment data. Better data improves underwriting. Better underwriting enables new products. New products improve retention.

This is integration density. Not the generic “synergy” of investor day slides. A specific, measurable outcome, 30 percentage points of improved renewal, that exists only because two businesses share infrastructure. Every new layer Sea adds creates new connection points with every existing layer. The returns on investment in any single layer accrue across all three businesses simultaneously.

The margin delay is rational if you accept this framing. Sea is not investing in logistics. It is investing in integration density. And the returns compound in ways a single-segment P&L will never capture.

The Monee Question

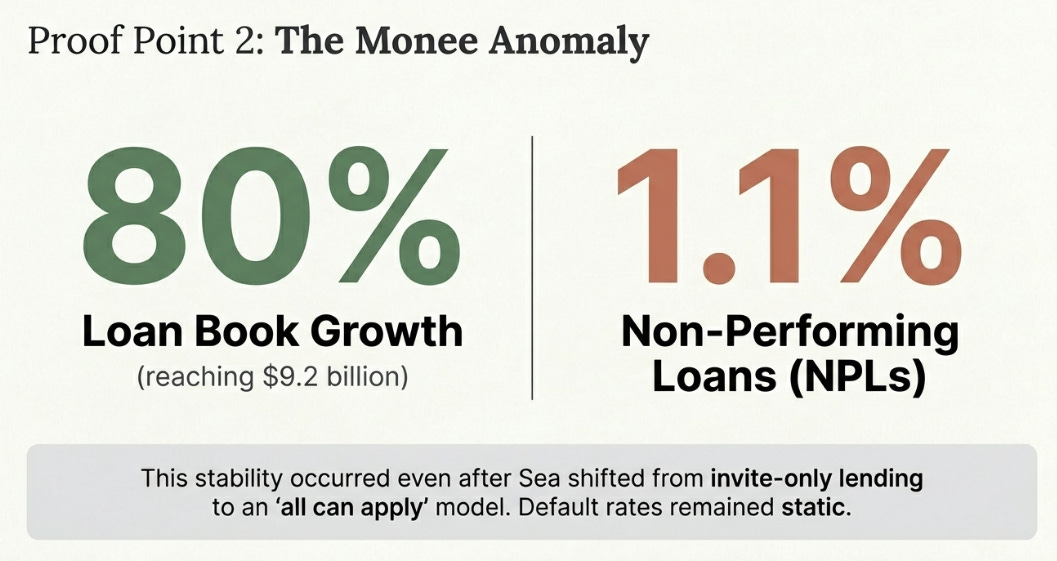

Monee’s loan book grew 80% to $9.2 billion. NPLs held at 1.1%. Sea shifted from invite-only lending to “all can apply”, opened the doors to everyone, and default rates didn’t move.

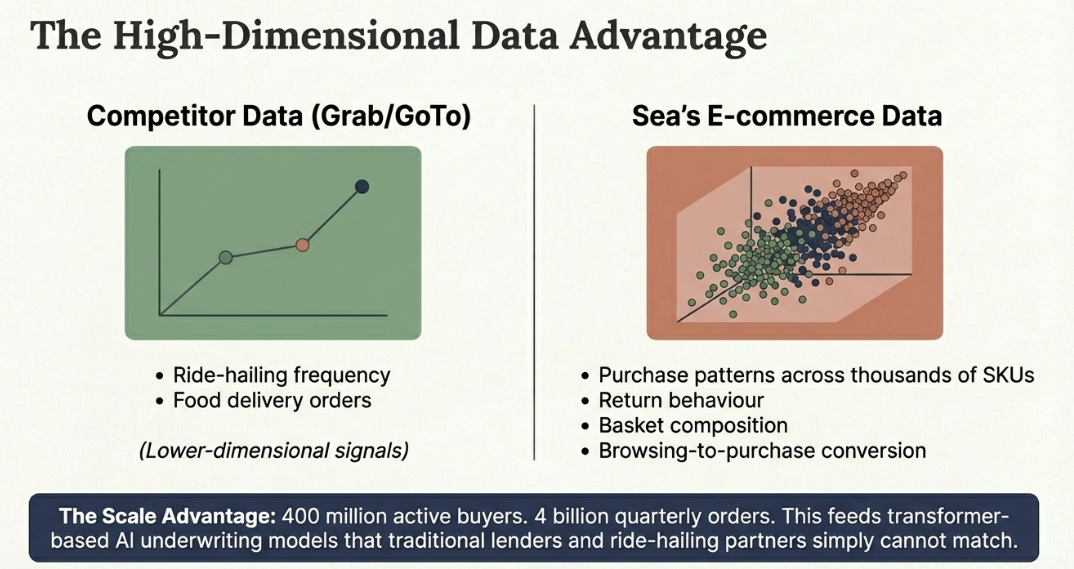

The natural question is why. Management points to Shopee’s transaction data feeding AI underwriting models that see things traditional lenders cannot, purchase patterns, return behavior, payment timing, browsing history, processed through transformer-based models trained on long-sequence behavioral data.

Grab has ride-hailing data. GoTo has Tokopedia. Why can’t they build this?

E-commerce transaction data is categorically different from ride-hailing data for credit underwriting. Purchase patterns across thousands of SKUs, return behavior, basket composition, browsing-to-purchase conversion, these are higher-dimensional signals about financial behavior than trip frequency or food delivery orders. Sea has this data at a scale no partnership can replicate, 400 million active buyers, 4 billion quarterly orders, because no partner would share transaction-level data at that granularity.

Permanent? No. Structural for 5-7 years in underdeveloped credit markets? Yes.

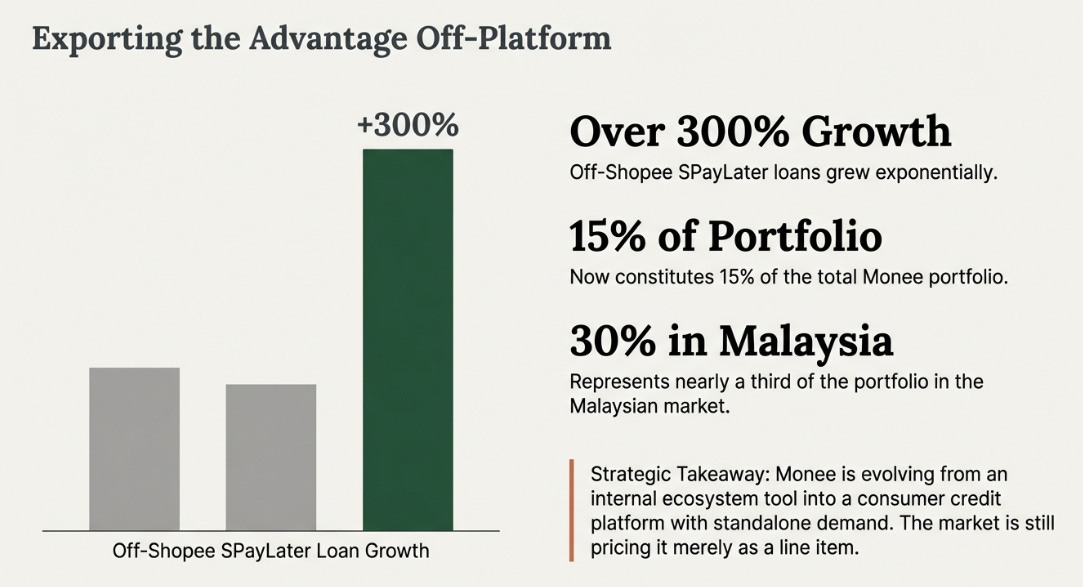

What shifts the framing is off-Shopee SPayLater loans, up over 300%, now 15% of the total portfolio. In Malaysia, 30%. Monee is becoming a consumer credit platform with standalone demand, built on a data advantage incubated inside the ecosystem but now being exported beyond it.

In Q3 I described Monee as evidence that the ecosystem worked. Better to say: Monee may be the part of the ecosystem that eventually generates the most value, and the market is still pricing it as a line item.

The Three-Year Question

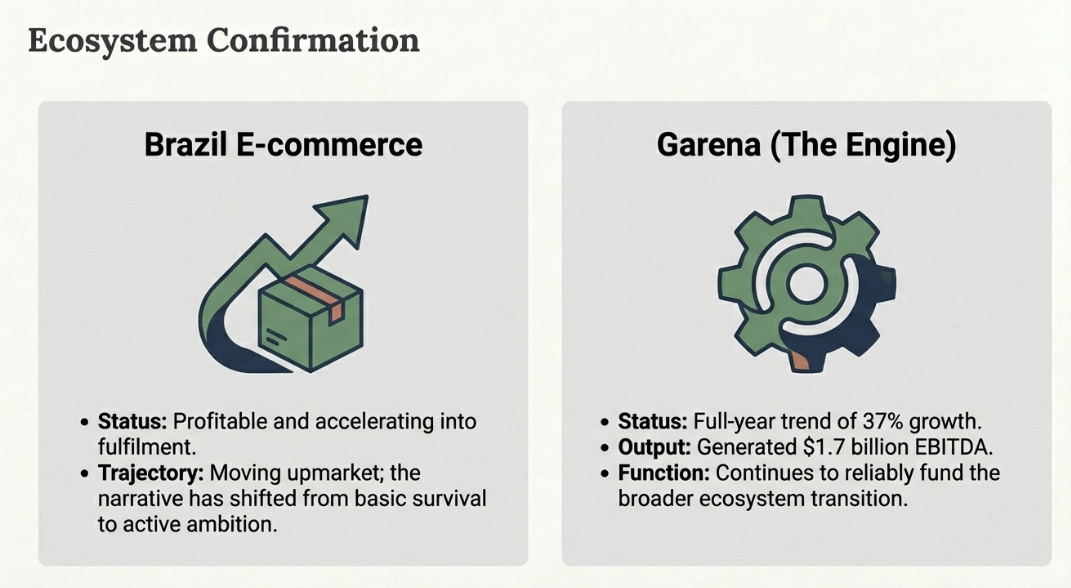

Brazil and Garena confirm the broader pattern. Brazil is profitable, accelerating into fulfillment, and moving upmarket, the question has shifted from survival to ambition. Garena’s Q4 bookings fell 20% sequentially because Q3 stacked two massive IP events in one quarter; the full-year trend of 37% growth and $1.7 billion EBITDA is what matters for the funding thesis. Neither changed the picture.

The three-year question is simpler and harder: does integration density convert to margin?

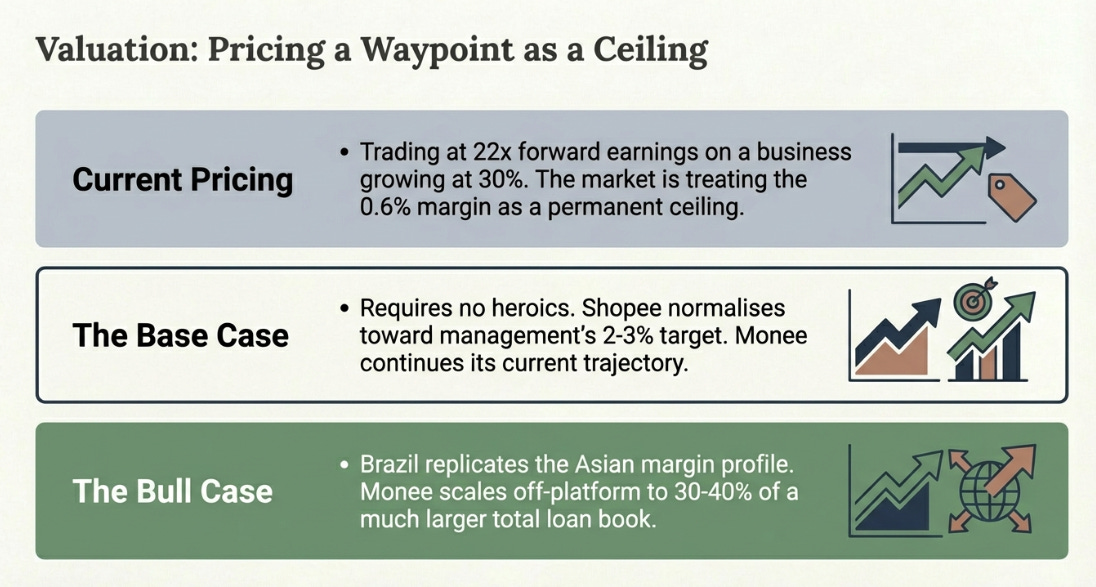

If it does, if the infrastructure creates durable advantages that compound and eventually require less incremental investment, then Shopee margins expand as the investment cycles end. Monee keeps compounding on proprietary data. Garena funds the transition. Sea generates $7-8 billion in EBITDA on $40-45 billion in revenue by 2028. That gets you to roughly double the current price. The bull case, Brazil replicating Asia’s margin profile, Monee scaling off-platform to 30-40% of a much larger book, gets meaningfully higher.

If it doesn’t, if competitors find ways around the physical moat, if the investment cycles prove perpetual, if a credit downturn exposes the underwriting as less robust than it appears, then Sea is a fast-growing company that never becomes highly profitable, and the current price is approximately fair.

The base case requires nothing heroic. Shopee margins normalize toward the 2-3% target management has reiterated for two years. Monee keeps doing approximately what it is already doing. That is a bet on continuation, not acceleration.

At 22 times forward earnings on a business growing 30%, markets price Sea as if the margin compression is permanent. The market treats 0.6% as a ceiling. I think it is a waypoint. I held that view three months ago. The waypoint was further away than expected.

The Choice

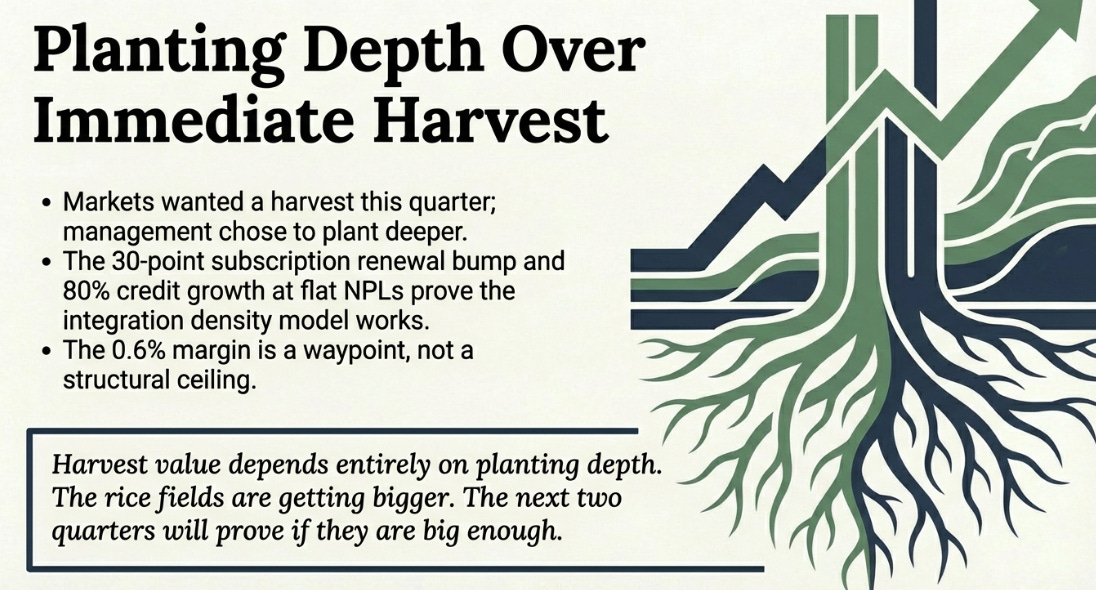

Markets wanted harvest this quarter. Management looked at what they are building, looked at the levers they discovered over the past year, and decided the fields were not ready. Frustrating for the impatient. Correct for anyone who believes harvest value depends on planting depth.

I am less confident about timing than three months ago. More confident about the payoff itself, because the evidence of what integration density produces, 30 points of improved subscription renewal, stable credit quality at 80% loan growth, a take rate that keeps climbing, got materially stronger.

The open question: is integration density durable, or a temporary lead that erodes as competitors build their own stacks? The next two quarters matter more than any model.

The rice fields are getting bigger. The question is whether they are big enough.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.