ServiceNow 1Q26: More Control, Less Conviction

The company delivered stronger AI and platform signals, but the market is no longer paying for narrative leadership without visible organic reacceleration and a gross-margin floor.

TL;DR

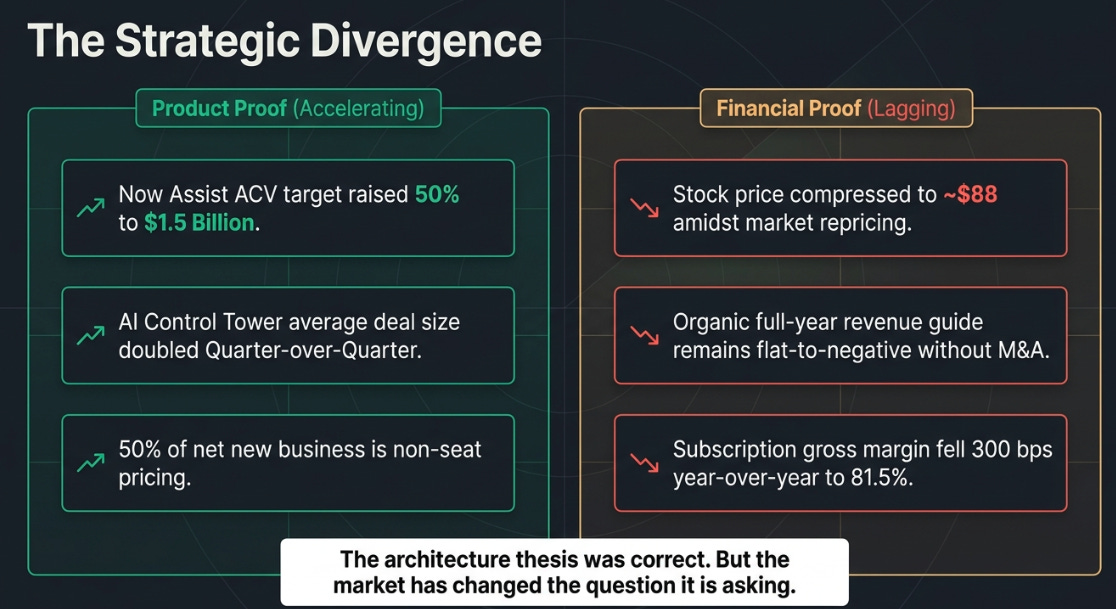

The product story strengthened: non-seat pricing now drives 50% of net new business, AI metrics accelerated, and multi-product adoption deepened.

The financial proof did not: the full-year raise was largely acquisition- and FX-driven, while organic growth and cRPO did not clearly inflect higher.

The real debate is now economic, not architectural: if gross margins stabilize and consumption scales, the bull case survives; if AI costs keep pressuring margins, the stock’s weakness is justified.

The stock kept falling. That has to be where this starts.

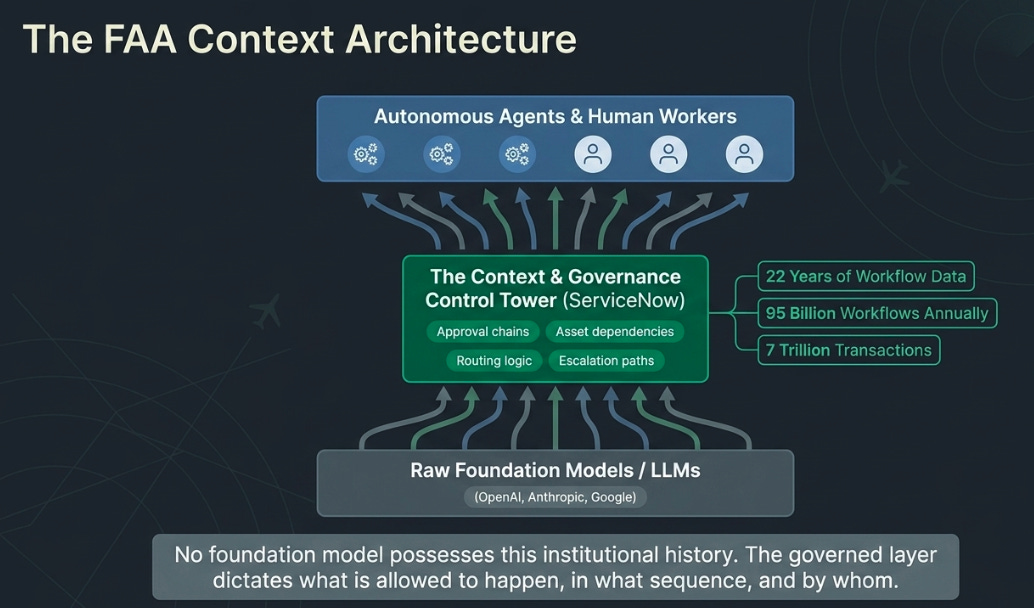

We have been constructive on ServiceNow for over a year, and not for shallow reasons. The thesis was never “good software company, strong management, AI tailwind.” It was more specific than that: as enterprise software shifted from applications used by people to systems coordinating people, data, and increasingly autonomous agents, the scarce layer would not be the model itself, and not even the application. It would be the governed layer that knows what is allowed to happen, in what sequence, by whom or what, against which systems, under which rules. ServiceNow looked increasingly like that layer. We called it the FAA of enterprise AI, the mandatory control tower for crowded airspace.

The product evidence has gotten stronger with every quarter we have covered. The stock has gone in the opposite direction. That gap is not a footnote; it is the subject of this article.

The instinct is to say the market is wrong. I do not think that is quite right. I think the market changed the question it is asking, and ServiceNow has not yet provided a conclusive answer to the new one. Understanding that shift, and whether this quarter moved the answer closer, is more useful than relitigating whether the architecture thesis was correct. It was. That is not the point anymore.

The old question and the new one

For most of the past decade, the question the market asked ServiceNow was straightforward: is this a high-quality enterprise software company that can sustain 20%+ growth at scale? The answer was consistently yes. Premium multiple. The stock compounded accordingly.

Starting in early 2026, the question changed. The SaaSpocalypse, roughly $2 trillion wiped from enterprise software in four months, reflected something deeper than a rotation or a rate scare. It reflected genuine uncertainty about whether AI agents fundamentally impair the per-seat economics that made these companies valuable in the first place. The new question became sharper and less forgiving:

Does AI make your business model bigger or smaller? Prove it with organic numbers, not architecture slides.

That is a harder question. It is also the right one. And the uncomfortable truth is that ServiceNow has not yet provided a conclusive answer.

The company has provided extraordinary directional evidence. Half of net new business is non-seat. Now Assist ACV was raised 50% to $1.5 billion. Autonomous Workforce resolves 90% of internal IT cases. AI Control Tower deal sizes doubled quarter-over-quarter. These are real, measurable, accelerating proof points that the platform is becoming more central as AI proliferates.

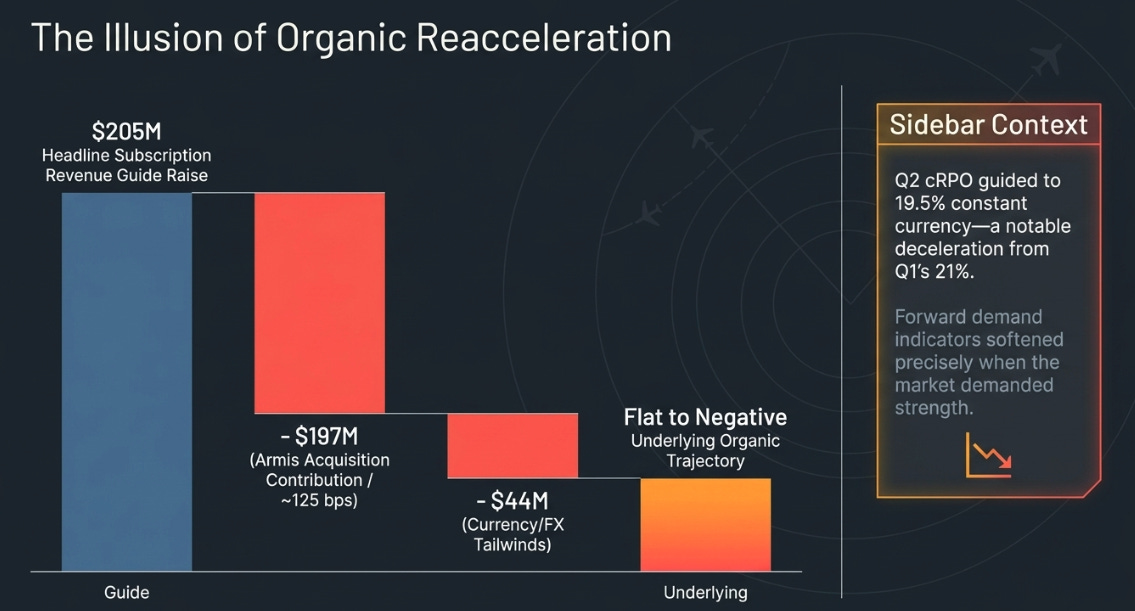

But the market is no longer asking whether the platform is becoming more central. It is asking whether that centrality translates into organic financial acceleration. This quarter, the organic full-year guide did not move. The $205 million raise at the midpoint decomposes into roughly $197 million from Armis and roughly $44 million from currency tailwinds. Strip those out and the underlying trajectory is flat to slightly negative.

That is the gap. Not between our thesis and reality, between the question ServiceNow is answering and the question the market is asking.

The fundamental question

Before looking at any numbers from Q1, it is worth asking the only question that actually determines whether $88 is a buying opportunity or a fair price for a business whose old economics are being questioned:

As AI agents spread through the enterprise, does ServiceNow become more valuable because more work needs to be routed, approved, secured, and audited through one governed layer, or does AI hollow out the seat-based and human-workflow economics faster than ServiceNow can monetize the new activity?

That question is better than “did they beat?” or “is Armis dilutive?” because it explains why the company can be strategically stronger and the stock can still be correctly weak. Both can be true simultaneously, and both were true this quarter.

Start with why the mechanism should work. What changed in the world is straightforward: enterprises are moving from software used by people to systems coordinating people, agents, and data across dozens of tools. That transition should make ServiceNow’s core capability more valuable, because ServiceNow’s value has never really been that it owns the best model or the prettiest interface. Its value is that it knows what an enterprise is actually trying to do, and how that work is supposed to happen. Approval chains, permissions, asset dependencies, compliance steps, routing logic, escalation paths, workflow context, that is the operating knowledge that turns raw intelligence into governed action. Twenty-two years of workflow data. Ninety-five billion workflows annually. Seven trillion transactions. No foundation model has that. No one is going to rebuild it from scratch.

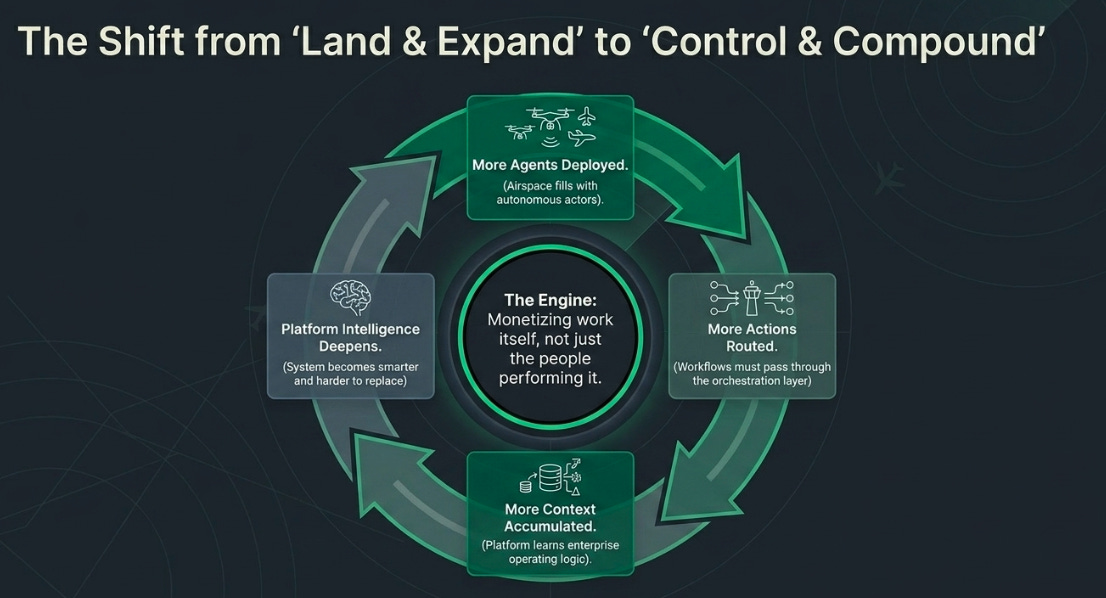

The compounding loop follows naturally. More agents deployed means more actions taken. More actions mean more workflows routed through the orchestration layer. More workflows mean more context accumulated. More context makes the platform smarter and harder to replace. This is what management described as “control and compound” replacing “land and expand.” The control tower becomes more essential, not less, as the airspace fills with autonomous actors.

That loop breaks in one of two ways.

The first is strategic. If foundation model providers, OpenAI, Anthropic, Google, build their own enterprise context layers, they could eventually route work directly to systems without needing ServiceNow’s governance. Agents would govern themselves. The tower would become unnecessary. I think this is unlikely in the medium term, because enterprise context is not a model problem; it is a data and process problem built over decades of institutional history. But it is worth naming.

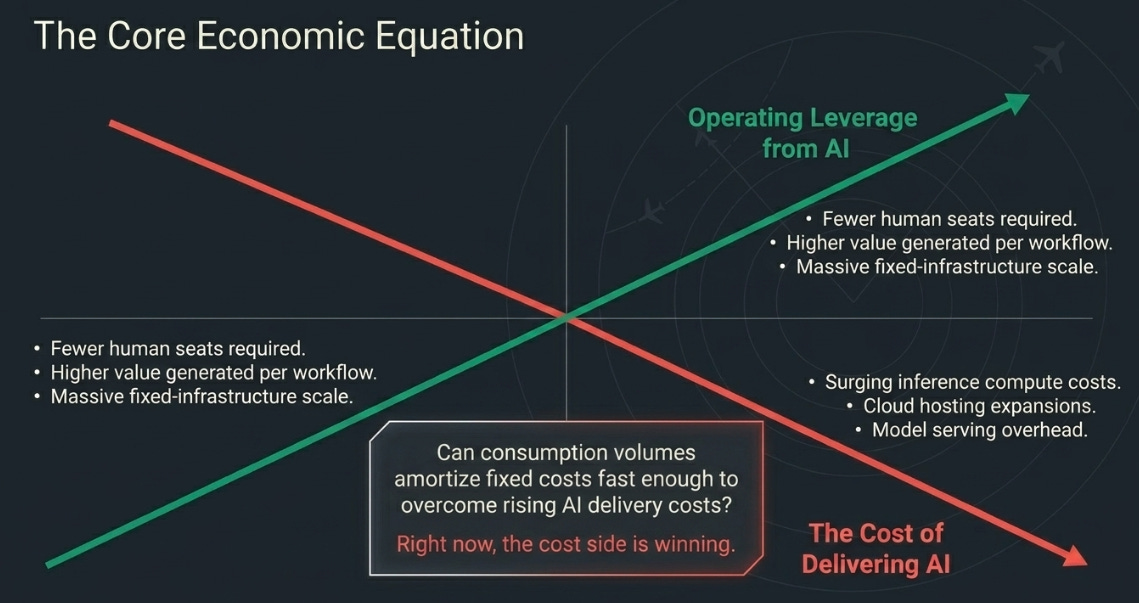

The second is economic, and it is the one this quarter surfaced as a genuine concern. If AI-generated work is real but structurally less profitable than the old seat-based model, if the cost of delivering governed AI workflows permanently exceeds the revenue premium customers pay, then the control tower works but does not generate profit at scale. The mechanism operates. The business model does not compound. ServiceNow becomes more important and less valuable at the same time.

That second failure mode is not theoretical. It shows up in the gross margin line. And that is what makes Q1 interesting.

What Q1 confirmed and what it did not

The quarter delivered two categories of evidence that need to be held side by side, because the tension between them is the entire story.

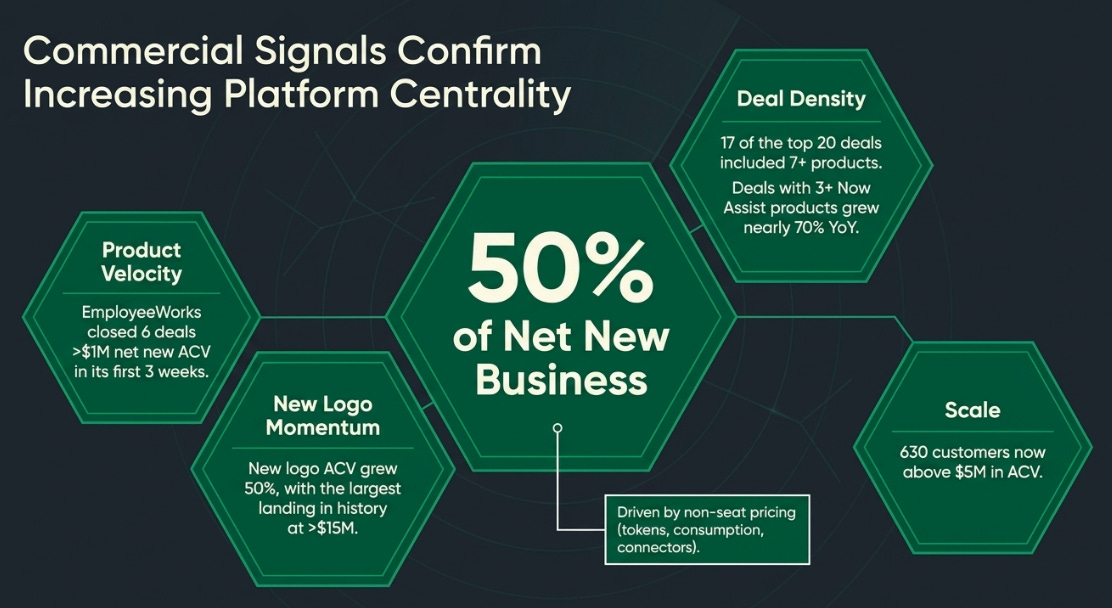

The product case is the strongest it has ever been. Start with the most important disclosure: 50% of net new business now comes from non-seat-based pricing, tokens, consumption, infrastructure, connectors. This may be the most strategically significant metric ServiceNow has reported in this cycle. The entire SaaSpocalypse thesis rests on the assumption that AI agents compress human seat counts and therefore compress SaaS revenue. ServiceNow just told the market that half of its new business no longer depends on that model. The company is monetizing work itself, governed activity across humans, agents, and systems, rather than merely the people performing it.

The rest of the quarter reinforced that reading. Now Assist customers spending more than $1 million in ACV grew more than 130% year-over-year. The company’s AI target for 2026 moved from $1 billion to $1.5 billion, a 50% increase, with management stressing the methodology still captures only the incremental AI contribution. McDermott disclosed this on the earnings call, pre-empting what was supposed to be a Financial Analyst Day headline. You do not burn your investor day surprise on a Wednesday call unless you are worried about the stock reaction and confident you have more to share at the main event.

EmployeeWorks, which came from the Moveworks integration completed barely three weeks before launch, closed six deals above $1 million in net new ACV in its first quarter, more than Moveworks closed in all of FY2025. AI Control Tower average deal size more than doubled quarter-over-quarter. Deals including three or more Now Assist products grew nearly 70% year-over-year, including 36 deals with five or more products. Seventeen of the top 20 deals included seven or more products. The company finished the quarter with 630 customers above $5 million of ACV. New logo ACV grew 50%, with the largest new customer landing in company history at over $15 million.

These are not aspirational metrics. They are commercial signals. They suggest ServiceNow is not merely attaching AI to existing contracts but using AI to increase platform density, deepening the control-plane architecture inside enterprises that are already committed.

The financial case remains messy. The full-year subscription revenue guide was raised $205 million at the midpoint. That sounds good until you decompose it. Armis contributes approximately 125 basis points to Q2 and full-year subscription revenue growth, as well as to Q2 cRPO growth. Currency provides a further tailwind. The organic raise, the part reflecting the actual underlying momentum of the business without acquisition help, is flat to slightly negative despite the Q1 beat.

Q2 cRPO was guided to 19.5% constant currency. That is a deceleration from Q1’s 21%. Management noted that a portion of Armis customer contracts include termination-for-convenience provisions, which limit how much contract value flows into cRPO. That makes the comparison imperfect, but the headline optic, the forward demand indicator softening in a quarter where the market desperately wanted to see it strengthen, is damaging regardless.

Q1 also absorbed an approximately 75 basis point headwind from delayed large on-premise deals in the Middle East, which management attributed to the ongoing conflict in the region and said had begun closing in Q2. That explains some of the shortfall against the buy-side whisper number but does not change the forward picture.

Now here is what I think is the most important and least discussed aspect of the quarter.

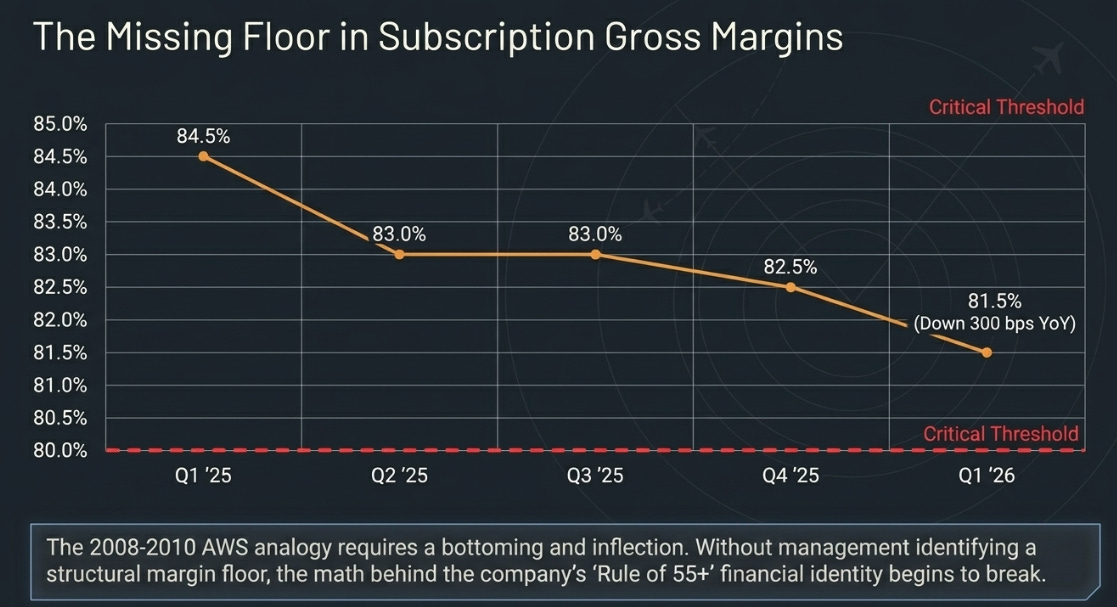

Non-GAAP subscription gross margin fell to 81.5%, down 300 basis points year-over-year. The trajectory tells the story: 84.5% in Q1 2025, 83% in Q2, 83% in Q3, 82.5% in Q4, 81.5% in Q1 2026. Full-year 2026 guidance holds it at 81.5%, which includes another 25 basis points of drag from Armis.

In prior articles, I compared this compression to AWS in 2008-2010, a deliberate investment phase, compressing margins during land-and-expand with the bet that operating leverage follows as usage compounds. I said to watch for stabilization at 82-83%. It did not stabilize. It kept falling.

This matters enormously because the fundamental mechanism only works if AI workflows are profitable at scale. The control tower thesis assumes that the marginal cost of routing an additional workflow through an existing context engine is low, that governance and orchestration generate high-margin revenue because the hard infrastructure is already built. But the actual cost of delivering AI, inference compute, cloud hosting, model serving, is showing up in the gross margin line and going the wrong direction.

The core question is whether the operating leverage from AI (fewer humans needed, more automation, higher value per workflow) eventually overcomes the cost-of-goods increase from delivering AI (more compute, more inference, more cloud capacity). Right now, the cost side is ahead. Operating margin expanded 100 basis points year-over-year to 32%, but that was driven by opex efficiency, not gross margin improvement. If subscription gross margins keep compressing 150-200 basis points annually without bottoming, the math behind ServiceNow’s “Rule of 55+” profile, the combination of revenue growth and profitability that defines its financial identity, begins to break.

The AWS analogy requires a bottoming and inflection. AWS margins eventually stabilized because per-unit compute costs declined while consumption volumes scaled across the fixed infrastructure base. ServiceNow’s version of this requires AI inference costs to come down, plausible, given the trajectory of model efficiency, and consumption volumes to reach a scale where the platform’s fixed costs are amortized across enough transactions to restore margins. I still think this is likely. But I am less certain about timing than I was six months ago, and the trend gives the bears more to work with than I previously acknowledged.

If Q2 gross margins fall below 80% with no management framework for where they bottom, I would materially reassess the economic thesis. That is the specific threshold.

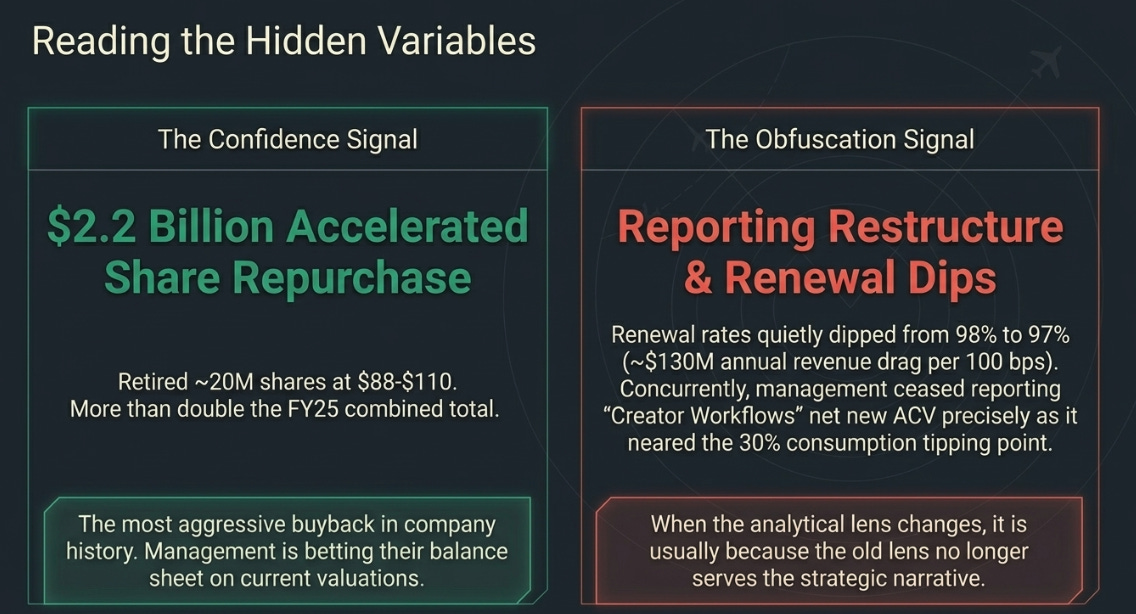

One other metric slipped through quietly. The renewal rate dipped to 97% from 98%, and management said nothing about it in prepared remarks. On a $13 billion+ subscription base, each 100 basis points represents roughly $130 million of annual revenue. The Q3 2025 dip to 97% was explained as a single large federal agency closure. This quarter’s dip was not explained at all. Ninety-seven percent is still extraordinarily high. The silence around it is what is notable.

Reading between the lines

Two decisions management made this quarter reveal more than the numbers.

First, ServiceNow changed how it reports net new ACV contribution, from product-level breakdowns (ITSM, ITOM, HRSD) to workflow-level breakdowns (Technology Workflows, CRM & Industry, Core Business, Creator). The company explicitly noted the two are “not comparable.” In my Q3 article, I tracked Creator Workflows at 23% of net new ACV and flagged 30% as the consumption tipping point. That metric is now gone. When a company changes the analytical lens, it is usually because the old lens no longer serves the strategic narrative. ServiceNow wants investors to evaluate it as a platform, not a collection of software modules. That is consistent with the control-plane thesis. It also means we lost the single best consumption-tracking metric at exactly the moment it mattered most.

Second, ServiceNow executed a $2.2 billion accelerated share repurchase in Q1, more than double what it repurchased in all of 2025 combined. The company retired approximately 20 million shares. That is the most aggressive buyback in ServiceNow’s history, executed at prices between roughly $88 and $110. Management is betting their own balance sheet at these levels. It does not guarantee the stock goes up. It tells you what the people with the most information think about value.

What we got right and what we got wrong

This is the section the article has to earn, and it should be brief.

What we got right was the strategic direction. ServiceNow does appear to be building something more important than a premium workflow SaaS franchise with AI features. The product evidence, the M&A logic, the disclosure evolution, the hybrid monetization shift, the multi-product deal density, the emphasis on context and governed execution, all of it points toward a company trying to move up a layer in the enterprise stack. I still think that is the right way to read the company.

What we got wrong was the speed at which that architecture story would become a stock story. We treated the category transition as if it should already command a new valuation framework. The market kept insisting on a more prosaic standard: show me clean organic acceleration, show me margins that make sense, show me a model investors can underwrite without mentally stripping out half the bridge. That is not the market being foolish. That is the market asking the bridge question before it pays for the destination.

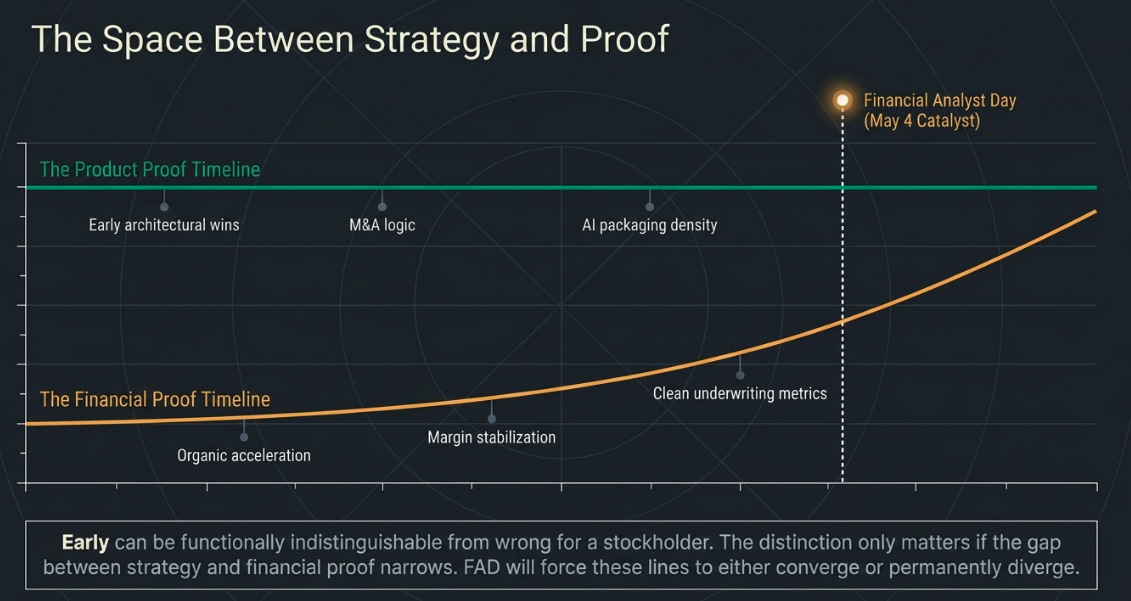

Early can be functionally indistinguishable from wrong for a stockholder. The distinction only matters if the thesis continues to gain strategic support while the gap to financial proof narrows over time. If it does not narrow, then “early” was just the polite word for an incorrect call.

The stock can stay weak even if the thesis is right. Product proof can lead financial proof by multiple quarters. Margin pressure can arrive before operating leverage does. Transitions are mispriced in both directions, bulls assume the market will recognize the new story quickly, bears assume the old economics are simply deteriorating, and reality is often that both are true for a while.

That is the regime ServiceNow is in.

Where we come out

The thesis is not broken. It is unproven on the market’s terms.

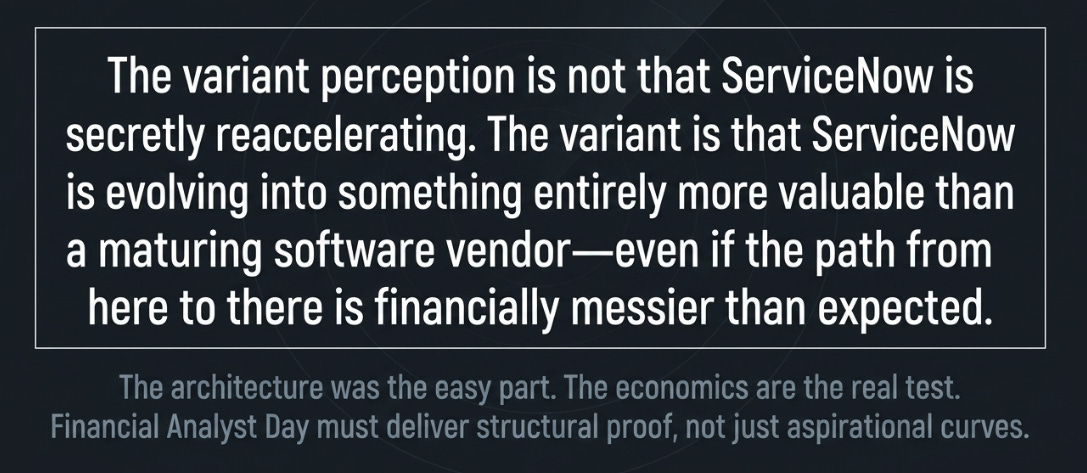

The variant perception remains that the market sees a maturing software company using M&A and AI rhetoric to soften deceleration. What I think is actually happening is more interesting: ServiceNow is in the middle of a genuine business-model transition, moving from monetizing workflow software through seats to monetizing governed activity across humans, agents, and systems. That transition is visible in the 50% non-seat mix, in the AI-native packaging across all tiers, in the infrastructure-like pieces (data fabric, context engine, security, orchestration), and in the types of commercial wins management now highlights. The variant is not that ServiceNow is secretly reaccelerating. The variant is that ServiceNow may be evolving into something more valuable than a maturing software vendor, even if the path from here to there is financially messier than bulls, including us, expected.

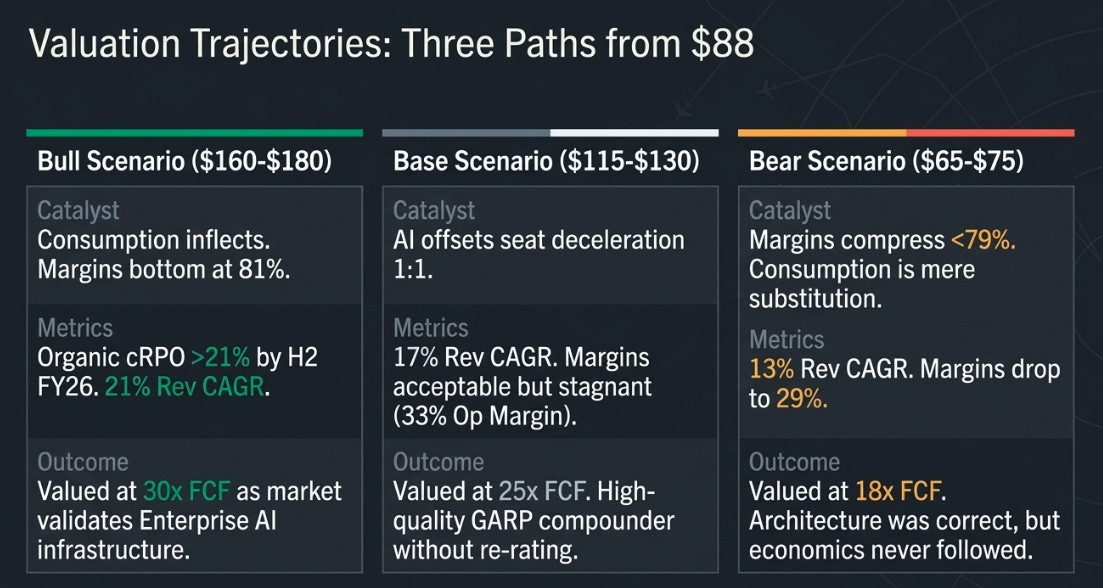

Three paths from $88 over three years:

Bull ($160-180): Consumption inflects. Organic cRPO re-accelerates above 21% constant currency by H2 FY26. Subscription gross margins bottom at 81% and stabilize as inference costs decline and consumption volumes create leverage. Armis and Veza deepen platform economics. Revenue compounds at 21% through FY28, operating margins expand to 35%, free cash flow margins reach 38%. Valued at 30x FCF. Requires the AWS analogy to finally validate and the market to begin evaluating ServiceNow as enterprise AI infrastructure, not maturing SaaS.

Base ($115-130): AI offsets seat deceleration roughly one-to-one. Organic growth settles in the high teens. Margins stay acceptable but do not expand meaningfully. ServiceNow becomes a high-quality GARP compounder without re-rating. Revenue compounds at 17%, operating margins hold at 33%, valued at 25x FCF. This is the “right strategy, delayed payoff” outcome.

Bear ($65-75): Gross margins continue compressing below 79%. AI delivery costs are structural, not cyclical. The consumption transition looks more like substitution than expansion. Microsoft bundles orchestration through Power Automate. Revenue growth settles at 13%, margins compress to 29%, valued at 18x FCF. This is the outcome where the architecture was correct but the economics never followed.

I do not think the bear case is the most likely one. But I understand it better after this quarter than I did before.

What to track:

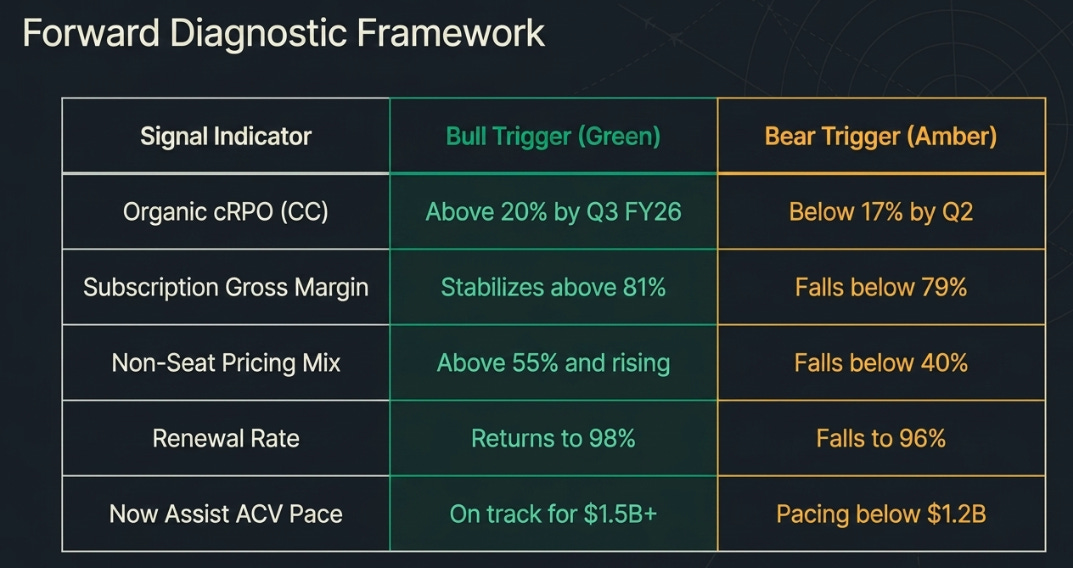

The near-term catalyst is Financial Analyst Day on May 4. Management has explicitly deferred the long-range plan, consumption flywheel curves, margin expansion trajectory, and SBC roadmap. What FAD must deliver to change the conversation: a specific organic growth framework for FY27 showing re-acceleration, a subscription gross margin bottoming target with structural reasoning, and consumption revenue curves that show when the deployment-to-usage inflection arrives. If FAD is specific and quantitative, the proof gap begins to close. If it is aspirational, the gap becomes permanent and the stock finds a lower floor.

The question that matters now

ServiceNow’s Q1 did not settle the debate. It clarified it.

The company looks more strategically important than it did a year ago. That is not a small point. The product evidence, the architectural positioning, the commercial signals, they are all better, not worse. The idea that ServiceNow is becoming the governed execution layer for enterprise AI is more plausible after this quarter than before it.

But the stock is not paid on plausibility. The market is asking for proof that the company’s growing strategic centrality will show up in organic growth, in margins that hold, in a model investors can underwrite without stripping out acquisitions and currency to find the real number underneath.

The question used to be whether ServiceNow was a great software company. That was easy. The question now is whether AI makes the model bigger or smaller, and ServiceNow’s product metrics say bigger while its financial metrics say: not yet, not cleanly, not organically.

That gap is uncomfortable. It is also exactly where the most interesting investment opportunities tend to live, in the space between a thesis that is directionally right and a market that refuses to pay for direction without proof.

We were early on the strategy. We were early in the wrong way on the stock. The open question is whether that gap narrows from here, or whether the stock has been telling us all along that the architecture was the easy part and the economics are the real test.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.