Snowflake 1Q27 Earnings: Second Interface Collapse

We were early on the architecture and uncertain on the conversion. The data started catching up.

TL;DR

Snowflake’s Q1 FY2027 shifted the AI debate from “disintermediation risk” to “consumption accelerator,” with product revenue up 34%, NRR at 126%, and guidance raised by more than the quarterly beat.

CoCo is the key architectural change: not just an AI product, but a new interface layer that compresses migrations, expands who can build on Snowflake, drives platform consumption, and improves Snowflake’s own operating leverage.

The thesis is stronger but less asymmetric at $240: Snowflake now looks fairly priced as a premium AI-enabled data platform, with further upside depending on whether CoCo/CoWork adoption, NRR, gross margins, and AI monetization prove durable over the next two quarters.

In December 2025, after Snowflake reported its third quarter, I wrote that the most important number in the print wasn’t product revenue growth of 29%, it was the 800-basis point gap between RPO growth and revenue growth. Enterprises were committing faster than they could deploy. “The ‘slowing growth’ narrative,” I argued, “has about two quarters left to live.”

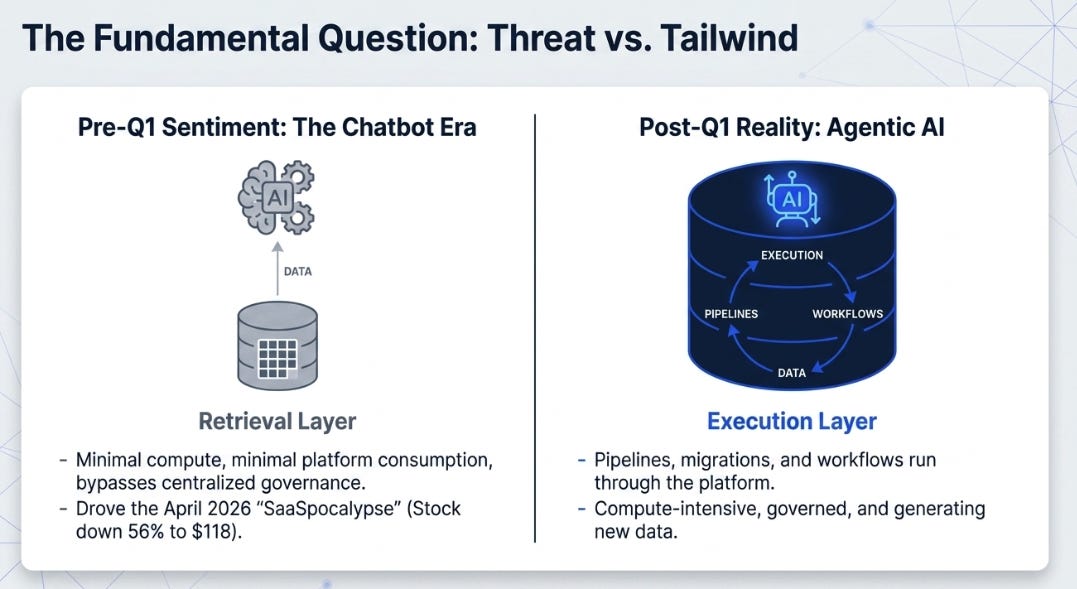

The stock dropped 8%. By April 2026, it had fallen to $118, down 56% from year-end. The software sector was in what trading desks called the “SaaSpocalypse.” Forward P/E multiples fell below the S&P 500 for the first time in history. Capital rotated from cloud into AI infrastructure and industrials. The market’s thesis was structural and specific: agentic AI would disintermediate data platforms entirely. If agents could query and act on enterprise data directly, why would anyone need a centralized warehouse with governance, permissions, and audit trails?

The uncomfortable part was that our architectural thesis made sense before the numbers confirmed it. Data sharing networks were scaling. The Anthropic partnership embedded models inside the governance perimeter, an architectural statement that models should operate inside Snowflake’s security boundary, not beside it, and harder for competitors to replicate than simply offering access to the same model. Nine-figure deals kept arriving, including one worth $400 million. But net revenue retention sat flat at 124–125% for three quarters, hard to reconcile with a platform acceleration narrative. The initial FY27 guide of 27% growth felt like managed deceleration. A thesis built on architecture without consumption proof is just a story the market has no obligation to believe.

What held us anchored were commitment signals the stock price couldn’t see: the RPO gap, the unprecedented deal sizes, and a governance architecture that became more valuable as AI raised the stakes of data access and auditability. But anchored is not the same as certain.

Then Snowflake reported Q1 FY2027, and the consumption evidence arrived.

The Fundamental Question

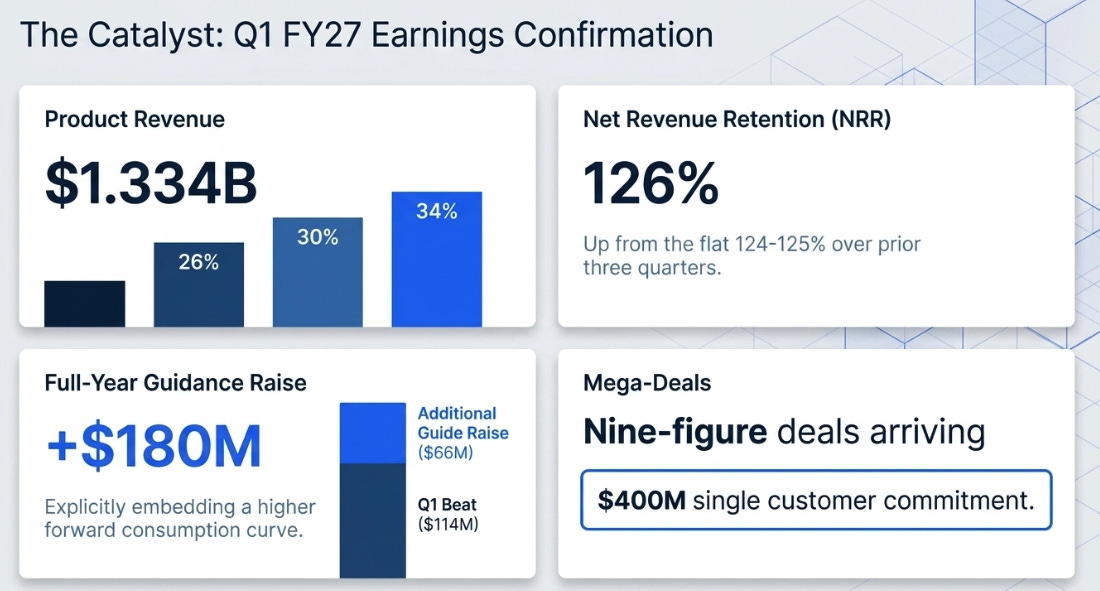

Product revenue of $1.334 billion, up 34% YoY, accelerating from 30% last quarter and 26% a year ago. Net revenue retention at 126%. Full-year guidance raised by $180 million to $5.84 billion. The stock moved 36% in a session.

The numbers are good. They are not the point. The point is what they reveal about a question that has been building for eighteen months: does AI consumption compound on top of data platform consumption, or substitute for it?

The chatbot era of AI was a retrieval layer that sat above the data platform. A user asked a question, a model answered, done. Minimal compute, minimal platform consumption, minimal strategic significance for Snowflake. Agentic AI is structurally different. When an agent builds a pipeline, deploys a workflow, executes a migration, or launches a monitoring process, those actions run through the data platform, compute-intensive, sustained, and generating new data and governance requirements that feed back into the platform. This distinction explains how the same underlying technology could first appear as a threat and then become a tailwind.

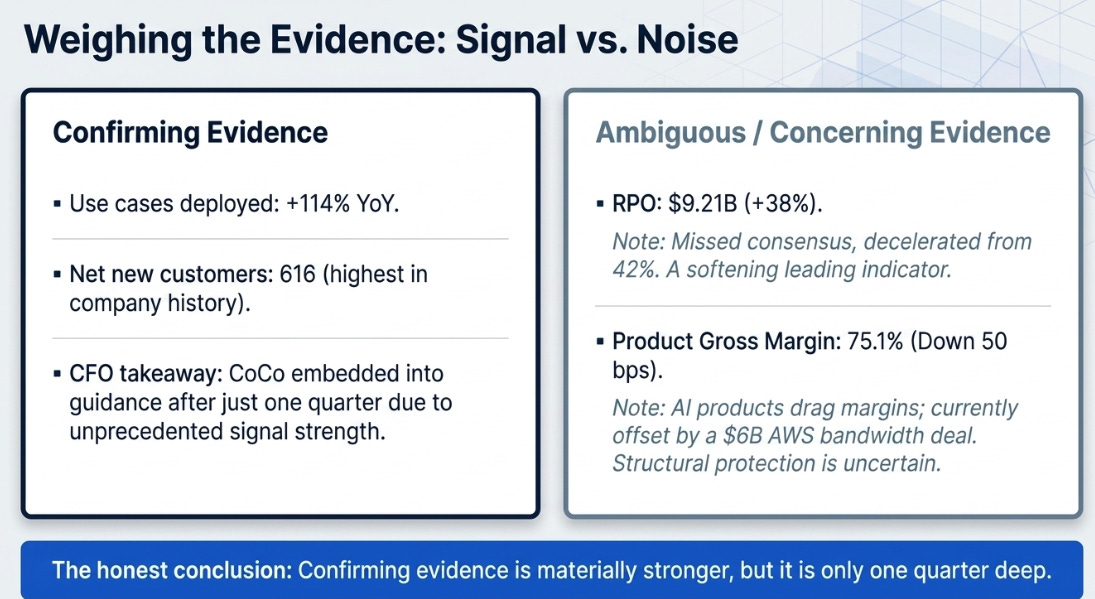

The confirming evidence is strong. Growth re-accelerated by 800 basis points in a single quarter. The $180 million guidance raise exceeded the Q1 beat by $114 million, management embedded a higher forward consumption curve, not just a flow-through. CFO Brian Robins said Cortex Code was “the largest driver to the increase in our forecast.” Use cases deployed on the platform increased 114% YoY. Net new customers of 616 were the most in company history. Snowflake usually waits for multiple quarters of consumption evidence before embedding new products into guidance; CoCo was embedded after one quarter because the signal was strong enough.

The ambiguous evidence requires attention. RPO of $9.21 billion grew 38% but missed consensus and decelerated from 42%. RPO was the leading indicator in my Q3 piece, the clue that commitments were outrunning consumption. Now that revenue has accelerated, the clue is less central but not irrelevant. A softening leading indicator alongside an improving lagging indicator is a mixed signal, not a clean one. Management says bookings are increasingly Q4-weighted, which is plausible but also convenient.

The concerning evidence centres on product gross margin: 75.1%, down 50 basis points. Management acknowledged AI products carry lower margins and said they are offsetting the drag with a $6 billion AWS bandwidth deal. Robins’s phrase, “committed to find efficiency to maintain 75%”, implies active management, not structural protection. The risk is that investors celebrate AI-driven growth before understanding whether it is high-quality growth. If AI crosses 20% of the product mix within the next eighteen months, which the adoption trajectory suggests is plausible, the offset math gets harder.

The honest conclusion: confirming evidence is materially stronger than concerning evidence. But it is one quarter deep.

CoCo Is Not the Product; CoCo Is the Interface

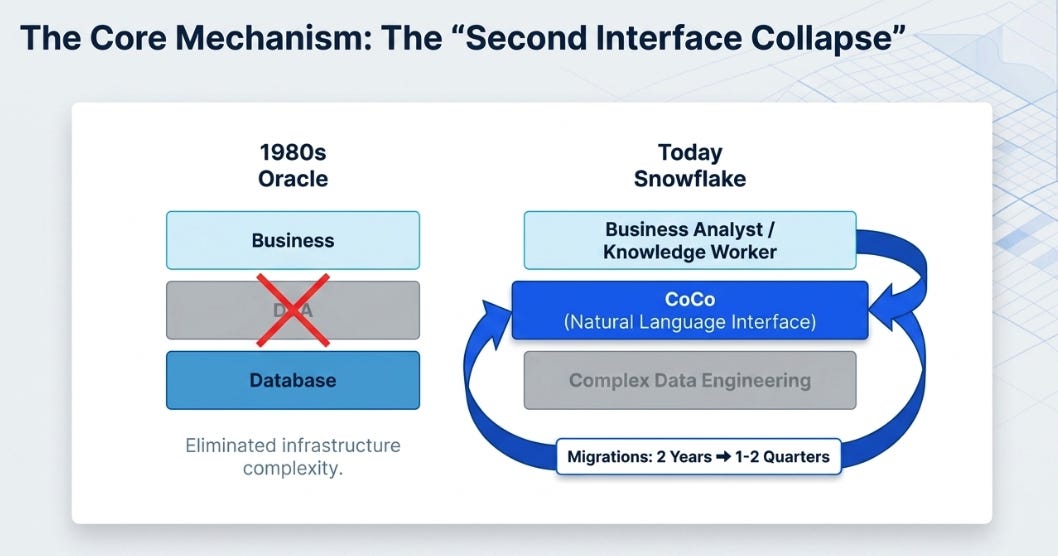

In August 2025, I described a pattern I called “interface collapse”, the elimination of complexity layers requiring specialised knowledge. Oracle won the database wars in the 1980s by making the DBA unnecessary. Snowflake’s first collapse did the same to infrastructure engineers. CoCo is the second collapse: it turns expert data work into natural-language workflows that a much larger population can execute. Migrations that took two years now take one to two quarters. A business analyst who needed an engineering team to build a pipeline can describe what they want and CoCo creates it.

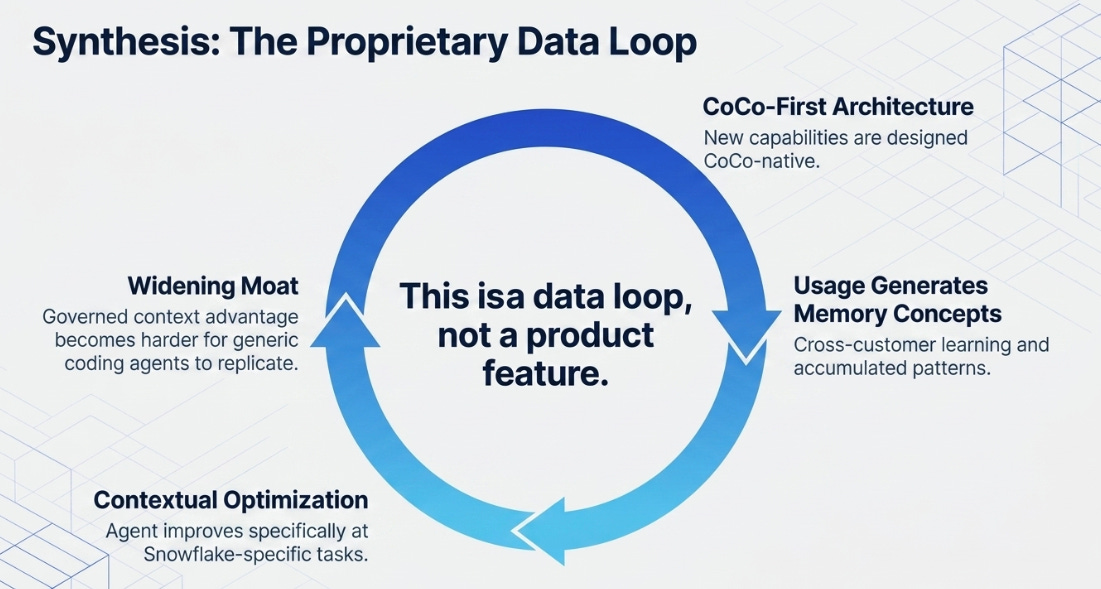

The Investor Day in June revealed an architectural commitment that goes beyond CoCo-as-product. Christian Kleinerman said every new capability must answer: how is the experience simpler with CoCo? Some features will be CoCo-accessible before they get traditional interfaces. Snowflake is building CoCo-first, meaning the proprietary context advantage compounds with every product release, because each release is designed to be CoCo-native. Management calls the accumulated patterns “memory concepts”: cross-customer learning that improves the agent with usage. This is a data loop, not merely a product feature. The more customers use CoCo within Snowflake, the better CoCo gets at Snowflake-specific tasks, and the harder it becomes for generic coding agents to compete on that terrain.

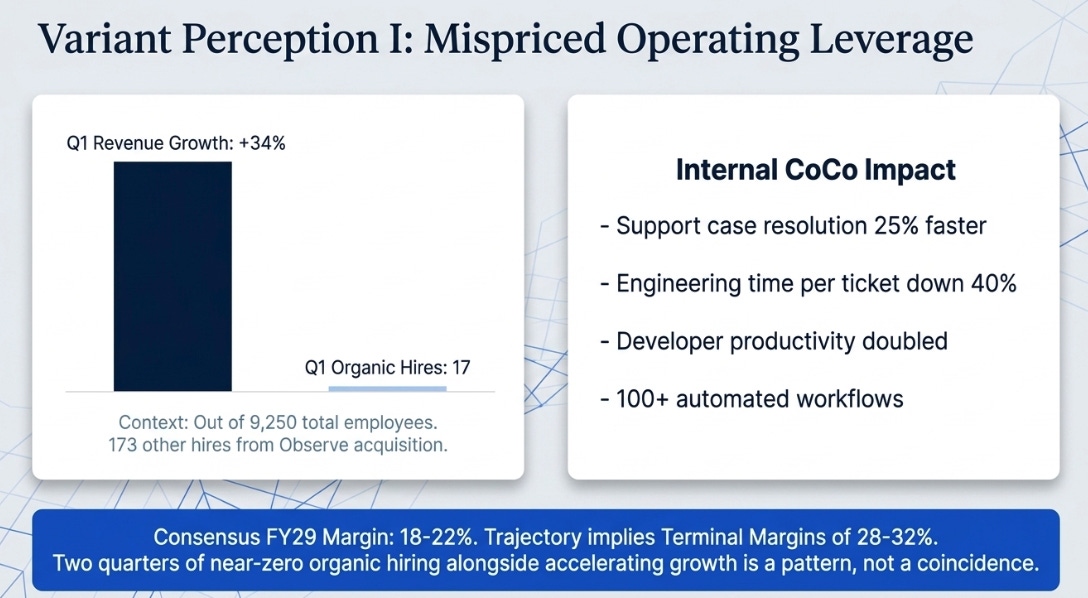

But the most revealing evidence of CoCo’s structural impact was not in the customer metrics. It was in Snowflake’s own headcount. The company added 190 employees in Q1, 173 from the Observe acquisition. Organic hiring was 17. Seventeen people, at a company growing revenue 34% with 9,250 employees.

The internal data explains why: support case resolution 25% faster, engineering time per ticket down 40%, developer productivity doubled, over 100 workflows automated across finance, marketing, sales, and HR. In the Q4 piece, I flagged Robins saying “AI has really changed the framework for investing in growth, it’s no longer tied to headcount.” At the time, that was a forward claim. Q1 made it measurable.

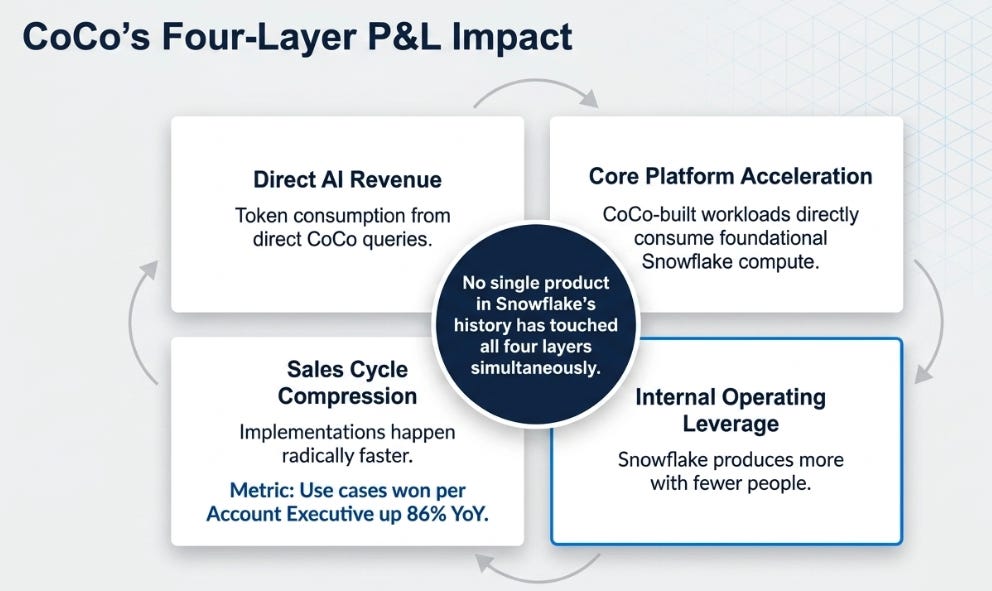

This is where CoCo transcends the “AI product” framing. It operates across four layers of the business simultaneously: direct AI revenue from token consumption; core platform acceleration as CoCo-built workloads consume compute; sales cycle compression as implementations happen faster, with use cases won per account executive up 86% YoY; and internal operating leverage as Snowflake produces more with fewer people. No single product in Snowflake’s history has touched all four layers of the P&L at once. The operating leverage is not a coincidence alongside CoCo, it is a consequence of the same mechanism driving customer revenue.

The counterargument is real. CoCo has been GA for one quarter. Cost governance could throttle adoption, Ramaswamy acknowledged it is “absolutely an issue.” CoWork, the more ambitious business-user agent surface, needs validation through large departmental rollouts before it can be considered proven. The loop is plausible. It is not yet proven durable.

The Variant Perception

The market moved from “AI destroys Snowflake” to “AI helps Snowflake.” Both framings are correct in direction and insufficient in magnitude.

What remains mispriced is the operating leverage, and this is the variant that matters most. Consensus projects roughly 18% non-GAAP operating margin for FY29. The trajectory is already accelerating, 6% in FY25, 10.5% in FY26, 13.5% guided for FY27, and the mechanism is self-reinforcing: better internal AI tools produce more output per person, funding investment in better tools. If the 17-hire dynamic persists across multiple quarters, terminal margins are 28–32%, not 18–22%. Two consecutive quarters of near-zero organic hiring while growth accelerates is a pattern, not a coincidence. No analyst model captures this because the mechanism, AI replacing headcount growth at scale inside a software company, has no precedent in enterprise software. The evidence is early. But it is no longer speculative.

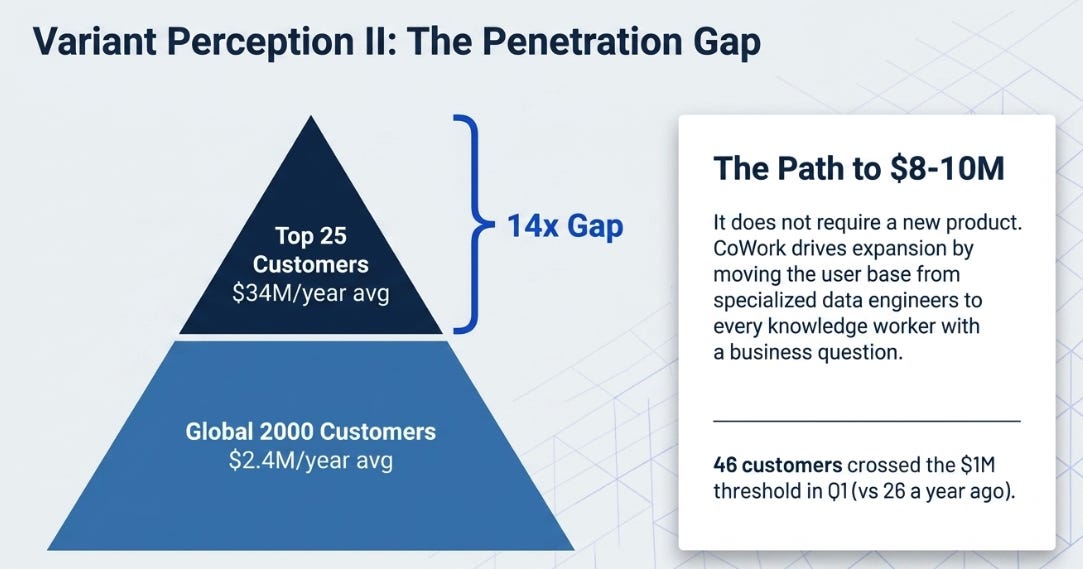

The second mispriced element is underpenetration. Top 25 customers average $34 million in annual spend. G2000 customers average $2.4 million, a 14x gap. CoCo compresses implementation timelines. CoWork, if it achieves departmental scale, expands the user base from data specialists to every knowledge worker with a business question. The 46 customers crossing the $1 million threshold in Q1, versus 26 a year ago, are the leading edge of that expansion. Moving the G2000 average from $2.4 million toward $8–10 million does not require a new product, it requires the existing platform to penetrate deeper inside accounts that have already committed.

What the market prices correctly: the multiple. At 13.6x FY27 EV/Revenue with 89% buy ratings and a $295 consensus target, the repricing from AI victim to AI beneficiary is done.

Three Answers to the Question

The stock is not pricing product revenue growth. It is pricing the answer to one question: does AI make Snowflake more central, merely more useful, or less differentiated? Each answer implies a different business over the next three years.

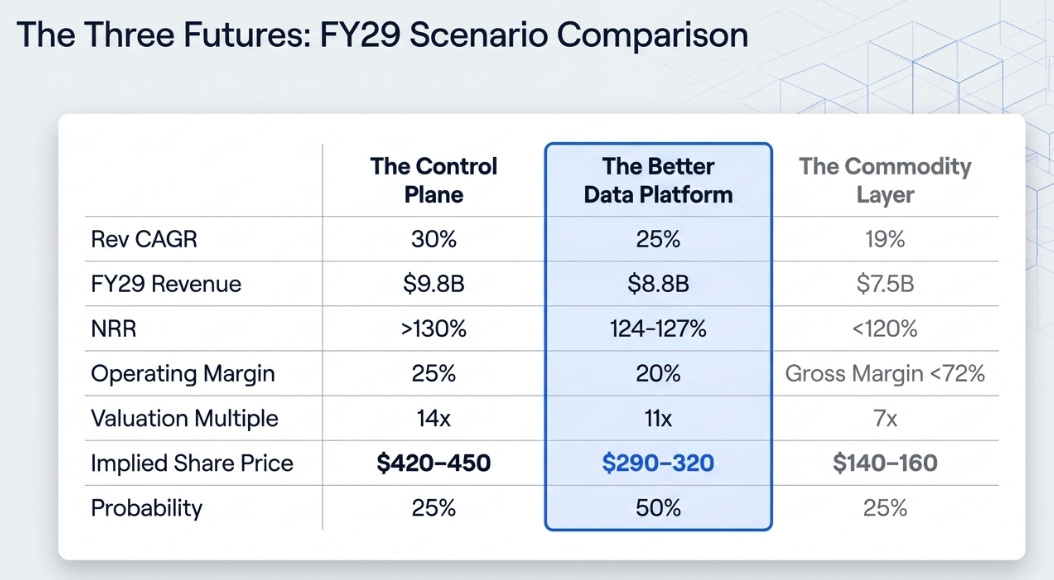

The Control Plane Compounds. CoCo and CoWork become the primary interfaces for enterprise data and AI work. The data loop proves durable. Revenue compounds at ~30% to ~$9.8 billion by FY29. NRR re-accelerates above 130% as CoWork expands the user base. Operating margins reach 25% as AI productivity raises the ceiling. At 14x FY29 product revenue: $420–450. Requires CoCo sustaining above 15,000 accounts, CoWork achieving departmental scale, and competitors failing to replicate the governed context advantage. Roughly 25% probability, real but demanding.

The Better Data Platform. Snowflake is a premium platform with useful AI features but CoCo does not create a second S-curve. Revenue compounds at ~25% to ~$8.8 billion. NRR holds 124–127%. Operating margin reaches 20%. At 11x: $290–320. A high-quality compounder, and at $240 you are paying a fair price for it. Roughly 50% probability.

The Commodity Layer. Open formats erode governance differentiation. Hyperscalers absorb the context layer. CoCo plateaus as customers throttle AI spend. Revenue compounds at ~19% to ~$7.5 billion. Gross margins compress to 72%. NRR erodes below 120%. At 7x: $140–160. Roughly 25% probability.

In the Q4 piece I estimated $260 from $164, or 58% upside. The thesis has strengthened. The asymmetry has narrowed. That is the tradeoff that comes with being early and staying through the confirmation.

The New Signposts

Six items, each testing a specific leg of the thesis.

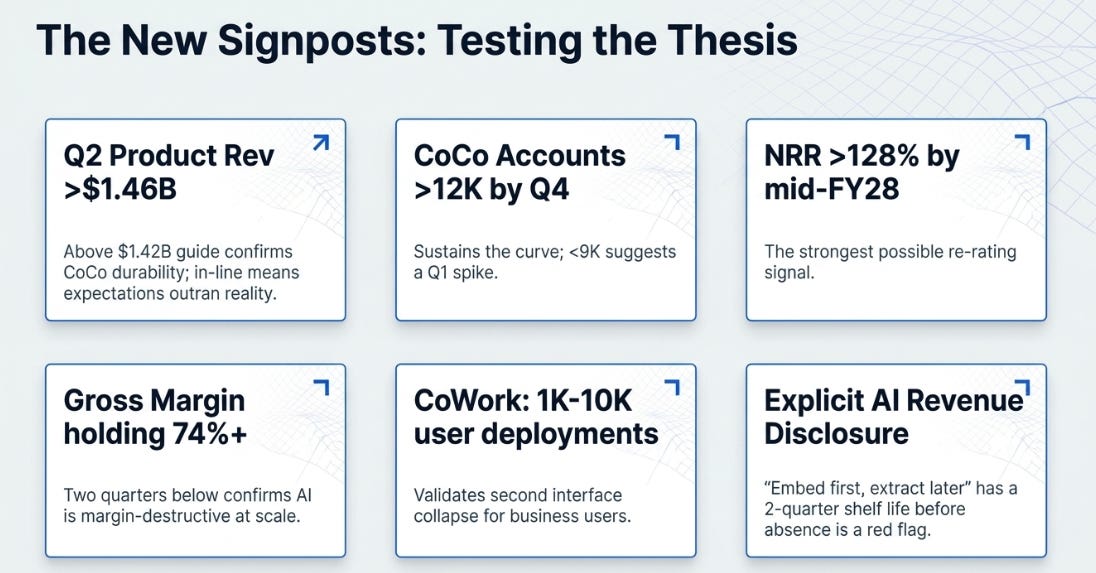

Q2 product revenue against the $1.42 billion guide, above $1.46 billion confirms CoCo durability; in-line means expectations have outrun reality. CoCo accounts through FY27, above 12,000 by Q4 sustains the curve; below 9,000 suggests a single-quarter spike. NRR toward 128% by mid-FY28, the strongest possible re-rating signal; below 123% means the expansion engine is weakening. Product gross margin, two quarters below 74% confirms AI is margin-destructive at scale. CoWork departmental deployments of 1,000–10,000 users, validates the second interface collapse for business users. Explicit AI revenue disclosure, “embed first, extract later” is credible but has a shelf life of two quarters before absence becomes a red flag.

Where We Stand

The thesis I held through $118 is closer to consensus at $240. That is a different kind of discomfort than a drawdown.

Conviction is higher than three months ago. Every structural signal, RPO conversion, interface collapse adoption, operating leverage, governed context positioning, moved in the direction I anticipated. The fundamental question has shifted from “is AI good or bad for Snowflake?” to “how far does the compounding loop extend?” That is a better question to sit with.

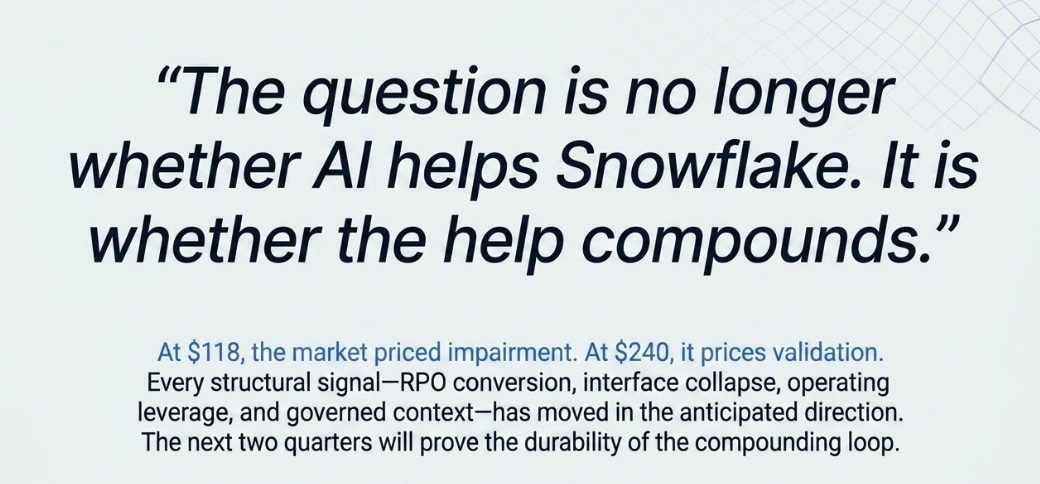

But at $118 the market was pricing impairment. At $240 it is pricing validation. The thesis is stronger, and the stock now reflects part of that strength. That does not make Snowflake less interesting, it makes the next evidence more important. The next two quarters will show whether the compounding loop is durable enough to justify a further re-rating, or whether Q1 was the high-water mark of a single-quarter adoption spike.

The best investment insights feel obvious in retrospect and unsettling in real time. The governed context layer thesis was unsettling at $118. It is approaching obvious at $240. I have learned to be more suspicious of the latter feeling than the former. The question is no longer whether AI helps Snowflake. It is whether the help compounds.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.