Snowflake 4QFY26: The Commitment Gap

Enterprises are signing nine-figure deals for a future Snowflake hasn't proven yet.

TL;DR

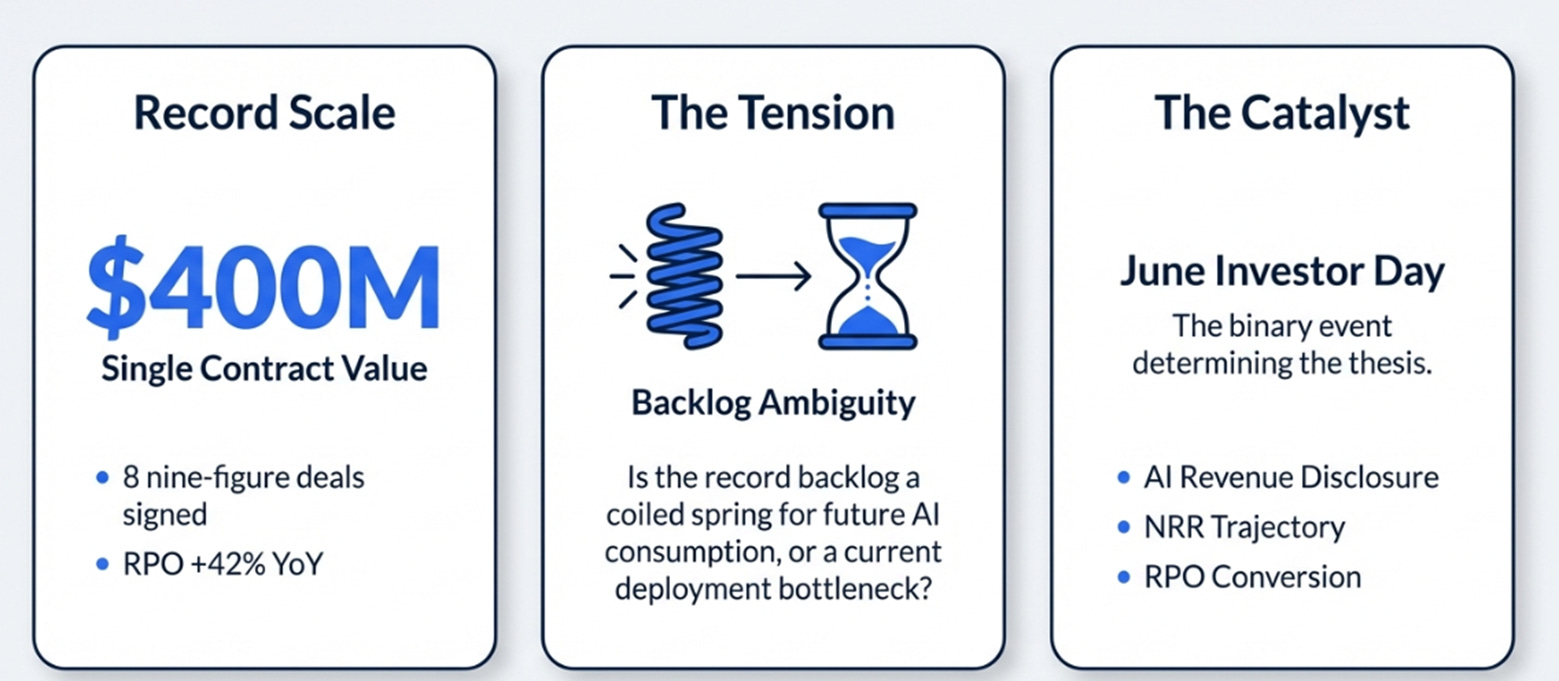

Enterprises are committing at record scale, RPO +42%, eight nine-figure deals, including a $400M contract, while revenue grows 30%.

The gap cuts both ways: backlog is either a coiled spring for AI-driven consumption or a deployment bottleneck waiting to surface.

June is the tell: AI revenue disclosure, NRR trajectory, and RPO conversion will determine whether Snowflake becomes the governed context layer of enterprise AI, or just a very good data warehouse.

The $400 Million Question

Last quarter, a large financial services company signed a deal with Snowflake worth more than $400 million. It was the largest contract in Snowflake’s twelve-year history. In the same quarter, Snowflake signed seven additional nine-figure contracts, up from two a year ago. Total remaining performance obligations reached $9.77 billion, growing 42% year-over-year, accelerating for the second consecutive quarter.

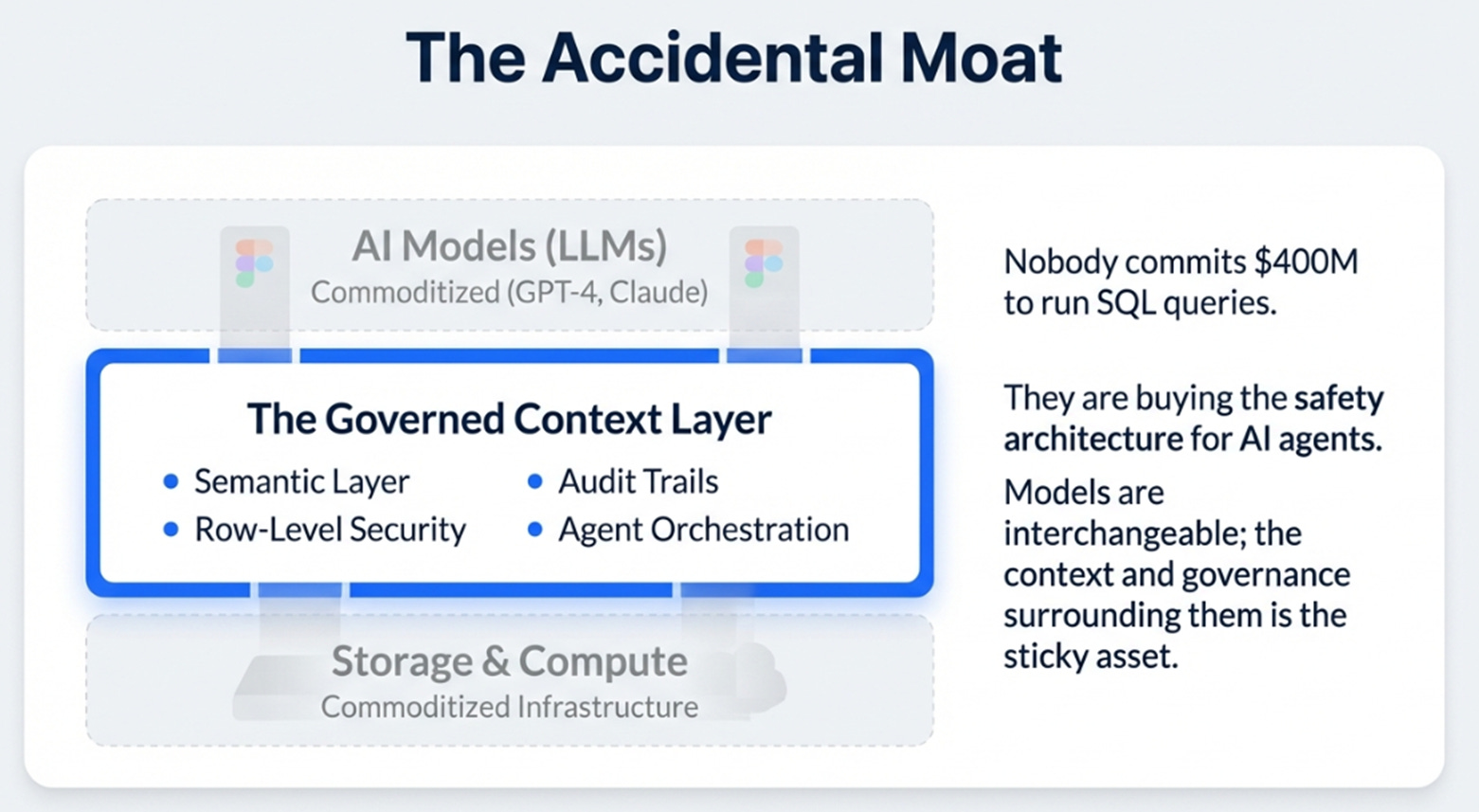

Nobody commits $400 million to run SQL queries.

The rest of the Q4 print was solid: product revenue of $1.23 billion grew 30%, non-GAAP operating margin expanded to 11%, and the company guided FY27 product revenue to $5.66 billion, 27% growth, above consensus. Net revenue retention held at 125%. Free cash flow in Q4 was $765 million.

The stock fell 3%.

This is the tension that defines Snowflake right now. Enterprise CIOs are making the largest infrastructure commitments in the company’s history. The stock market is discounting them. RPO grew 42%. Revenue grew 30%. The stock dropped.

Somebody is wrong. The question is who, and the answer depends on what you think that $400 million was actually buying.

The Accidental Moat

Here is what I think it was buying: a governed context layer.

Not a data warehouse. Not a lakehouse. Not access to an AI model. A system that knows which data exists across the enterprise, who is authorized to access it, what the business definitions mean, and how to safely expose all of that to AI agents, with full auditability and governance.

This is a product category that did not exist eighteen months ago. It exists now because the bottleneck on enterprise AI shifted.

For a decade, the constraint was model quality. Models weren’t good enough for production use. That constraint broke in 2024 and 2025 as foundation models from Anthropic, OpenAI, and Google reached the threshold where enterprises could deploy them against real business problems. The moment that happened, a new constraint emerged: context and governance. Can the AI agent access the right data? With the right permissions? Using the right business definitions? Without leaking sensitive information or producing ungoverned outputs?

Every enterprise that has tried to deploy AI agents at scale has discovered this within weeks. The model is the easy part. You can swap in Claude or GPT or Gemini. The hard part is the data foundation underneath, the cataloging, the semantic layer, the row-level security, the cross-cloud interoperability, the audit trail. Without that, you don’t have an AI agent. You have a liability.

Snowflake built all of this over the past decade. Not because they anticipated AI agents, because that’s what a modern cloud data platform required. Governance, security, cataloging, and semantic layers were table stakes for winning enterprise data warehouse deals. The AI revolution made those table stakes the most valuable part of the entire stack.

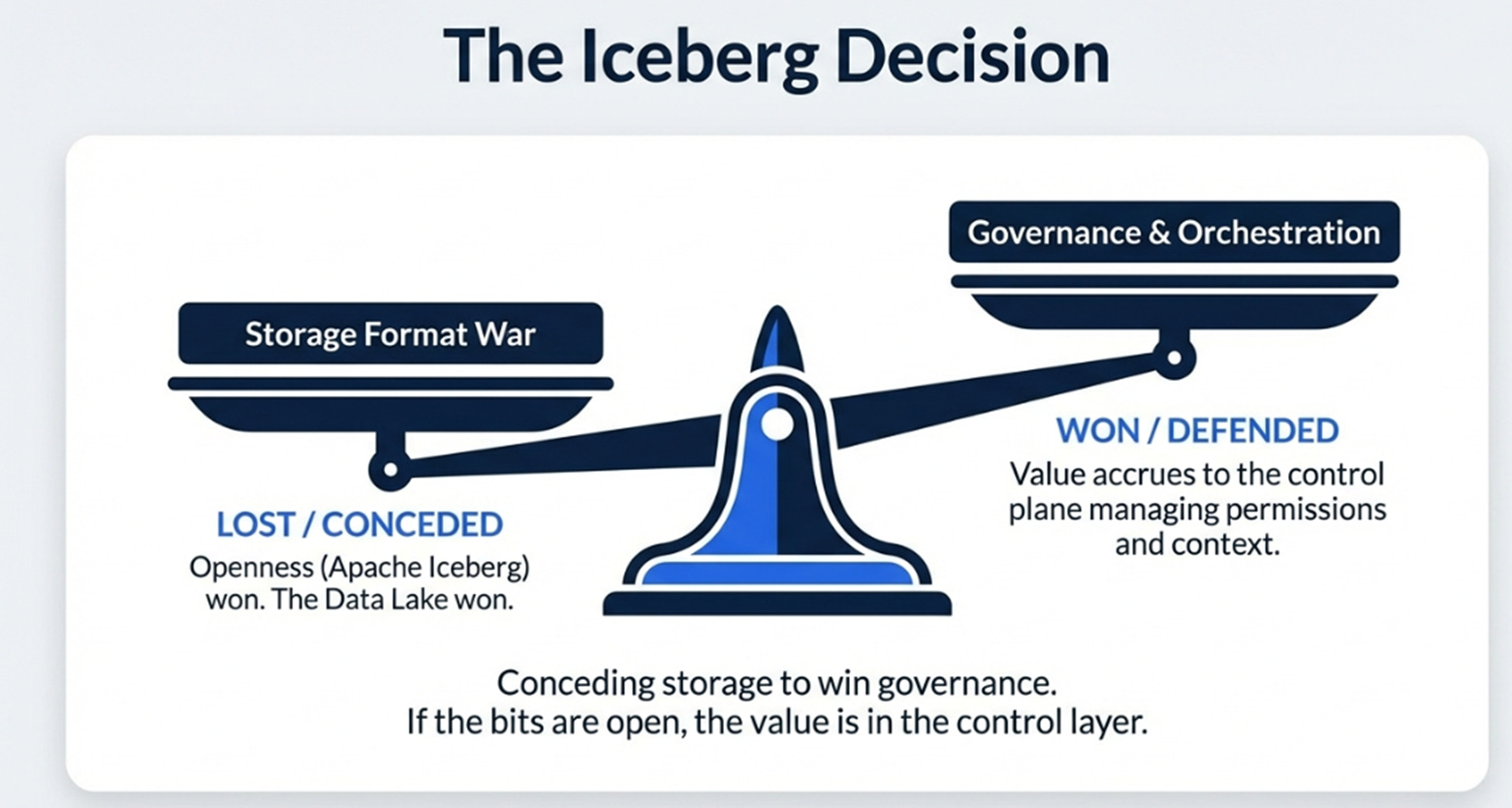

This is the strategic context for the Iceberg decision, which I think is the most important product choice Snowflake has made under Sridhar Ramaswamy. By embracing Apache Iceberg as a first-class storage format, including managed writes and managed block storage, Snowflake effectively conceded the storage format war. The data lake won. Openness won. Fine.

But that concession shifts the competitive battleground upward, to the governance and orchestration layer, where Snowflake has a decade of accumulated advantage. If the bits are open and portable, the value accrues to whoever manages the context around those bits, the permissions, the definitions, the security, the agent orchestration. Snowflake is betting that’s them.

The 42% RPO growth is enterprises voting yes on that bet. The $400 million deal is a CIO saying: I need a governed context layer for AI, and I need it now, and I’ll commit for years because rebuilding this from scratch is worse than the cost of commitment.

Both Directions

Now here’s the part where I have to be honest about the gap.

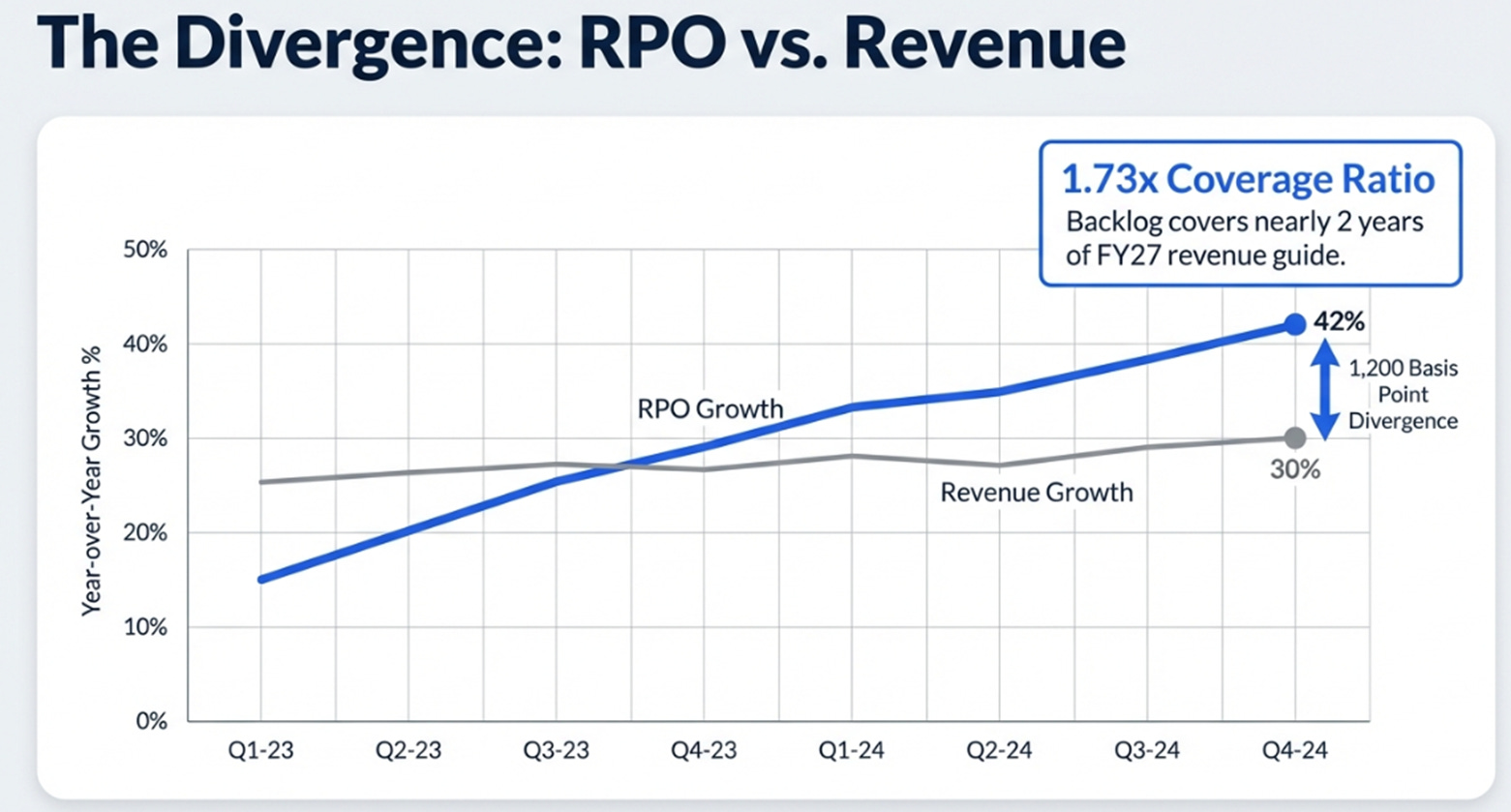

RPO grew 42%. Revenue grew 30%. That 1,200 basis point divergence is the most important number in the print, and it can be read in opposite directions.

The bull read is straightforward: it’s a coiled spring. Enterprises are committing capital to Snowflake’s platform faster than they can deploy against it. Large-scale AI transformations take 12-18 months to go live. The contracted backlog now covers 1.73 times the FY27 revenue guide, the highest coverage ratio in Snowflake’s history. Revenue will catch up. Give it time.

The skeptic’s read is equally valid. Customers are committing faster than they can deploy, and that’s a problem, not a feature. Professional Services revenue grew 32%, faster than product revenue, which hints at deployment bottleneck. The twelve-month RPO conversion rate declined from 50% earlier in the year to 46%, meaning contracts are getting longer but consumption isn’t accelerating proportionally. If a customer sits on $400 million in credits and can’t figure out how to deploy Cortex agents effectively in year one, that renewal conversation in year three looks very different.

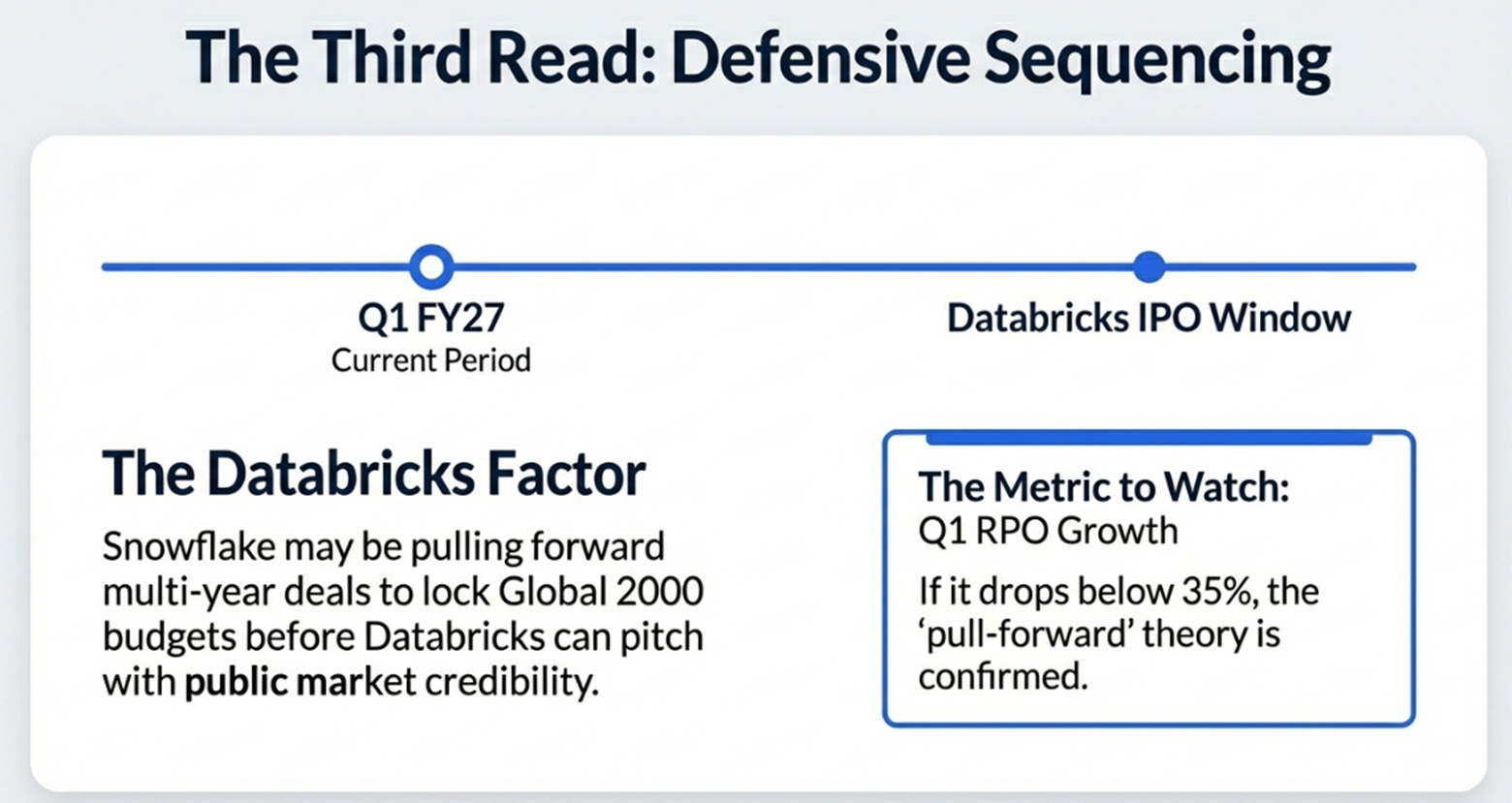

There is also a third read that nobody is discussing: timing. Seven nine-figure deals in Q4, a compensation plan reweighted toward bookings, an urgency to lock in Global 2000 accounts, all while Databricks IPO speculation intensifies. Snowflake may be deliberately pulling forward multi-year commitments to take enterprise budget off the table before Databricks can pitch from the credibility of a public listing. If Q1 RPO growth drops below 35%, this explanation gains weight.

Layered on top of all of this is the AI monetization question. Snowflake reported 9,100 accounts using AI features, 2,500 on Snowflake Intelligence in just three months, and 4,400 on Cortex Code. Those are strong adoption numbers. They did not, however, update the $100 million AI revenue run-rate they disclosed in December.

I think this is deliberate sequencing, not evasion. Embed first, extract later. Sridhar said on the call that he’s “slightly indifferent” whether revenue comes from running a query or running a model, a statement that only makes sense if AI consumption is blurring into core platform consumption in ways that make a clean “AI revenue” figure artificially reductive. That’s a credible explanation for now. But this strategy has a shelf life. The Investor Day in June is the natural deadline. If Snowflake shows a specific AI revenue figure above $300 million with a visible path to $1 billion, the stock re-rates. If they show another adoption dashboard, the market’s patience expires.

The Wrong Framework

The consensus view of Snowflake is that it’s a high-quality data infrastructure company growing 27%, with gradually improving margins, trading at roughly 10 times forward revenue. Fair value under this framework: $160-180, which is approximately where the stock sits. The implicit assumption is that AI is narrative, not revenue. NRR at 125% confirms structural deceleration. Gross margin compression from 76% to 75% signals the beginning of a margin trap. Good company, fair price.

I think this framework is wrong. Not because the numbers are wrong, but because the category is changing.

Three things the market is mispricing.

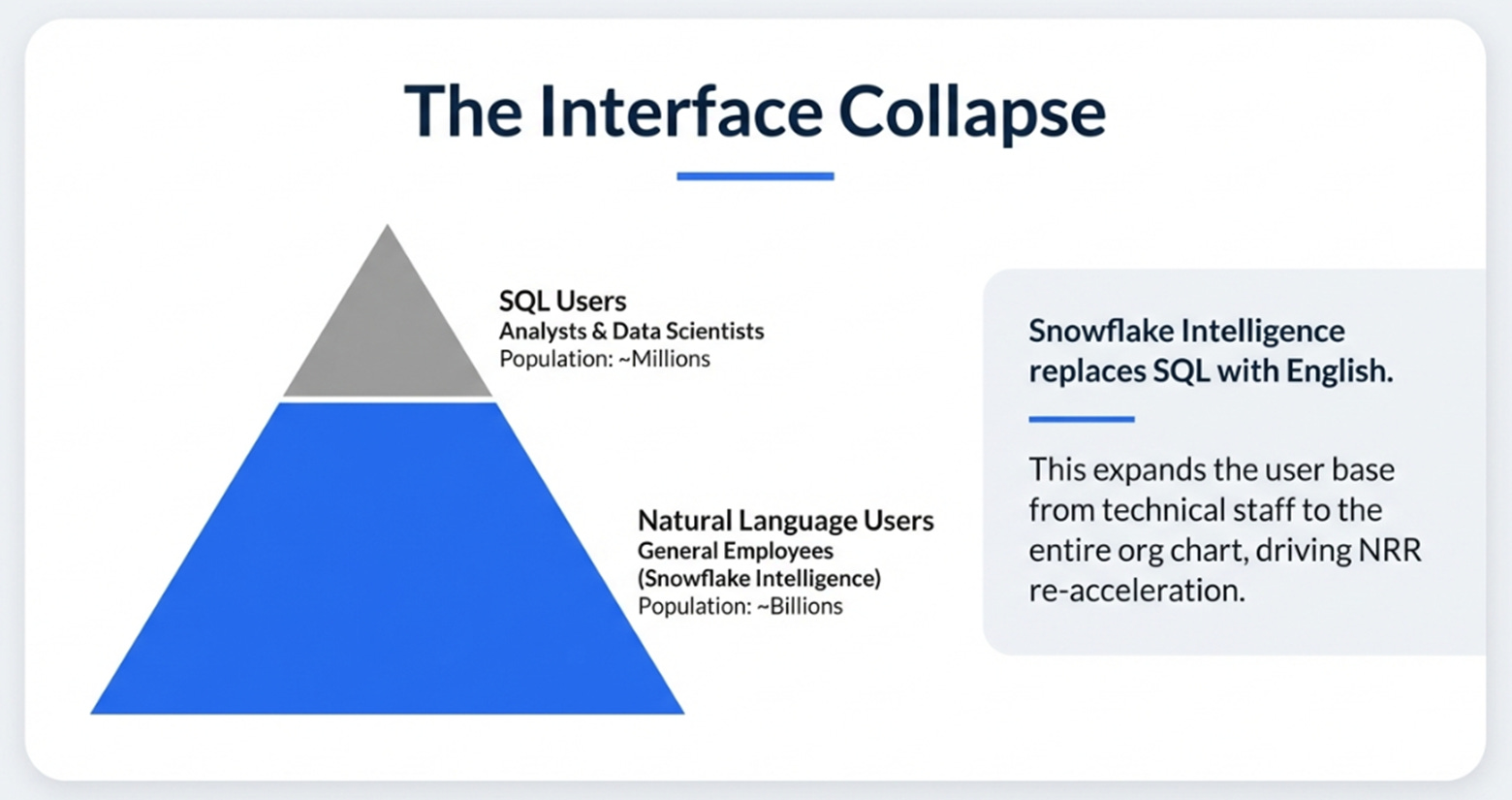

First, the Interface Collapse. Snowflake Intelligence puts a natural language interface on enterprise data. If it works at scale, the addressable user base for Snowflake queries expands from people who know SQL to people who have business questions, from millions to everyone. The planned per-user pricing cap that Sridhar mentioned is the tell: they’re anticipating a fundamentally different consumption pattern where many casual users replace few power users. If that plays out, NRR re-accelerates over two to three years as entirely new user categories drive expansion within existing accounts. The 56 customers above $10 million in annual spend, growing 56% year-over-year, is the earliest leading indicator. No consensus model captures this mechanism because the evidence isn’t in the quarterly data yet.

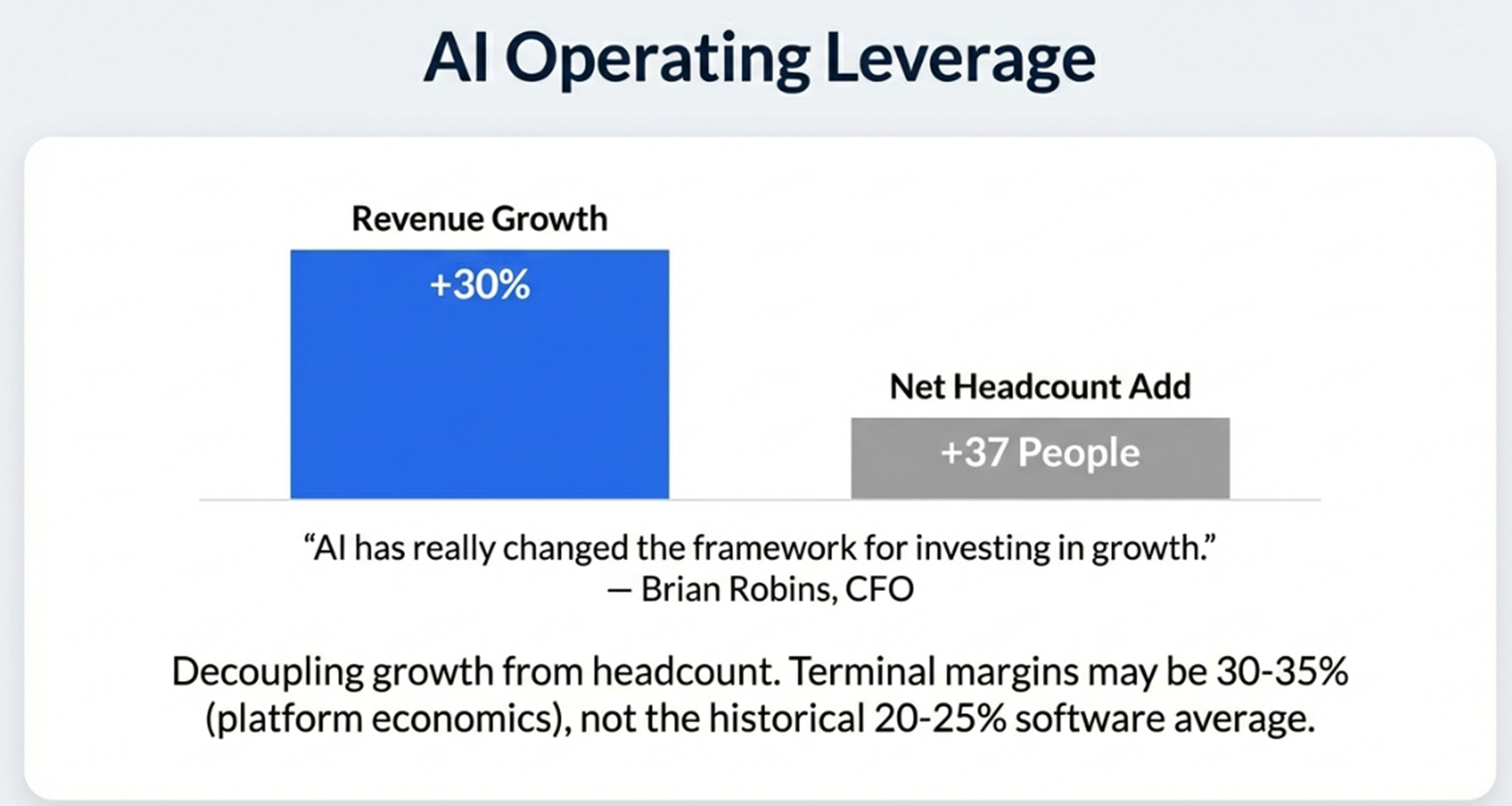

Second, AI-driven operating leverage. This is the most underappreciated part of the print. Snowflake conducted a roughly 200-person reduction in force in Q4 and added only 37 net headcount, while growing revenue 30%. They replaced a $5 million internal dashboarding system with Snowflake Intelligence. SRE investigations went from hours to minutes. CFO Brian Robins said plainly: “AI has really changed the framework for investing in growth. It’s no longer tied to headcount.” Meanwhile, SBC is guided to decline in absolute dollars for the first time in the company’s history.

This matters beyond Snowflake’s own P&L because the ecosystem is picking it up. One partner, Evolv Consulting, described shifting their entire business model from hourly billing to fixed-fee after Cortex Code made Snowflake implementations predictable. When your tooling makes your partners’ economics structurally better, those partners bring more workloads to your platform. That is a compounding flywheel that competitors cannot replicate by matching individual product features.

If this dynamic is real and replicable across 13,300 customers, the terminal operating margin isn’t 20-25% (typical enterprise software), it’s 30-35% (platform economics). The margin expansion from 6% in FY25 to 10.5% in FY26 to 12.5% guided for FY27 is accelerating, not decelerating. The market is extrapolating linear improvement when the underlying dynamic may be non-linear.

Third, the category itself. The governed context layer is either a durable product category worth a premium multiple, or a feature set that hyperscalers eventually absorb. Consensus prices zero probability of the former. The $9.77 billion in RPO says enterprises disagree.

The Math

Here is the math on what each outcome is worth.

Starting point: approximately $164 per share, $55 billion enterprise value, FY26 product revenue of $4.47 billion.

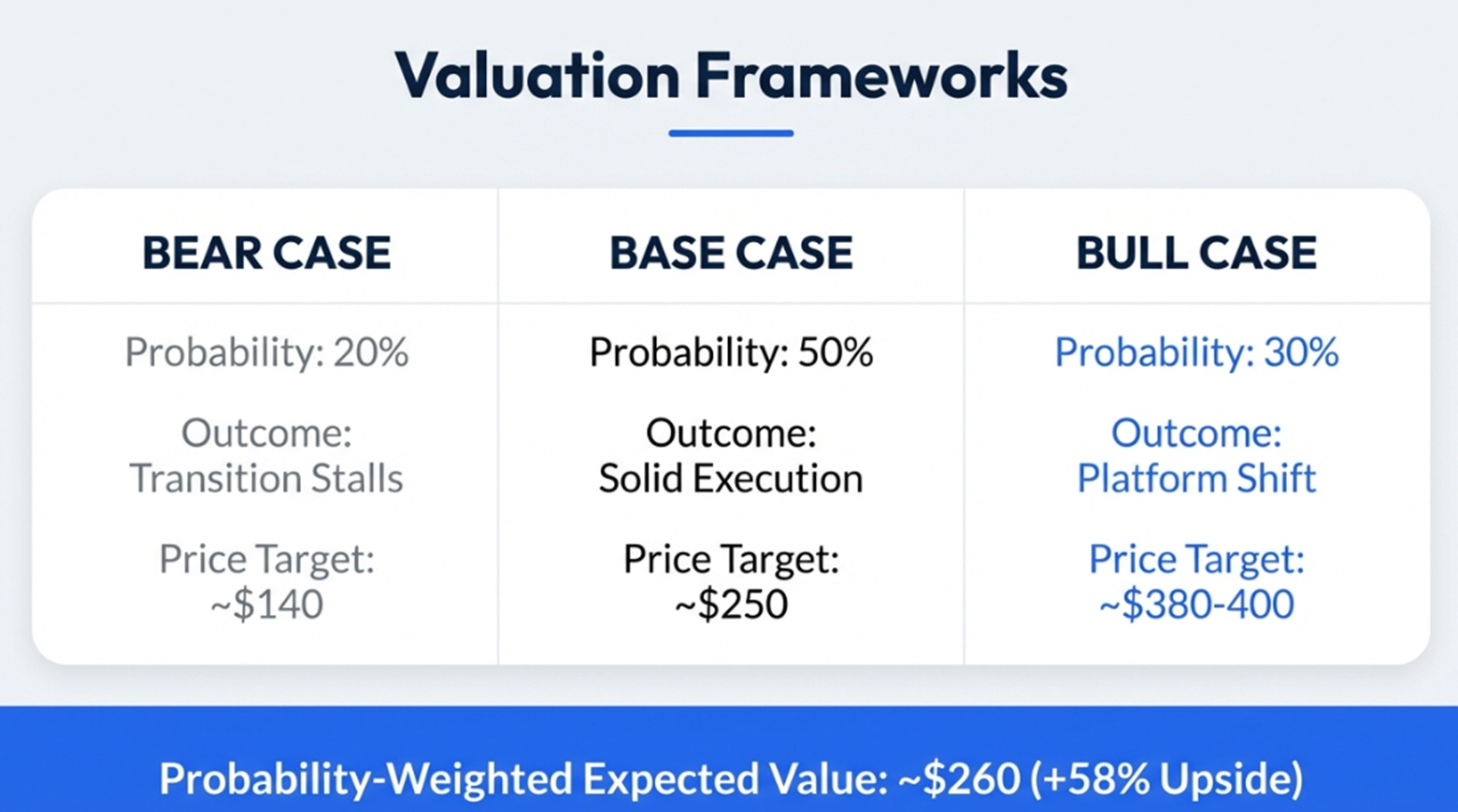

The bull case (30% probability): The platform transition works. Product revenue compounds at 28% annually through FY29, reaching roughly $9.4 billion. Intelligence, Cortex Code, and Observe collectively exceed $1.5 billion. Operating margin reaches 22% as AI-driven productivity bends the cost curve. NRR re-accelerates above 128%. At 14 times FY29 product revenue, the stock reaches $380-400, roughly 140% upside, or 35% annualized. The catalyst is an AI revenue disclosure above $500 million at Investor Day plus an NRR uptick by mid-FY27.

The base case (50% probability): Solid execution, partial validation. Revenue compounds at 25% to $8.7 billion. AI contributes incrementally but doesn’t create a new S-curve. Operating margin reaches 18%. NRR holds at 124-126%. At 10 times FY29 product revenue: $240-260, roughly 55% upside, 16% annualized. This doesn’t require AI to become a distinct revenue engine, just steady consumption growth and margin expansion.

The bear case (20% probability): The transition stalls. Revenue compounds at 20% to $7.7 billion. AI monetization disappoints. Gross margins compress to 72% as inference costs weigh. Hyperscaler bundling pressures new logo win rates. NRR erodes to 120%. At 7 times: $140-150, roughly flat to down 10%.

The probability-weighted expected value is approximately $260, or 58% upside from here. The asymmetry is what matters: the bear case is roughly flat, the bull case is a double-plus.

June

Five signposts that will determine which scenario plays out:

AI revenue disclosure at Investor Day in June: above $300 million confirms the embed-then-extract strategy is working. No disclosure means the strategy has become an excuse. NRR: hold above 124% and the floor is confirmed. An uptick to 127% would be the single strongest re-rating catalyst available. Product gross margin: below 74% for two consecutive quarters and the margin trap thesis wins. RPO conversion rate: below 44% and the implementation gap is real, commitments aren’t becoming consumption. Revenue per employee: above $600K in FY27, up from $518K in FY26, and the AI productivity thesis is validated in the P&L.

Now return to the question from the beginning.

What was that $400 million deal actually buying? Not a database. Not storage. Not compute. It was buying an insurance policy, the guarantee that when the board asks “are our AI agents secure, governed, and auditable?” the answer is yes. Every model, every data source, every user, inside the governance perimeter.

The governed context layer is either the most valuable real estate in enterprise AI, or a transitional waypoint before the hyperscalers absorb it. Snowflake’s customers have made their bet, $9.77 billion worth. The stock market says prove it.

The commitment gap will close. June tells us which direction.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.