SpaceX and the Price of Belief

Valuing the world’s fastest builder of scarce physical infrastructure

TL;DR

SpaceX looks wildly expensive on conventional numbers, but the real IPO question is whether Musk can once again turn belief into capital, capital into capacity, and capacity into proof.

Colossus may matter more than Grok: the AI segment’s most valuable asset could be SpaceX’s ability to build powered, cooled, usable compute capacity faster than hyperscalers can.

The stock’s fate depends on whether Anthropic and Google-style demand proves temporary “bridge capacity” or the beginning of a durable scarcity business; if proof lags belief, financial gravity returns.

There was a long period when Tesla was almost impossible to value correctly.

That does not mean the sceptics were wrong. They were often right. The company was too expensive on near-term numbers. Production was messy. The promises were too large. The balance sheet mattered. Dilution mattered. Execution risk mattered. At various points, the distance between what Tesla was and what Tesla claimed it would become seemed almost indefensible.

And yet, that was never the whole story.

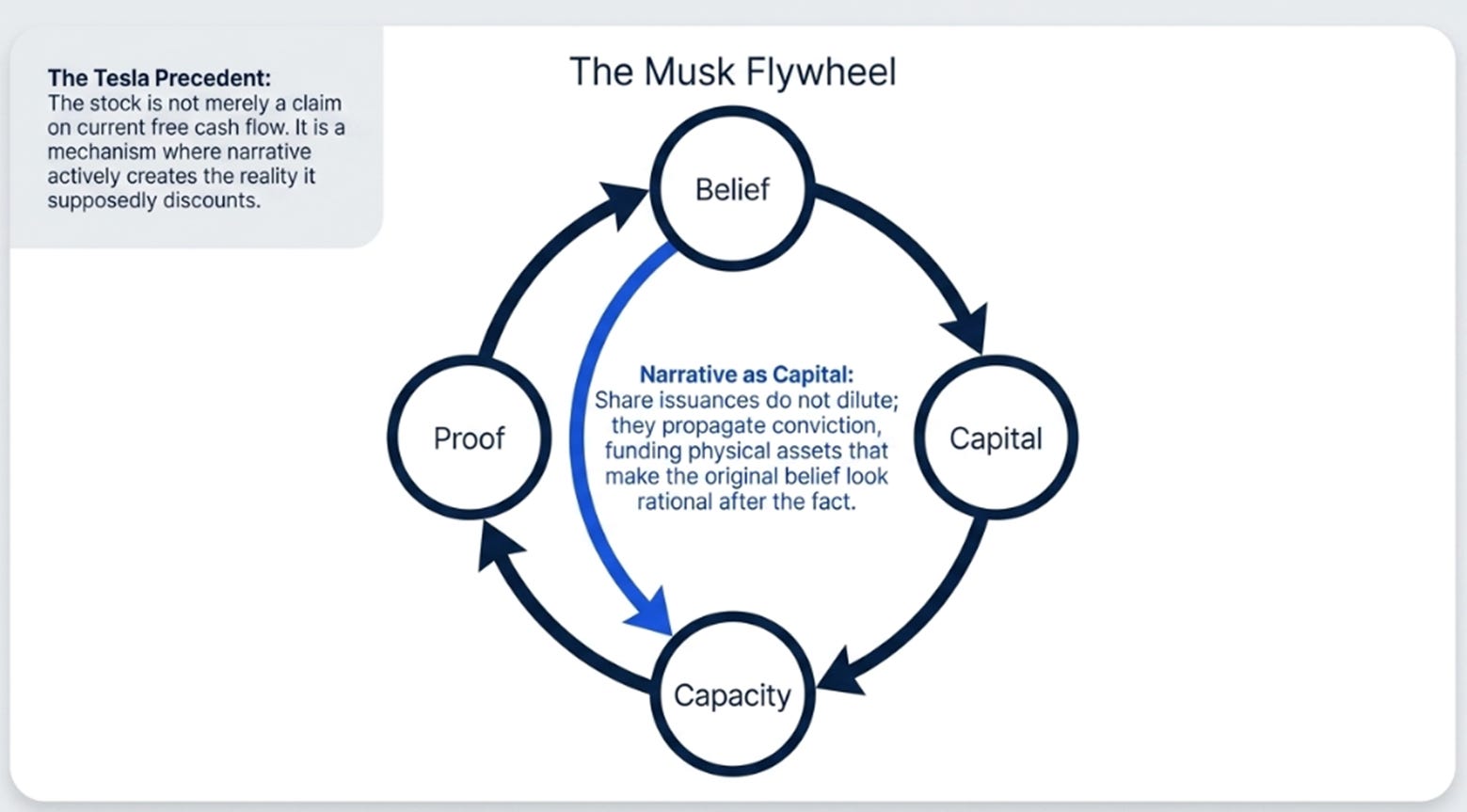

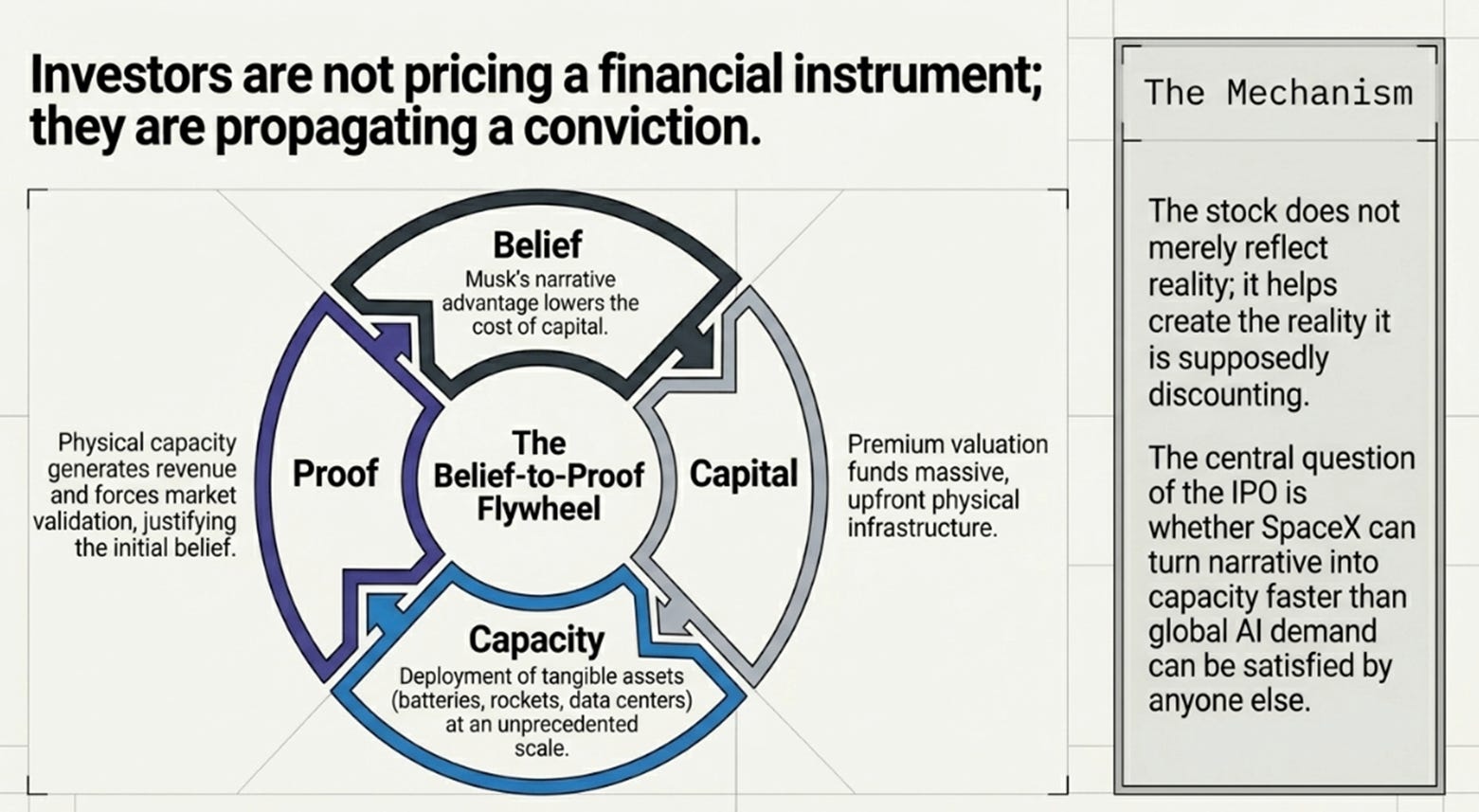

Tesla’s stock was not merely a claim on current car deliveries, gross margins, and free cash flow. It was also a mechanism. Belief in Elon Musk’s future gave the company access to capital. That capital funded factories and batteries and software and manufacturing scale. Those physical assets made parts of the original belief look less absurd after the fact. Share issuances that should have diluted the stock instead increased it, because investors were not pricing a financial instrument, they were propagating a conviction. The stock was not merely reflecting reality. At times, it was helping create the reality it was supposedly discounting.

This is not a comfortable way to think about investing. It sounds circular, and sometimes it is. Narrative can fund genuine progress, but it can also postpone accountability. Belief can become capacity, or it can become overpayment. The difficult part is that both things can be true at different times in the same company’s life.

SpaceX now presents the same problem, on a much larger canvas.

The Obvious Observation and the Interesting One

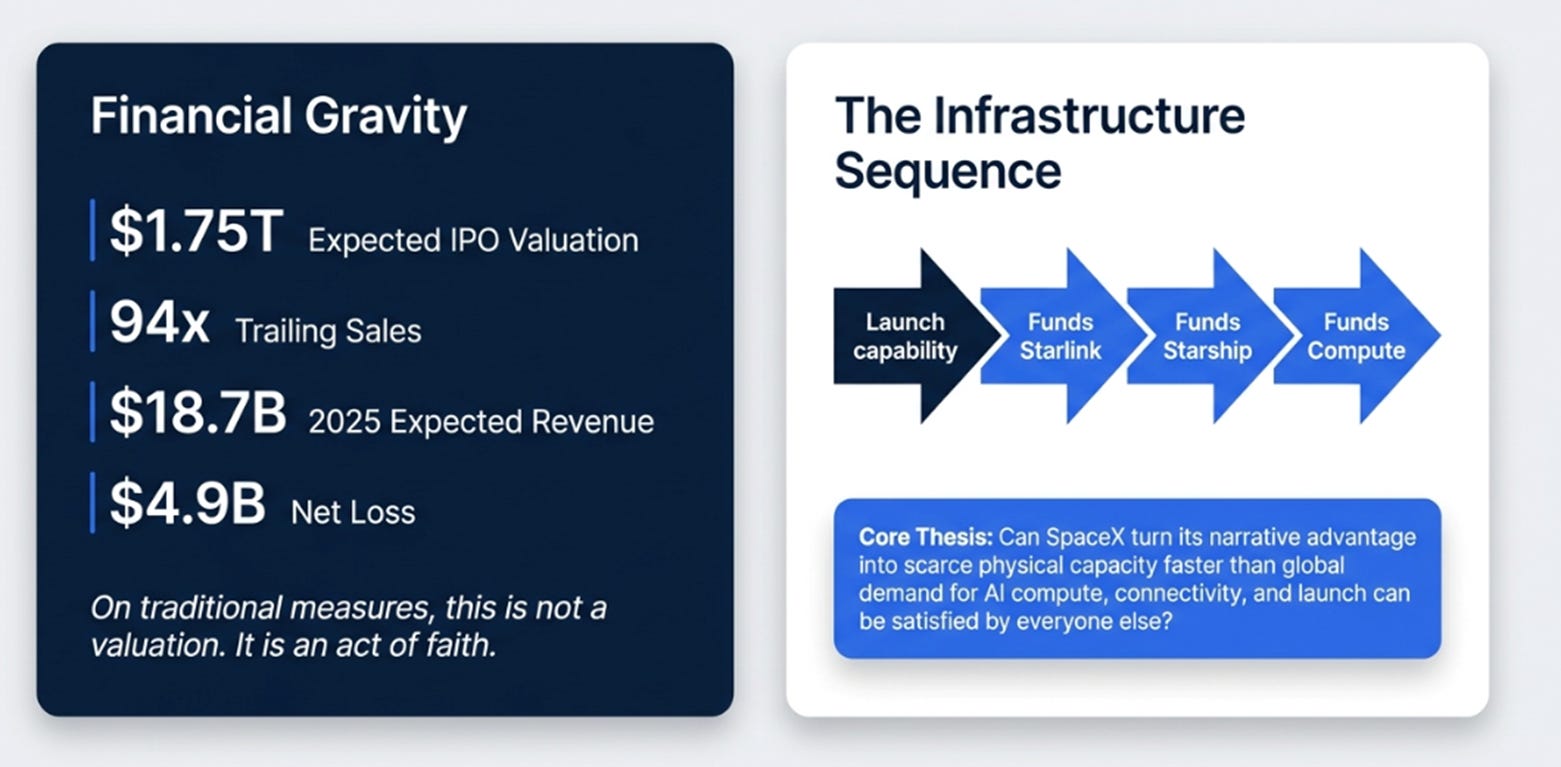

The ordinary observation about SpaceX is that it is expensive. That is true. At the expected IPO price of $135 per share, the company is being valued at approximately $1.75 trillion on $18.7 billion of 2025 revenue, roughly 94 times trailing sales, on a consolidated income statement that shows a net loss of $4.9 billion. On traditional measures, that is not a valuation. It is an act of faith.

But that is the least interesting observation about the IPO.

The more interesting question is: what kind of faith?

Investors are not merely being asked to believe in rockets. They are being asked to believe in a sequence: launch capability funded Starlink, Starlink funds Starship, Starship enables next-generation satellites and satellite-to-mobile and eventually compute in orbit. They are being asked to believe that the same company which made access to orbit cheaper can use that advantage to build the next set of scarce physical assets the world needs. They are being asked to believe that, once again, Musk can turn belief into capital, capital into capacity, and capacity into proof.

That is the real question at the heart of the SpaceX IPO:

Can SpaceX turn its narrative advantage into scarce physical capacity faster than global demand for AI compute, connectivity, and launch can be satisfied by everyone else?

Everything else is a sub-question.

SpaceX’s First Loop

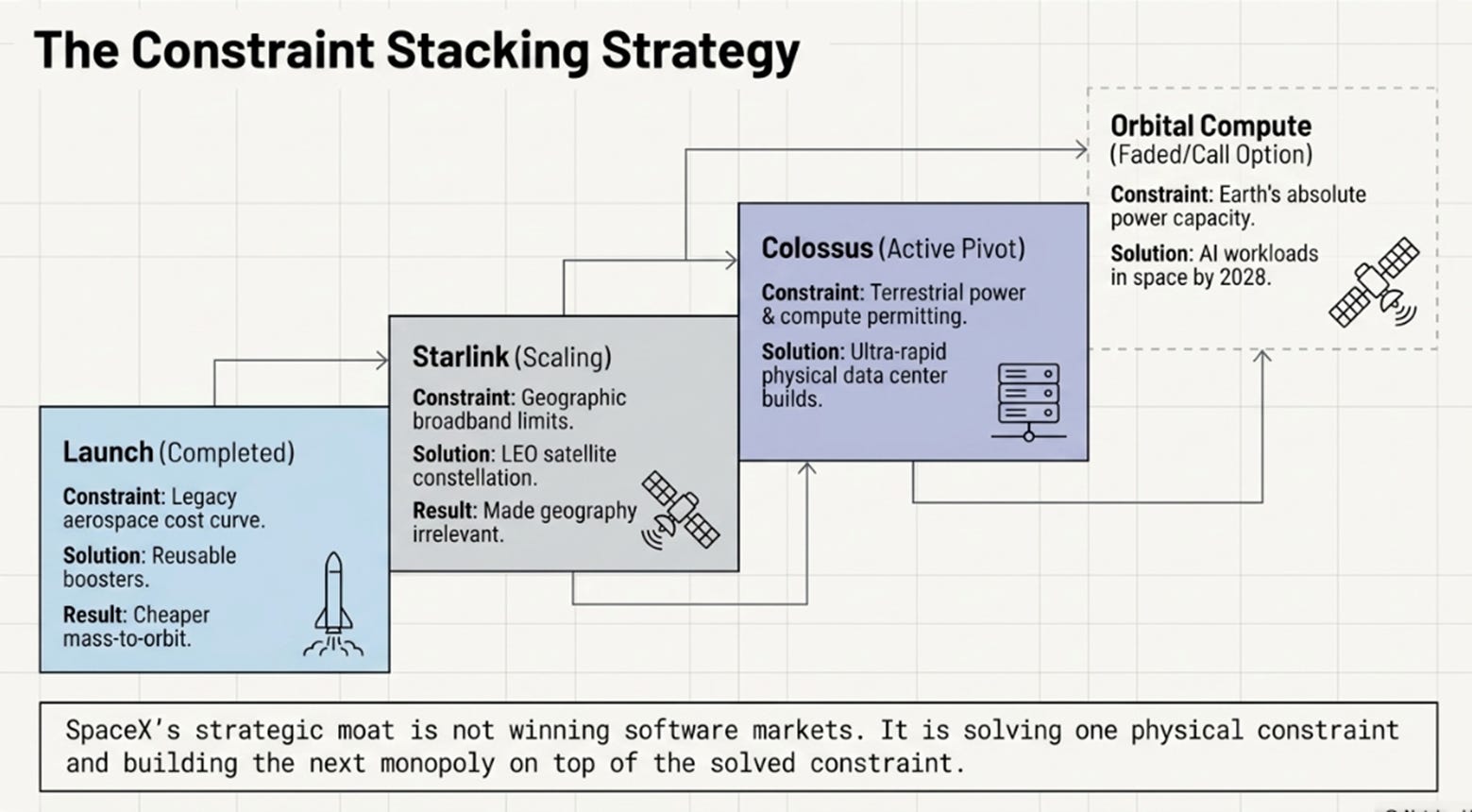

SpaceX’s original job was not “space exploration” in the abstract. It was more specific: move mass to orbit more cheaply, more reliably, and more frequently than the legacy aerospace system could manage.

That distinction matters. The customer hiring SpaceX was not buying poetry. A government customer needed mission assurance. A satellite operator needed delivery to orbit. NASA needed crew and cargo transport. The job was to remove the launch bottleneck. And SpaceX removed it: the S-1 reports approximately 620 Falcon 9 orbital launches with an over-99 percent mission success rate, a first-stage booster reflown as many as 34 times, and more than 80 percent of global mass to orbit each year since 2023.

Once that bottleneck was solved, SpaceX did something more important than sell cheaper launches to third parties. It became its own best customer.

Starlink was the proof.

The conventional way to understand Starlink is as satellite broadband. That is accurate but incomplete. Starlink is what happened when cheaper launch created a business that would not have made sense under the old cost curve. Thousands of satellites in low-Earth orbit are not an incremental improvement over geostationary broadband; they are a different architecture for making geography less relevant. The rural household does not hire Starlink because it likes satellites. It hires Starlink because fibre will not come soon. Airlines do not install Starlink because they want to make Musk happy. They install it because passengers expect the internet in the air to feel more like the internet on the ground.

This created a compounding loop: cheaper launch enabled more satellites, more satellites improved coverage, better service attracted more subscribers, more subscribers funded more launches, and more launches made the system progressively harder to replicate. Starlink’s 2025 numbers show the loop working: $11.4 billion of revenue, up roughly 50 percent year on year, at $7.2 billion of segment Adjusted EBITDA, with 10.3 million subscribers across 164 countries.

The pattern to hold in mind is not the specific numbers. It is the sequence. SpaceX’s most important strategic move is not winning a market. It is solving one physical constraint and then building the next business on top of the solved constraint.

The S-1 suggests SpaceX is attempting to do this again. But the next constraint is not launch. It is physical AI compute capacity.

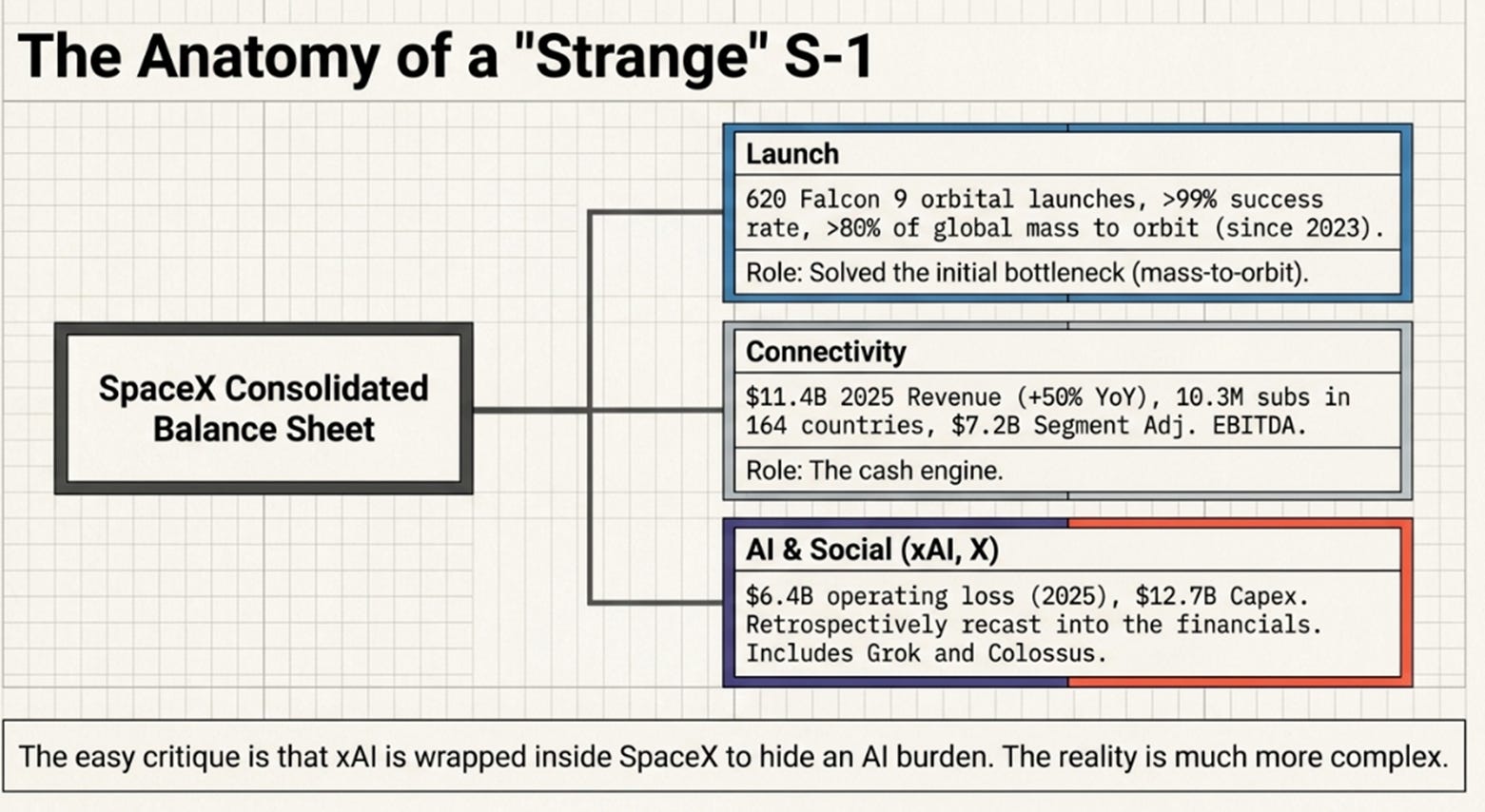

The Strange S-1

At first glance, the SpaceX S-1 looks like several companies stitched together.

There is the launch business: Falcon, Dragon, Starship, government contracts, mission success rates. There is the connectivity business: Starlink broadband, enterprise, aviation, maritime, satellite-to-mobile. Then there is the AI business: xAI, Grok, X, Colossus, Colossus II, and eventually compute in orbit.

A note on reading these numbers: the S-1’s consolidated financials were retrospectively recast to include xAI and X, because the transactions were between entities under common control. That means the historical comparisons are not as clean as a typical company going public with an organic segment history. When you see “2023 revenue: $10.4 billion,” that includes xAI and X revenue retroactively attributed to that period. The trends reflect a reconstructed combined entity, not SpaceX’s standalone trajectory.

The easy critique is that xAI is being wrapped inside SpaceX because xAI alone would be much harder to justify. That critique should not be dismissed. The AI segment brought a $6.4 billion operating loss in 2025, consumed $12.7 billion of capital expenditure, and houses a frontier model that has not established itself at the top tier. The founding research team departed. X, the social network folded into the segment, is a complicated asset. If one were simply underwriting Grok against Claude, Gemini, and GPT-4, SpaceX would look less like a clean space-and-connectivity story and more like an extraordinary company carrying a speculative AI burden.

But that framing may miss the point.

The better question is not whether Grok is the best model today. It is whether Grok is the business, or whether Grok caused SpaceX to build something more valuable.

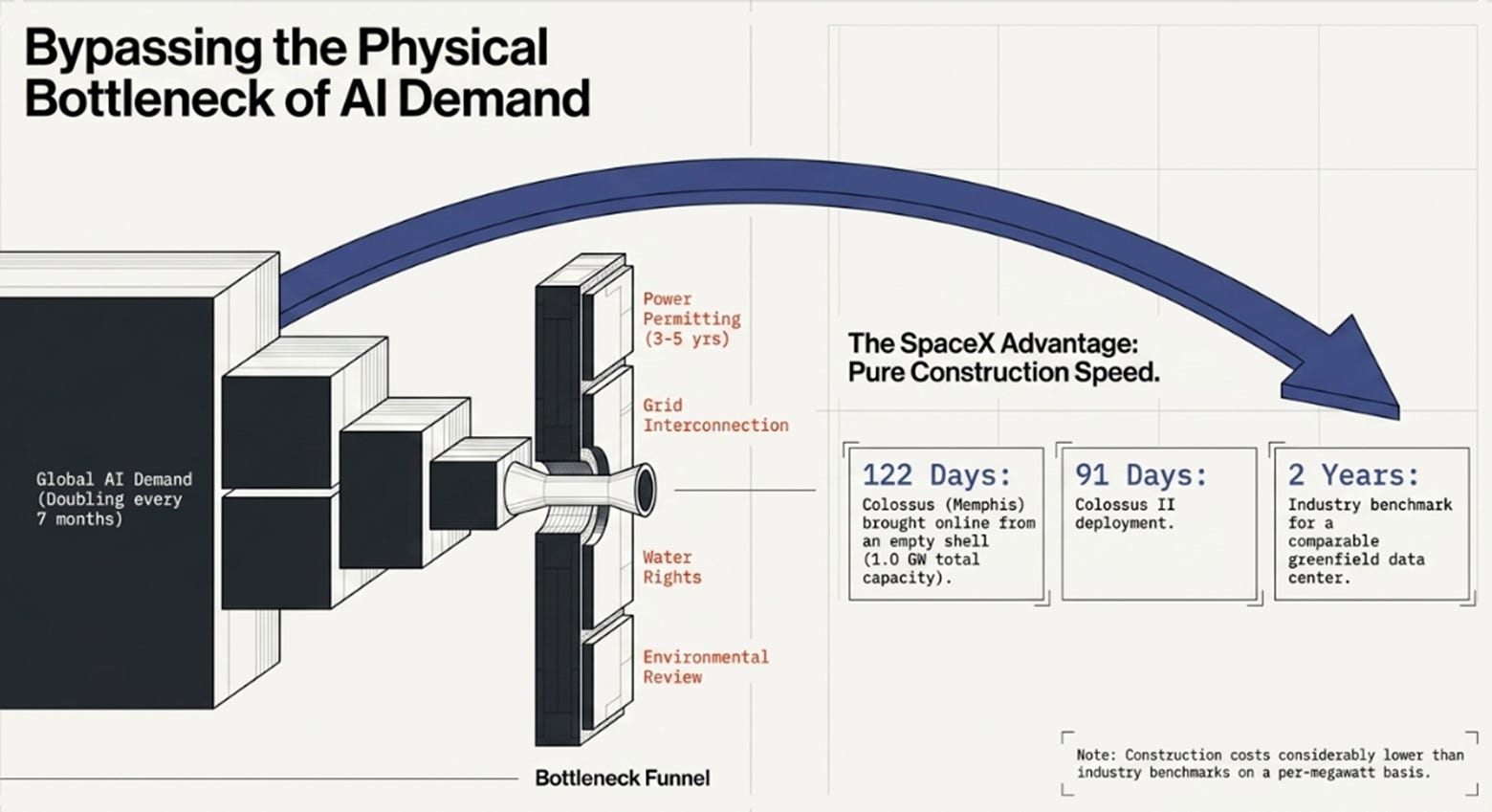

That something is physical compute capacity. Colossus, SpaceX’s flagship AI compute site in Memphis, came online in 122 days from an empty factory shell. Colossus II followed in 91 days. For context, the industry benchmark for bringing a comparable greenfield data centre online is approximately two years. The S-1 notes that construction costs for Colossus II were “considerably lower than industry benchmarks on a per megawatt basis.” Together, the two sites provide approximately 1.0 gigawatt of compute power.

The AI story in the S-1 is not really about a chatbot. It is about chips, power, cooling, land, networking, and construction speed, physical bottlenecks that happen to sit squarely in Musk’s demonstrated area of strength. There is a useful historical echo here: Samuel Insull dominated American electricity in the early 1900s not because his power was better, a kilowatt-hour is a kilowatt-hour, but because he built generation capacity faster than anyone else. In a market where demand outpaces physical supply, the fastest builder earns the scarcity premium. That principle may now apply to AI compute.

Musk is inconsistent in unconstrained software markets. X has made that obvious. But physical constraints have historically been his best arena. Rockets are physical. Cars are physical. Factories are physical. Batteries are physical. Data centres are physical. Power is physical. The world of AI may be discovering that the most important software market in history is increasingly limited by the least software-like problems.

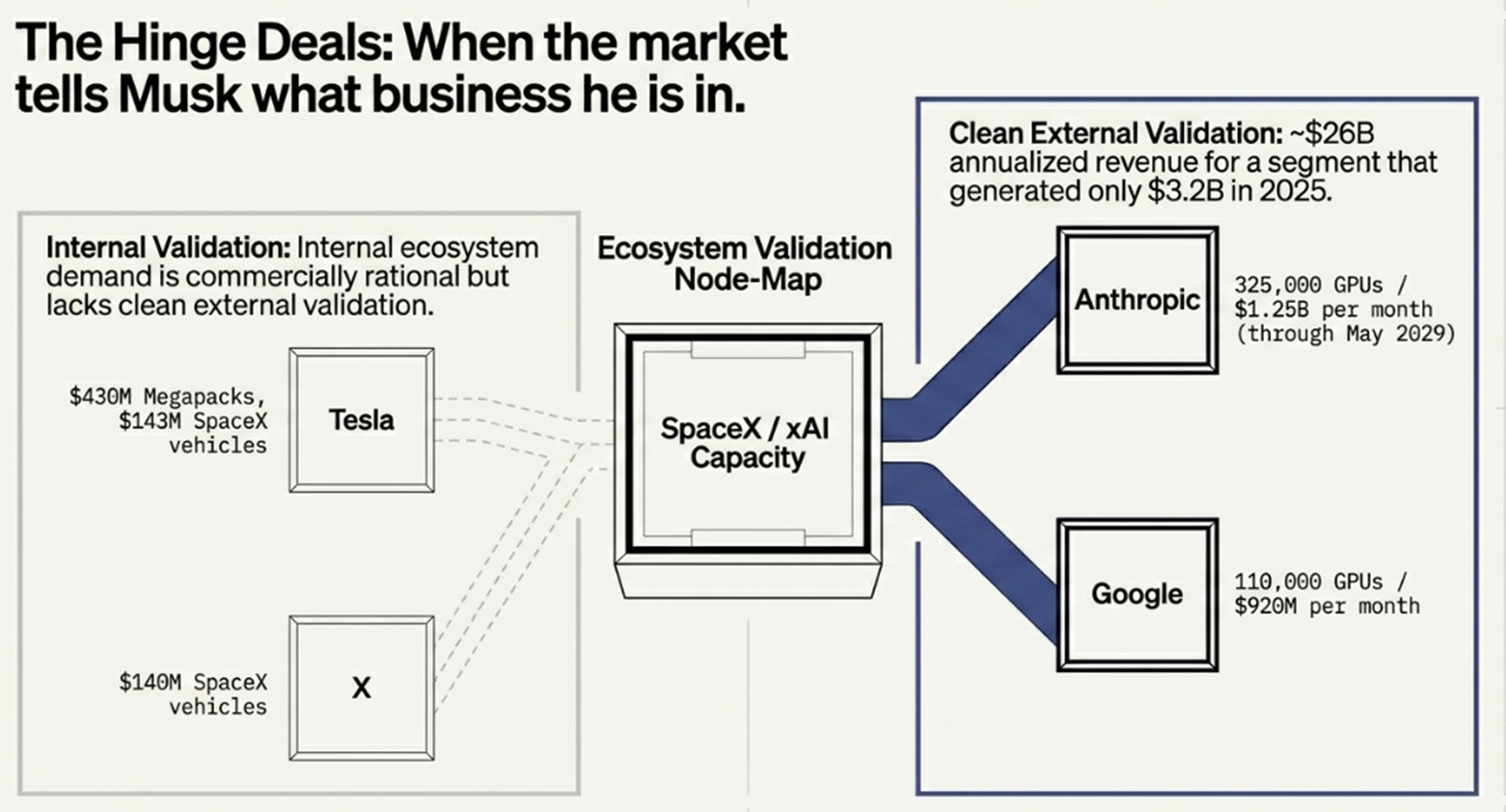

The Market Tells Musk What Business He Is In

The Anthropic and Google deals are the hinge of the SpaceX story.

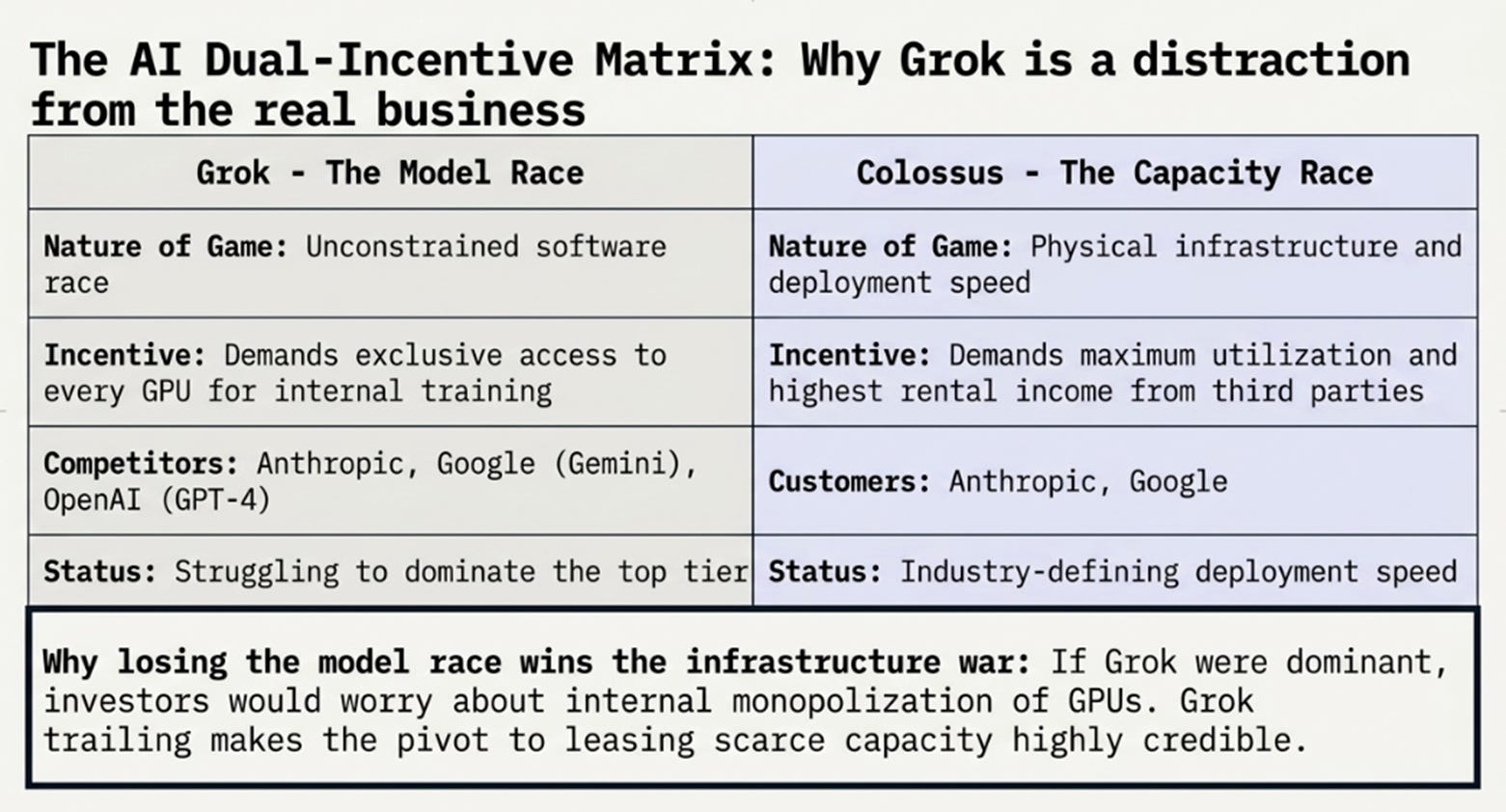

xAI was always two businesses sharing a balance sheet. There was the model business, Grok, competing against Claude, Gemini, and GPT on talent, data, and algorithmic insight. And there was the physical-capacity business, Colossus, competing on construction speed, power availability, and deployment timeline. These businesses have opposing incentives. The model business wants exclusive access to every GPU to improve Grok. The physical-capacity business wants maximum utilisation at the highest price from whoever will pay. Every GPU rented to Anthropic is a GPU not training Grok. Both cannot get what they want.

The Anthropic deal resolved the tension. In May 2026, Anthropic, a direct competitor in the frontier model race, signed a contract for access to approximately 325,000 NVIDIA GPUs across Colossus and Colossus II, at $1.25 billion per month through May 2029. SpaceX does not need Anthropic to prefer Grok. It only needs Anthropic to need compute. That is a profound difference.

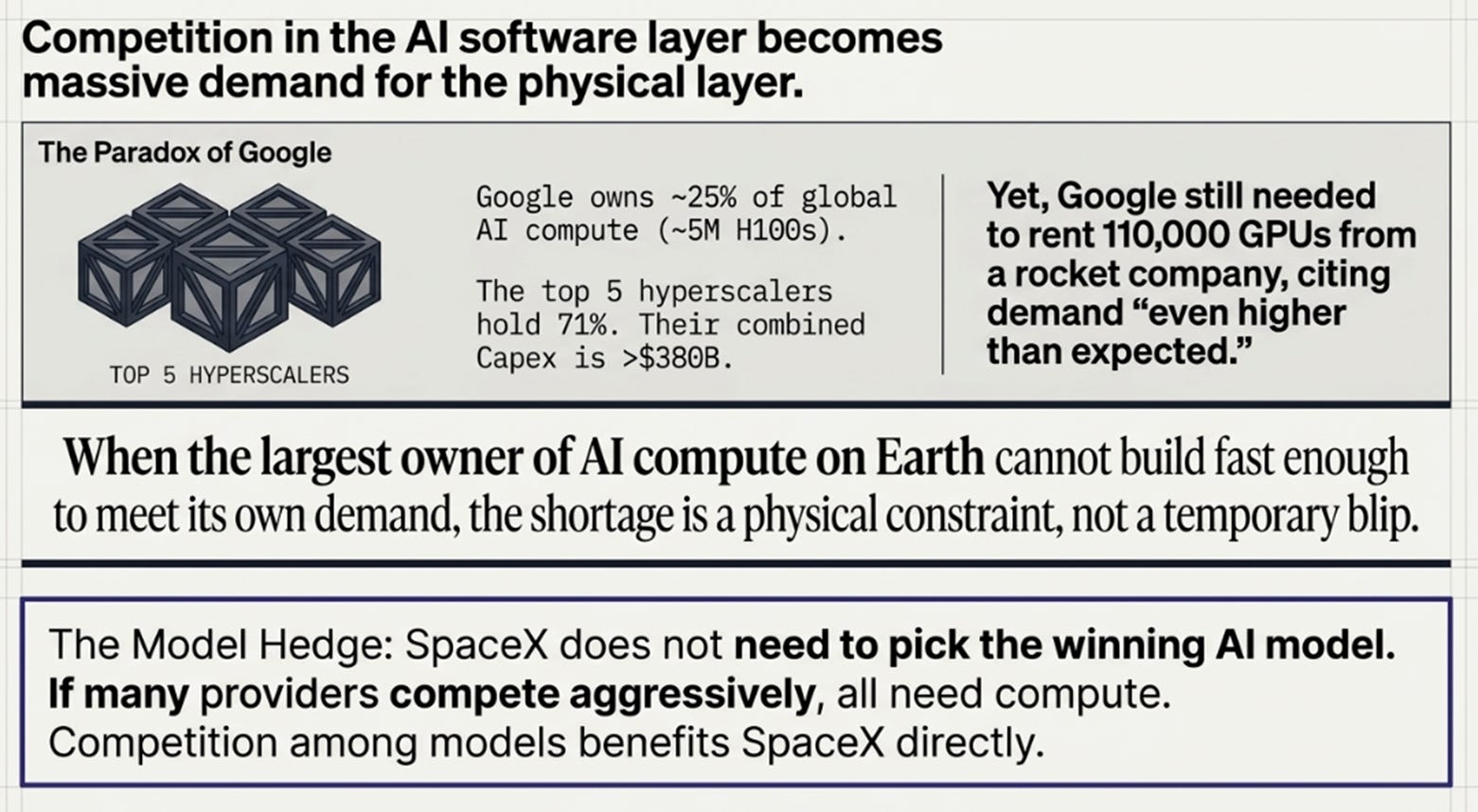

The Google deal, announced in early June via a regulatory filing, made it structural. Google is, by Epoch AI’s April 2026 analysis, the single largest owner of AI compute on the planet, holding roughly 25 percent of global capacity, equivalent to approximately 5 million H100-class processors. The five largest U.S. hyperscalers collectively hold an estimated 71 percent of global AI compute, up from 63 percent in early 2024. Their combined annual capital expenditure exceeds $380 billion. And Google still needed to rent 110,000 GPUs from a rocket company at $920 million per month, describing the arrangement as “bridge capacity” for demand that was “even higher than we expected.”

When the largest owner of AI compute on Earth cannot build fast enough to meet its own demand, the shortage is not a temporary blip. It is a physical constraint. And the nature of that constraint matters: power permitting takes three to five years in many jurisdictions. Grid interconnection queues are multi-year. Water rights for cooling face growing political opposition. Environmental review adds 12 to 18 months. Community resistance to large-scale data centre projects is intensifying. These bottlenecks do not respond to larger cheques. They respond to time. And AI demand, by Epoch AI’s estimate, doubles roughly every seven months.

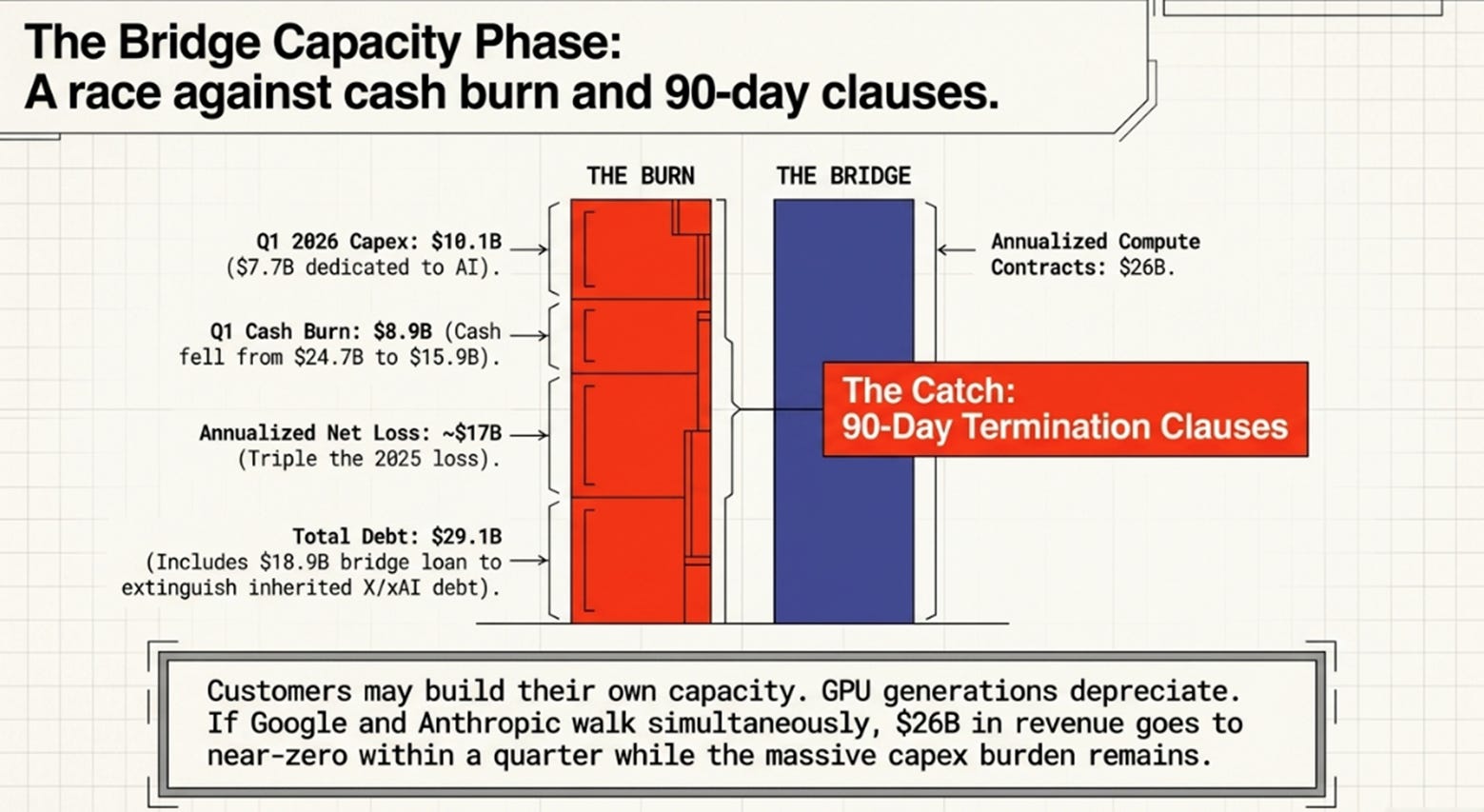

The combined contracts represent approximately $26 billion in annualised revenue for a segment that generated $3.2 billion in all of 2025.

There is an uncomfortable irony in Grok’s competitive position that may actually strengthen the investment thesis. If Grok were dominant, investors would have reason to worry that the leasing business might be deprioritised in favour of internal model training. Grok not being dominant makes the pivot to selling scarce physical capacity credible and likely durable. The most important customer for SpaceX’s AI buildout may not be Grok. It may be Grok’s competitors.

The Variant Perception

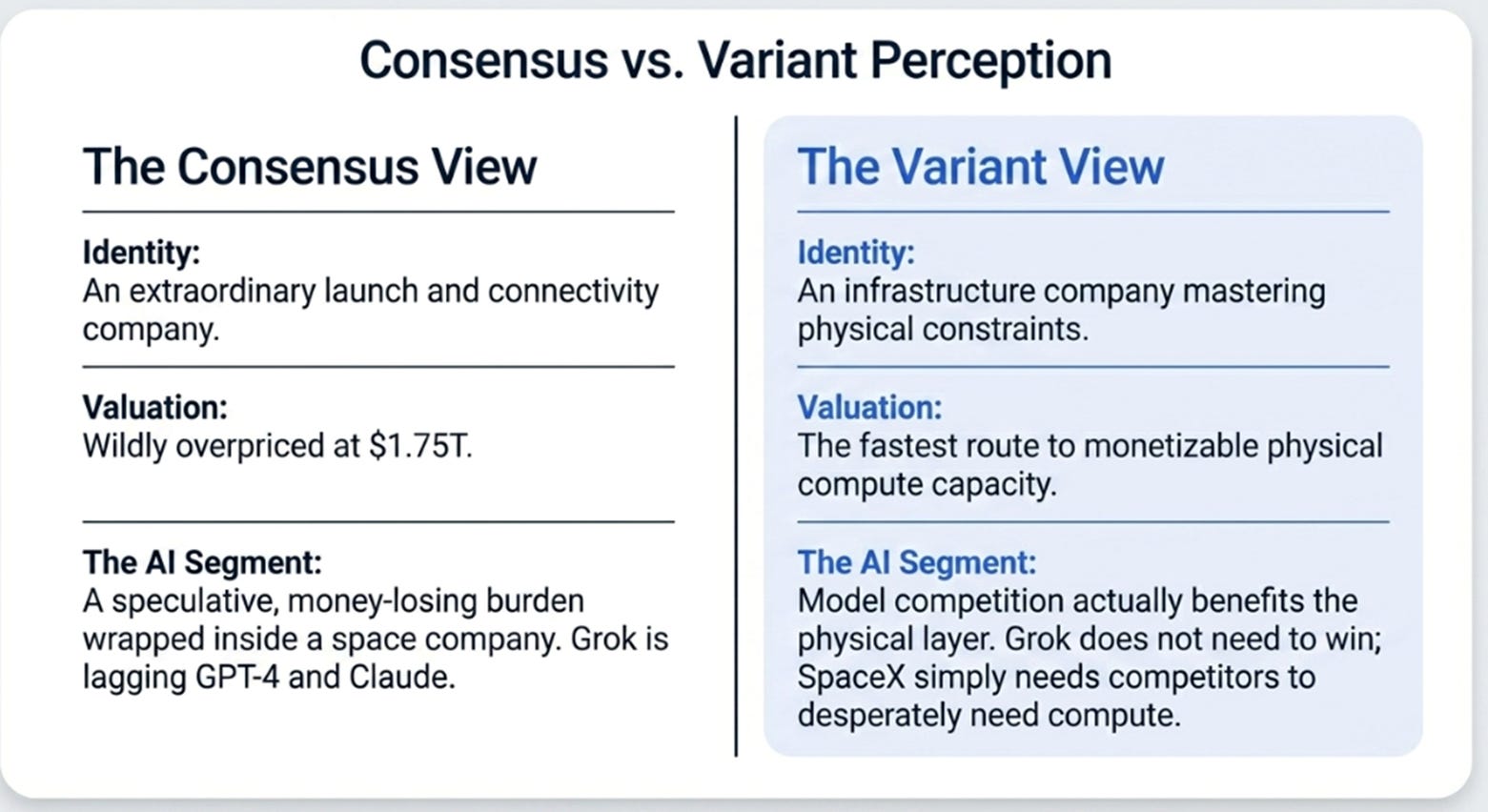

The consensus view is straightforward: SpaceX is an extraordinary launch and connectivity company, with a money-losing AI business attached.

The variant view is different. The AI segment may be misread. The near-term value may not rest on Grok winning the model race, but on SpaceX becoming the fastest route from demand to usable compute.

This matters because AI is moving from a purely software race into a race for physical capacity. The model companies can raise capital, hire researchers, and find users. They cannot instantly create powered, cooled, networked compute capacity at scale. The bottleneck is not just chips. It is chips plus power plus buildings plus interconnect plus time.

If that bottleneck persists, something interesting follows: competition among AI model companies may actually benefit SpaceX. If one model provider wins everything, SpaceX has a single dominant customer. If many model providers compete aggressively, all of them need compute. Competition in the model layer becomes demand for the physical layer. SpaceX does not need to pick the winning model. It can sell to all of them.

The 90-day termination clauses in both contracts deserve honest treatment. They reduce revenue durability, these are not long-term locked commitments. But they also enable repricing in a persistent shortage. Which reading is correct depends on whether scarcity is temporary or structural. That is the core bet.

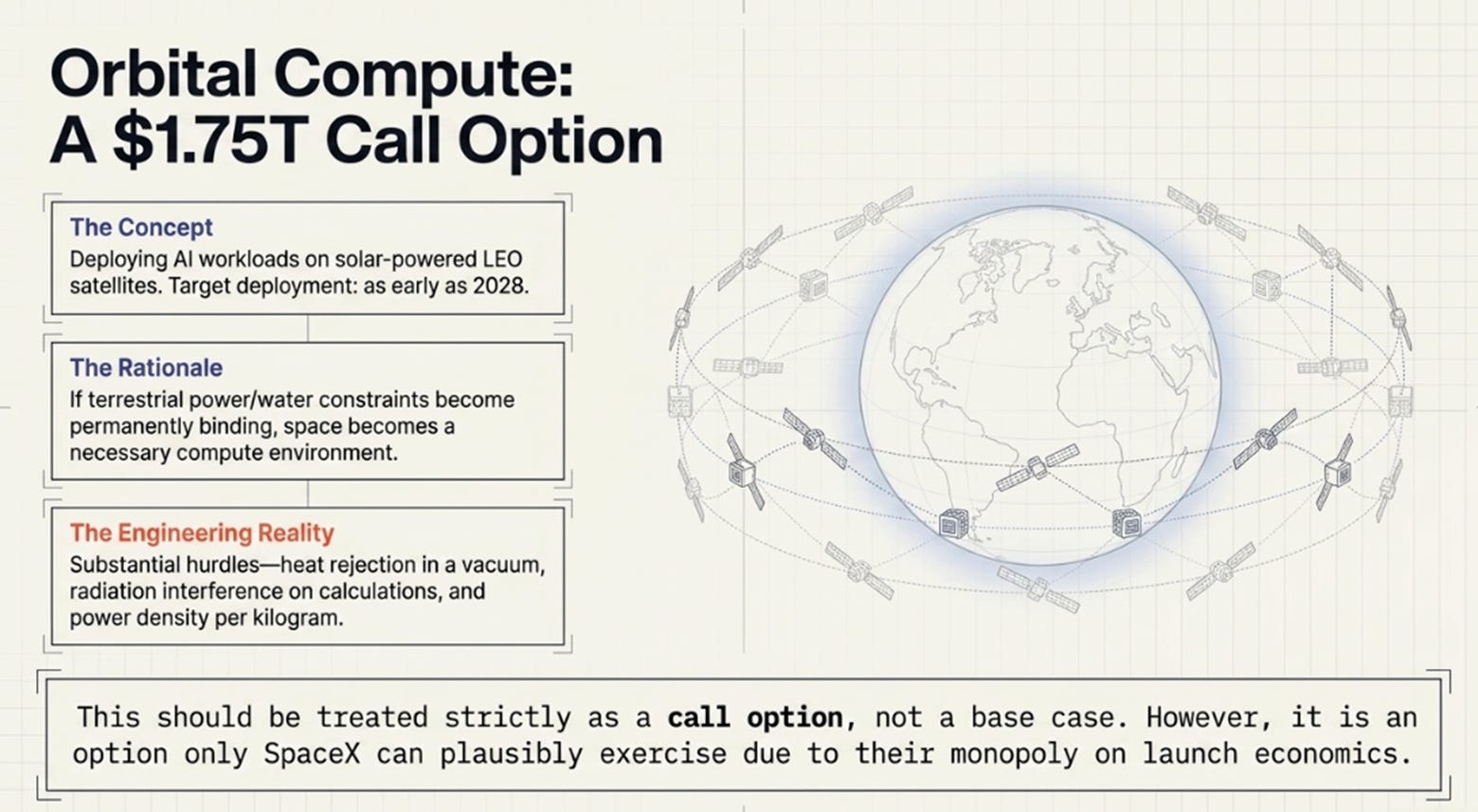

The orbital compute option, deploying AI workloads on satellites powered by solar energy, should be treated as a call option, not a base case. The S-1 targets initial deployment as early as 2028, and the engineering challenges are substantial: heat rejection in the vacuum of space, radiation effects on calculations, power density per kilogram, and the sheer scale of deployment required. But it is an option only SpaceX can plausibly exercise, because it requires launch economics, satellite manufacturing capability, and operational experience in orbit that no other entity currently possesses. If terrestrial power and permitting constraints prove genuinely binding at the scale AI demands, this option moves from speculative to necessary.

What Bulls May Be Missing

The danger is that the thesis sounds too clean.

Contract durability is the most important near-term risk. The Anthropic and Google deals are not the same as a permanent annuity. They may be bridge capacity. They may be renegotiated. They may be cancelled. Both contracts are terminable on 90 days’ notice after initial periods. Customers may build their own capacity within two or three years. GPU generations depreciate quickly, today’s H100s will be two generations old by 2029. A data centre that looks scarce today can become less scarce if supply catches up or if model efficiency improves dramatically. The most important mistake a bull could make is treating every dollar of compute revenue as if it deserves the same multiple as durable recurring cloud revenue. It probably does not.

The cash burn is not just high, it is accelerating. Q1 2026 capital expenditure was $10.1 billion, of which $7.7 billion was AI, against only $1.0 billion of operating cash flow. Cash fell from $24.7 billion to $15.9 billion in three months. Annualise the Q1 2026 net loss of $4.3 billion and you get roughly $17 billion, more than triple the full-year 2025 loss of $4.9 billion. The company is simultaneously funding Starship development, AI compute buildout, a $19.6 billion spectrum acquisition (EchoStar, approved but not yet closed, expected November 2027), and inherited debt from the xAI and X absorption. Total principal debt stood at $29.1 billion at March 31, 2026.

The IPO is partly a debt cleanup, not purely a growth capital raise. The S-1 discloses a $20 billion bridge loan in March 2026, with proceeds used to extinguish X and xAI debt, including X B-1, X B-3, xAI fixed and floating loans, and xAI 12.5% senior secured notes. The repayment amount was approximately $18.9 billion, including a $1.16 billion prepayment penalty. Part of what investors are funding when they buy the IPO is the financial consequences of absorbing xAI and X, not only the next generation of Starship and AI compute.

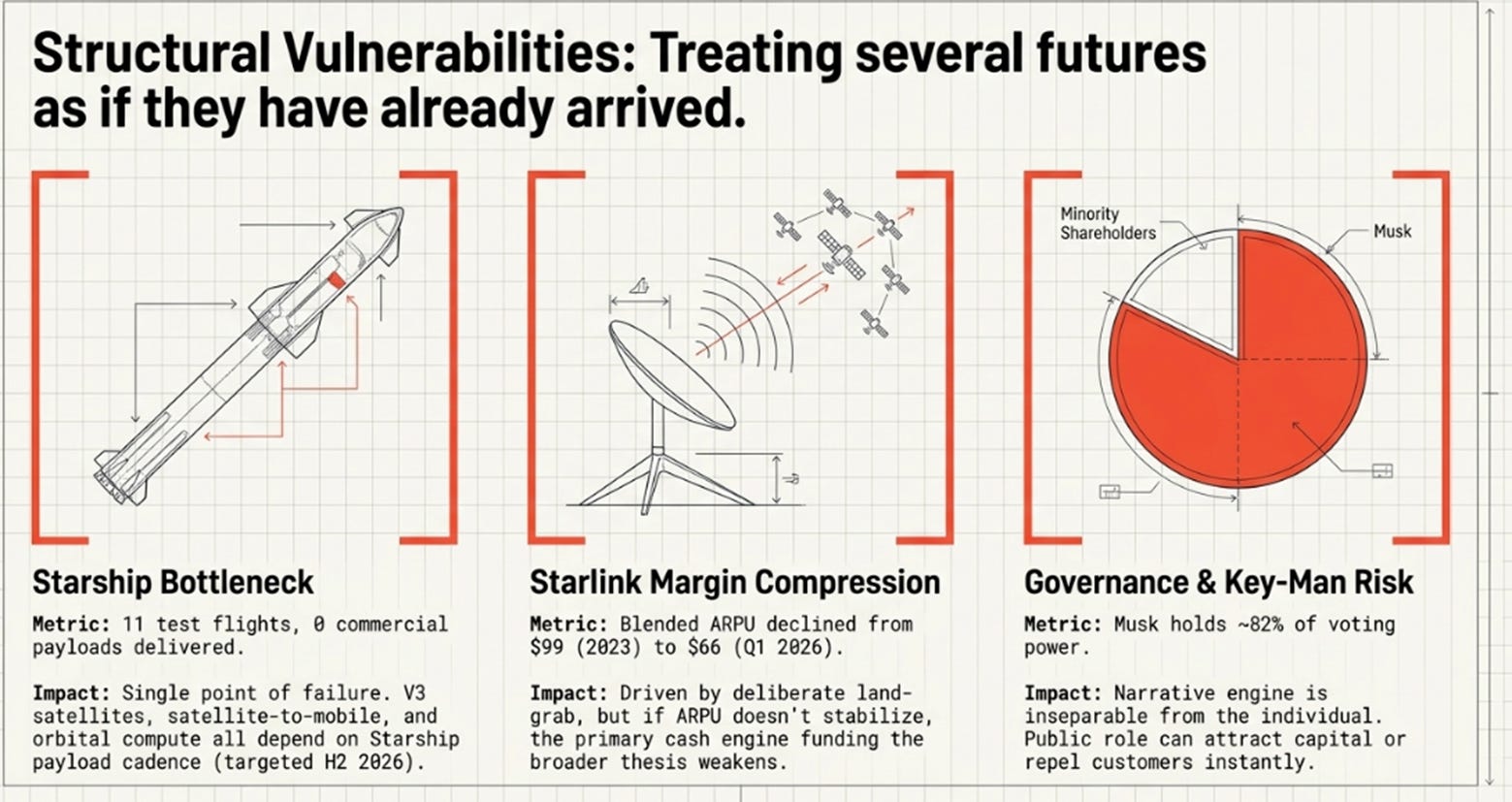

Starship is a single point of failure for too many futures. Nearly everything in the long-term thesis, next-generation V3 Starlink satellites, satellite-to-mobile at scale, cost-per-kilogram reductions, orbital compute, depends on one vehicle that has completed 11 test flights and has not yet delivered a commercial payload to orbit. The S-1 targets the second half of 2026 for payload service. If Starship is delayed meaningfully, multiple revenue lines delay with it.

Starlink’s cash engine is strong but the price trajectory is worth watching. Blended ARPU has declined every year, from $99 per month in 2023 to $66 in Q1 2026. The decline is mix-driven, reflecting a deliberate land-grab in newer, lower-priced geographies, and the expectation is that V3 satellites and premium aviation, maritime, and enterprise plans will stabilise or improve the trajectory. But V3 depends on Starship. If ARPU continues declining and subscriber growth alone has to carry the revenue line, the funding engine for everything else weakens.

Revenue concentration after the deals is extreme. Two customers will account for the vast majority of AI segment revenue, both with short-term termination rights. If both walked simultaneously, unlikely but not impossible, SpaceX would go from $26 billion in annual AI revenue to near-zero within a quarter, while still carrying the capex burden of facilities built to serve that demand.

Signal quality varies across the business. SpaceX is now part of a broader Musk ecosystem in which Tesla, xAI, X, and SpaceX transact with one another. Tesla’s 2025 10-K/A discloses $573 million in revenue received from Musk-controlled entities, including $430 million in Megapack sales to xAI and $143 million from SpaceX vehicle purchases. These transactions may be commercially rational and were reviewed by Tesla’s Audit Committee at arm’s-length terms. But internal ecosystem demand is less informative than independent third-party demand. That is precisely why Anthropic and Google matter so much: they are cleaner external validation. The more SpaceX’s growth comes from independent customers rather than intra-ecosystem activity, the stronger the thesis becomes.

Musk himself is the narrative engine and the governance risk. SpaceX benefits from his credibility, ambition, and talent magnetism. But the dual-class structure concentrating approximately 82 percent of voting power in his hands limits minority shareholder influence. His operational attention is split across multiple companies. His public role can attract capital and talent, or it can repel customers and partners, depending on the moment. The IPO structure reinforces this: investors are not buying ordinary governance rights. They are buying exposure to a company where one person’s judgment is inseparable from the thesis.

The danger is not that SpaceX is fake. It is obviously not fake. The danger is that investors treat several futures as though they have already arrived.

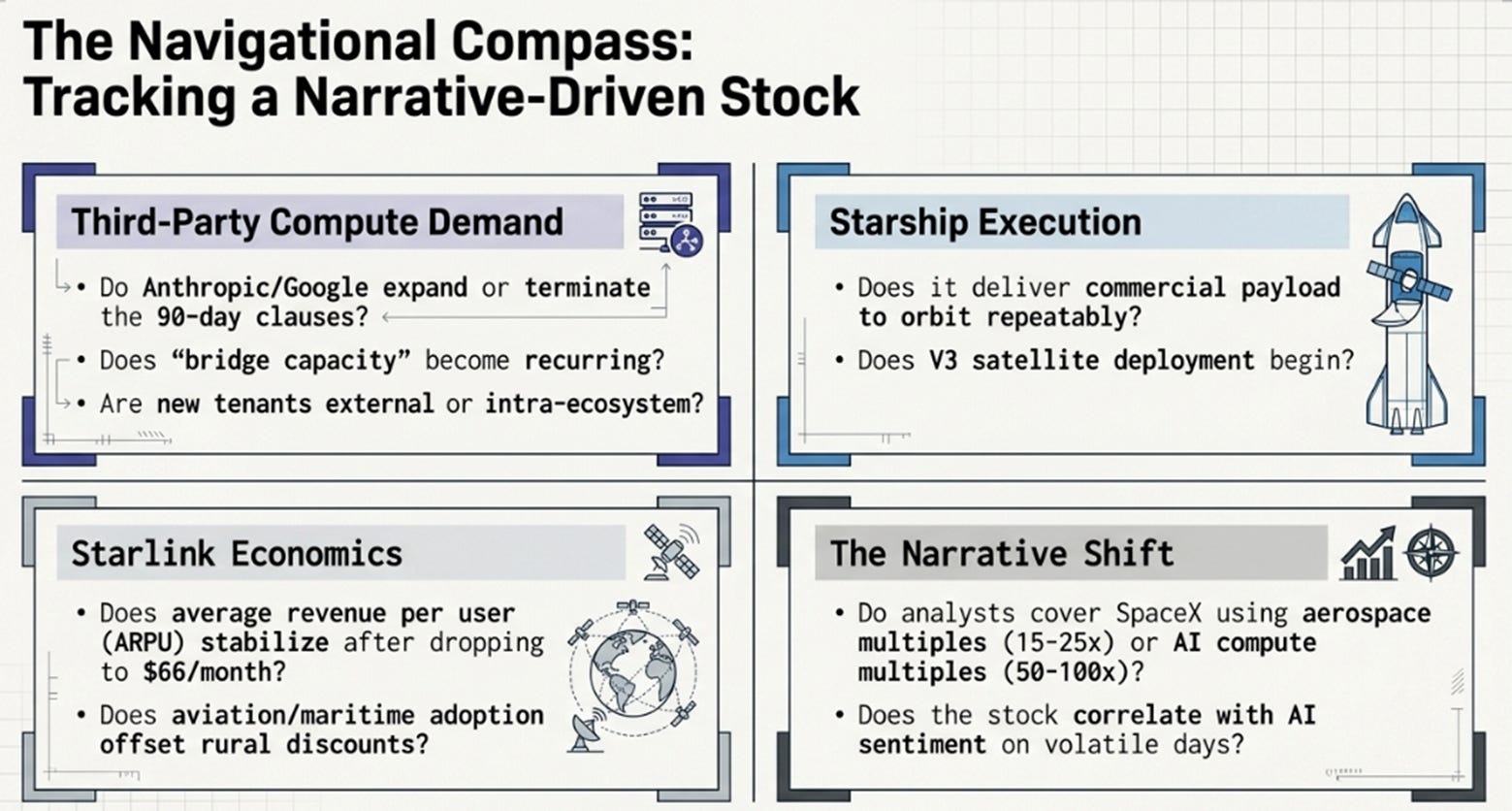

How to Follow a Narrative-Driven Stock

For most companies, belief follows proof. For Musk companies, belief often arrives early and pays for the proof. That is the uncomfortable mechanism. Narrative lowers the cost of capital, attracts talent, pressures suppliers, and gives management permission to make long-term bets that would look irrational inside a more conventional company.

This can be an advantage. It can also be a trap. If belief funds physical capacity, and that capacity wins customers, the narrative becomes self-confirming. If belief funds capacity that customers do not want, or that arrives too late, financial gravity returns.

The right way to follow SpaceX is not simply to ask whether revenue grew this quarter. It is to ask whether proof is accumulating in the places that matter.

Third-party compute demand. Do Anthropic and Google expand, renew, reduce, or terminate? Do new customers appear? Does “bridge capacity” become recurring dependency? Is pricing holding or compressing? Does SpaceX disclose utilisation rates? Is new demand coming from independent third parties or from within the Musk ecosystem?

Starship. Does it deliver payload to orbit on a repeatable basis? Does reuse become real? Does cadence increase meaningfully? Do V3 satellites begin deployment? Are there external commercial payloads, or is the manifest mostly internal Starlink missions?

Starlink. Are subscribers still growing? Is average revenue per user stabilising after the mix-driven decline from $99 to $66 per month? Are aviation and maritime customers increasing? Does direct-to-cell move from promise to meaningful use? Does the EchoStar spectrum acquisition close on schedule?

Orbital compute. This should be tracked as an option. Can SpaceX demonstrate useful compute from orbit? What is the power per kilogram? How effectively is heat removed? What are the error rates? Does the concept produce useful work at a cost that can eventually compete with terrestrial alternatives?

The narrative itself. This may sound soft, but it is not. Does the market increasingly describe SpaceX as a supplier of scarce AI compute capacity, or does it continue to see AI as a Grok story? Which analysts cover the stock, and what comparison set do they use, aerospace names at 15 to 25 times earnings, or AI and compute names at 50 to 100 times? Does the stock correlate with AI sentiment or aerospace sentiment on volatile trading days? What does Musk emphasise on the first earnings call?

Only after these questions should one return to the traditional metrics: revenue by segment, capital expenditure per megawatt, revenue per megawatt, EBITDA, free cash flow after growth spending, debt trajectory, dilution, and stock-based compensation. The numbers will eventually decide the stock. But the narrative will decide where the numbers are allowed to go first.

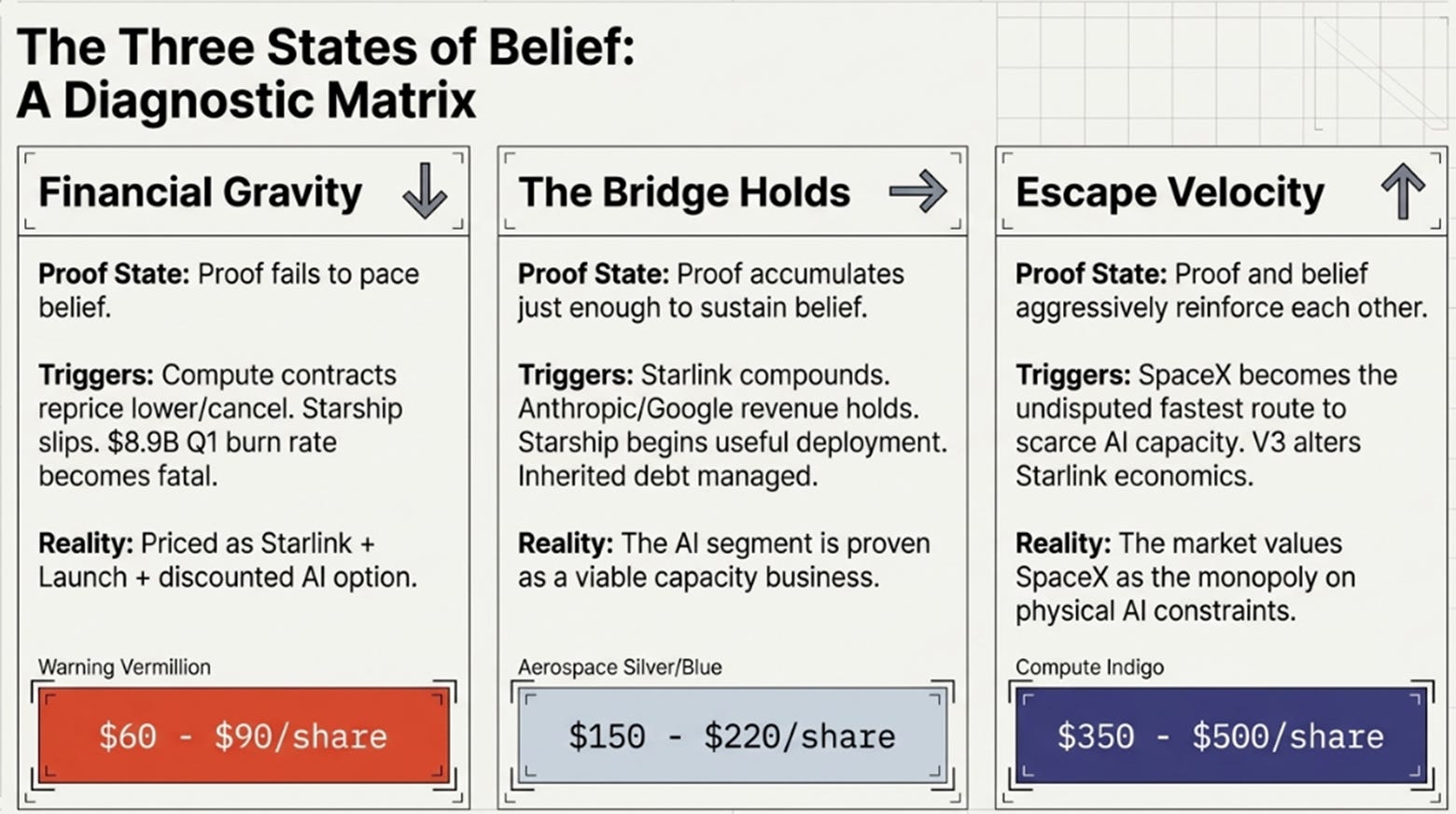

Three States of Belief

The usual labels, bull, base, and bear, are not quite right for SpaceX. This is a stock that will trade on states of belief as much as financial estimates. The better framing is to ask which regime the stock is operating in, and to watch for evidence of transitions between them.

Financial Gravity

In this state, proof fails to keep pace with belief. Starship slips. Compute contracts prove temporary or reprice lower. AI capital spending remains heavy without a clear return. Grok continues to consume resources without strengthening the broader thesis. Starlink remains an excellent business, but not enough to carry every future embedded in the IPO price. The cash burn, $8.9 billion in Q1 alone, persists while contracted revenue proves less durable than hoped. Orbital compute remains a slide in a presentation.

This is not a “SpaceX fails” case. That distinction matters. SpaceX can remain one of the most important companies in the world and still disappoint public-market investors if the stock capitalised too much too early. In this state, SpaceX is valued as Starlink plus launch plus a discounted AI option. An indicative three-year range: $60 to $90 per share.

The Bridge Holds

In this state, proof accumulates at roughly the pace required to sustain belief. Starlink keeps compounding. Starship begins useful deployment, even if slower than hoped. V3 satellites improve capacity economics. Anthropic and Google-style compute revenue mostly holds. New compute customers appear, though investors still debate contract duration and margin quality. Grok improves enough to remain strategically relevant without becoming the centre of the thesis. The inherited debt from xAI and X is managed down without further distress.

The IPO valuation was demanding, but not fatal, because the AI segment starts to look less like a cash drain and more like a capacity business with identifiable customers. An indicative three-year range: $150 to $220 per share.

Escape Velocity

In this state, proof and belief reinforce each other. Starship cadence becomes real. V3 changes Starlink economics. Compute customers expand or are joined by new entrants. SpaceX becomes the fastest route to scarce AI capacity, and the market stops treating the AI segment as “Grok plus losses” and starts treating it as a way to monetise the physical constraints of AI demand. Orbital compute moves from concept to working prototype.

Belief funds capacity. Capacity wins customers. Customers validate belief. That validation supports the stock. The stock supports further capacity creation. The loop that worked in a smaller way for Tesla, and then for launch and Starlink, begins to operate again.

In this state, investors stop asking whether the multiple is high and start asking how large the next market can become. An indicative three-year range: $350 to $500 per share.

These are not predictions. They are states. The article’s purpose is to give the reader a framework for recognising which state they are in as evidence arrives, not to declare which state is most likely.

The First Future That Has to Arrive

The SpaceX IPO asks investors to pay for several futures at once.

One future is Starlink becoming a much larger global connectivity business. Another is Starship reducing the cost of orbit enough to change satellite economics again. Another is direct-to-cell expanding the reach of mobile networks. Another is Grok becoming a meaningful AI product. Another is Colossus becoming a durable compute business. Another is compute in orbit.

Not all of these futures need to arrive for the stock to work. But the first one does.

The first future is not Mars. It is not even Grok. It is proof that the Anthropic and Google deals are not merely temporary overflow demand, but early evidence of a repeatable business in selling scarce compute capacity. If that proof arrives, if contracts hold, if new tenants sign, if the physical bottleneck persists, the rest of the thesis gets room to develop. If it does not, financial gravity returns.

SpaceX is almost certainly expensive on normal near-term financial measures. It may also be one of the few companies where normal near-term measures do not capture the mechanism investors are actually buying. The right stance is neither blind faith nor reflexive dismissal.

The right question is whether proof is accumulating fast enough to keep belief productive.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.