Spotify 4Q25 Earnings: The Taste Graph

Spotify’s 4Q25 earnings and why AI makes aggregation stronger, not weaker

TL;DR:

AI doesn’t disintermediate platforms built on subjective data. It commoditizes facts, not preference graphs trained on billions of human decisions.

The flywheel is accelerating. 751M MAUs, record Q4 net adds, rising constant-currency ARPU, and a breakout gross margin signal structural operating leverage.

The moat is behavioral. Every skip, save, and prompt deepens Spotify’s “language-to-taste” dataset: an asset that scales with AI rather than competing against it.

From Bloomberg, February 10, 2026:

Spotify Technology shares are rallying on Tuesday, after the audio-streaming company’s first-quarter forecast was better than expected, with analysts especially positive on its margin outlook... Shares up as much as 18%, the biggest intraday gain since October 2019.

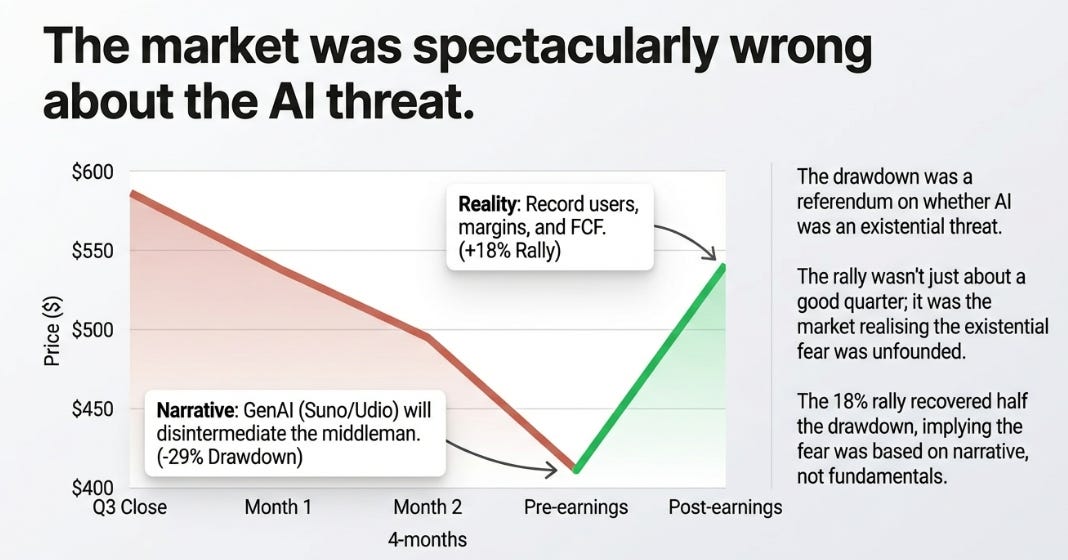

My initial reaction to the 18% pop was not that Spotify had a great quarter. It did. My reaction was that the market had spent three months being spectacularly wrong about what kind of company Spotify is, and was now being confronted with the evidence.

From its Q3 close of $580, Spotify had fallen 29% to roughly $415 heading into this print, nearly all of it attributable to a single narrative: AI music generation tools like Suno and Udio would disintermediate streaming, or at least compress Spotify’s margins and competitive position. The stock had become a referendum on whether AI was an existential threat to the audio middleman. And then Spotify reported a quarter in which it added more users than any quarter in company history, posted record gross margins, generated €834 million in free cash flow, and, most importantly, articulated the single most compelling AI strategy I’ve heard from any consumer platform in 2025.

The 18% rally was the market giving back half the drawdown. Which tells you the other half was never about fundamentals.

The Metrics Detective Work

Let me start with the table the sell-side will circulate, and then explain what it’s actually telling you.

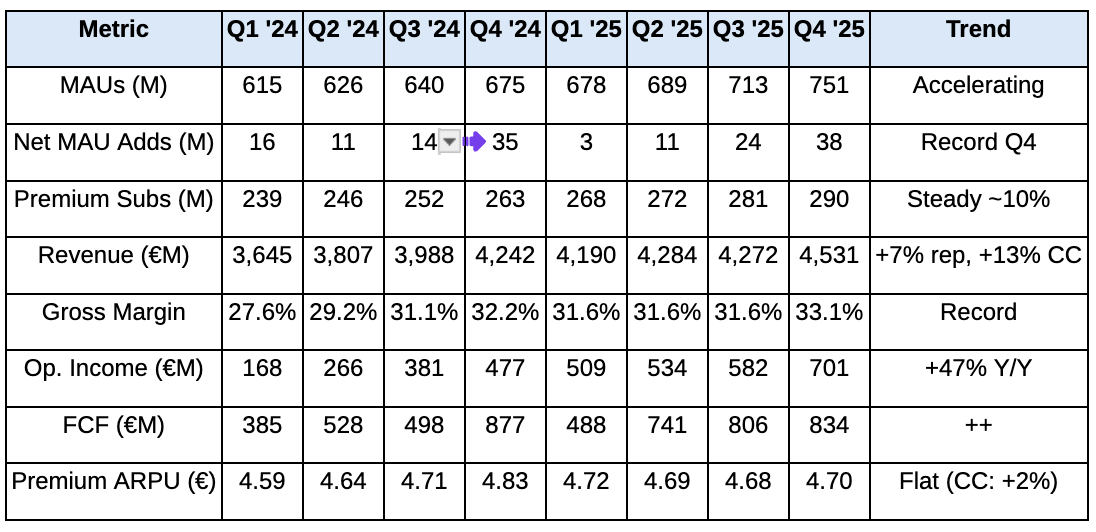

Source: Spotify Shareholder Decks, Claude estimates for select prior quarters

There are four things in this table worth unpacking.

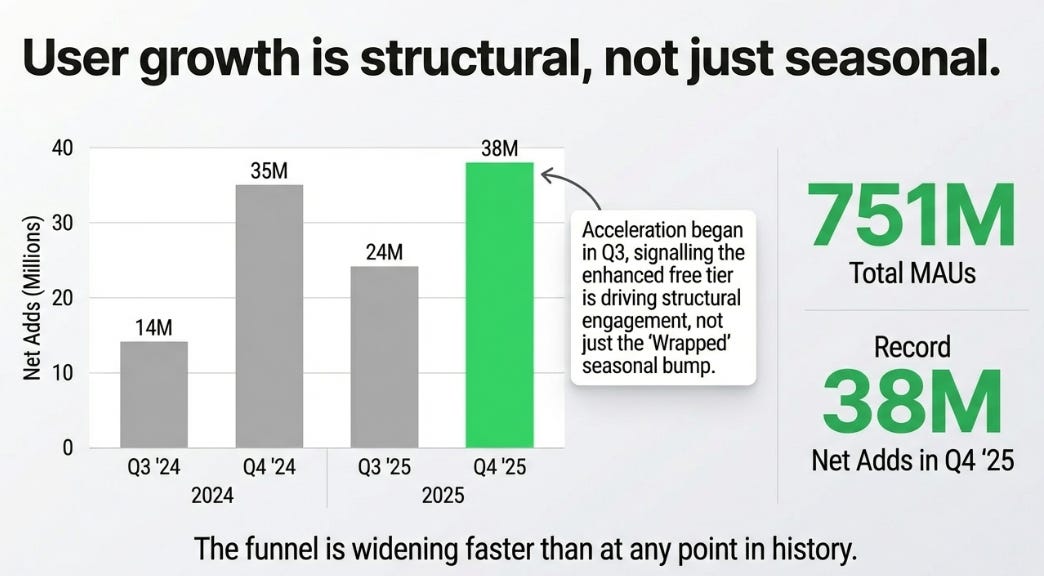

First, the MAU acceleration is real and structural, not just Wrapped. Yes, Q4 always gets a Wrapped bump, Q4 2024 added 35 million, and Q4 2025 added 38 million. But look at Q3: 24 million net adds in 2025 versus 14 million in 2024. The enhanced free tier launched in late Q3, and its engagement effects are already visible in the intake numbers. This isn’t seasonal noise. The funnel is widening.

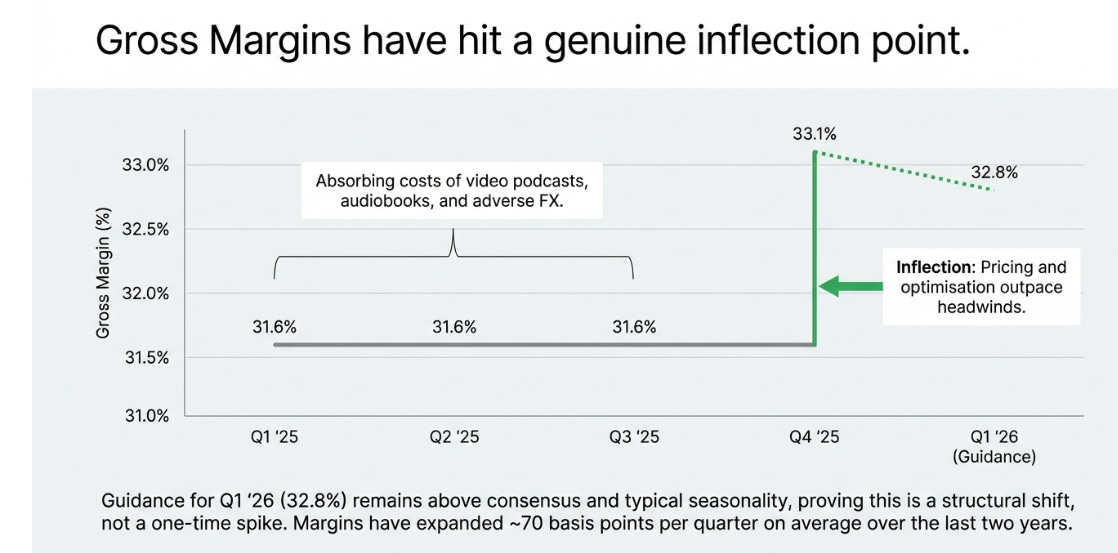

Second, gross margin has hit a genuine inflection point. The 2025 quarterly pattern tells the story: 31.6%, 31.6%, 31.6%, 33.1%. Three consecutive flat quarters followed by a breakout. The first three quarters were the company absorbing video podcast costs, audiobook expansion, and adverse FX, and still holding margins flat. Q4 was the quarter where pricing and content cost optimization finally outpaced those headwinds. The Q1 2026 guide of 32.8%, above consensus, above typical seasonal patterns, suggests this isn’t a one-time spike.

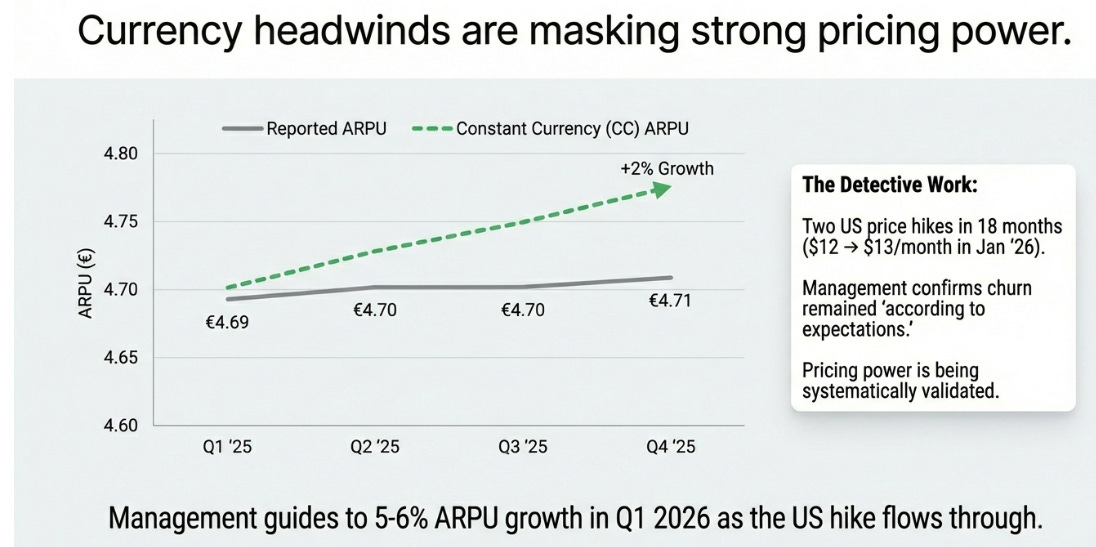

Third, ARPU tells a very specific story about pricing power. Reported ARPU has been essentially flat for a year, bouncing between €4.68 and €4.72 since Q1 2025. This looks concerning until you realize FX is masking the underlying trend: constant-currency ARPU grew +2% in Q4, and management guided to 5-6% ARPU growth in Q1 2026 as the January US price hike ($12 → $13/month) flows through. Spotify has now raised prices twice in 18 months in the US, with churn each time coming in “according to expectations.” This is pricing power being systematically validated, quarter by quarter.

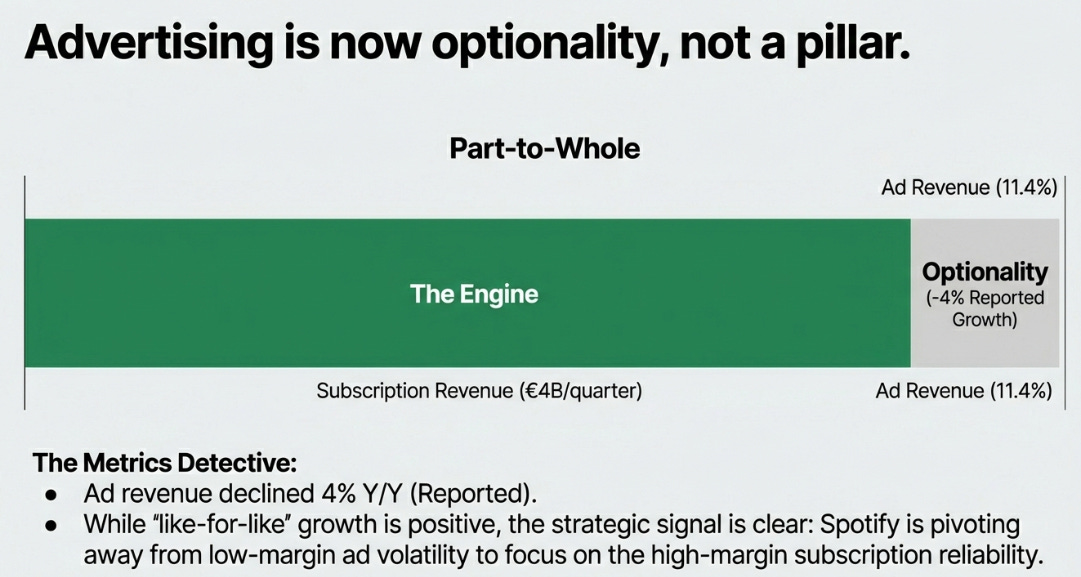

Fourth, and this is the metrics detective work, pay attention to what Spotify stopped emphasizing. For years, the company led with ad-supported revenue growth as evidence of the dual-revenue flywheel. This quarter, advertising revenue was mentioned almost as an afterthought, a few sentences from the CFO, a brief Q&A exchange. Ad revenue declined 4% Y/Y on a reported basis. Management created a new metric to explain it away: “like-for-like” growth of ~7% excluding podcast inventory optimization. When companies introduce new metrics that make underperforming segments look better, you should notice.

The strategic interpretation, though, is not bearish. It’s that Spotify is quietly giving up on advertising as a pillar and reframing it as optionality. At 11.4% of revenue and shrinking, ads are becoming a rounding error on a subscription business generating €4 billion per quarter in Premium revenue. This is a deliberate strategic choice, and probably the right one.

The Language-to-Taste Dataset

I want to spend real time on the most important thing said on the call, because I think it has implications well beyond Spotify.

Co-CEO Gustav Söderström laid out the AI thesis in his prepared remarks, but the critical moment came during Q&A when he explained the dataset Spotify is building through AI DJ and Prompted Playlist:

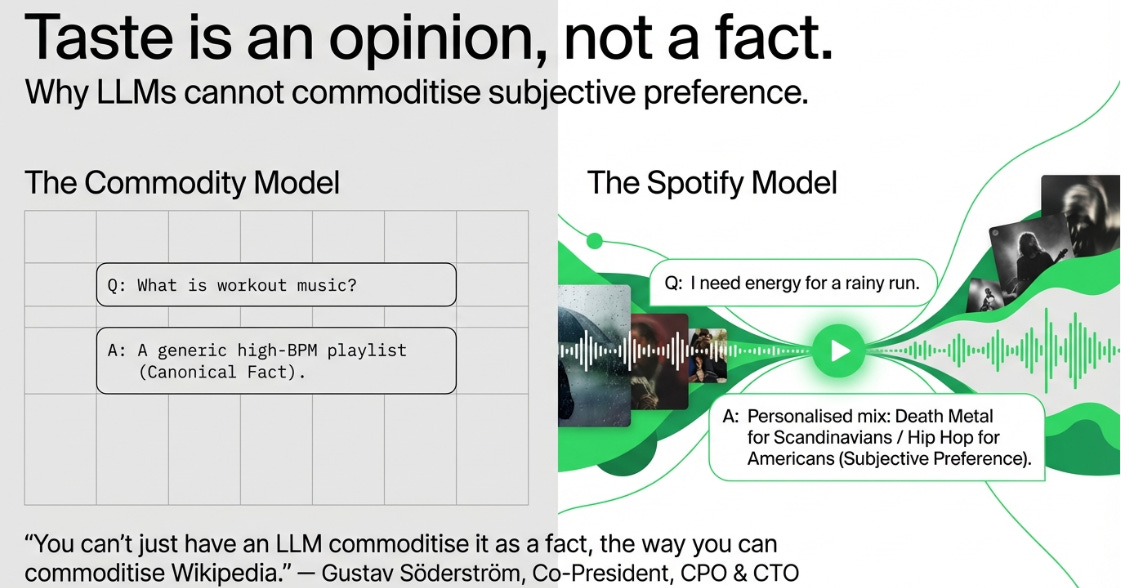

“You may think it is a canonical dataset, meaning there is a factual answer to, for example, ‘What is workout music?’ There is no factual answer to what is workout music. In fact, it turns out that taste is not a fact, it’s an opinion. So if you look at something like workout music, on average, for an American, it’s usually hip hop. For a European, it’s usually EDM. For many Scandinavians, it’s something like heavy metal or even death metal... You can’t just have an LLM commoditize it as a fact, the way you can commoditize Wikipedia.”

This is a profound strategic insight that I think most analysts missed because it wasn’t attached to a revenue number.

Here’s the framework. Over the past two years, the AI discourse around consumer companies has been dominated by a single question: “Can an LLM replace this?” The implicit assumption is that if a product’s value derives from information retrieval or content recommendation, then a sufficiently powerful language model trained on the open internet can replicate it. This assumption has driven the devaluation of search engines, news aggregators, and, apparently, music streaming platforms.

Söderström is arguing that this assumption is wrong for a specific, structural reason. Spotify’s product is not information retrieval. It is not “tell me who wrote this song” or “what albums did this artist release.” Those are canonical queries that an LLM can answer from training data. Spotify’s product is subjective preference resolution at individual scale: taking a vague, context-dependent, culturally inflected natural-language expression of mood and intent, “I need something energetic but not too loud, kind of like what I was listening to last summer”, and mapping it to specific audio content that the individual user will find satisfying.

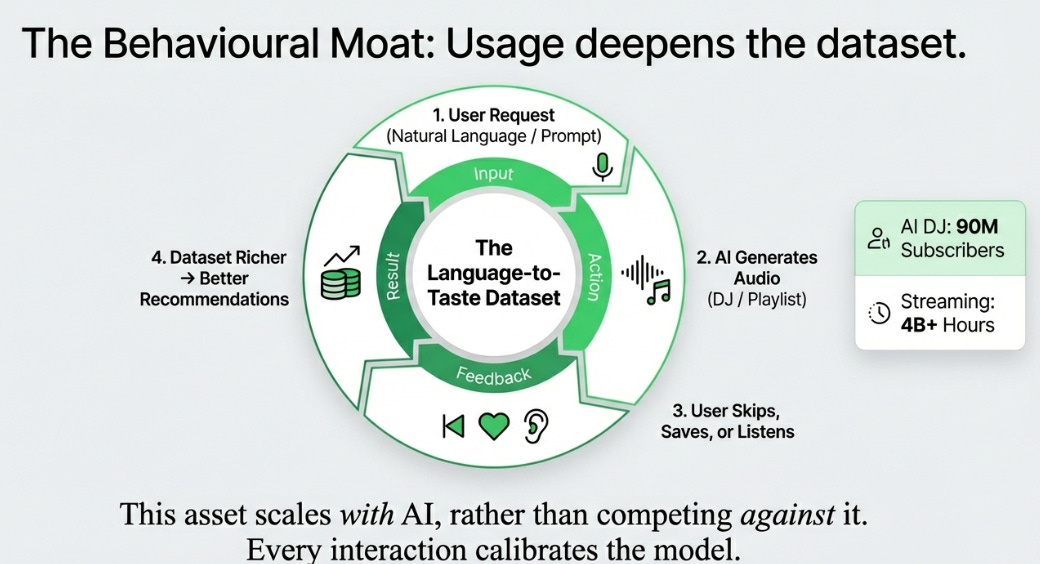

That mapping requires two things no LLM possesses: the individual’s complete behavioral history (every skip, save, replay, and listening session across years) and the population-level preference calibration (hundreds of millions of individual taste profiles, each slightly different, each trained against the same content catalog). Spotify has both. No one else does. And the products that are generating this data, AI DJ (90 million subscribers, 4 billion+ hours) and Prompted Playlist, are creating a flywheel where every interaction makes the dataset richer and the recommendations better.

This is the real moat, and it’s the kind of moat that gets wider with AI, not narrower. The more capable the language models become, the more Spotify can do with the preference signals it has already collected, and the more users interact through natural language interfaces, the more preference signals it collects. This is the exact opposite of the disruption narrative that took 29% off the stock.

I’ll make a broader observation. The companies most vulnerable to AI disruption are the ones whose core value can be expressed as structured information: factual databases, reference works, standard analysis. The companies least vulnerable are the ones whose core value is embedded in billions of subjective, idiosyncratic human preferences that only they have observed. Spotify is squarely in the latter category. So, for what it’s worth, is Netflix. And I’d argue this framework explains a lot about which consumer platforms will thrive in the AI era and which will struggle.

The Profitability Transformation in Context

Let me put some numbers on how dramatically Spotify’s economics have changed, because the sheer velocity of the transformation deserves its own analysis.

Source: Spotify filings, Bloomberg consensus estimates

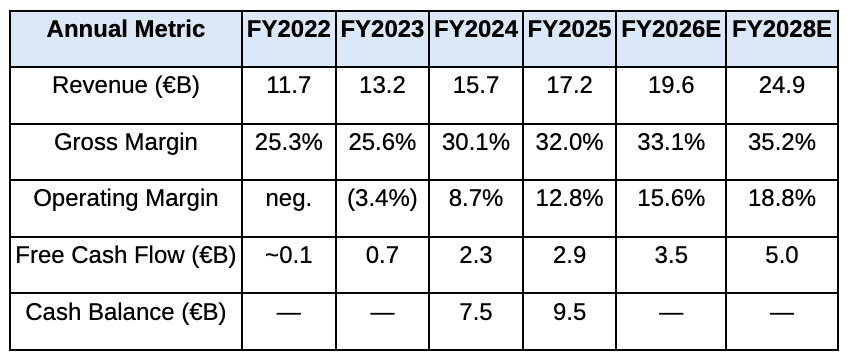

In three years, Spotify went from a 25% gross margin loss-maker to a 32% gross margin business generating nearly €3 billion in free cash flow. Consensus expects FCF to approach €5 billion by 2028. The company now sits on €9.5 billion in cash against minimal debt (€433 million long-term, plus €1.5 billion in exchangeable notes settling in March). This is not “turning profitable”, this is a complete transformation of the business economics.

The question I keep coming back to is: does the market appreciate the durability of this change, or is it still modeling the old Spotify, the one where labels could claw back margin at will?

There’s a credibility tracking exercise worth doing here. Go back to Q1 2024, when Spotify first started guiding to meaningful margin expansion. CFO Christian Luiga said then that pricing would outpace content costs and that gross margins would improve “steadily.” Here we are, eight quarters later, and gross margins have expanded from 27.6% to 33.1%, roughly 70 basis points per quarter on average. Management has beaten or met its own gross margin guidance in every single quarter during this stretch. Luiga’s guidance credibility is, by any objective measure, excellent.

Which makes his Q4 comments worth parsing carefully:

“While we do not give full year guidance for gross margin and operating margin, we are expecting both to improve in 2026. For gross margin, we expect our recent pricing adjustments to help drive revenue growth that outpaces the net content cost growth in 2026.”

And then the caveat:

“That said, the quarterly progression of our margins could again be variable, depending on the timing of disciplined investments.”

This is Luiga-speak for: “Don’t extrapolate the Q4 record linearly; we’re going to reinvest some quarters, and the margin line will be lumpy.” Having tracked his guidance for two years, I’d read this as conservative sandbagging from someone who has consistently under-promised and over-delivered. The real signal is “both improve in 2026”, that’s a commitment, not a hope.

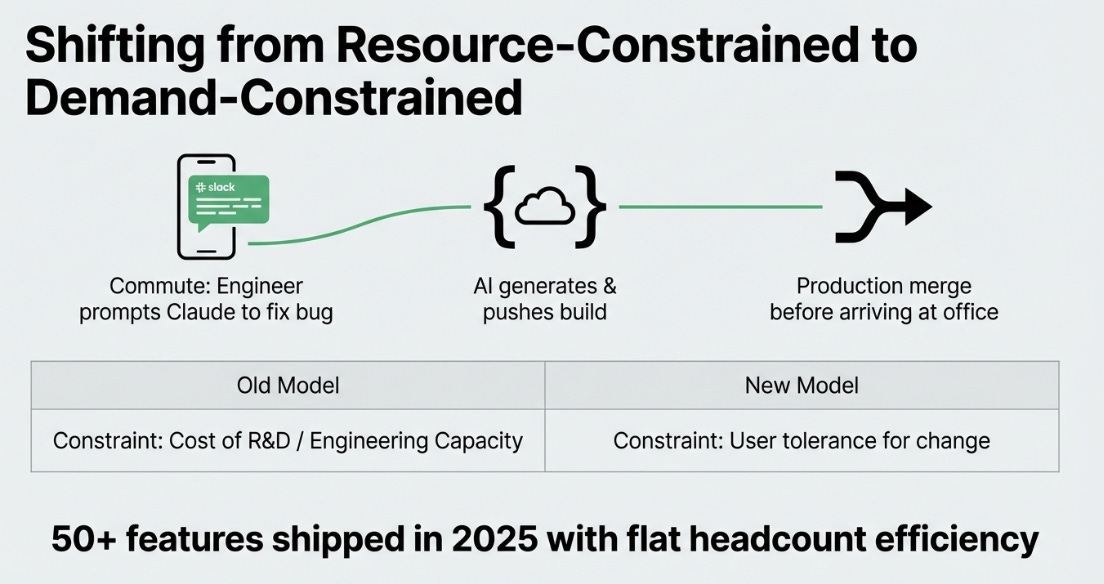

The Honk System and What It Reveals About Spotify’s Operating Model

There’s an operational detail from the call that I think is strategically significant and that most coverage has treated as a throwaway anecdote.

Söderström described an internal system called “Honk”:

“An engineer at Spotify on their morning commute from Slack on their cell phone, can tell Claude to fix a bug or add a new feature to the iOS app. And once Claude finishes that work, the engineer then gets a new version of the app, pushed to them on Slack, on their phone, so that he can then merge it to production, all before they even arrive at the office.”

And then, about senior engineers:

“They haven’t written a single line of code since December. They actually only generate code and supervise it.”

I think this matters more than the headline numbers for understanding Spotify’s trajectory. Here’s why.

The historical constraint on Spotify’s business was not demand (751 million people clearly want the product) or pricing power (they’ve proven they can raise prices with minimal churn). The constraint was the cost of building new product surface area. Every new feature, video podcasts, audiobooks, AI DJ, Prompted Playlist, mixing tools, requires engineering investment. The traditional label-versus-platform margin argument assumes that Spotify has a relatively fixed capacity to invest in product while labels extract a relatively fixed portion of revenue. If AI dramatically increases product velocity while reducing R&D cost per feature, that assumption breaks.

Spotify shipped 50+ features in 2025. Söderström didn’t say “we plan to ship more.” He said something much more interesting about the economics of doing so: that the limiting factor is no longer engineering capacity, it’s “the amount of change that consumers are comfortable with.” That is a company that has moved from a resource-constrained development model to a demand-constrained one. The implications for operating leverage are significant.

Consider this in the context of Söderström’s broader argument about AI and aggregation:

“There is this fear that software companies are not gonna exist anymore, everyone rolls their own products. I certainly don’t think that’s going to be true for consumer products. I think what will happen is something more like what happened with the Internet. When the Internet came along, everyone thought that we would all have our own web pages. What actually happened was there ended up being very few web pages. In times of lower friction, things actually tend to aggregate, not disaggregate.”

This is exactly right, and it’s the insight that connects Spotify’s AI productivity tools to its competitive position. If AI makes it cheap to build software, the winners are the companies with distribution and data advantages that new entrants can’t replicate, because those advantages become the only thing that differentiates one piece of software from another. Spotify’s distribution (751M MAUs, 2,000+ device integrations) and data (the taste graph, the preference dataset) are precisely those advantages. AI doesn’t help competitors catch up. It lets Spotify pull further ahead.

The Counter-Narrative: What Could Go Wrong

I’ve been bullish so far, so let me steelman the bear case, because there are real risks the market is right to worry about even if the specific AI narrative was wrong.

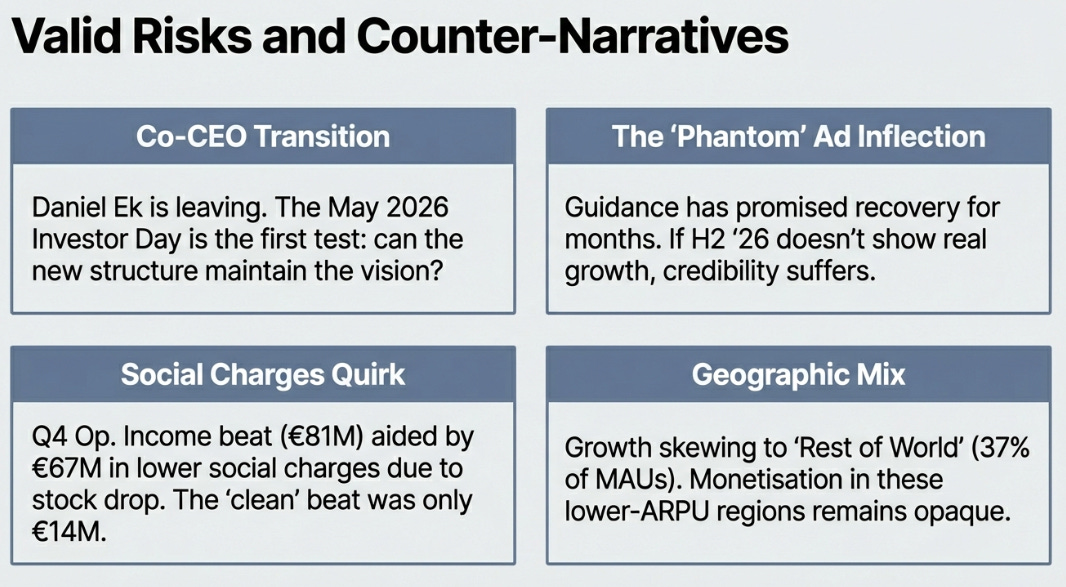

The co-CEO transition is a genuine experiment. This was Daniel Ek’s final earnings call as CEO, and he gave a gracious, confident farewell that sounded like a founder who believes the war is over. Maybe he’s right. But co-CEO structures have a terrible historical track record. Söderström described their approach, a single reporting group, 3-hour weekly E-team meetings, deliberate synchronization, and it sounded thoughtful. But the real test isn’t whether they can run a meeting together; it’s whether they can make hard tradeoffs together when the product vision and the revenue target pull in opposite directions. The May 2026 Investor Day will be the first public test. I’ll be watching for whether two people can tell one story.

The advertising business has been “about to inflect” for a while. Norström has been guiding to an H2 advertising recovery since mid-2025. We’re now entering H1 2026, and ad revenue still declined on a reported basis in Q4. The like-for-like adjustments are reasonable, and the ad tech rebuild is a real thing, but at some point the company needs to deliver actual ad revenue growth, not just increasingly creative ways of explaining why it’s declining. If H2 2026 comes and goes without a visible inflection, this becomes a credibility issue for the new leadership.

The Social Charges quirk is worth more scrutiny than it gets. €67 million of the €81 million operating income beat came from the stock falling. Prior-year Q4 carried €97 million in Social Charges, meaning roughly €147 million of the Y/Y improvement was this line item alone. Investors who take the operating income beat at face value without adjusting for this are being naive. The “clean” beat was roughly €14 million, real, but modest.

Geographic mix continues to shift toward lower-ARPU markets. Rest of World went from 34% to 37% of MAUs in a single year. If these users don’t eventually convert at rates that justify the growth investment, the record MAU numbers are a vanity metric. Management has been conspicuously vague about regional conversion rates, which is the kind of thing you’re vague about when the numbers aren’t great.

The Strategic Picture

Zoom out. What does this quarter tell us about where Spotify sits in the broader competitive landscape?

Three years ago, the knock on Spotify was that it was a commodity music distributor trapped between powerful label suppliers and indifferent consumers, operating at structurally thin margins with no path to sustained profitability. Every part of that thesis has been systematically disproven. The margins have expanded by 800 basis points. The free cash flow has gone from negligible to €2.9 billion annually. The user base has grown from ~500 million to 751 million MAUs. The product has expanded from music-only to podcasts, audiobooks, video, and AI-powered interactive experiences. And the data moat, the thing that was supposedly absent, turns out to be the most defensible asset of the AI era.

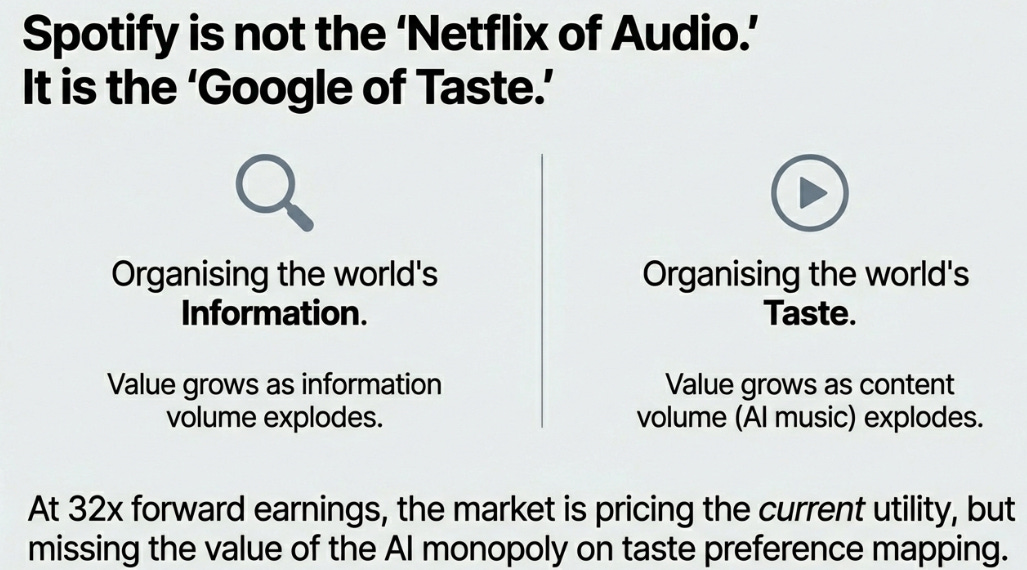

The comparison I keep reaching for is not Netflix (which Spotify structurally resembles in its subscription model) but Google. Google’s core insight was that organizing the world’s information becomes exponentially more valuable as the volume of information grows. Spotify’s emerging insight is that organizing the world’s taste preferences becomes exponentially more valuable as the volume of content grows. AI music generation doesn’t threaten Spotify for the same reason the explosion of web content didn’t threaten Google , it made the search engine more essential, not less.

At 32x forward earnings with 18% EPS growth, the stock is fairly valued for what it is today. What it doesn’t price is what Spotify is becoming: the company that owns the mapping between human language and human taste, at global scale, in the age of infinite content. If you believe that dataset has the kind of compounding value I think it does, the current price is a gift. If you think taste can be commoditized by a sufficiently large language model, sell the stock.

I know which side I’m on.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.