Tencent’s 1Q26 Earnings - The tollbooth moves from metaphor to architecture

The market sees AI capex. Tencent is trying to build the tollbooth for China’s agent economy.

TL;DR

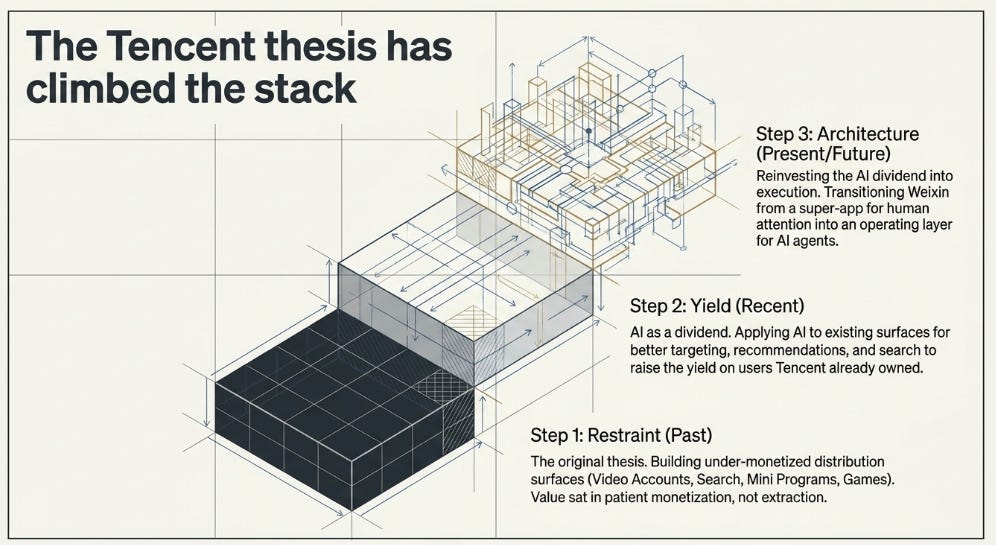

The Tencent thesis has not reversed; it has climbed the stack. We started with under-monetized distribution, then AI-driven yield, and now the question is whether Weixin becomes the operating layer where AI agents actually act.

1Q26 gave evidence, not victory. Core Tencent remains strong enough to fund the buildout, ex-new-AI operating profit grew 17%; while Hy3, WorkBuddy, AIM+, Video Accounts, and Mini Programs-as-skills show the tollbooth moving from metaphor to architecture.

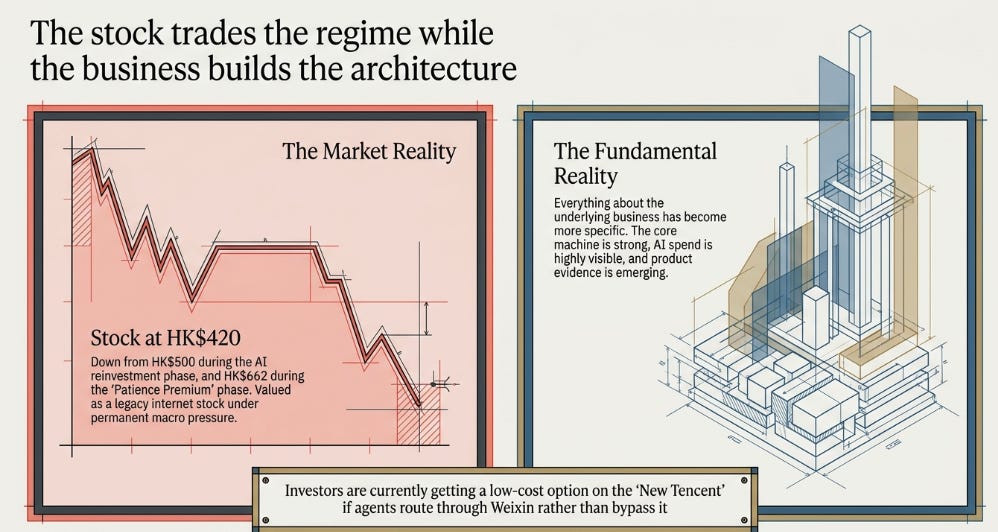

The market is rationally skeptical, but the price may be too harsh. At around HK$420, Tencent is being valued like old Tencent under China-internet pressure, while investors get a low-cost option on new Tencent, if agents route through Weixin rather than bypass it.

The stock is at HK$420. It was HK$662 when we wrote The Patience Premium. It was around HK$500 when we wrote that the AI dividend was being reinvested. Everything we have said about the business has become more specific. None of it has been rewarded by the stock.

That requires an honest reckoning before we earn the right to say anything about 1Q26.

The original Tencent thesis was about restraint. Tencent had spent years building assets it deliberately refused to over-monetize: Video Accounts, Weixin Search, Mini Programs, Mini Shops, payments, games. The point was not that Tencent lacked revenue levers. It was that Tencent had more levers than the market valued, because management had chosen not to pull them too early.

The second thesis was about yield. AI was not primarily valuable to Tencent because it could build the biggest foundation model. It was valuable because Tencent already owned the distribution surface. Better recommendations, better targeting, better content creation, better search and better live operations could raise yield on users Tencent already had.

The third thesis forced a correction. The AI dividend was real, but it was not simply being harvested. Tencent was reinvesting it. We were right that AI could improve the core. We were wrong that Tencent would avoid the infrastructure cycle. Management chose to spend.

That is not a reversal. It is an evolution. The strategic direction has been consistent: Tencent’s value sits in distribution, not just in products; in controlled surfaces, not just in content; in patient monetization, not extraction. What changed was the mechanism. First levers, then yield, now execution.

The question after 1Q26 is therefore not whether Tencent still has a patience premium. It does. It is not whether AI is improving the business. It is. The question is more ambitious and more dangerous:

Can Tencent turn Weixin from a super-app for human attention into an operating layer for AI agents — without turning AI into a permanent tax on the core business?

The Question Changed

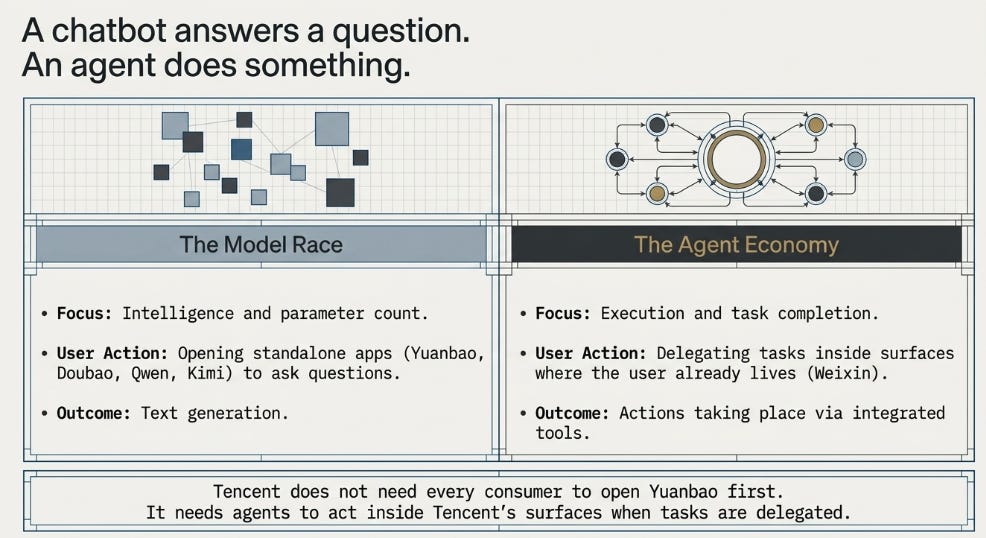

A chatbot answers a question. An agent does something.

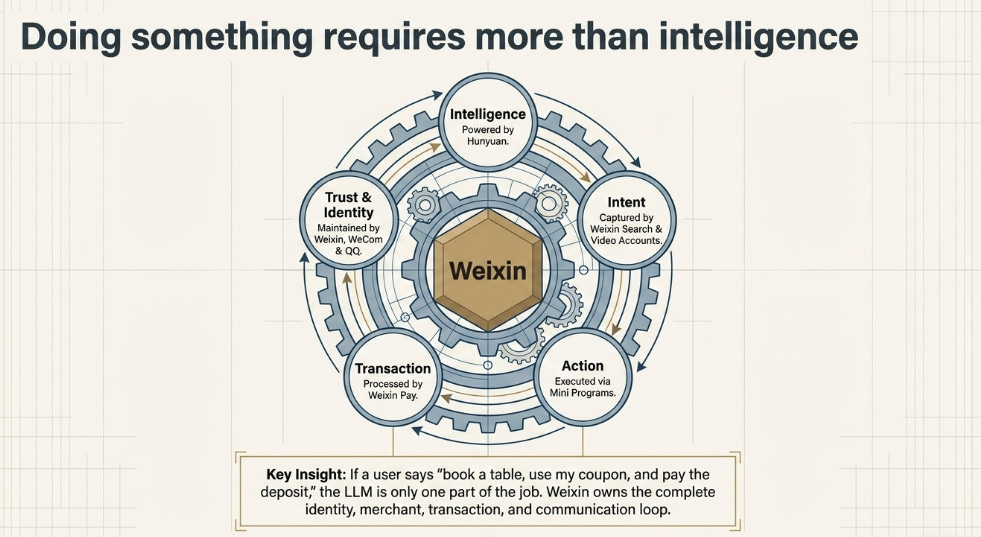

That distinction matters. Doing something requires more than intelligence. It requires identity, permissions, service access, payment rails, communication and trust. Tencent has a model, Hunyuan. But that is not the heart of the thesis.

Tencent has Weixin.

Weixin has the user relationship. Mini Programs provide service access. Weixin Pay processes transactions. WeCom and QQ extend the communication layer into work and social contexts. Video Accounts captures attention. Weixin Search captures intent. Tencent Cloud provides infrastructure. Games, music, video and literature provide IP and engagement. Hunyuan increasingly provides intelligence.

This is why the model race is the wrong frame. Tencent does not need every Chinese consumer to open Yuanbao before Doubao, Qwen or Kimi. It needs agents to act inside Tencent’s surfaces when users delegate tasks.

The product is not the chatbot. The product is Weixin with agents inside it.

1Q26 mattered because this idea moved from metaphor toward architecture.

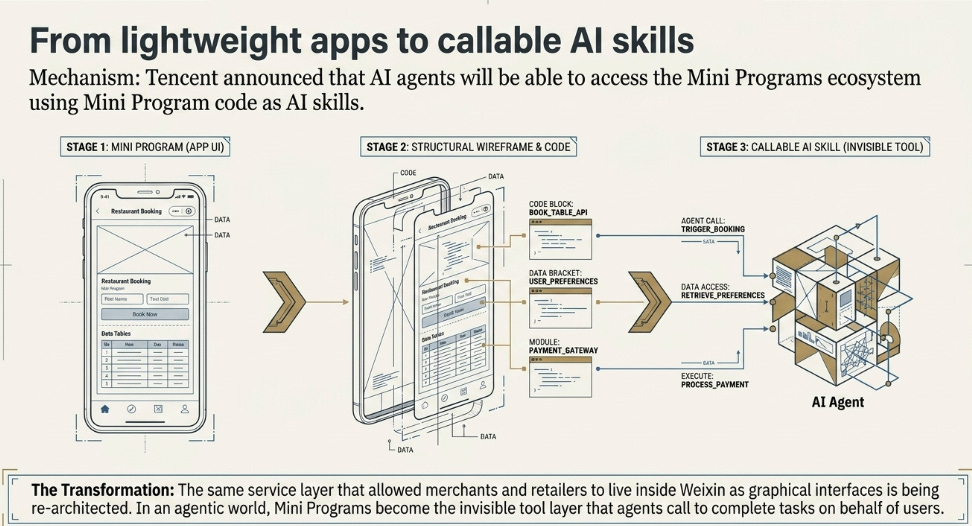

Tencent said users can control AI agents through Weixin, WeCom, QQ, Yuanbao, QQ Browser and third-party applications. More importantly, it said that over time, AI agents will be able to access the Mini Programs ecosystem using Mini Program code as AI skills.

That sentence is the article.

Mini Programs were originally lightweight apps inside Weixin. In an agentic world, they become callable tools. The same service layer that let merchants, restaurants, government services, games, retailers and content providers live inside Weixin can become the tool layer agents call when they need to complete a task.

If a user says, “book a table, use my coupon, tell my friend, and pay the deposit,” the model is only one part of the job. The agent needs identity, merchant access, transaction capability and a communication loop. Weixin has all four.

That is the tollbooth.

Two Companies, One Filing

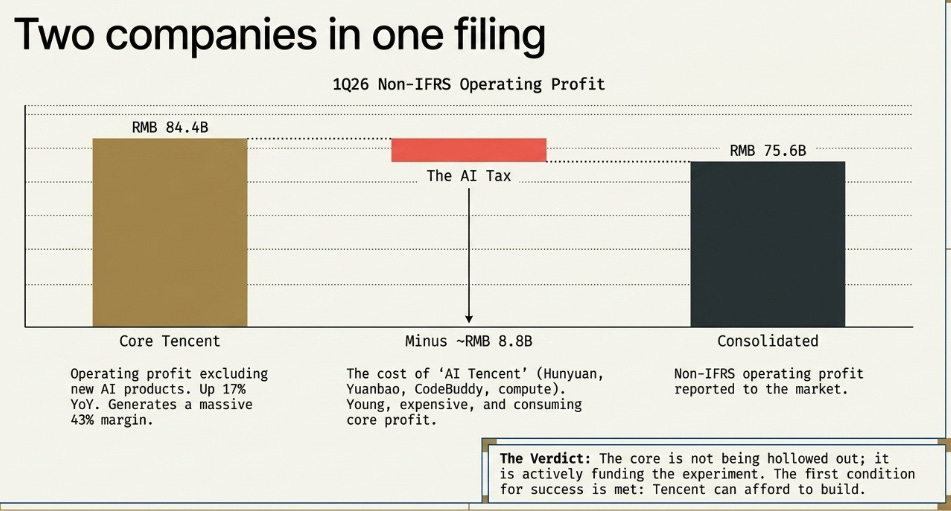

The most important number in Tencent’s quarter was not revenue. Revenue grew 9% to RMB196.5 billion. Gross profit grew 11%. Non-IFRS operating profit grew 9%. Non-IFRS net profit grew 11%. Fine numbers, not extraordinary numbers.

The important number was RMB84.4 billion.

That was non-IFRS operating profit excluding new AI products, up 17% year-on-year. Consolidated non-IFRS operating profit was RMB75.6 billion. The difference — roughly RMB8.8 billion — is the cost of AI Tencent: Hunyuan, Yuanbao, CodeBuddy, WorkBuddy, QClaw and the associated product investments.

Tencent is now effectively showing investors two companies in one filing.

The first is Core Tencent: games, ads, payments, Weixin, content, cloud and enterprise services. This business is still compounding operating profit at a mid-teens rate and, excluding new AI products, generated a 43% non-IFRS operating margin.

The second is AI Tencent: young, expensive, not yet fully monetized, and consuming some of the profit the core business generates.

This is the cleanest evidence that the thesis has not broken. The core is not being hollowed out. It is funding the experiment.

That does not mean the experiment is automatically good. A great core business can fund bad projects for years. The question is whether AI becomes a compounding layer or a permanent tax. But the first condition is met: Tencent can afford to build.

The market sees the same facts and reaches a different conclusion. It sees capex, depreciation, slower buybacks and no explicit AI ARR. It sees a China internet stock in a hostile regime. It sees management calling the stock dislocated while still choosing compute over a more aggressive repurchase.

The market is not stupid. It is refusing to capitalize the tollbooth until the tolls are visible.

The Storm and the Tollbooth

This is the part we underweighted.

The prior pieces focused on Tencent’s supply side: what Tencent could build, what levers it could pull, what AI could improve. The demand side — what happens when China consumption is weak, Hong Kong tech de-rates, and investors sell the whole internet complex — was treated as a risk, not the regime.

That was too light.

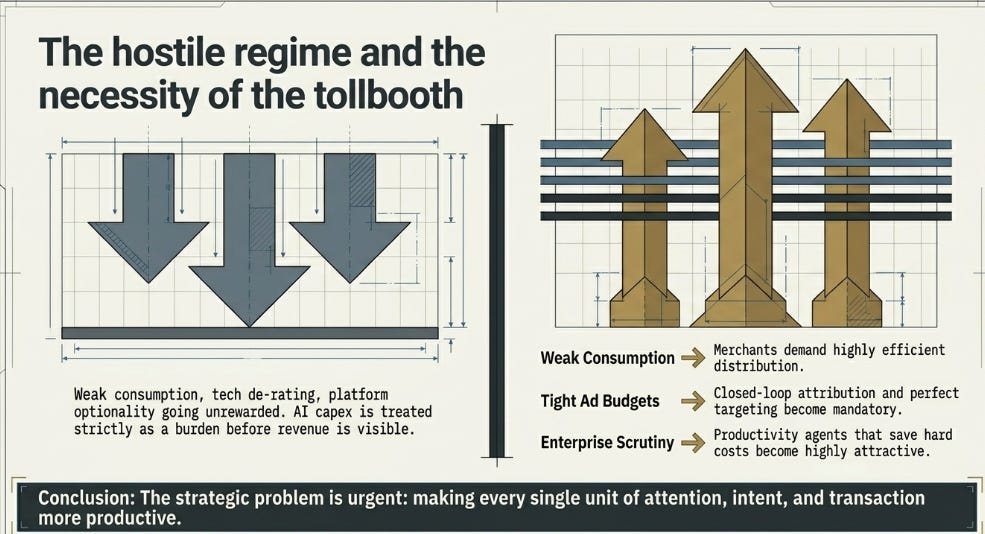

Tencent is not falling because investors carefully modeled WorkBuddy and rejected it. It is falling because the regime is hostile. China internet is in a penalty box. AI capex is being treated as a burden before revenue is visible. Capital is not rewarding Hong Kong-listed platform optionality. The market is asking for proof, not architecture.

The uncomfortable truth is that both sides can be right. Tencent can be building something valuable, and the stock can stay cheap until the value is legible.

But there is an inversion worth taking seriously: the same regime crushing the stock may make the tollbooth more necessary.

When consumers are cautious, merchants need more efficient distribution. When ad budgets tighten, better targeting matters more. When enterprises scrutinize spend, productivity agents that save time and cost become more attractive. When platforms compete for scarce dollars, closed-loop attribution becomes more valuable.

That does not automatically make Tencent immune. Weak consumption can still hurt payments, ads, games and merchant appetite. But it does make the strategic problem Tencent is solving more urgent: how to make every unit of attention, intent and transaction more productive.

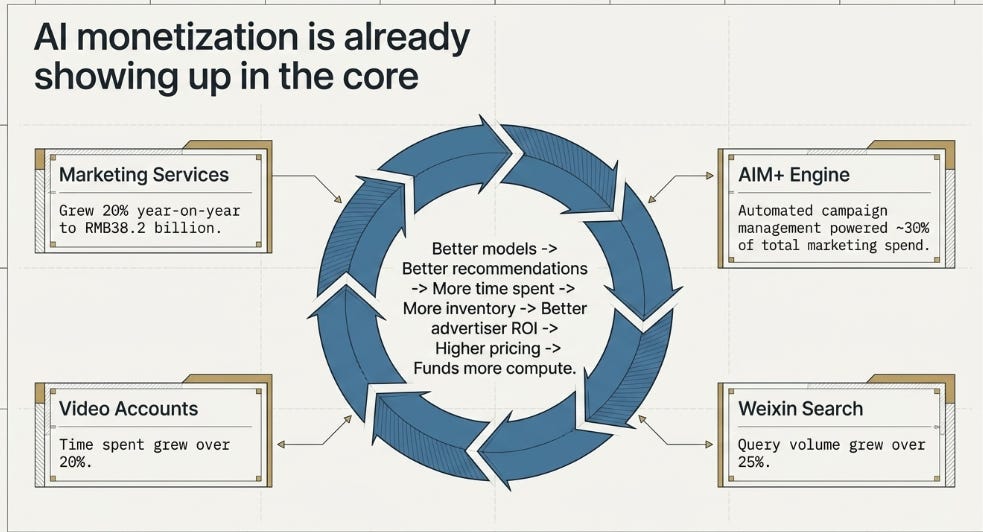

Advertising is the first proof.

Marketing Services grew 20% year-on-year to RMB38.2 billion. AIM+, Tencent’s automated campaign management solution, powered roughly 30% of total marketing services spend. Video Accounts time spent grew over 20%. Weixin Search query volume grew over 25%.

This is AI monetization already showing up in the old business.

Better models improve recommendations. Better recommendations increase time spent. More time spent creates inventory. Better targeting improves advertiser ROI. Higher ROI supports pricing. Higher monetization funds more compute. More compute improves the models again.

That is the AI dividend. The difference now is that the dividend is funding the tollbooth.

The Quarter Was Better Than the Headline

The headline revenue miss was real, but it was not the story.

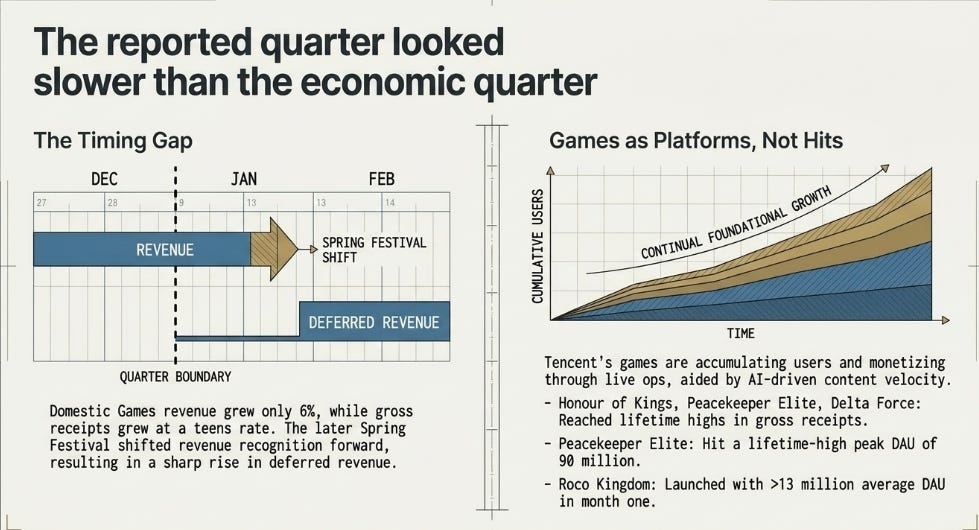

Domestic Games revenue grew only 6%, while gross receipts grew at a teens rate. The gap was timing: the later Spring Festival shifted revenue recognition into future quarters. Deferred revenue rose sharply, which means some of the economic activity already happened but has not yet appeared in reported revenue.

More importantly, the games business looked structurally strong. Honour of Kings, Peacekeeper Elite and Delta Force reached lifetime highs in gross receipts. Peacekeeper Elite hit a lifetime-high peak DAU of 90 million. Roco Kingdom launched with more than 13 million average DAU in its first month. League of Legends saw a resurgence after process and content changes at Riot.

This is not just a good games quarter. It is evidence that Tencent’s games are behaving less like hits and more like platforms.

A hit launches, peaks, fades and needs replacement. A platform accumulates users, adds modes, expands content, deepens social loops and monetizes through live operations. AI helps because it increases content velocity: 3D assets, animation, rendering, intelligent guides, NPC behavior, personalization and faster refresh cycles.

The reported quarter looked slower than the economic quarter.

What Would Prove the Tollbooth

The thesis is stronger than before, but the burden of proof is also higher.

Tencent has not yet disclosed agent transaction volume, agent task completion, WorkBuddy ARR, Mini Program AI-skill usage, or a clear payback period for AI capex. Retention is useful. Deployment across internal products is useful. OpenRouter token usage is useful. None of it is the same as toll revenue.

That is why the market is skeptical.

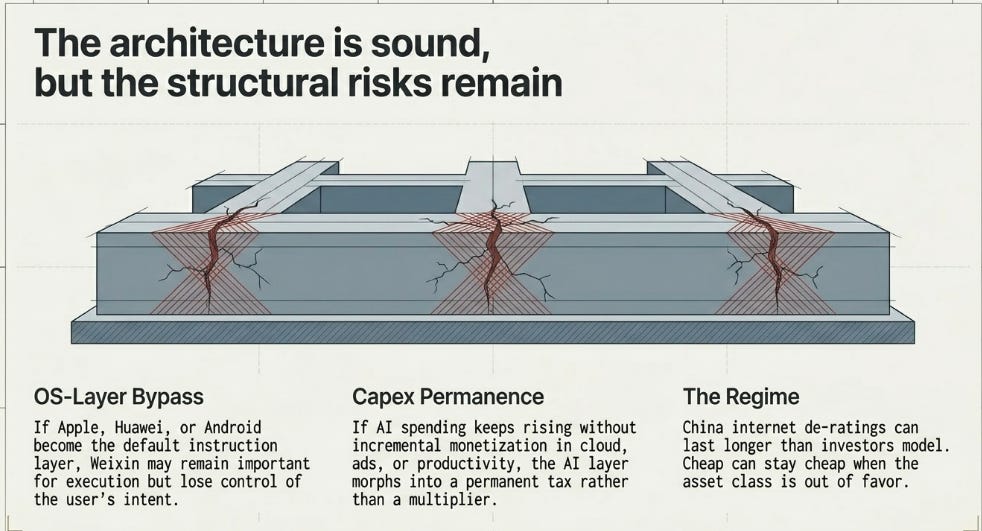

The single biggest risk is the OS-layer bypass. If Apple, Huawei, Android or another device-level agent becomes the default instruction layer, Weixin may remain important for execution but lose control of intent. In that world, Tencent is still a powerful infrastructure layer, but not necessarily the agent operating layer.

The second risk is capex permanence. If AI spending keeps rising while cloud, ads, productivity and games do not show enough incremental monetization, the AI layer becomes a tax on Core Tencent rather than a multiplier of it.

The third risk is the regime. China internet de-ratings can last longer than investors expect. Cheap can stay cheap when the factor is out of favor.

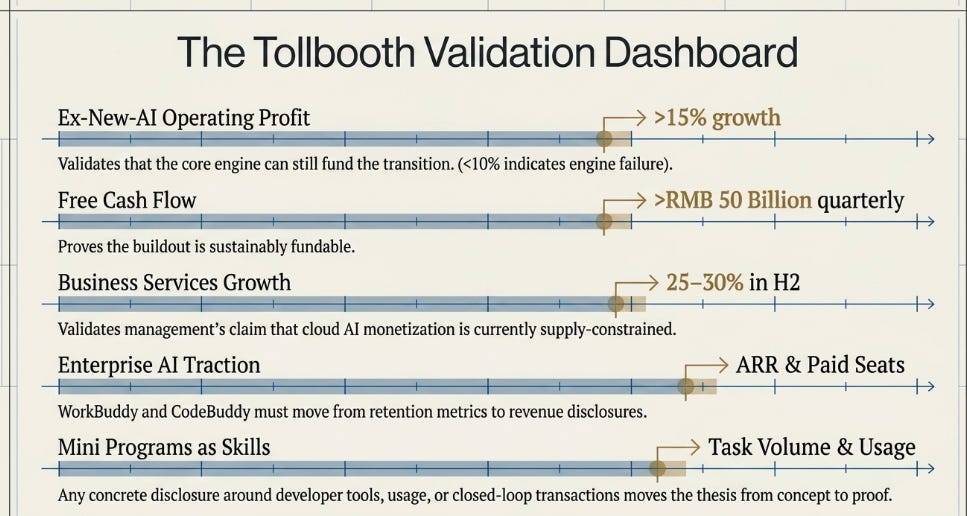

So the dashboard matters.

Ex-new-AI operating profit growth above 15% means the core can still fund the transition. Below 10% means the engine is weakening. Business Services growth above 25–30% in the second half would validate management’s claim that cloud AI monetization was supply constrained. Video Accounts ad load moving toward 6–7% while time spent still grows double digits would prove AI-powered monetization. WorkBuddy and CodeBuddy need to move from retention to revenue: paid seats, ARR, enterprise customers, task volume or token consumption. Quarterly free cash flow above RMB50 billion means the buildout is fundable. Below RMB40 billion for multiple quarters means the market’s concern is right. Any disclosure around Mini Programs as AI skills — timeline, developer tools, usage, task volume, closed-loop transactions — would move the thesis from concept to proof.

Three Futures

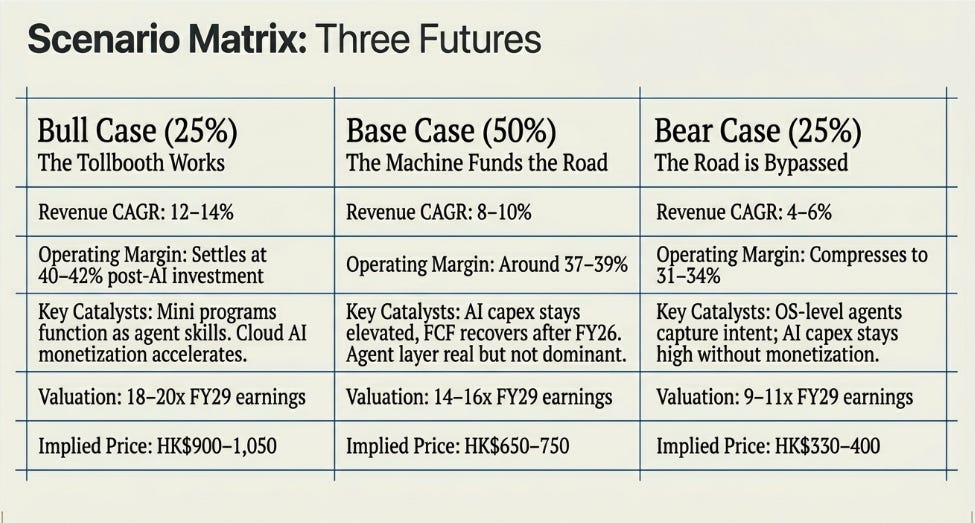

The bull case is The Tollbooth Works. Revenue compounds at 12–14% over three years. Gross margin reaches 59–60%. Non-IFRS operating margin settles around 40–42% even after AI investment. Business Services sustains 25%+ growth as Tencent Cloud monetizes AI demand. Marketing Services grows high-teens to low-20s as Video Accounts ad load rises without damaging engagement. WorkBuddy and CodeBuddy move from retention to revenue disclosures. Mini Programs become agent skills in practice, not just concept. The market re-rates Tencent to 18–20x FY29 earnings. That points to roughly HK$900–1,050. Probability: 25%.

The base case is The Machine Funds the Road. Revenue compounds at 8–10%. Gross margin rises gradually to 57–58.5%. Non-IFRS operating margin remains around 37–39%. Games remain resilient. Ads continue to outgrow the industry. AI capex stays elevated, but free cash flow recovers after FY26. The agent layer becomes real but not yet dominant. The market applies 14–16x FY29 earnings. That points to roughly HK$650–750. Probability: 50%.

The bear case is The Road Is Bypassed. Revenue compounds at 4–6%. Gross margin falls toward 54–55%. Non-IFRS operating margin compresses to 31–34%. AI capex stays high without visible monetization. Business Services fails to accelerate. Video Accounts monetization stalls or hurts engagement. OS-level agents capture intent before Weixin agents form habits. Tencent remains a good old internet company, not the action layer for the new one. The market values it at 9–11x FY29 earnings. That points to roughly HK$330–400. Probability: 25%.

The scenario table says something important. The bull case is no longer simply “Tencent monetizes Video Accounts.” That was the Patience Premium. The bull case now requires Tencent to own a new layer.

The burden of proof is higher. The entry price is lower.

The Stock and the Thesis

So, have we changed our view too often?

I do not think so. The strategic direction has been consistent. The evidence changed, and the mechanism evolved.

We were right that Tencent had under-monetized distribution. We were right that AI could raise yield on that distribution. We were wrong that Tencent could avoid the infrastructure cycle. We were right to update the thesis from harvesting to building. 1Q26 now gives evidence that the buildout is real, but not yet proof that it pays.

That is the honest answer.

Tencent’s 1Q26 did not prove it owns China’s agent economy. It proved something narrower but still important: the core machine is strong, the AI spend is visible, the product evidence is emerging, and the market is not paying much for the possibility that the tollbooth works.

The stock is trading the regime. The thesis is trading the tollbooth.

One of those is temporary. The other is still unproven. That is what makes the position uncomfortable. It is also what makes it interesting.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.