Tencent’s 4Q25 Earnings: The AI Dividend Gets Reinvested

Tencent proved it could monetise AI without an arms race. The real question now is whether WeChat becomes the execution layer for China’s agent economy.

TL;DR

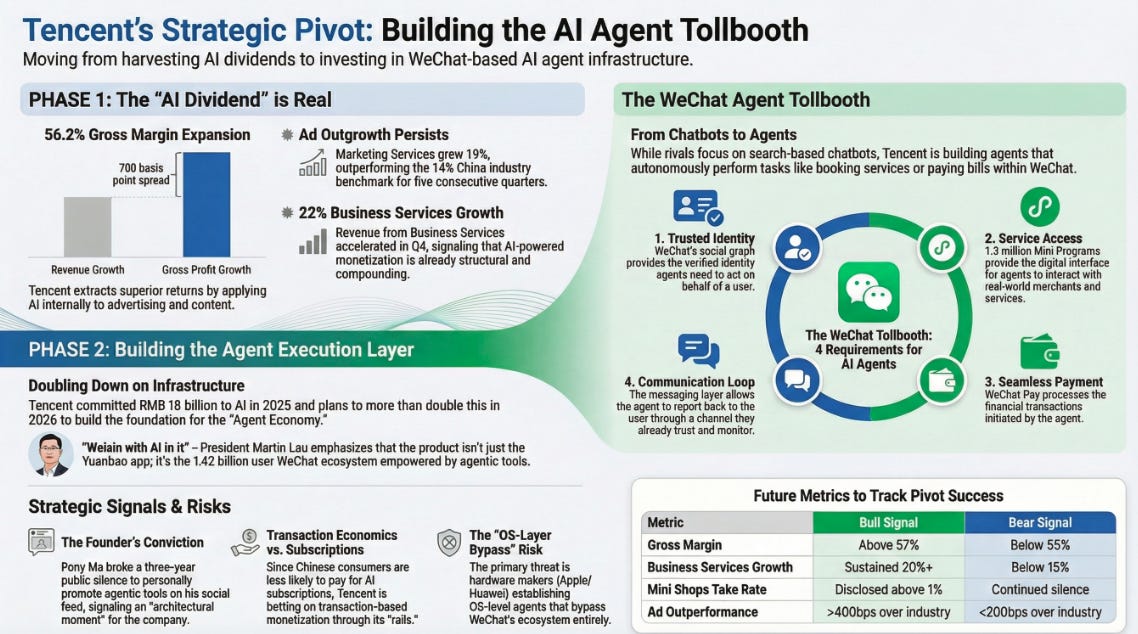

The original operating thesis held. Margins expanded, ad outgrowth persisted, and Business Services accelerated, proof that Tencent’s AI dividend is real and already compounding in the core business.

What broke was the capital allocation assumption. Tencent is no longer avoiding the infrastructure cycle; it is choosing to reinvest heavily, betting that WeChat can become China’s execution layer for AI agents.

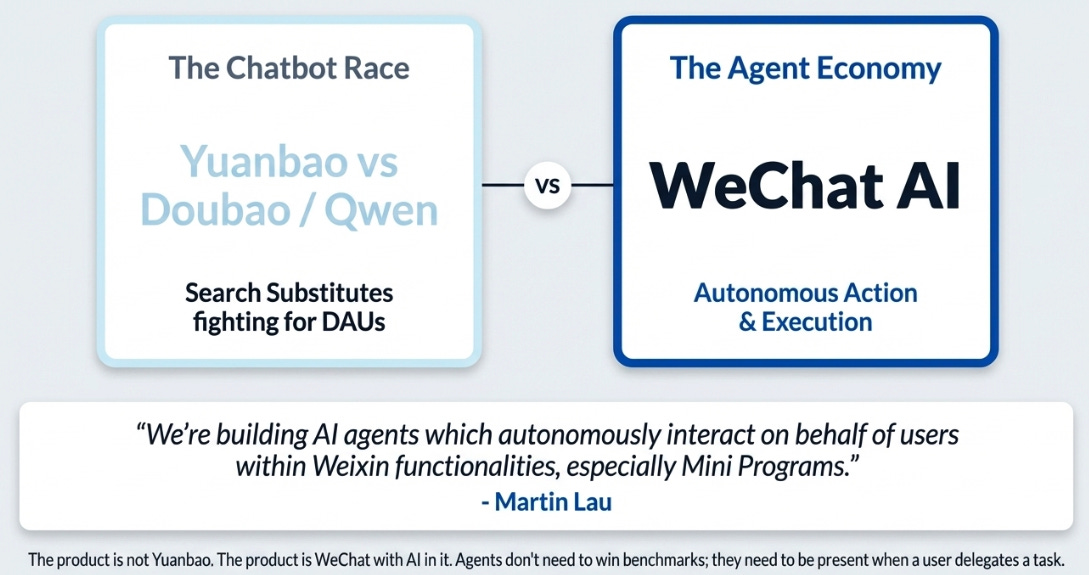

The market may still be asking the wrong question. This is no longer mainly about Yuanbao versus rival chatbots, it is about whether Tencent owns the rails that agents will need for identity, service access, payments, and user communication.

Three months ago we wrote that Tencent’s edge was being profitable while rivals burned capital. The thesis was clean: AI value accrues to those who own the user relationship, not those who build the biggest datacenter. We called it the AI dividend, the 700 basis point spread between gross profit and revenue growth that proved you could extract superior AI returns without entering the infrastructure arms race.

Then Martin Lau said this on the Q4 FY25 earnings call:

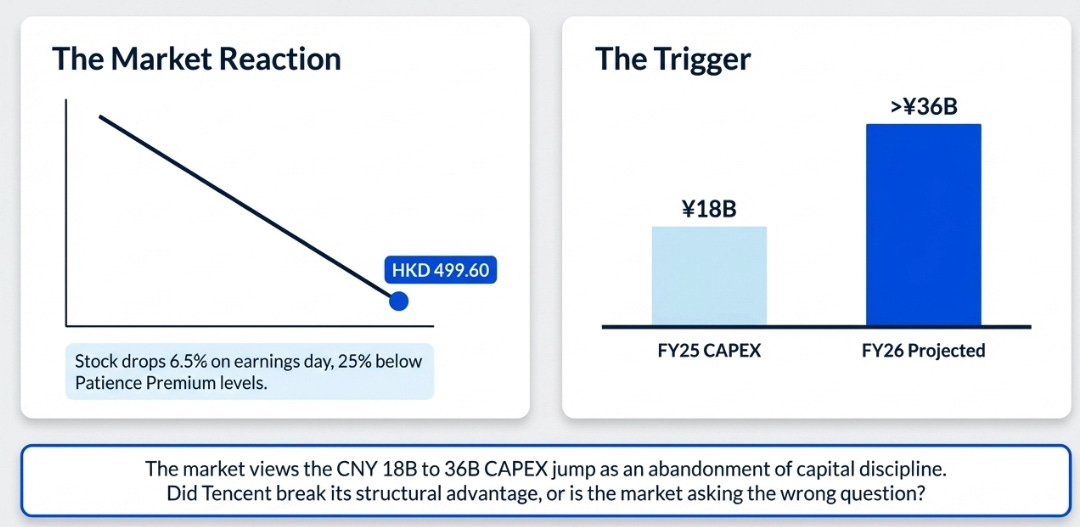

“Our spending on our two biggest new AI products, HunYuan and Yuanbao, was CNY 7 billion in Q4 of 2025 and CNY 18 billion for the full year. We expect to more than double these investments in 2026.”

The stock fell 6.5% on the day. It has since declined to HKD 499.60, 23% below where we wrote the AI Dividend piece, 25% below where we wrote the Patience Premium.

Two things need to be said before any analysis proceeds.

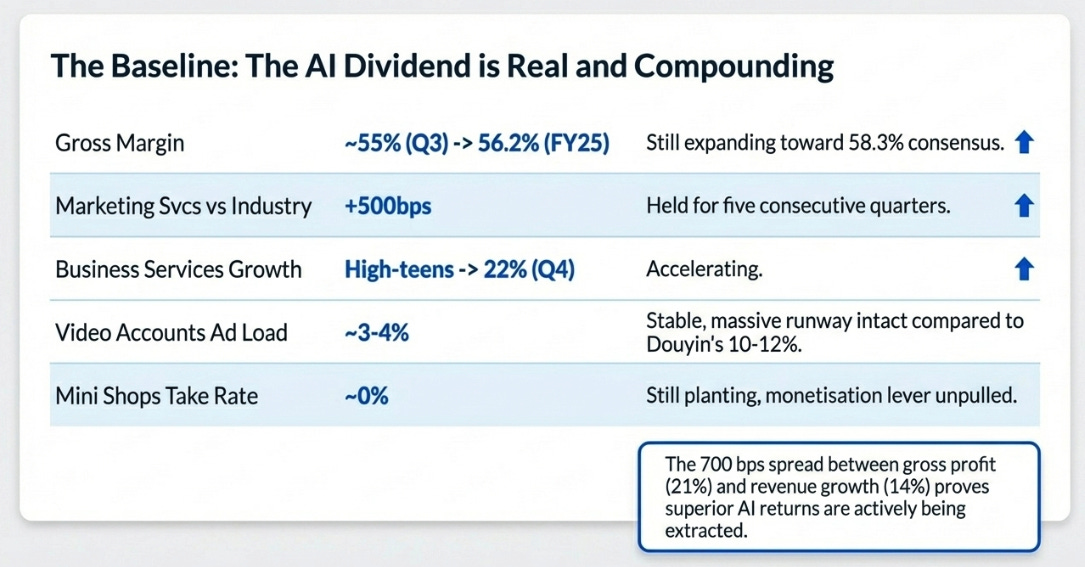

The business validated the thesis. Gross margins expanded to 56.2% for the full year. Marketing Services grew 19% against a 14% China industry benchmark. Business Services accelerated to 22% year-on-year in Q4. The AI dividend was real, structural, and compounding exactly as described.

The capital allocation thesis was wrong. We argued Tencent would extract AI value without entering the infrastructure cycle. They entered the infrastructure cycle. The question is whether that changes the investment case or deepens it.

Our answer: it deepens it. But only if you’re willing to update the framework honestly. Which is what this piece attempts.

What Held, The Dividend Is Real

Start with what the data actually shows, because the narrative around Q4 FY25 obscured something important: the operating results were excellent.

The “Patience Premium” piece argued Tencent had built monetisation levers it was deliberately not pulling. Video Accounts at 3–4% ad load versus Douyin’s 10–12%. Weixin Search below 10% of advertising revenue. Mini Shops take rates near zero. The argument was that these levers existed, were proven by competitors, and were controlled by management with a decade-long track record of patient execution.

Every one of them is still turning:

The AI Dividend piece called the 700 basis point spread between gross profit and revenue growth the financial signature of AI-powered monetisation working. FY2025 delivered 21% gross profit growth against 14% revenue growth. The spread held. The harvest the Patience Premium described, levers proven by competitors, controlled by management, available when needed, is proceeding exactly as argued.

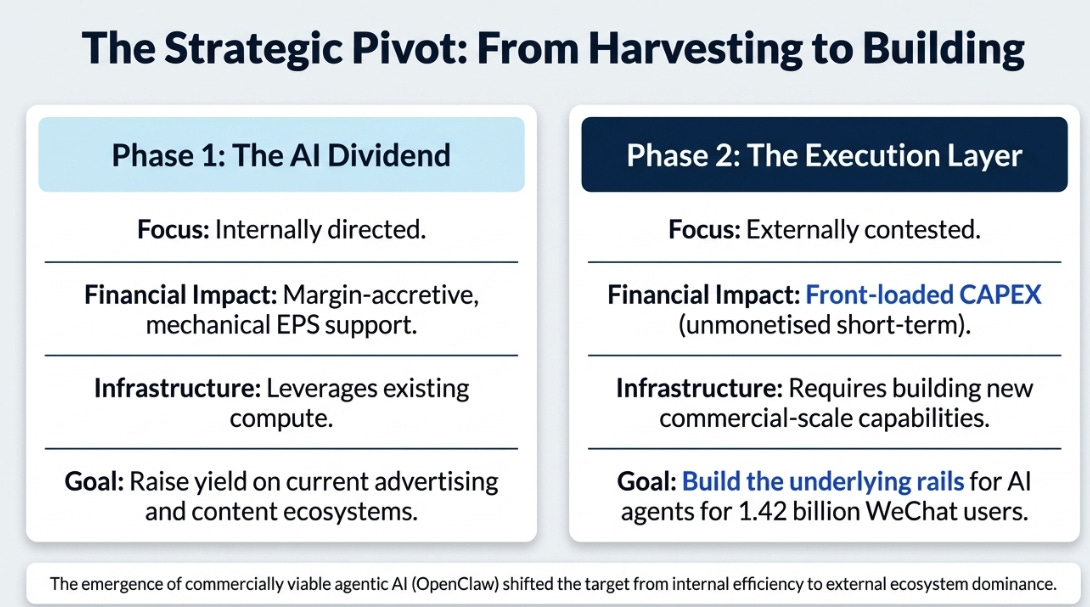

What changed is not the harvest. What changed is that Tencent decided not to wait for it.

What Changed, The Dividend Is Being Reinvested, Not Collected

Here is the sentence from the AI Dividend piece that requires the most honest revisiting:

“President Martin Lau made the strategic choice explicit: ‘We actually believe that there’s no insufficiency of GPUs for us at this moment for our internal use.’”

We cited that quote as evidence of strategic discipline, Tencent pointing AI investment inward at advertising and content rather than outward at low-margin infrastructure. Three months later, the same management team committed to more than doubling infrastructure investment. Both statements were true. What changed wasn’t the compute availability. It was the opportunity.

Between Q3 FY25 and Q4 FY25, OpenClaw emerged as a commercially viable agentic AI paradigm. The GPU sufficiency statement reflected Phase One reality, deploying AI within existing businesses to raise yield. The RMB 36 billion commitment reflects Phase Two ambition, building the execution layer for AI agents operating inside WeChat on behalf of 1.42 billion users.

These are not the same strategic decision. Phase One was internally directed, margin-accretive, and required no additional infrastructure beyond what Tencent already owned. Phase Two is externally contested, requires building capability that doesn’t yet exist at commercial scale, and demands capital investment before the return profile is visible.

Lau framed the distinction explicitly:

“We are breaking out our investment in new AI products because we view these strategic investments conceptually similar to investment in an affiliate or to CapEx. These are upfront investments required to build the necessary foundation to unlock new value as opposed to ongoing operating expenses.”

This is management asking investors to hold two equations simultaneously: Phase One returns already flowing through the P&L, and Phase Two costs front-loaded in 2026 with returns arriving later. The market’s 6.5% reaction was not irrational. When a company reduces mechanical EPS accretion while increasing spend on unmonetised products, the short-term earnings trajectory gets worse before it gets better. What the market got wrong was treating the investment as evidence of strategic weakness rather than strategic expansion.

The prior articles asked: how does AI make Tencent’s existing business more valuable? The correct question after Q4 FY25 is different: what is Tencent worth if WeChat becomes the execution layer for AI agents in China?

Those are not the same question. The first has a bounded answer, better margins, higher eCPM, more recurring gaming revenue. The second has a potentially unbounded answer. And the answer to the second question begins with this:

“We’re building AI agents which autonomously interact on behalf of users within Weixin functionalities, especially Mini Programs.”, Martin Lau

Read that sentence slowly. Not a chatbot. Not a search product. Agents that act, inside the surface where 1.42 billion people already conduct their digital lives, paying bills, messaging friends, discovering merchants, booking services. The agent doesn’t need to win a benchmark. It needs to be present when the user delegates a task. And the user’s tasks are already happening inside WeChat.

The product is not Yuanbao. The product is Weixin with AI in it.

What the Market Is Getting Wrong

The consensus view on Q4 FY25 can be summarised in one sentence: quality compounder, temporary AI investment headwind, buy on weakness, 12–18 month payoff as margins recover and buybacks resume.

This is probably right about the near-term stock trajectory. It is asking the wrong strategic question.

Lau was direct about why:

“We actually believe that AI chatbot applications are largely competing with search applications rather than with every other application.”

The market is valuing Tencent’s AI position by measuring Yuanbao’s user numbers against Doubao and Qwen. Lau is saying that’s not the contest. The chatbot category is a search substitute. The agent category is something different, and the agent category is where WeChat’s structural advantages are overwhelming rather than merely competitive.

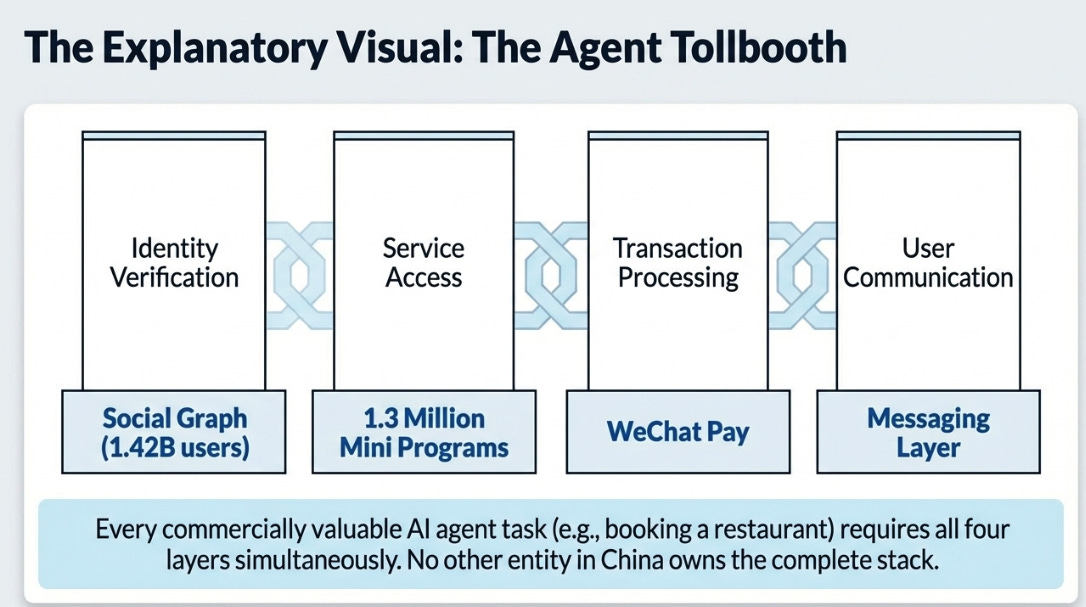

To understand why, consider what an AI agent actually needs to complete a real-world task. It needs to verify who it’s acting for. It needs to access the services the user wants. It needs to process payment. It needs to report back through a channel the user trusts and monitors. Four requirements. Every commercially valuable agent task needs all four simultaneously.

WeChat owns all four in a single surface. The social graph provides identity. 1.3 million Mini Programs provide service access. WeChat Pay processes the transaction. The messaging layer closes the loop. No other entity in China owns all four. Alibaba has payments and merchant access but not communication. ByteDance has attention but not trusted identity or full merchant integration.

This is the tollbooth. When an agent books a restaurant, whether built by Tencent, ByteDance, or a startup, it needs to authenticate the user, access the restaurant’s booking system, and process the payment. Three of those four requirements route through WeChat infrastructure. Tencent doesn’t need to build the best agent. It needs to own the rails the agents run on.

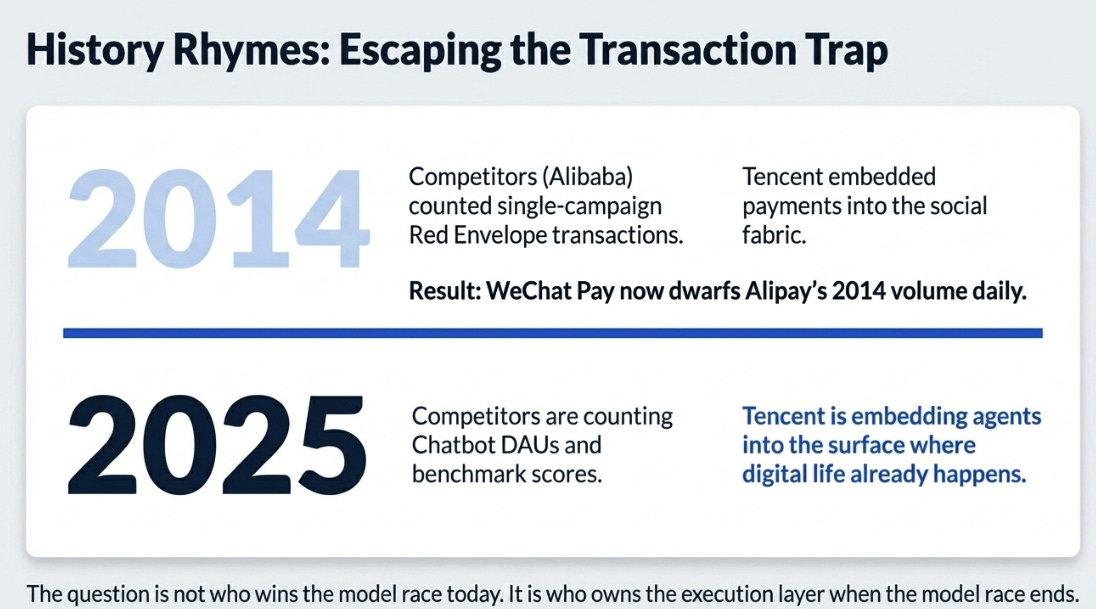

The Patience Premium piece made an analogy that becomes more precise here. In 2014, Alibaba counted red envelopes. Tencent counted relationships. Alibaba optimised for the transaction volume of a single campaign. Tencent embedded payments into the social fabric of the holiday itself. A decade later, WeChat Pay processes more daily transactions than Alipay managed in that entire campaign.

The same strategic moment is occurring one layer up. Competitors are counting chatbot DAUs. Tencent is embedding agents into the surface where Chinese digital life already happens. The question is not who wins the model race. It is who owns the execution layer when the model race is over.

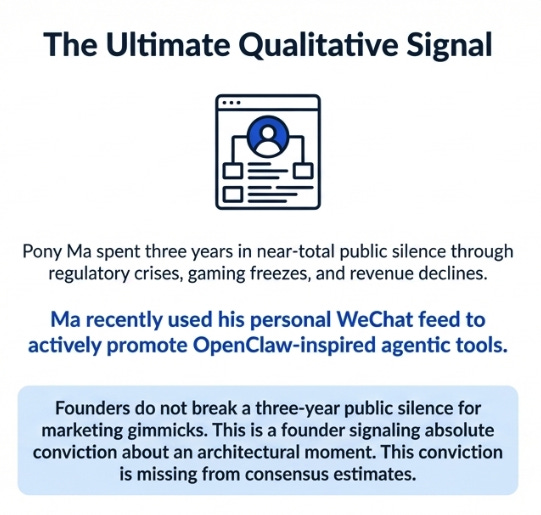

And then there is this, the most telling signal in the entire earnings package, reported almost as an aside by Bloomberg:

The normally publicity-shy Ma used his own WeChat feed to promote OpenClaw-inspired agentic tools.

Founders don’t go public about products they’re uncertain about. Pony Ma spent three years in near-total public silence through the regulatory crisis, the gaming licence freeze, the revenue decline. His re-emergence to personally promote agentic tools through his own social feed is not a marketing decision. It is a founder communicating conviction about an architectural moment. That conviction doesn’t appear in Bloomberg consensus estimates. It should.

Variant Perception and Three-Year Scenarios

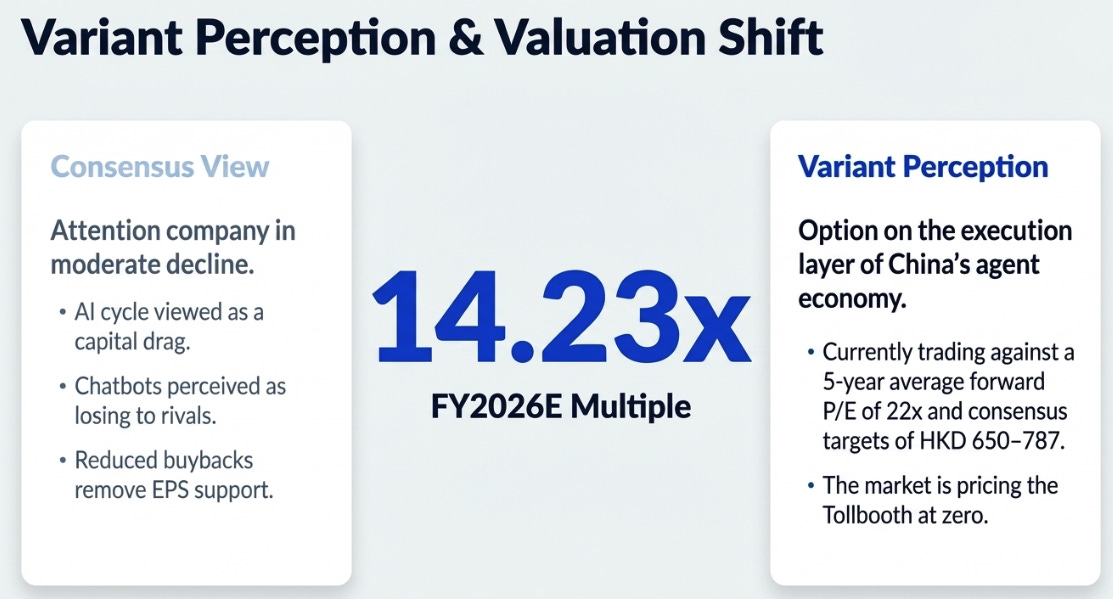

The Patience Premium framed Tencent as an option on Chinese consumer attention priced like the options had expired. At HKD 662, we argued the market was offering utility multiples for a company with social network monetisation potential.

The updated framing is both more precise and more ambitious. Tencent is an option on the execution layer of China’s agent economy, currently priced like an attention company in moderate decline.

At HKD 499.60, against a Bloomberg consensus price target range of HKD 650–787 and a five-year average forward P/E of approximately 22x, the 14.23x FY2026E multiple embeds a specific worldview: the AI investment cycle is a drag without a visible return path, the chatbot products are losing to better-funded competitors, and the buyback reduction removes the mechanical EPS support that justified premium pricing.

Each of those concerns is legitimate. None of them addresses the tollbooth.

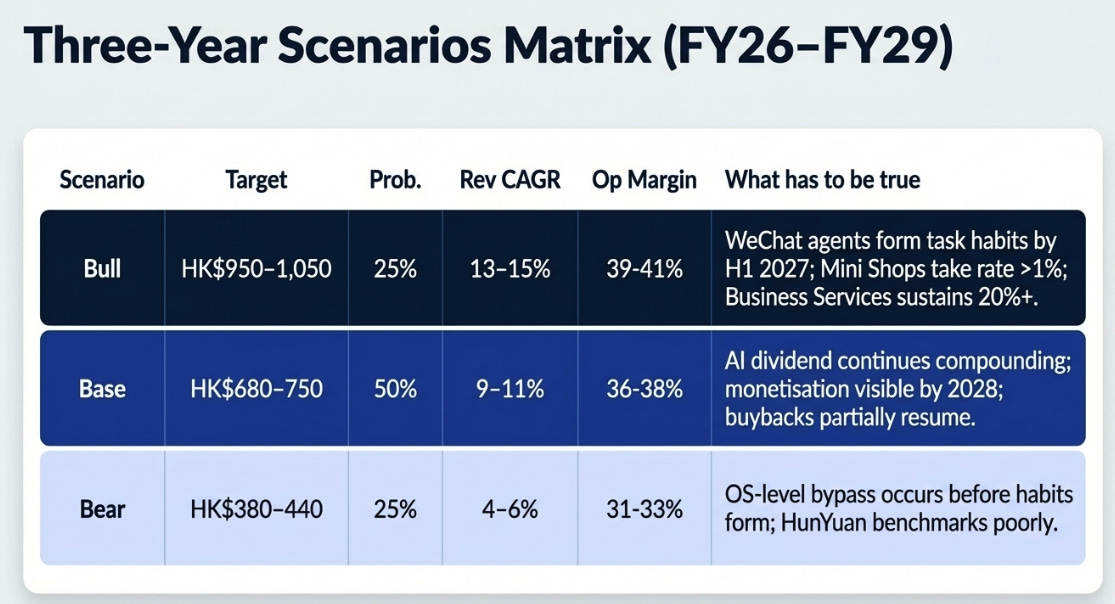

The prior articles’ price targets require honest revision given the capital allocation shift. The Patience Premium’s base case of HKD 859 is still achievable but the timeline extends, the Phase Two investment cycle pushes it toward FY2028 rather than FY2027. The AI Dividend’s 18-month target of HKD 1,100–1,150 was too aggressive on timing; that outcome, if it occurs, is a three-year view.

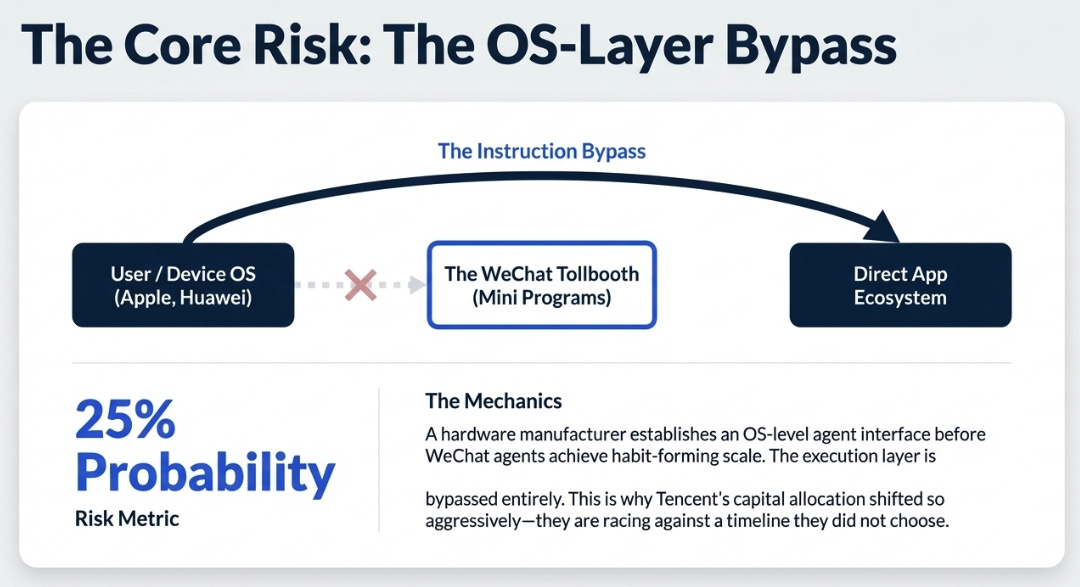

There is also one new bear case risk that didn’t exist when we wrote either prior piece: the OS-layer bypass. If a hardware manufacturer, Huawei, Apple, or a device maker not yet prominent, establishes an OS-level agent interface before WeChat agents reach habit-forming scale, the tollbooth is bypassed at the instruction layer. Users instruct the OS, which accesses apps directly without routing through WeChat’s Mini Programs ecosystem. The four-layer execution stack that makes WeChat’s position so strong becomes irrelevant if the agent never enters WeChat in the first place. This risk gets 25% probability, higher than anything in prior articles, because the capital allocation shift means Tencent is now racing against a timeline it didn’t choose.

One specific input worth noting: Lau made the clearest possible statement about why the subscription model, the primary AI monetisation path in the US, is unavailable in China:

“Unlike in the U.S. where you can actually get consumers to pay subscriptions... In China, those are not sort of that available.”

This is not a weakness in the Tencent thesis. It is the answer to why the execution layer thesis is the only viable AI business model at scale in China, and why Tencent’s specific asset combination is worth more than a 14x multiple implies. If subscriptions are off the table, the only path to AI monetisation is transaction economics. Transaction economics require the rails. Tencent owns the rails.

The Updated Dashboard

The Patience Premium tracked five metrics. Six now, one addition that didn’t exist as a concept when we wrote the prior pieces.

Gross margin trajectory. Above 57% = Phase One still compounding, mix shift structural. Below 55% = competitive pressure winning. Bloomberg consensus at 58.3% by FY2028 is the bull embedded in the fundamental model that the sentiment narrative ignores.

Marketing Services versus China ad industry. Above 400 basis points outperformance = AI yield enhancement intact. Below 200 basis points = the eCPM advantage is narrowing and the AI dividend thesis requires revision.

Business Services growth. Above 20% sustained = execution layer monetisation beginning to show in reported numbers. Below 15% = the Phase Two ramp is slower than the Tencent Cloud analogy implies, and the timeline for returns extends further.

Mini Shops disclosure. Any GMV number with a stated take rate above 1% = the harvest has begun. Continued silence = still planting. The Patience Premium’s best observation holds here: the silence is data. When management starts disclosing the number, the monetisation has started.

Management language on agents. Specific task completion metrics or agent usage data = product-market fit emerging from theory into practice. Continued product description without metrics = still in the discovery phase, which is not necessarily bad but extends the timeline for the scenario table above.

New, any metric Tencent introduces that didn’t exist in prior quarters. This is the most reliable leading indicator in the entire dashboard. Companies do not invent new disclosures for businesses that are struggling. The quarter management introduces agent task volume, closed-loop transaction share, or Mini Shops take rate is the quarter the transition from thesis to evidence becomes legible.

The Patience Premium ended with this: Some companies monetise because they must. Tencent monetises when they choose.

That framing still holds, but Q4 FY25 added a layer. Tencent chose to stop collecting the dividend and reinvest it instead. The question the next four quarters answer is whether that choice was disciplined capital allocation or a costly detour.

The evidence so far suggests the former. The business is stronger than the stock price implies. The structural position is more defensible than the chatbot narrative acknowledges. And a founder who spent three years publicly silent just promoted his company’s agentic tools on his personal feed.

That’s not nothing.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.