The Route Changes

Why backward-looking metrics fail during disruption, and how to tell whether a moat still matters

TL;DR:

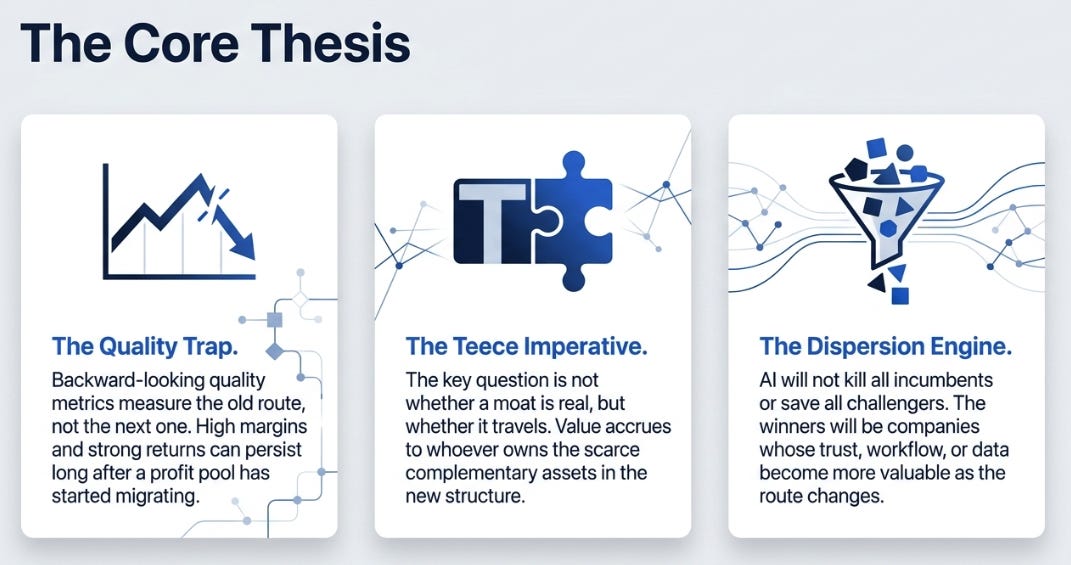

Backward-looking quality metrics measure the old route, not the next one. High margins, stable earnings, and strong returns can persist long after a profit pool has started migrating.

The key question in disruption is not whether a moat is real, but whether it travels. Teece’s insight matters: value accrues to whoever owns the scarce complementary assets needed in the new structure.

AI will not kill all incumbents or save all challengers; it will create dispersion. The winners will be companies whose trust, workflow ownership, data, distribution, or ecosystem become more valuable as the route changes.

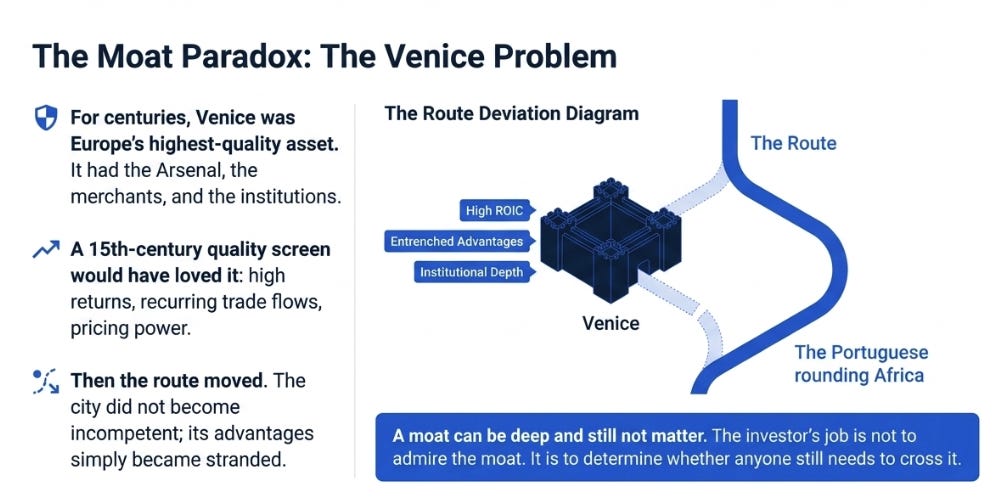

For centuries, Venice was the highest-quality asset in Europe.

It had the location, the fleet, the merchants, the institutions, the financing networks, and the Arsenal, perhaps the most advanced industrial operation of its time. More importantly, it had the route. Goods moving between East and West passed through the Adriatic, and Venice sat at the tollbooth. Its wealth was not simply a function of what it produced; it was a function of where it stood.

A fifteenth-century quality screen would have loved Venice. Durable competitive position, recurring trade flows, pricing power, institutional depth, high returns on capital, and centuries of proof. This was not a speculative asset. It was not a turnaround. It was the definition of proven quality.

Then the Portuguese rounded Africa.

Venice did not suddenly become incompetent. Its merchants did not forget how to trade. Its ships did not stop floating. Its institutions did not collapse overnight. The problem was simpler and more devastating: the route moved.

Once that happened, the very things that made Venice great became less relevant. The Arsenal could keep building ships. The bankers could keep financing commerce. The politicians could keep managing the republic. But the flow of value no longer needed to pass through the Adriatic. Venice’s quality had not disappeared. It had been stranded.

This is the central problem with quality investing during disruption. The spreadsheet measures the city. It does not tell you where the route is going.

The Missing Half of the Quality Trap

In my earlier piece, The Quality Trap, I argued that traditional quality screens are often museum catalogs. They identify the winners of the last era with remarkable precision, then mistake that precision for foresight.

The argument was straightforward. Companies with high returns on equity, stable earnings, low leverage, strong margins, and pricing power often look safest at precisely the moment their profit pools have begun to migrate. Newspapers in 2000 were wonderful businesses on paper. IBM in 2010 looked far cleaner than Microsoft. Legacy consumer brands had historical margins, distribution advantages, and brand equity that had compounded for decades. The numbers were not wrong. They were simply describing an economic structure that was already changing.

I still think that argument is right. But it was incomplete.

If every incumbent with great historical metrics is suspect when the route changes, then the conclusion is too blunt. Walmart survived Amazon. The New York Times survived digital media. Microsoft survived the transition from desktop software to cloud computing. In fact, Microsoft is the complication hiding inside my own argument: in 2010 it was itself a legacy incumbent, apparently past its prime, and yet it became one of the defining winners of the next era.

That means the real question cannot be “incumbent or challenger?” It cannot even be “quality or disruption?” Those are lazy oppositions. The harder question is this: when the route changes, which advantages travel?

Some moats become islands. They remain real, but the traffic leaves. Other moats become bridges. They allow a company to cross from one profit pool to the next.

The investor’s job is not to admire the moat. It is to determine whether anyone still needs to cross it.

Teece and the Theory of the Route

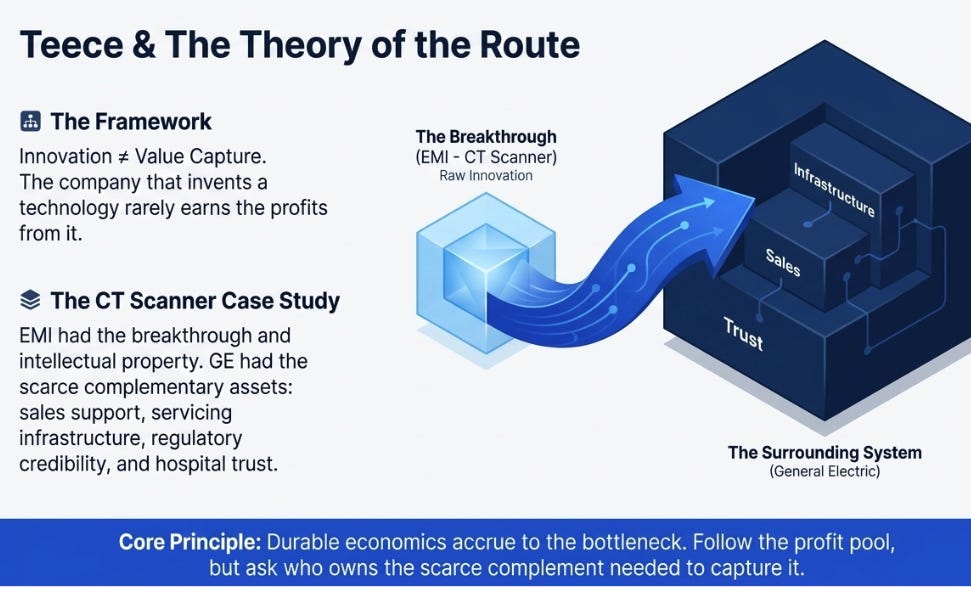

The cleanest way to understand this distinction was laid out by David Teece in his 1986 paper, Profiting from Technological Innovation.

Teece’s insight was simple, powerful, and still underappreciated: innovation and value capture are not the same thing. The company that invents a technology does not necessarily earn the profits from that technology. Those profits often accrue to whoever owns the complementary assets required to commercialize it.

The classic example is EMI and the CT scanner. EMI helped invent one of the most important medical technologies of the twentieth century. It had the breakthrough. It had the intellectual property. It had the technological lead.

What it lacked was the surrounding system. Hospitals did not just need a machine. They needed sales support, training, maintenance, procurement confidence, servicing infrastructure, regulatory credibility, and trust. General Electric had those assets. EMI had the invention; GE had the complements. The technology mattered, but the complement determined who got paid.

This is the intellectual foundation for thinking about quality during disruption. When a new technology appears, the exciting thing is rarely the only valuable thing. Often it is not even the most valuable thing. The durable economics accrue to the bottleneck around the technology: the asset that remains scarce after the innovation spreads.

This is why “follow the profit pool” is necessary but not sufficient. You also have to ask who owns the scarce complement needed to capture that profit pool.

Sometimes the complement belongs to the innovator. Sometimes it belongs to the incumbent. Sometimes it belongs to neither. The answer has little to do with who is old, who is new, who invented the technology, or who has the cleanest historical metrics. It has everything to do with who controls the bottleneck in the new structure.

This explains why Walmart survived and Borders did not. Both faced e-commerce. Borders had stores, inventory expertise, and a retail brand. Walmart had procurement scale, logistics infrastructure, supplier leverage, local presence, and physical nodes that could be integrated into an omnichannel model. In one case, the assets were stranded. In the other, they could travel.

It also explains why The New York Times diverged from most newspapers. The internet destroyed the local newspaper bundle, but it increased the value of trusted national brands. In a world of infinite content, scarcity moved from distribution to trust. The Times owned an asset that became more valuable after the route changed.

This is the refinement to the quality trap. The question is not whether the old moat was real. It usually was. The question is whether that moat controls a scarce complement in the new structure.

Why Traditional Metrics Invert

The Sparkline piece on AI disruption is valuable because it gives empirical scaffolding to what otherwise sounds like a collection of anecdotes. (https://www.sparklinecapital.com/post/ai-disruption)

Its core finding is simple and important: traditional value metrics work reasonably well in insulated industries, but struggle badly in industries exposed to technological disruption. That should not be surprising, but it is still underappreciated. In stable industries, low multiples often reflect mispricing. In disrupted industries, low multiples often reflect the market recognizing that current earnings are not durable.

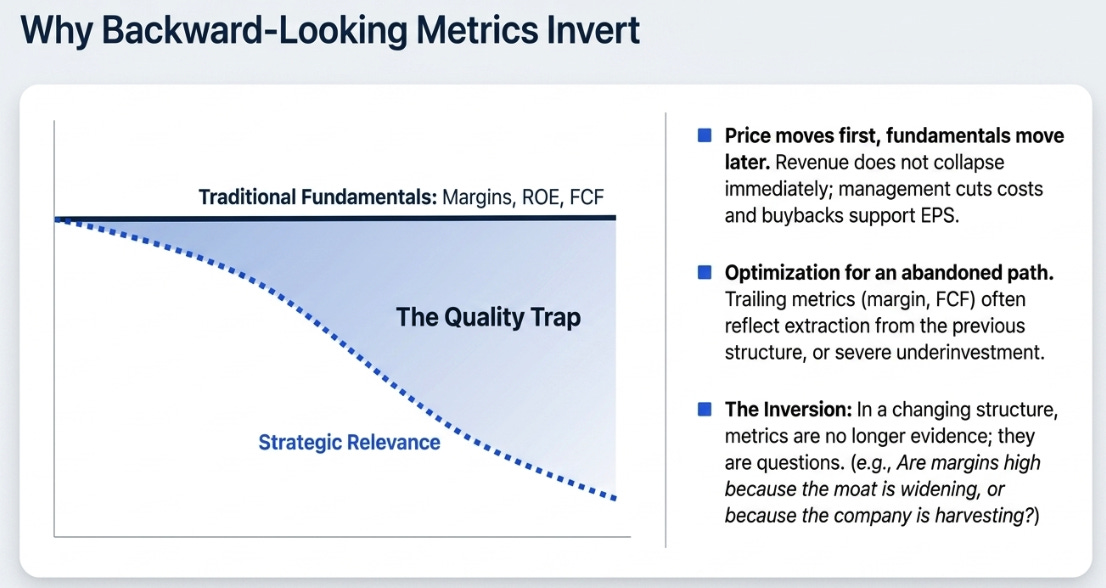

The mechanism is brutal. Price moves first. Fundamentals move later.

A company facing disruption can look cheap for years. Revenue does not collapse immediately. Customers take time to leave. Contracts roll off slowly. Management cuts costs. Buybacks support earnings per share. Margins can hold up even as the strategic position deteriorates. The multiple compresses against earnings that still look real. That is the value trap.

But the same logic applies to quality.

A quality trap happens when the metrics remain beautiful because the old route has not fully decayed. Return on equity, operating margin, free cash flow, and earnings stability are all lagging indicators. They are evidence of what the company has been able to extract from the previous structure. They are not, by themselves, evidence that the next structure will require the same company.

This is why backward-looking metrics do not merely fail during disruption; they can invert. They select for the companies that look best under the old regime. But in a route change, the best-looking old-regime companies may be the most exposed. They are optimized for a path customers are abandoning.

That does not mean traditional quality is useless. It means its usefulness is conditional. In a stable structure, quality metrics are evidence. In a changing structure, they are questions.

Why are margins high? Because the company has a durable advantage, or because it is underinvesting? Why is free cash flow strong? Because the business compounds internally, or because management has no better use for capital? Why is leverage low? Because the company is disciplined, or because it is harvesting? Why are returns on capital high? Because the moat is widening, or because the denominator is being starved?

The same number can mean opposite things depending on whether the route is stable or moving.

Sparkline’s “intangible value” framework is interesting for precisely this reason. I would not treat it as a magic formula; any proprietary backtest deserves skepticism. But the direction is right. It attempts to measure the assets that Teece would have told us to look for: intellectual property, brand, human capital, and network effects. In other words, it tries to identify the complements that traditional accounting either misses, expenses, or misclassifies.

That is the real lesson. The answer to disruption is not to abandon valuation or quality. It is to redefine what must be valued.

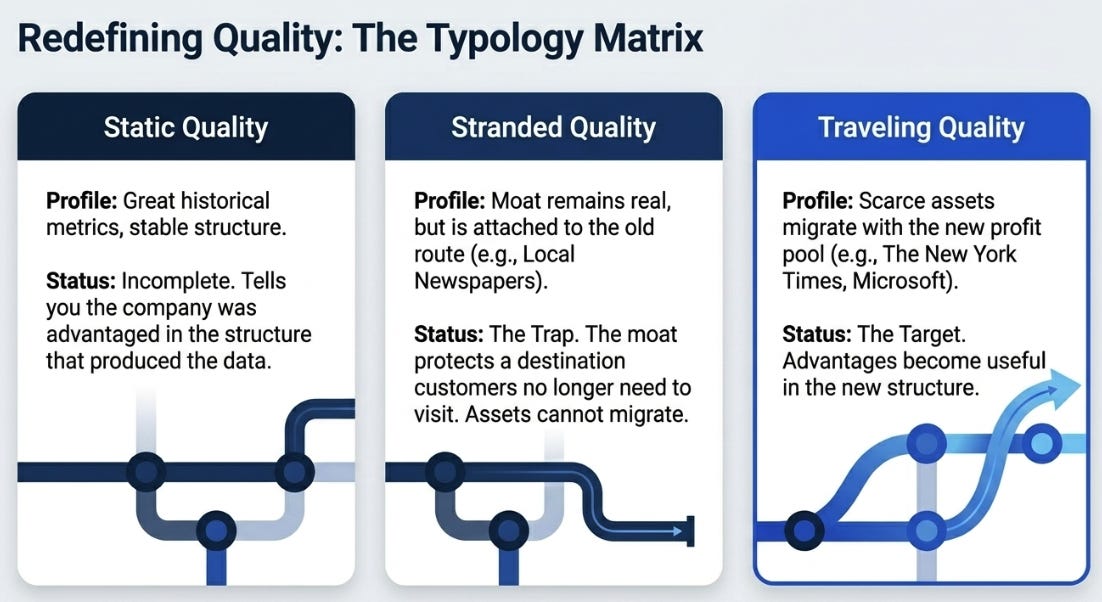

Static, Stranded, and Traveling Quality

There are three kinds of quality during disruption.

Static quality is the easiest to identify. The business has great historical metrics. It screens well. It has high margins, stable earnings, low leverage, and a long record of profitability. Static quality is not fake; it is simply incomplete. It tells you the company was advantaged in the structure that produced the data.

Stranded quality is more dangerous. This is the business whose moat remains real but is attached to the old route. The company may still have brand, scale, distribution, assets, and customer relationships. The problem is that the customer’s route to value is changing in a way that makes those assets less central. The moat protects something, but not the bottleneck.

Traveling quality is what investors should be looking for. These are companies whose advantages become useful in the new structure. They may be incumbents or challengers. They may screen well or badly. The defining feature is that their scarce assets migrate with the profit pool.

This framework is more useful than the standard debate between quality and growth. Growth investors can overpay for companies that have the technology but not the complement. Quality investors can overpay for companies that have the complement to an old world. Value investors can buy optically cheap companies whose earnings are about to be structurally impaired.

The right question is more specific: what remains scarce after the technology spreads?

If the answer is “nothing the company owns,” the moat is stranded. If the answer is “the company’s trust, data, distribution, workflow, regulatory position, ecosystem, or implementation capability,” the moat may travel.

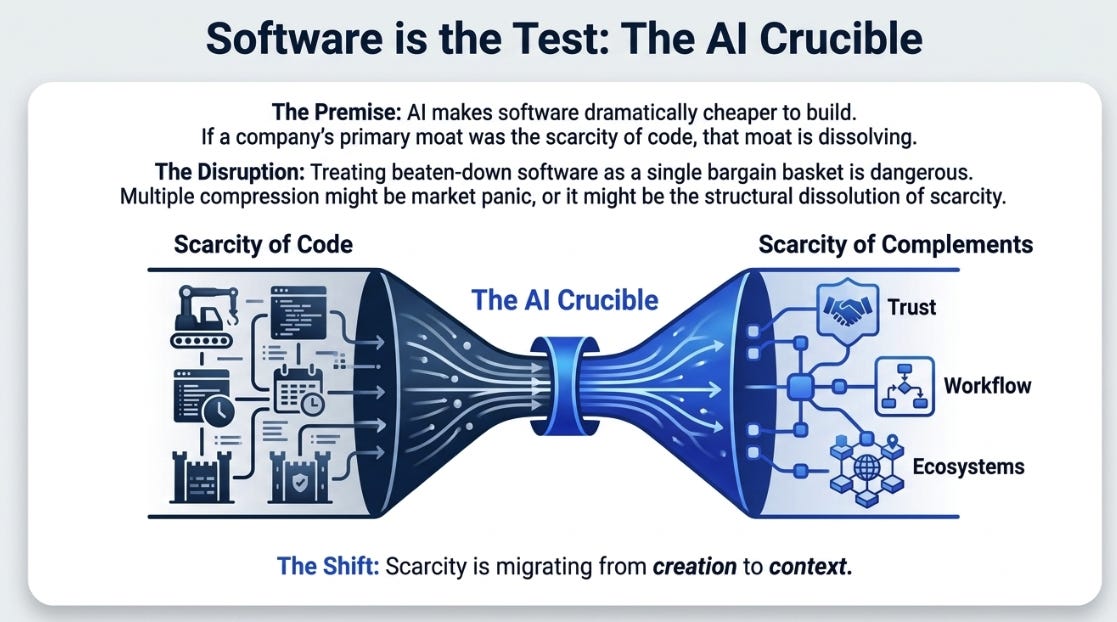

Software Is the Test

The software selloff is the cleanest current test of this framework.

The market’s fear is understandable. If AI makes software dramatically cheaper to build, then the economics of software must be re-examined. A product that once required large engineering teams may be built by a smaller team with AI assistance. Features that took quarters to develop may take weeks. Internal tools that companies previously bought may become easier to generate. The scarcity of code is falling.

If code was the moat, this is a problem.

This is why treating beaten-down software as a single bargain basket is dangerous. Some software companies are cheap because the market is panicking. Others are cheap because their business model depended on a scarcity that AI is dissolving.

The distinction is not obvious from the multiple. A software company trading at a low forward earnings multiple may be a bargain or a trap. The question is what the customer was really paying for.

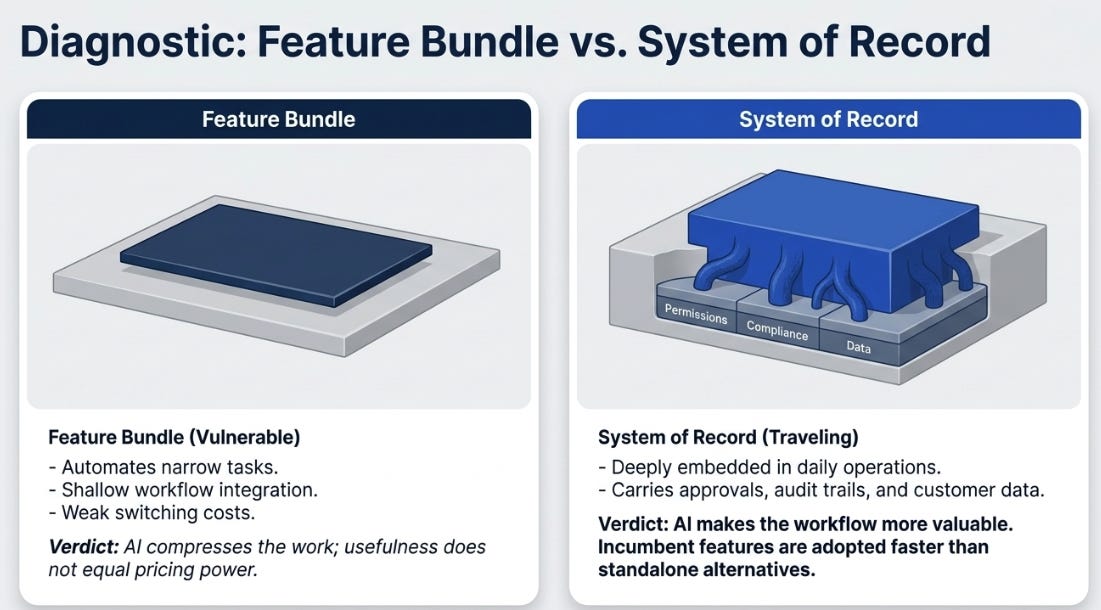

Some software is vulnerable because it is a feature bundle. It automates a narrow task, has shallow workflow integration, limited proprietary data, weak switching costs, and pricing linked to work AI can now compress. These products may still be useful, but usefulness is not the same as pricing power. If AI makes alternatives easier to build, the product becomes less scarce.

Other software is different. It is a system of record. It sits inside a company’s daily operations. It carries permissions, history, approvals, audit trails, integrations, reporting, compliance, customer data, and employee training. The software is not merely a tool; it is a place where work happens.

For these companies, AI may be disruptive, but not necessarily destructive. If the vendor owns the workflow, AI can make the workflow more valuable. If the vendor owns the data context, AI can make that context more useful. If the vendor has trust in a regulated or mission-critical environment, AI can increase the premium on reliability. If the product is deeply integrated, AI features from the incumbent may be adopted faster than standalone alternatives.

This is the Teece question applied to software: if AI makes code abundant, what is the scarce complement?

For some companies, there may not be one. For others, the answer may be workflow ownership, proprietary data, compliance, trust, implementation capability, ecosystem depth, or customer context.

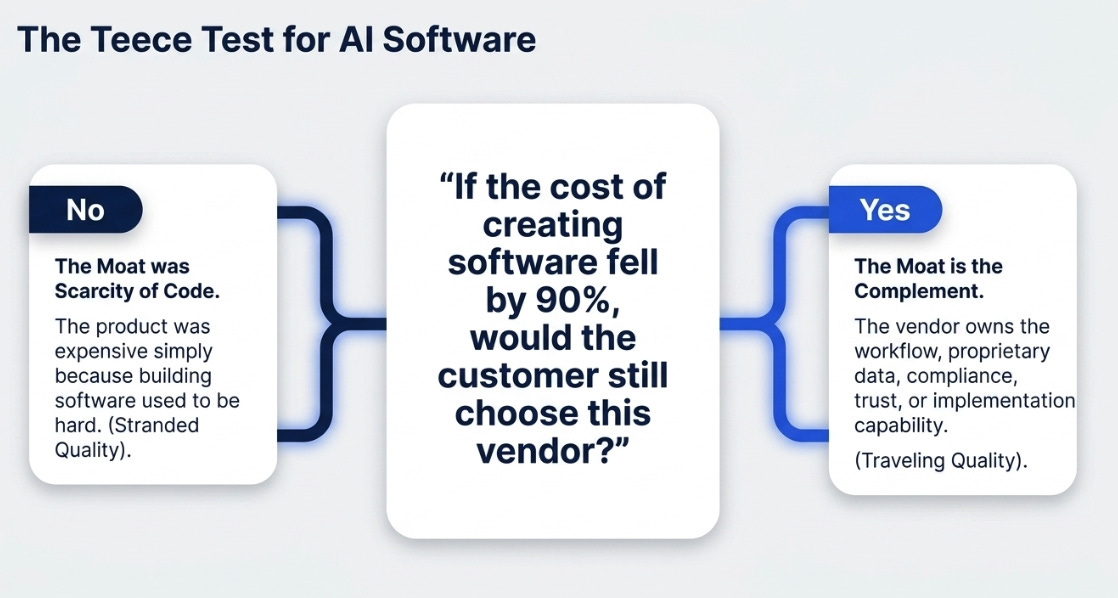

This leads to a practical test: if the cost of creating software fell by 90%, would the customer still choose this vendor?

If the answer is no, the moat was probably software scarcity. If the answer is yes, the moat is somewhere else.

That is why AI may create enormous dispersion within software. It will compress some companies and strengthen others. It will reveal which products were merely expensive because building software used to be hard, and which products were expensive because they occupied scarce positions inside customer operations.

The market’s first reaction is to sell the category. The investor’s job is to sort the category.

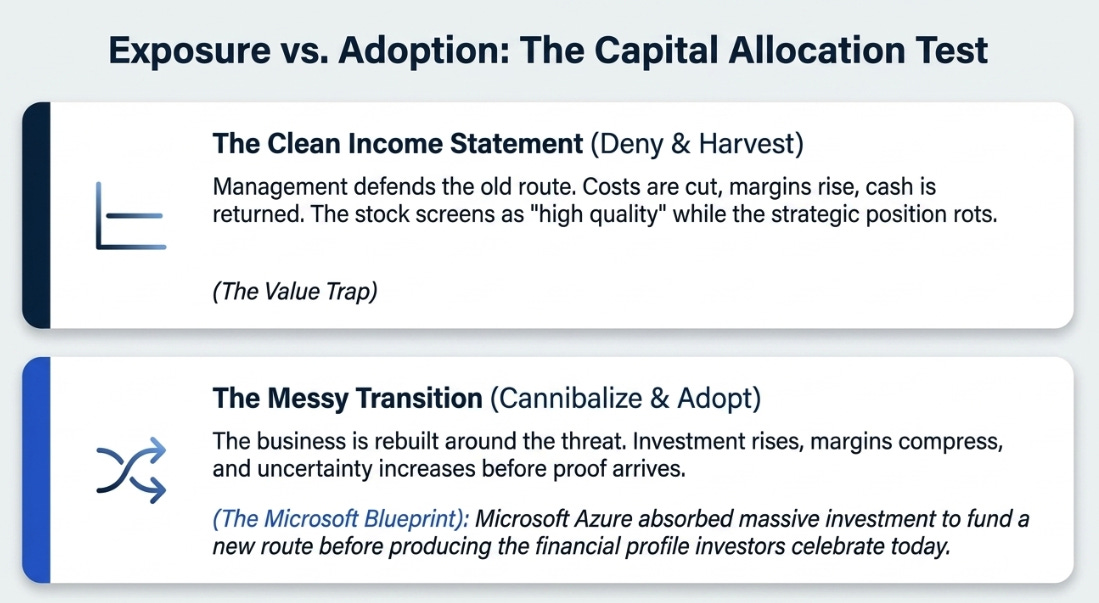

Adoption Versus Exposure

One of the more interesting points in Sparkline’s work is that software is not merely exposed to AI. It is also adopting AI aggressively.

That distinction matters. Exposure tells you where the threat is. Adoption tells you who is responding.

A company facing disruption has three choices. It can deny the shift, harvest the old model, or cannibalize itself. The third path is the only one that produces traveling quality, but it is also the hardest to recognize in traditional financial statements. It often depresses margins, increases expenses, and creates uncertainty before it creates proof.

This is why capital allocation matters more than commentary. Every management team says it is embracing AI. The question is whether the business is being rebuilt around it. Where is the company hiring? What is being integrated into the core product? Is AI a feature, a pricing lever, or a restructuring of the workflow? Is the company willing to weaken a legacy revenue pool to strengthen its position in the new one?

Microsoft’s cloud transition worked because it was not a press release. It was capital allocation. Azure absorbed investment before it produced the financial profile investors later celebrated. The old company funded the new route.

That is the pattern to look for today. The winners in software will not be the companies that mention AI the most. They will be the companies whose existing complements, data, workflow, trust, distribution, developer ecosystems, customer relationships, make their AI adoption more valuable than a competitor’s demo.

The losers will not necessarily be the companies that lack AI. Some will have AI features. Some will have impressive demos. The issue will be that their complements are weak. They will have product but not position.

Where the Route Goes

Venice’s tragedy was not incompetence. That is what makes the story useful. The city did not fail because it forgot how to be Venice. It failed because being Venice mattered less once the route changed.

That is the risk in every quality portfolio today. The businesses may be well managed. The margins may be real. The returns may be high. The balance sheets may be clean. The moats may even be deep.

But if the route is moving, the key question is not how good the city looks. The question is whether the route still runs through it.

That is the refinement to the quality trap. Backward-looking metrics fail because they measure the quality of the old route. The investor’s job is to determine whether the company’s moat is stranded on that route or whether it owns the scarce complement required on the new one.

Some companies will be Venice: excellent, historic, and bypassed. Some will be Walmart: attacked by the new route but able to bend its assets toward it. Some will be Microsoft: written off as a legacy incumbent while quietly owning the relationships, talent, and infrastructure needed for the next platform shift. Some will be EMI: inventors of the future without the complements needed to profit from it.

AI will create all four.

It will create companies with breathtaking technology and weak value capture. It will create incumbents with beautiful financials and stranded moats. It will create apparent bargains whose earnings have not yet caught down to reality. It will also create survivors whose old advantages become more valuable when carried into the new structure.

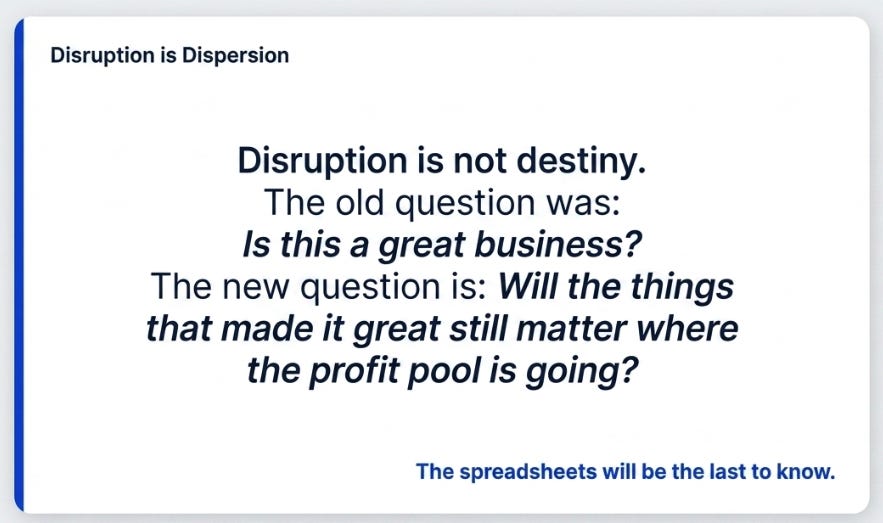

The old quality question was: is this a great business?

The better question is: will the things that made it great still matter where the profit pool is going?

That is the difference between static quality and traveling quality. Static quality tells you the city was rich. Traveling quality tells you the route still passes through it.

The spreadsheets will be the last to know.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.