Toast 1Q26 Earnings: The Register, the Moat, and the Manager

Toast’s quarter looked like another guidance disappointment. Underneath, the company is testing whether its restaurant operating system can become an agentic labor layer, just as DoorDash reminds inve

TL;DR

Toast is no longer just trying to be the system restaurants use; it is trying to be the system that does the work restaurants used to outsource.

The quarter strengthened the long-term thesis; higher monetization, strong ARR growth, Toast IQ usage, and early Toast IQ Grow ROI, but weakened near-term confidence because guidance did not flow through cleanly.

The next test is not revenue growth; it is whether Toast can monetize outcomes: higher take rate, paid AI attach, stable GPV/location, contained credit losses, and a credible direct-demand loop through Toast Local.

The Thesis Held; the Stock Didn’t

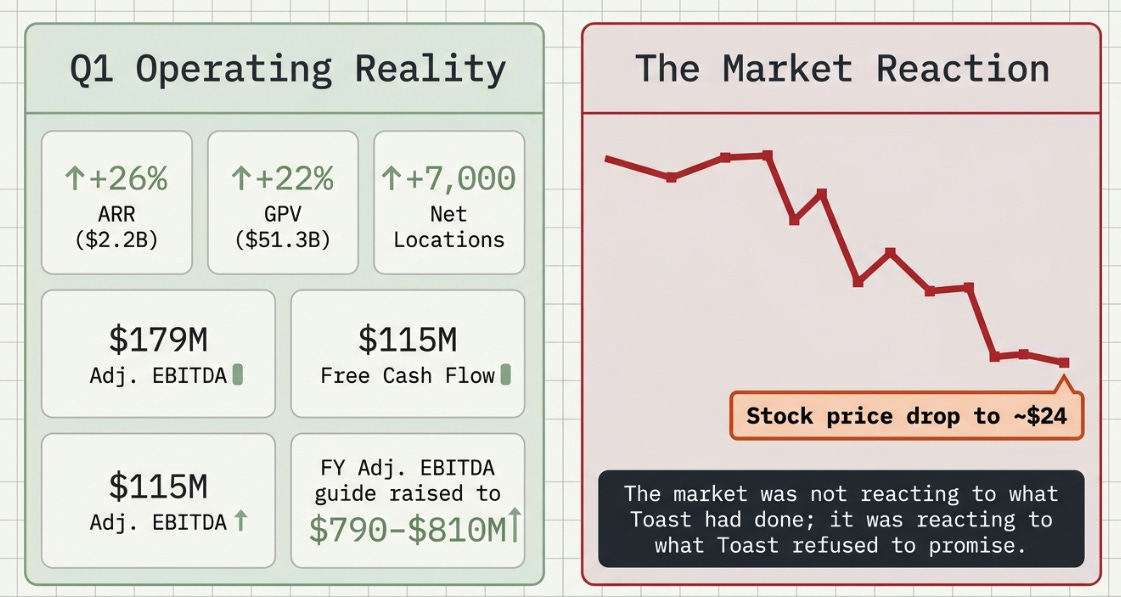

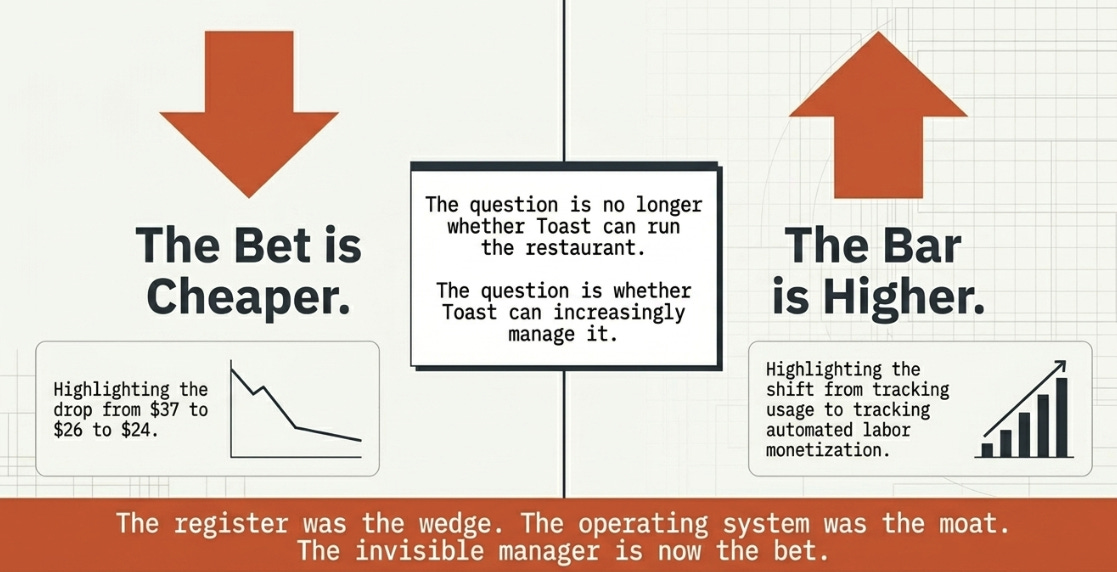

In November, we wrote about Toast at roughly $37 as the restaurant integration layer. In February, we wrote again around $26, arguing that the market was confusing chosen reinvestment with structural margin pressure. Today the stock is closer to $24, and before asking readers to follow the thesis a third time, the honest place to start is with the gap.

The business did many of the things we wanted. The stock did not.

That deserves an accounting.

Toast grew ARR 26% to $2.2 billion, added roughly 7,000 net locations, grew GPV 22% to $51.3 billion, delivered $179 million of adjusted EBITDA, generated $115 million of free cash flow, and raised full-year adjusted EBITDA guidance to $790–810 million. The headline operating metrics were not weak.

And yet the stock sold off because the quarter did not answer the question investors wanted answered: will Toast let upside fall to the bottom line? Q1 adjusted EBITDA beat consensus, but Q2 guidance came in below Street expectations, and the full-year raise largely reflected the Q1 beat rather than a meaningfully higher second-half trajectory. The market was not reacting to what Toast had done; it was reacting to what Toast refused to promise.

That was the same tension as last quarter, but with a more important twist. The prior debate was whether Toast’s margin pause reflected investment or deterioration. This quarter showed something more interesting: Toast is no longer merely reinvesting the profit sanctuary into new markets. It is trying to use AI to turn its restaurant operating system into something closer to restaurant labor.

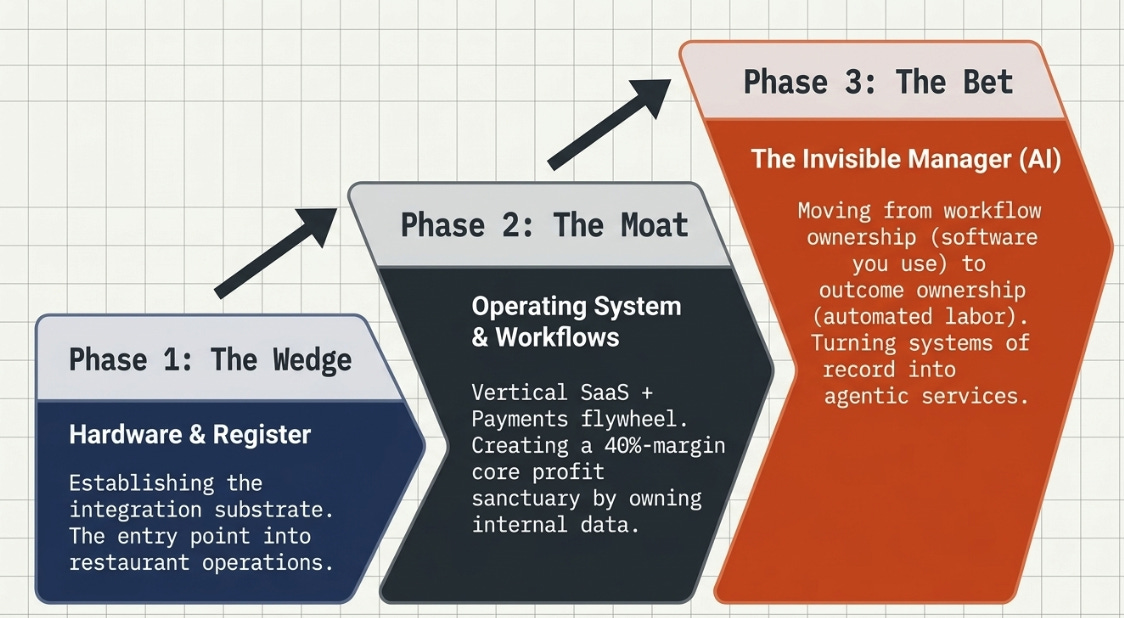

The register was the wedge. The operating system was the moat. The invisible manager is now the bet.

The Quarter Had Two Stories, and the Market Priced the Worse One

From Software You Use to Work You No Longer Do

The fundamental question for Toast is no longer whether restaurants will adopt cloud POS. They have. Nor is it whether Toast can be profitable. It is. The question is whether Toast can convert workflow ownership into outcome ownership.

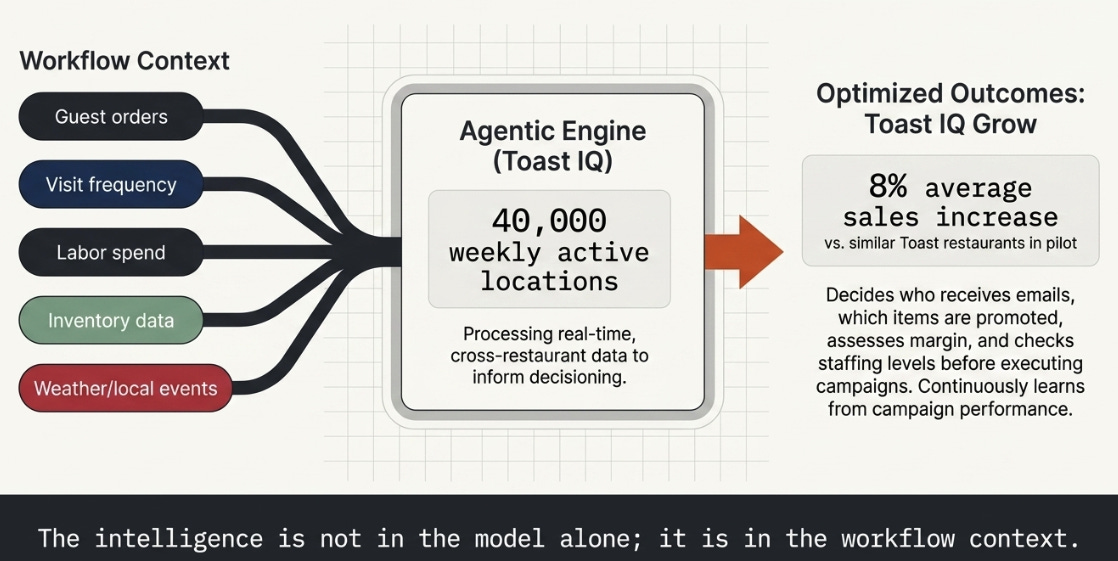

Toast’s management said this directly. Aman Narang described Toast’s evolution from point-of-sale into a system of record, then laid out the next step: Toast has “always provided the software,” but with AI it can now “provide the service that can actually do the work” for operators across marketing, bookkeeping, payroll, tax, and other non-core functions. The reason this matters is that the data required for those functions, guest orders, visit frequency, labor spend, inventory spend, business performance, already lives inside Toast and becomes more valuable with every new location and transaction.

That is the bull half of the quarter. Toast IQ now has 40,000 weekly active locations. Toast IQ Grow, the first agentic product, builds and optimizes campaigns from a restaurant’s past performance data, sales forecast, and eventually weather and local events. Management said pilot customers saw an average 8% sales increase versus similar Toast restaurants.

This is not just an AI feature. A standalone marketing tool can write an email. Toast can decide which guest should receive it, which menu item should be promoted, what margin that item carries, whether the restaurant can staff the incremental demand, and whether similar restaurants saw the same pattern. The intelligence is not in the model alone; it is in the workflow context.

DoorDash Is Not a POS Problem; It Is a Demand Problem

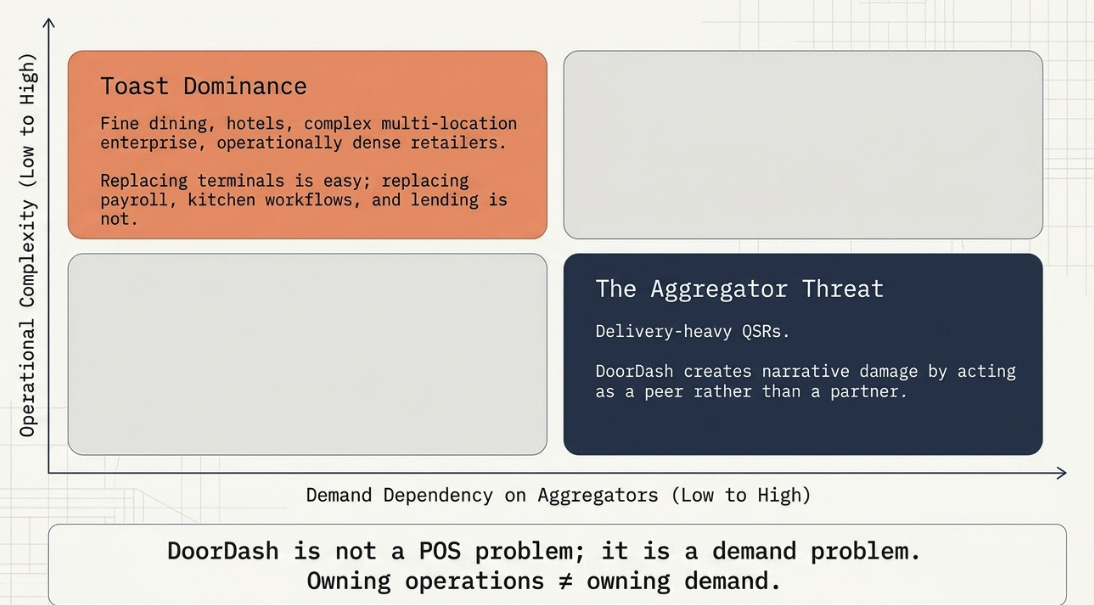

The bear half of the quarter arrived from the other direction. During Q&A, Rothschild’s Dominic Ball asked directly about DoorDash POS activity in San Francisco, Phoenix, and New York, and whether DoorDash was moving from partner to peer. That is the right strategic question. Toast may own the operating layer, but DoorDash and Uber own large parts of the demand layer.

These are not the same games. Toast’s integration layer is hard to displace in full-service restaurants, hotels, fine dining, complex multi-location enterprise, and operationally dense retailers. Replacing the terminal is easy; replacing payments, payroll, inventory, kitchen workflows, scheduling, lending, marketing, and now an agent layer is not. But in delivery-heavy QSR, where operational complexity is lower and demand dependency on aggregators is higher, the moat is thinner. DoorDash does not need to replace Toast everywhere to matter. It only needs to create enough narrative damage in enough high-volume categories to compress the multiple.

That is what happened this quarter: the agent thesis got more real, and the aggregator threat got more visible. The market priced the second faster than the first.

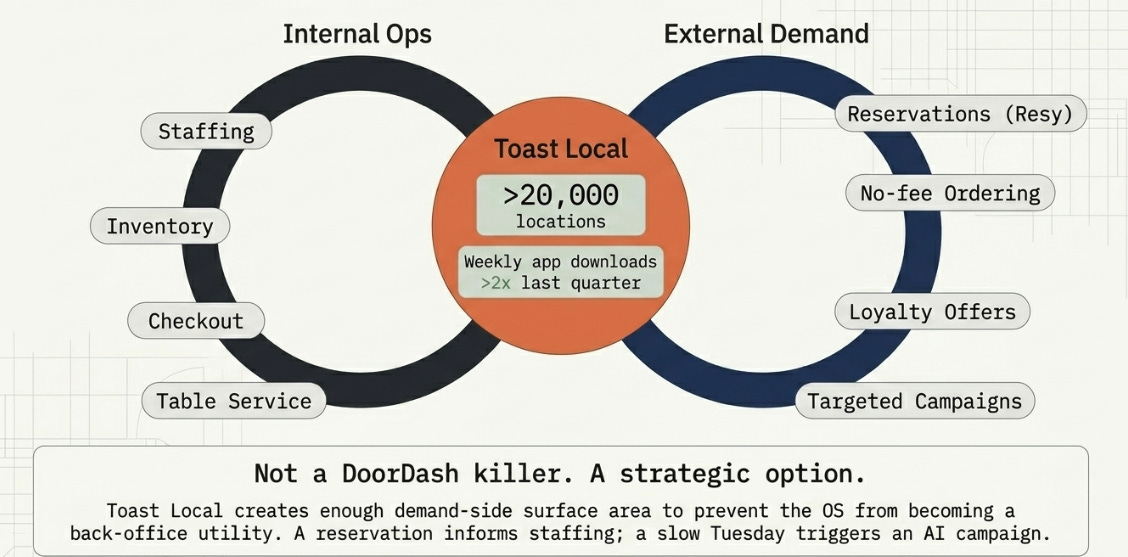

Toast Local Is the Countermove, Not the Answer Yet

Toast Local is the piece that both bulls and bears need to take more seriously.

Management framed Toast Local as a low- or no-commission channel for restaurants to generate demand, with no-fee ordering, loyalty rewards, targeted offers, and reservations through Resy and Toast Tables at more than 20,000 locations. Weekly app downloads more than doubled last quarter.

This is not a DoorDash killer. That is the wrong test. DoorDash is a consumer habit; Toast Local is still a strategic option. The better question is whether Toast can create enough demand-side surface area to prevent the operating system from becoming a back-office utility while aggregators own the guest relationship.

The old Toast thesis was internal: own the workflows. The new Toast thesis is both internal and external: own enough of the workflow and enough of the guest loop that the data compounds in both directions. A reservation can inform staffing. A loyalty offer can inform inventory. A payment credential can make checkout invisible. A guest history can make table service more personal. A slow Tuesday can trigger an agent-created campaign.

That is the point. Toast Local does not need to become DoorDash. It needs to connect demand to operations in a way DoorDash cannot, because DoorDash does not run the restaurant.

The Old Variant Perception Was Payments; the New One Is Management

Our prior view was that Toast was misclassified. The market saw payments-heavy revenue and valued the company like a payments processor with software attached. We argued the opposite: Toast is a restaurant operating system with payments as the monetization rail. That view still holds. The prior articles emphasized the vertical SaaS + payments flywheel, the integration substrate, the 40%-margin core profit sanctuary, and the decision to reinvest rather than harvest.

What changed is the nature of the upside.

The old variant perception was: Toast is not payments; it is restaurant infrastructure.

The updated variant perception is: Toast is not just infrastructure; it is trying to become the invisible manager.

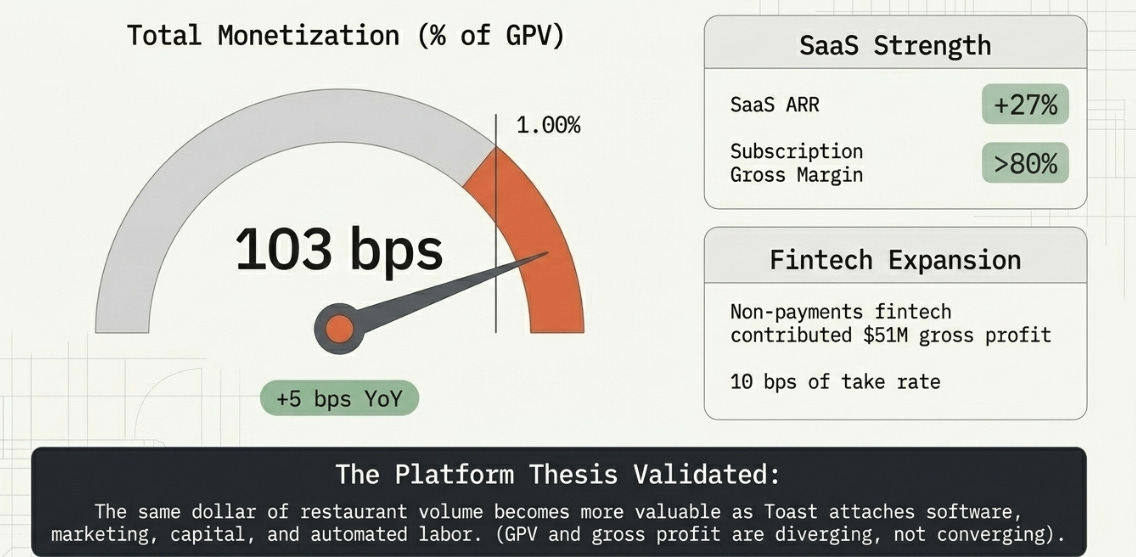

That is a more ambitious thesis, but also a more falsifiable one. AI usage is no longer enough. Toast has to show that restaurants will pay for work performed, not merely software provided. If Toast IQ Grow drives an 8% sales lift but Toast cannot capture meaningful economics, the product may be great for retention but not transformative for valuation. If it can charge for outcome-oriented work across marketing, payroll, bookkeeping, inventory, scheduling, and demand generation, then total monetization as a percentage of GPV should rise for years.

That metric is already moving. Total monetization across SaaS and fintech crossed 1% of GPV for the first time, reaching 103 bps, up 5 bps year over year. SaaS ARR grew 27%, subscription gross margin exceeded 80%, and non-payments fintech contributed $51 million of gross profit and 10 bps of take rate.

If Toast were merely a processor, GPV and gross profit growth would eventually converge. The platform thesis requires the opposite: the same dollar of restaurant volume becomes more valuable as Toast attaches more software, fintech, marketing, capital, and automated labor to it.

Why the Stock Fell Anyway

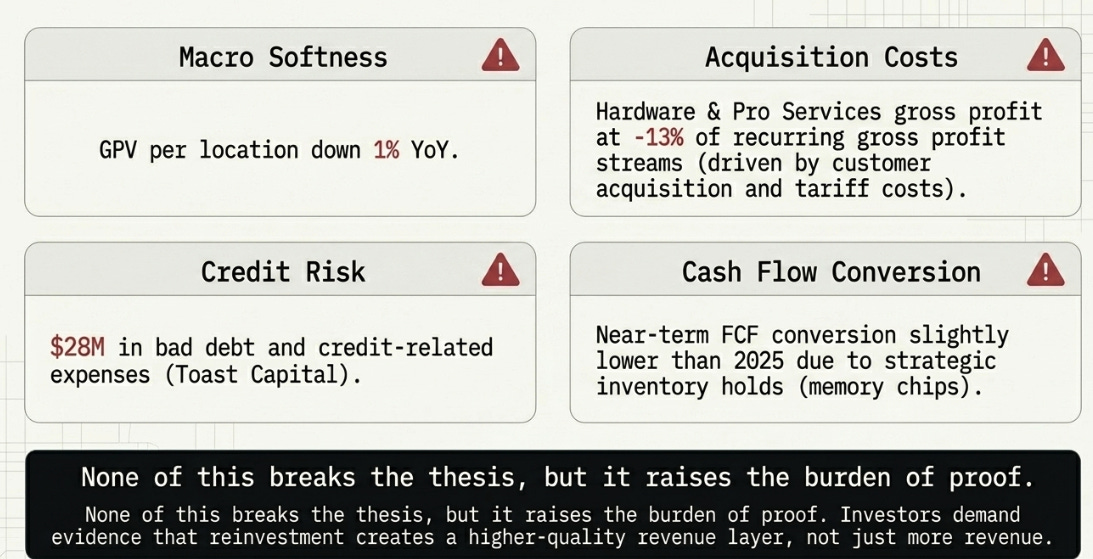

The market’s frustration is not irrational.

GPV per location declined 1% year over year. Hardware and professional services gross profit was negative 13% of recurring gross profit streams as Toast leaned into customer acquisition and absorbed tariff costs. Bad debt and credit-related expenses were $28 million. Management also said free cash flow conversion will be slightly lower than 2025 because it is strategically buying memory chips and holding more inventory near term.

None of this breaks the thesis. It does raise the proof burden.

Toast is asking investors to underwrite several things at once: continued core share gains, enterprise execution, international and retail expansion, hardware drag normalization, Toast Capital credit discipline, and now AI monetization. That is a lot to ask in a market that has turned hostile toward software stories without near-term flow-through.

The right critique is not “Toast missed the quarter.” It did not. The right critique is: Toast needs to prove that reinvestment creates a higher-quality revenue layer, not just more revenue.

Three Futures for the Invisible Manager

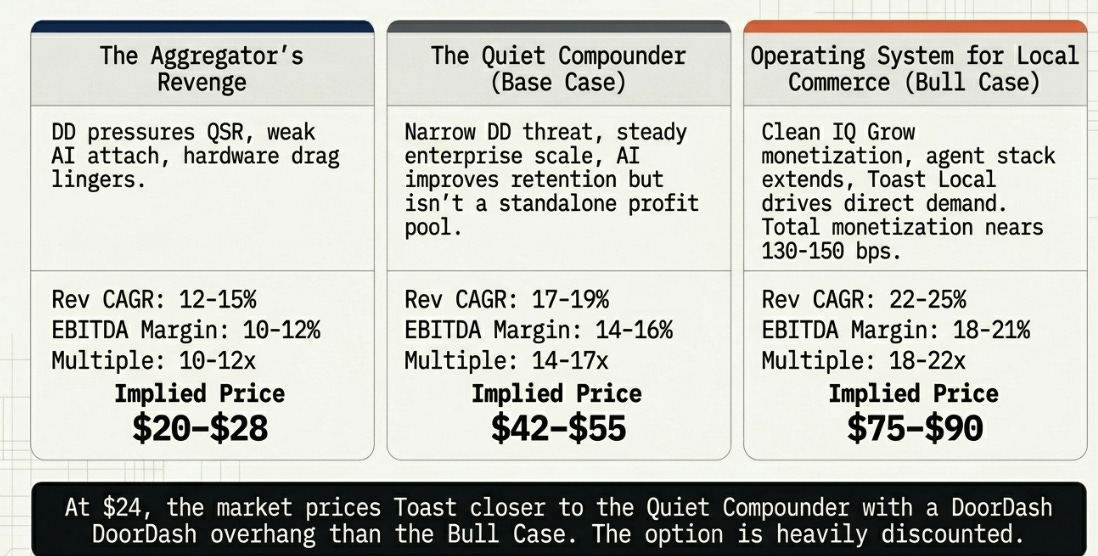

The scenario math is less important than the strategic world each scenario implies, but discipline still matters. Starting from roughly $24, and using the Bloomberg path you shared, FY26 revenue around $7.4 billion, FY28 revenue around $10.2 billion, FY28 EBITDA around $1.35 billion, the three-year outcomes look like this.

The Aggregator’s Revenge. DoorDash and other demand aggregators pressure delivery-heavy QSR, Toast IQ Grow sees usage but weak paid attach, GPV per location stays soft, credit losses rise, and hardware drag lingers. Toast remains a good vertical POS/payments company, but not a re-rated platform. Revenue compounds roughly 12–15%, EBITDA margins stall around 10–12%, and the stock trades at 10–12x EBITDA. That yields roughly $20–28 three years out. The buyback and balance sheet help, but the multiple stays capped.

The Quiet Compounder. DoorDash proves to be a narrow threat, not a platform breaker. Core restaurants keep adopting Toast, enterprise and drive-thru scale steadily, international and retail contribute but do not transform the story, and AI improves retention and attach without becoming a huge standalone profit pool. Revenue compounds 17–19%, EBITDA margins move toward 14–16%, and the stock trades at 14–17x EBITDA. That yields roughly $42–55. This remains the base case: Toast is not yet the invisible manager, but it is a much better business than the current multiple implies.

The Operating System for Local Commerce. Toast IQ Grow monetization is clean, the agent stack extends into payroll, bookkeeping, scheduling, inventory, and demand generation, Toast Local creates a credible direct-demand loop, and total monetization moves from 103 bps toward 130–150 bps over time. Revenue compounds 22–25%, EBITDA margins approach 18–21%, and the market reclassifies Toast as a high-quality vertical platform at 18–22x EBITDA. That gets the stock to $75–90.

The important point is not that the bull case is certain. It is not. The important point is that at $24, the market is not paying for it. The stock is priced closer to The Quiet Compounder with a DoorDash overhang than to The Operating System for Local Commerce.

The Next Few Quarters Are About Proof, Not Story

The next few quarters need to turn the story from plausible to measurable.

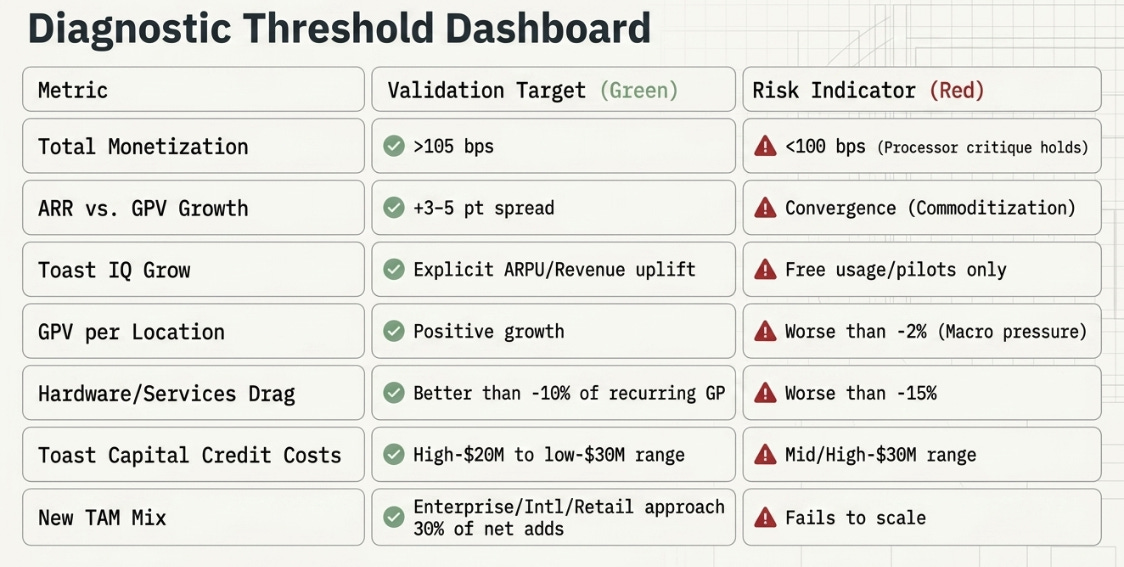

The first metric is total monetization. Above 105 bps of GPV would suggest the platform is becoming more valuable per dollar of restaurant volume. Below 100 bps would make the processor critique harder to dismiss.

The second is the spread between subscription ARR growth and GPV growth. A 3–5 point positive spread supports the software layer. Convergence suggests commoditization.

The third is Toast IQ Grow monetization. Usage, pilots, and anecdotes are not enough anymore. The market needs attach rate, ARPU uplift, revenue contribution, or explicit evidence that AI work is being paid for.

The fourth is GPV per location. Positive growth would ease the macro concern. Worse than -2% would suggest restaurant demand pressure is becoming more than noise.

The fifth is hardware and professional services losses. Better than -10% of recurring gross profit would suggest the subsidy is contained. Worse than -15% would make the acquisition-cost problem harder to dismiss.

The sixth is Toast Capital. Credit costs in the high-$20 million to low-$30 million quarterly range are manageable. A move into the mid- or high-$30 million range would force a harder look at whether lending is adding more cyclical risk than strategic value.

The seventh is new TAM mix. Enterprise, international, and retail approaching 30% of net adds would validate the expansion thesis. If they remain small, the core is still doing most of the work.

The Bet Is Cheaper, but the Bar Is Higher

The business evidence improved. The stock evidence did not.

That distinction is uncomfortable, but it is the entire setup. Toast is not broken because Q2 guidance disappointed. It is also not vindicated because Toast IQ usage is high. The company has moved from a familiar thesis, vertical software plus payments, into a more ambitious one: software that becomes labor.

The market is focused on the right problems: guide shape, DoorDash, GPV per location, hardware drag, credit risk, and AI monetization. But it may be using the wrong time horizon. The question is no longer whether Toast can run the restaurant. The question is whether Toast can increasingly manage it.

At $37, that was an expensive possibility. At $26, it was a more interesting one. At $24, the option is cheaper, but the proof burden is higher.

The register was the wedge. The operating system was the moat. The invisible manager is now the bet.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.