Toast 4Q25 Earnings: The Price of Ambition

What the market misses about the difference between choosing lower margins and having lower margins.

TL;DR:

Toast didn’t disappoint, it delivered a record year, then told investors it will spend upside rather than bank margin expansion.

The market still values Toast like a payments processor, but the business is increasingly a restaurant operating system (Shopify-style), now deepened by Toast IQ.

Margin pressure in 2026 isn’t just “investment”: it’s also chips, tariffs, and a scaling hardware subsidy, plus an underpriced macro risk via Toast Capital.

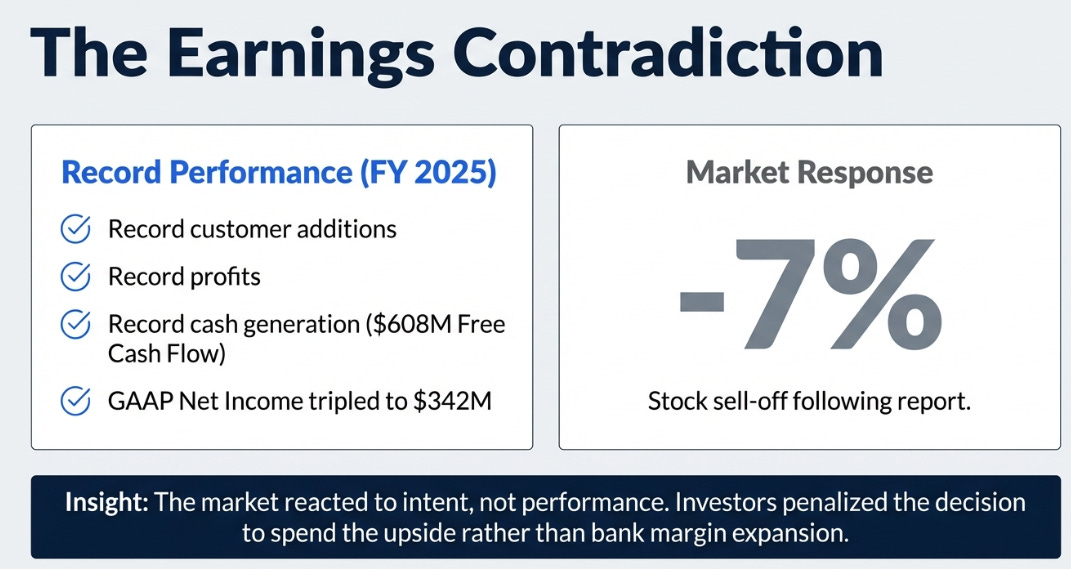

Toast reported its fourth quarter earnings, and the results presented a contradiction worth examining. The company delivered its best year by virtually every measure, record customer additions, record profits, record cash generation, and the stock fell 7%. The market was not reacting to what Toast had done. It was reacting to what Toast said it intended to do with the money.

This is a pattern worth understanding, because it recurs throughout the history of technology platforms, and the companies that get it right tend to be the ones the market punishes most severely in the moment.

The Harvest-or-Invest Decision

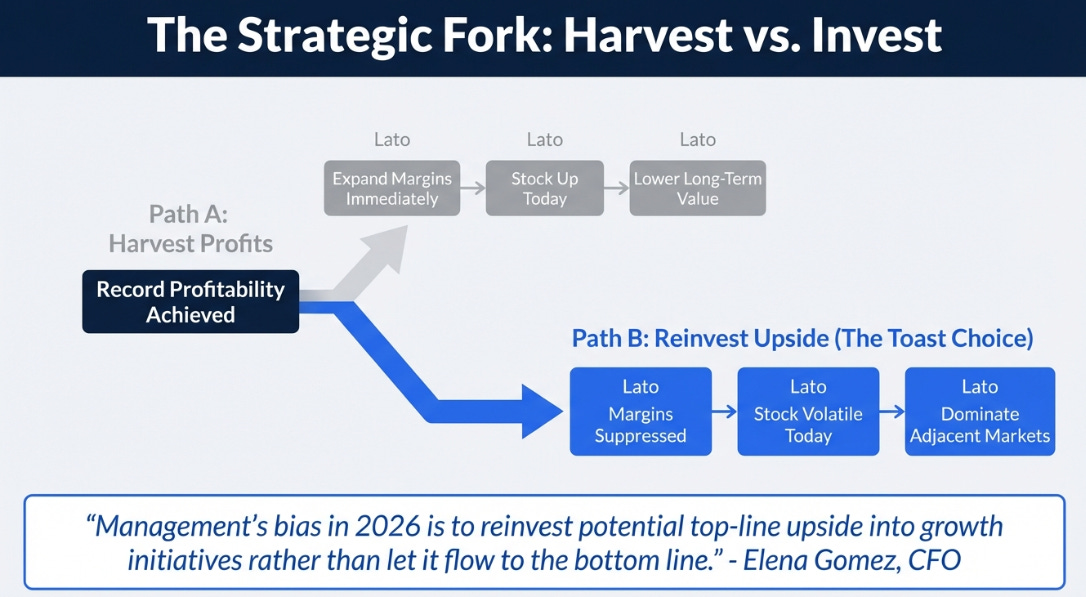

Consider the basic economics of a platform business that has achieved product-market fit in its initial market. The platform has built something customers want, the unit economics work, and the core business is generating substantial profits. At this point, management faces a choice that will define the next decade of the company’s trajectory: harvest those profits and let margins expand, or deploy them to replicate the playbook in adjacent markets before competitors can establish themselves.

The first path makes the stock go up immediately. The second path makes the company worth dramatically more in ten years. They are, in the near term, mutually exclusive.

Toast just chose the second path, and it did so with unusual transparency. On the earnings call, CFO Elena Gomez stated explicitly that management’s bias in 2026 is to reinvest potential top-line upside into growth initiatives rather than let it flow to the bottom line. She wasn’t hedging or being diplomatic. She was telling the market: if things go better than expected, we will spend the upside. Do not model an EBITDA beat.

The market heard this and concluded that margins were stalling. What actually happened is more interesting.

The Operating System, Not the Payment Rail

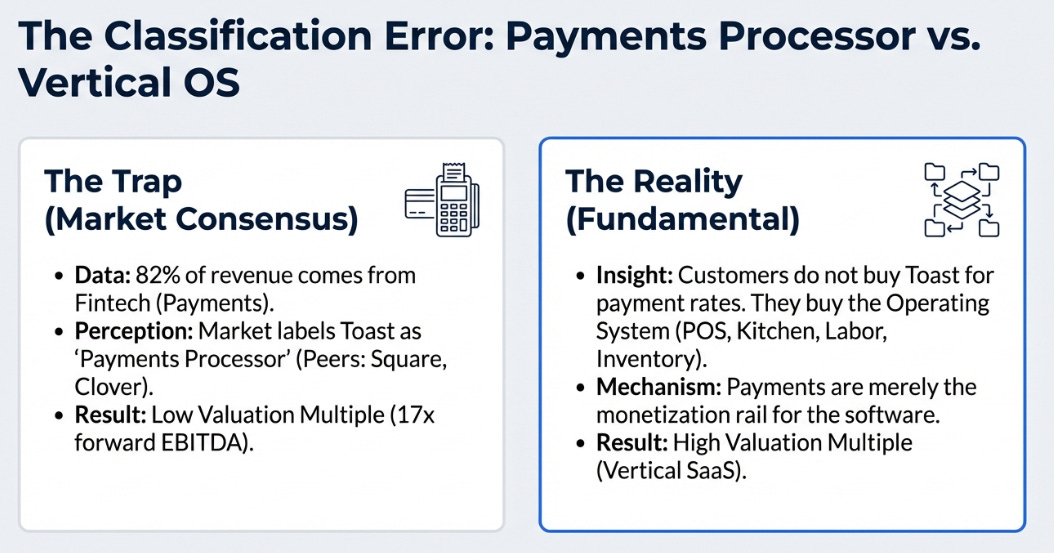

To understand what Toast reported, you first need to understand what Toast actually is, because the market has this wrong, and the misclassification is the source of the valuation disconnect.

Approximately 82% of Toast’s revenue comes from financial technology solutions, which is mostly payment processing. Analysts look at that revenue mix, slot Toast into the payments/fintech category alongside Square and Clover, and value it accordingly. By that framing, Toast at 17x forward EBITDA looks like a modestly premium payments company navigating a difficult investment cycle.

But revenue composition is the wrong lens. The right lens is what creates the customer relationship and what makes it durable. No restaurant chooses Toast because of its payment processing rates. They choose it because Toast is the operating system that runs their entire business, point of sale, kitchen operations, online ordering, employee scheduling, inventory, marketing, loyalty, lending, and now AI-driven insights. Payments flow through that system as a natural consequence of owning the transaction layer, not as the reason the system exists.

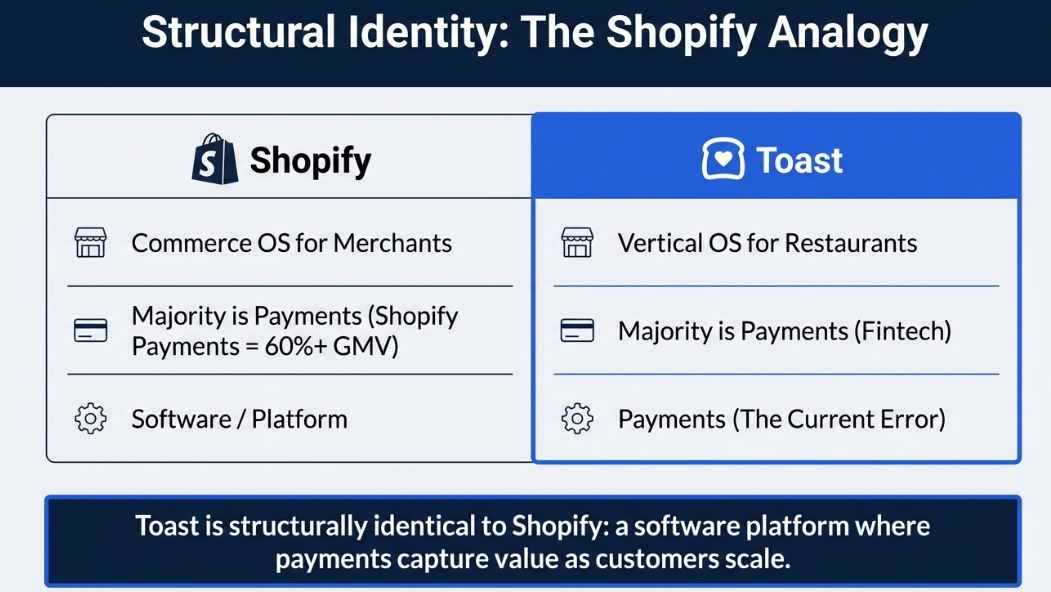

The closest structural analogy is Shopify. Shopify’s revenue is majority payments, Shopify Payments processes over 60% of GMV, but nobody values Shopify as a payments company. The market values it as the commerce operating system for independent merchants, with payments as the embedded monetization rail that scales with merchant success. Toast is structurally identical: a vertical operating system for restaurants, with payments as the monetization layer that captures value as operators grow.

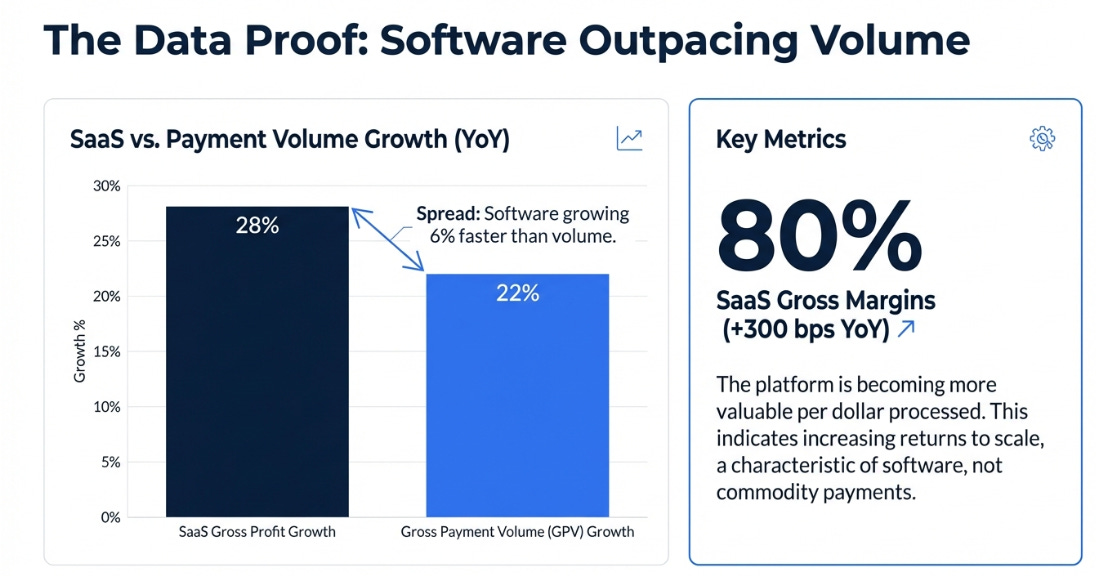

The Q4 data proves this framing is correct. Subscription and fintech gross profit grew 28% while gross payment volume grew 22%. If Toast were a payments business, those numbers would converge. Instead, the software layer is growing six percentage points faster than the volume layer, and that spread is widening. SaaS gross margins expanded 300 basis points year-over-year to 80%. The platform is becoming more valuable per dollar that flows through it. That is the defining characteristic of a software business with increasing returns to scale.

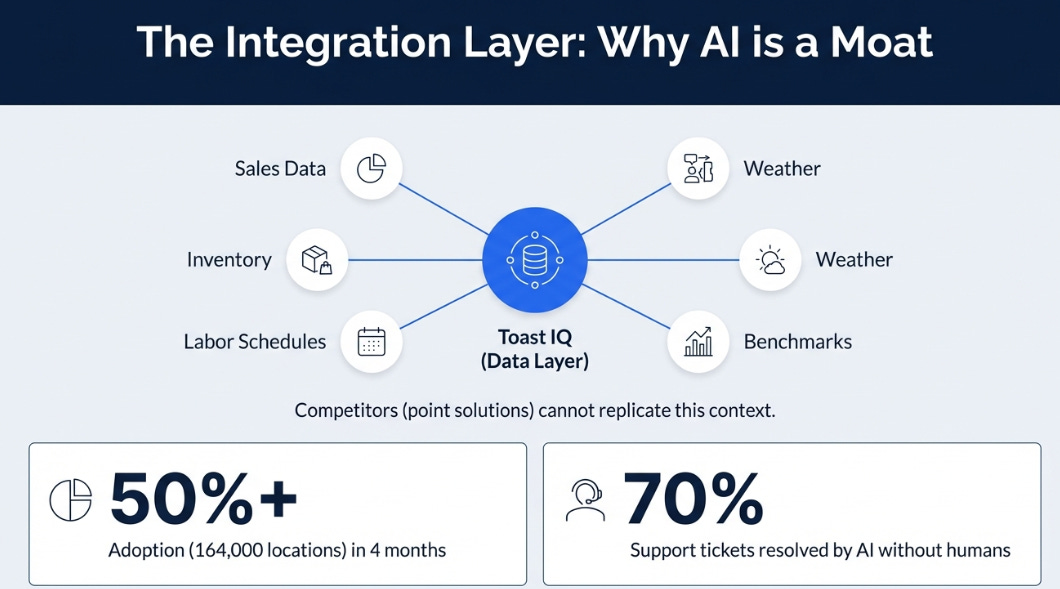

Part of that margin expansion came from a development with structural implications. CEO Aman Narang disclosed that over half of all support interactions now start with an AI agent, and 70% of those never reach a human. Toast IQ, the company’s AI assistant, has been adopted by more than half of all 164,000 locations in under four months, processing over a million queries. Operators use it to analyze sales, update menus, generate marketing content, and manage inventory, workflows that previously required manual effort or third-party services.

The critical thing about Toast IQ is not the support cost savings. It is that Toast IQ can only exist because Toast controls the complete data and workflow layer of the restaurant. When an operator asks “why are my Thursday nights slow?” the answer requires integrating sales data, inventory costs, labor schedules, weather context, and benchmarks from tens of thousands of comparable restaurants. A competitor selling a point solution cannot answer that question because they don’t have access to the full picture. And Narang laid out where this goes next: from copilot to workflow automation to agentic execution to owning entire business functions, marketing, payroll, bookkeeping. If Toast captures even a fraction of the spend restaurants currently direct to fractional hires and third-party vendors for those functions, it opens a revenue layer that sits entirely outside current Wall Street models.

This is the integration layer I described in my Q3 analysis, now with concrete product plans and measurable adoption data.

The Profit Sanctuary Under Load

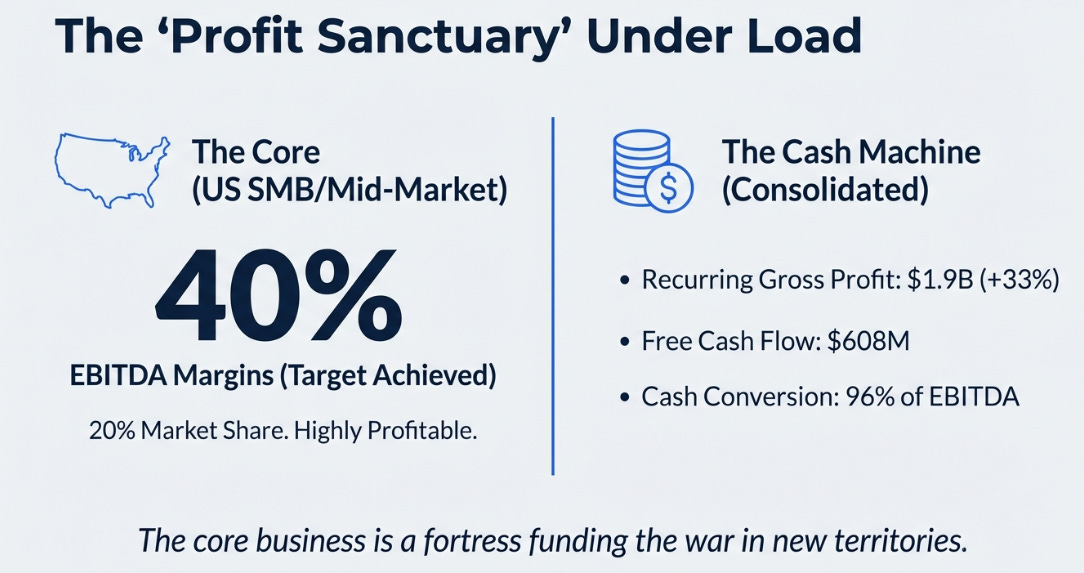

The core US small and medium restaurant business operates at approximately 40% EBITDA margins. Management reaffirmed this on the call and noted they achieved the target ahead of schedule. The core also grew market share to 20% of US SMB and mid-market restaurants, nearly doubled in three years, with sales productivity in the highest-density geographies still outperforming the company average. The saturation thesis does not hold.

Meanwhile, the full-year numbers were striking. Recurring gross profit grew 33% to $1.9 billion. Free cash flow reached $608 million, converting 96% of adjusted EBITDA into cash. GAAP net income tripled to $342 million. This is not a company approaching profitability. It is a cash machine.

The question is what to do with that cash machine, and Toast’s answer is to point it at three adjacent markets simultaneously. Enterprise added marquee wins, Applebee’s, Firehouse Subs, Papa Murphy’s, and management announced a drive-thru product launching later in 2026, which opens the quick-service restaurant segment, by far the largest restaurant category Toast hasn’t meaningfully penetrated. International expanded to Australia as the fourth market, with the total addressable market roughly three times the domestic one. Food and beverage retail got a dedicated sales team, and the early results have been strong enough that Toast is testing beyond food and beverage into adjacent retail verticals.

Each of these new markets doubled its collective ARR in 2025. Each is growing faster than the core restaurant business was at a comparable stage. And each requires upfront investment that suppresses consolidated margins in the near term, which is why the FY2026 EBITDA guide of $775–795 million landed roughly in line with consensus rather than above it, and why a new headwind (approximately 150 basis points of margin drag from surging memory chip costs hitting the hardware line) made the picture look even less appealing.

The 40% core margins are intact. They are being deliberately deployed, not structurally impaired. There is a difference between choosing lower consolidated margins and having lower consolidated margins, and the market is not making that distinction.

The Risk That Isn’t Priced

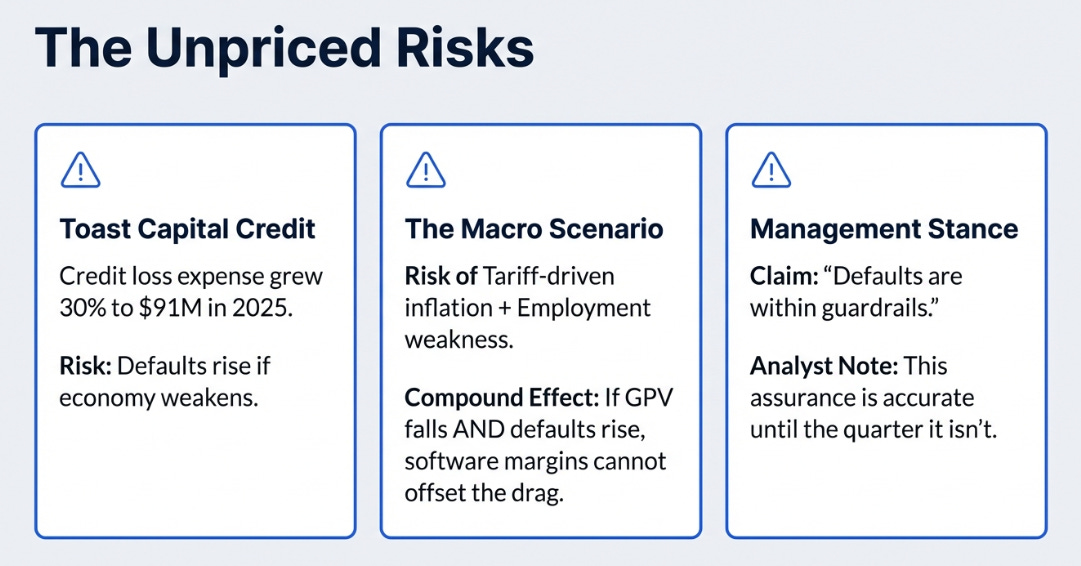

There is a risk embedded in this strategy that deserves more attention. Toast Capital, the lending product, saw credit loss expense grow 30% to $91 million in 2025. The model, merchant cash advances based on projected future sales, performs well when the economy cooperates and poorly when it doesn’t. GPV per location declined 1% year-over-year in Q4, a small number that could be noise or could be an early signal that restaurant consumer spending is softening. If tariff-driven inflation and employment weakness hit simultaneously, declining payment volume and rising credit losses would compound in a way that no amount of software margin expansion can offset. Management says defaults are within guardrails. That is the kind of assurance that is accurate until the quarter it isn’t.

The Variant Perception

The consensus view is that Toast is a decelerating growth story entering an investment cycle with hardware headwinds, a payments company that got expensive and is normalizing. The variant perception is that Toast is a software platform with a payments monetization layer, and the “investment cycle” is the highest-return deployment of capital available to management: building three new billion-dollar-ARR businesses simultaneously from a profit sanctuary generating 40% margins and $600 million in free cash flow. The market is pricing the near-term margin pause. It is not pricing the optionality being created.

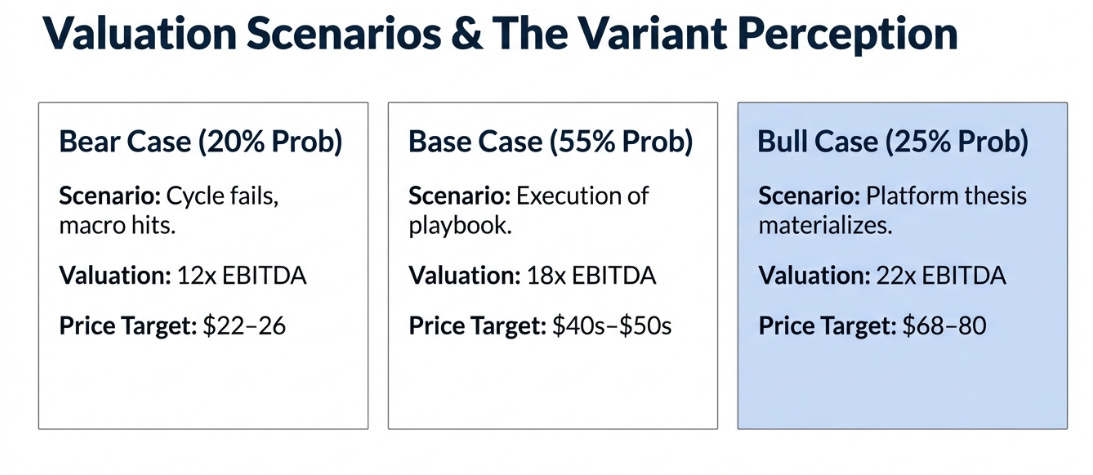

To quantify the gap between those two framings: if the investment cycle fails and macro deteriorates, Toast is roughly fairly valued here, call it $22–26 on a payments-like 12x multiple, with 15% revenue compounding and compressed margins. I’d assign that about 20% probability. If Toast executes the base playbook, 18% revenue compounding, modest margin expansion as the 2026 hardware headwind fades, new TAMs contributing meaningfully but not transforming the growth profile, the stock reaches the mid-$40s to low-$50s over three years at 18x EBITDA, roughly 55% probability. If the platform thesis fully materializes, enterprise scales with drive-thru, international expands, Toast IQ captures outsourced service spend, margins reach 40% on a consolidated basis, the stock reaches $68–80 at 22x, roughly 25% probability. The probability-weighted expected value is approximately $50, or 90% upside from the current price.

Every one of those scenarios offers better risk/reward from $26 than it did from the $37 starting point in my Q3 analysis. The absolute targets came down; the return from here went up. And the $500 million buyback authorization, an unusual move during a self-described investment year, suggests management agrees the stock is mispriced.

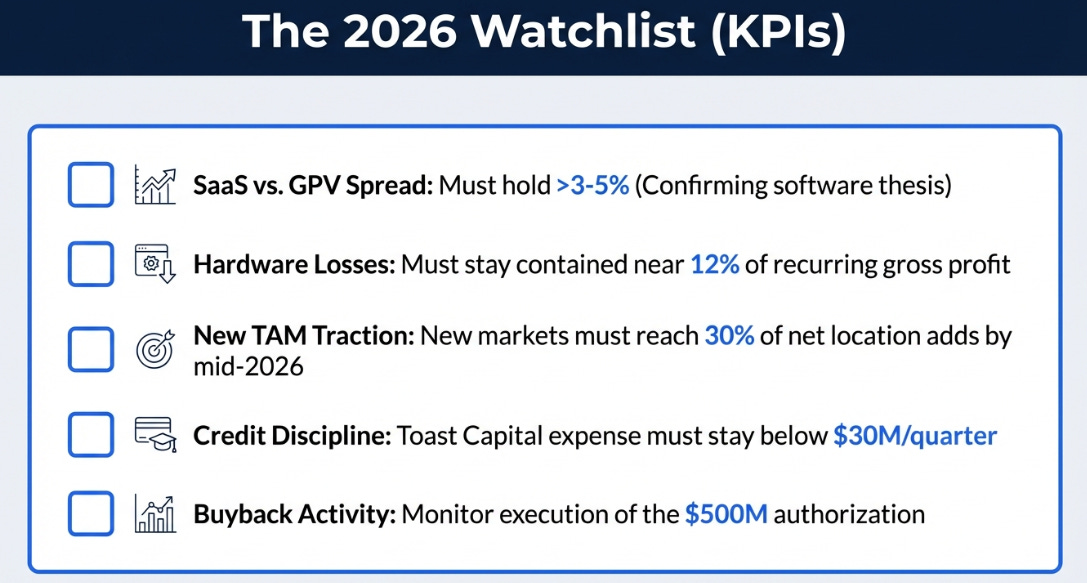

Four things will determine which path materializes over the next year. Whether the SaaS-versus-GPV growth spread holds above three to five percentage points, confirming the software thesis. Whether hardware losses stay contained near 12% of recurring gross profit as memory chip costs cycle through. Whether new TAMs reach 30% of net location additions by mid-2026, validating the multi-vector growth story. And whether Toast Capital credit expense stays below $30 million per quarter, keeping the lending thesis intact.

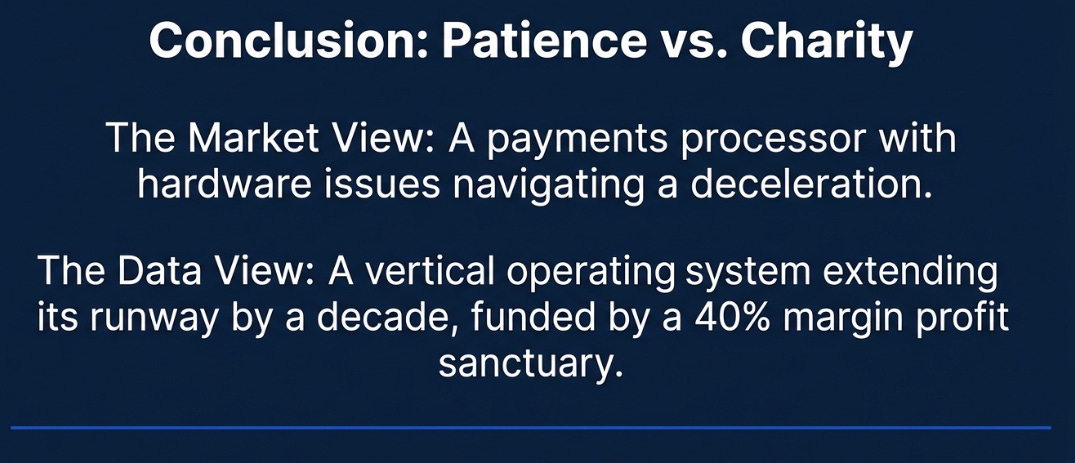

The market is pricing Toast as a payments processor navigating an inconvenient investment cycle. The business looks more like a vertical operating system choosing to extend its growth runway by a decade, funded by a profit sanctuary the market refuses to look through, deepened by an AI layer competitors cannot replicate, and expanding into three adjacent markets each growing faster than the core did at the same stage. One of those framings is wrong. The answer will determine whether buying at $26 was an act of patience or an act of charity. The evidence, on balance, favors patience.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.