TSMC 1Q26: The Bottleneck Travels

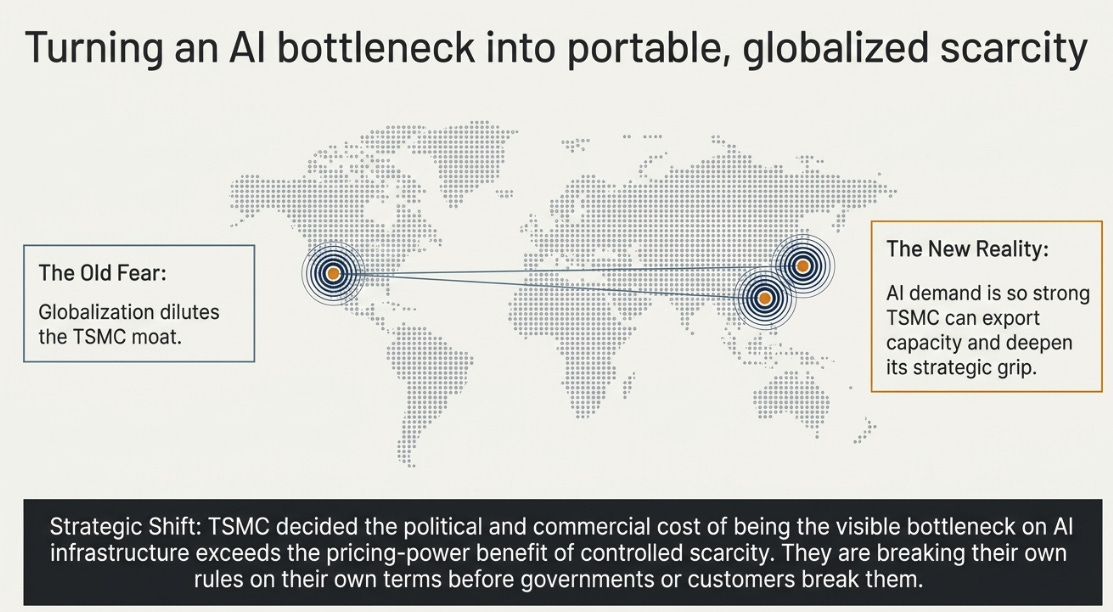

The old fear was that globalization would dilute TSMC's moat. This quarter suggests something more interesting; AI demand is strong enough that TSMC can export capacity and still deepen its strategic

TL;DR

TSMC didn’t just beat and raise: it broke a long-standing rule by adding fresh N3 capacity at a mature node, which signals unusually strong demand visibility.

That move suggests TSMC is turning scarcity into something portable: it can globalize capacity without obviously weakening its strategic grip on AI infrastructure.

But operating strength and shareholder returns are no longer the same story: TSMC’s partner pricing and capex-heavy posture may cap how much of the AI upside investors actually capture.

From Bloomberg’s automated note this morning:

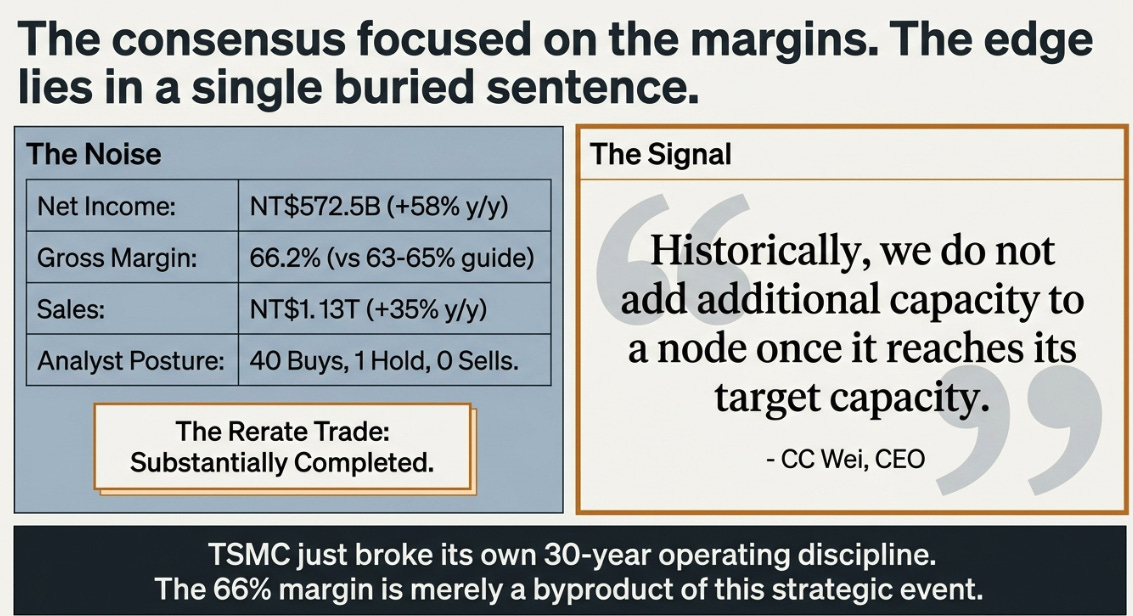

TSMC reported net income for the first quarter that beat the average analyst estimate. Net income NT$572.5 billion, +58% y/y, estimate NT$542.38 billion. Gross margin 66.2% vs. 62.3% q/q, estimate 64.5%. Sales NT$1.13 trillion, +35% y/y. Operating profit NT$658.97 billion, +62% y/y. 40 buys, 1 hold, 0 sells.

Revenue was pre-announced two weeks ago, so the surprise was not in the headline. It was in two places, and only one of them has gotten the attention it deserves.

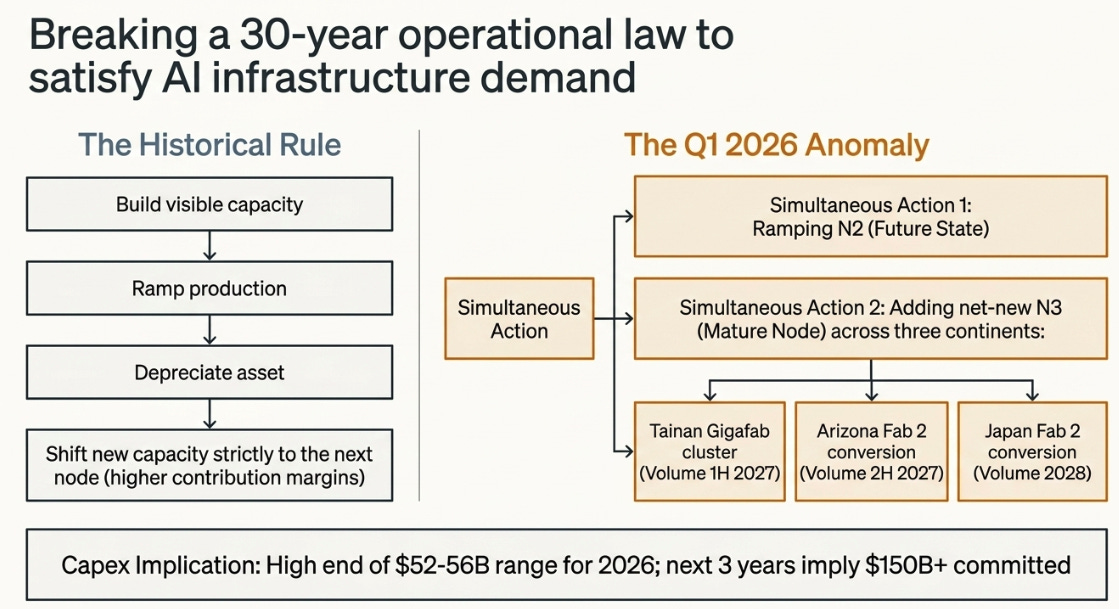

The first surprise, the 66.2% gross margin against 63-65% guidance, the full-year revenue guide raised from “close to 30%” to “above 30%”, Q2 guided to $39-40B, drove the consensus reaction. Another beat, another raise, more evidence of the position we have been bullish on for five consecutive quarters. The second surprise was buried halfway through CC Wei’s prepared remarks. He announced that TSMC is adding net new capacity to N3, a node already in volume production for over three years, across three continents at once. He prefaced it with a sentence that should have been the headline of every TSMC write-up this week and was the headline of almost none: “Historically, we do not add additional capacity to a node once it reaches its target capacity.”

That sentence is the strategic event. The 66% margin is the byproduct.

From Sovereignty Paradox to Portable Scarcity

We have written about TSMC five times in the last twelve months, and the arc has been consistently bullish. The Semiconductor Sovereignty Paradox (April 2025) argued the company was being forced into a transformation that would compromise its moat. That framework was wrong, and Q2 2025 forced the revision, Margin Myths Shattered upgraded the bull case from 20% to 60% on the evidence that 58.6% gross margins survived the headwinds the prior piece had built a thesis around. The Sandbagging Monopolist (October 2025) refined the mechanism, controlled scarcity wrapped in conservative guidance. The Constraint Is the Product (January 2026) pushed the bull case to 65% and added the base-load argument. The stock went from roughly $140 in early 2025 to $380 today. The directional call has been right.

I want to be clear about what this quarter does and does not do to that arc, because the temptation, one I succumbed to in earlier drafts of this piece, is to treat each subsequent print as more confirmation of the same thesis. The honest position is different. At $380, with 40 buys, 1 hold, 0 sells, and the rerate trade substantially completed, the analytical job is no longer to argue that TSMC is misunderstood. The market has, by any reasonable measure, arrived. The job now is to evaluate what the company is doing with its strategic position, and to ask whether the move TSMC made today, which is genuinely significant, translates into shareholder returns at the same rate the operating performance suggests it should.

Those are different questions. I do not think our prior arc distinguished between them carefully enough.

The Capacity Rule, Broken

A new N3 fab in the Tainan Gigafab cluster, volume 1H 2027. Arizona Fab 2, construction complete, converted to N3 with volume in 2H 2027. Japan Fab 2 converted to N3, volume in 2028. Continued N5-to-N3 conversion in Taiwan on top of all of that. Capex to the high end of the $52–56 billion 2026 range; Wendell Huang said next-three-year capex will be “significantly higher” than the past three years’ $101B total, implying $150 billion or more committed for 2026–2028.

The capacity rule is not a stylistic preference. It is the operating discipline that has defined TSMC’s financial architecture since Morris Chang founded the company in 1987. You build the capacity you have visible orders for, you ramp it, you depreciate it, and you do not go back and add to it at an older node, new capacity goes to the next node, where pricing is fresh and contribution margins are higher. The through-cycle margin discipline, the deliberate node-transition tempo, the “narrow the gap” pricing posture we wrote about in October, all of it rests on the rule. Breaking it is a choice with consequences.

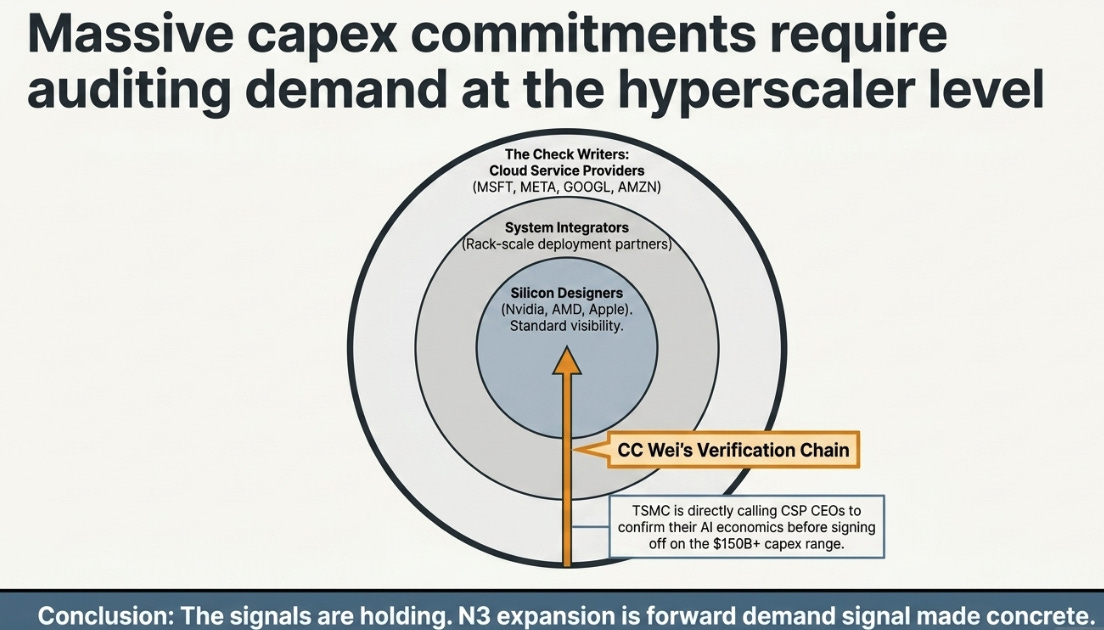

Two readings of the announcement are both true and both worth holding. The first is that demand visibility through 2027–2028 is now large enough that N2 cannot meet it alone, and N3 expansion is forward demand signal made concrete. CC’s verification chain matters here: he repeatedly references “customers, customers’ customers, and the CSPs”, TSMC is auditing demand at the hyperscaler level, not just at the silicon designer level, before committing. That is the same verification process Wei described doing personally last quarter when he called cloud service provider CEOs to confirm their AI economics before signing off on the original capex range. The signals are holding. The capex is moving up in response.

The second reading is that TSMC has decided the political and commercial cost of being the visible bottleneck on AI infrastructure has come to exceed the pricing-power benefit of remaining the bottleneck. There is a version of the next eighteen months where the U.S. government, the customer base, and Taiwan’s own diplomatic position all converge on the view that controlled scarcity in advanced node capacity is no longer acceptable when AI infrastructure is being framed as national security. TSMC is moving ahead of that. They would rather break their own capacity rule on their own terms than have it broken for them.

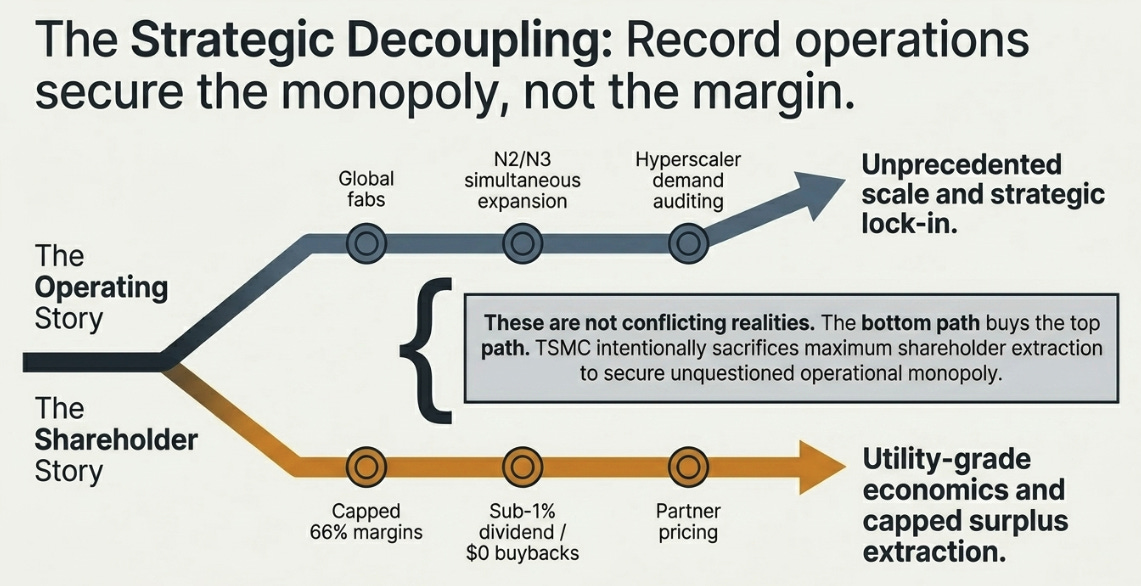

This is not a bullish or bearish observation. It is a strategic observation about what kind of company TSMC is choosing to become, and that choice is the through-line to everything that follows.

The Partner Doctrine and What It Costs You

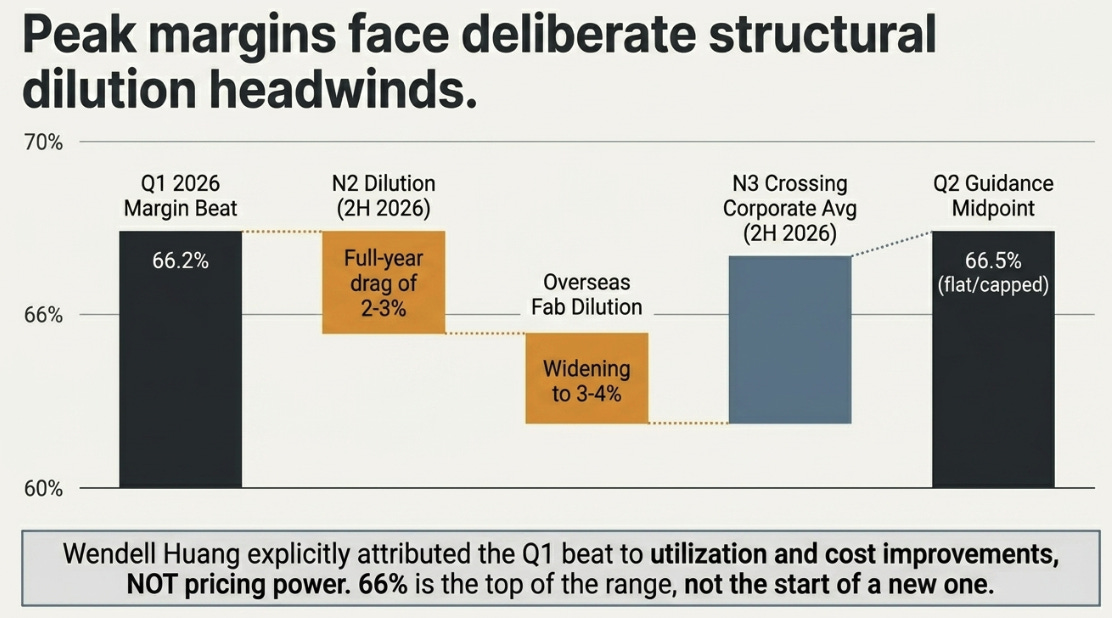

The margin beat’s composition matters more than the headline number. Wendell attributed the 120bp beat versus guidance to “higher-than-expected overall capacity utilization rate and better cost improvement efforts”, explicitly not to pricing. Q2 guidance of 66.5% gross margin midpoint adds only 30 basis points QoQ, a sharp deceleration from Q1’s 390bp jump, because N2 dilution flows through in 2H 2026 at 2-3% full-year drag, overseas dilution widens from 2-3% in early stages to a newly-disclosed 3-4% in later stages, and the offset is N3 crossing corporate-average margin in 2H 2026. The puts and takes roughly net to flat-to-slightly-up margins at peak utilization. The 66% is closer to the top of the range than the start of a new one.

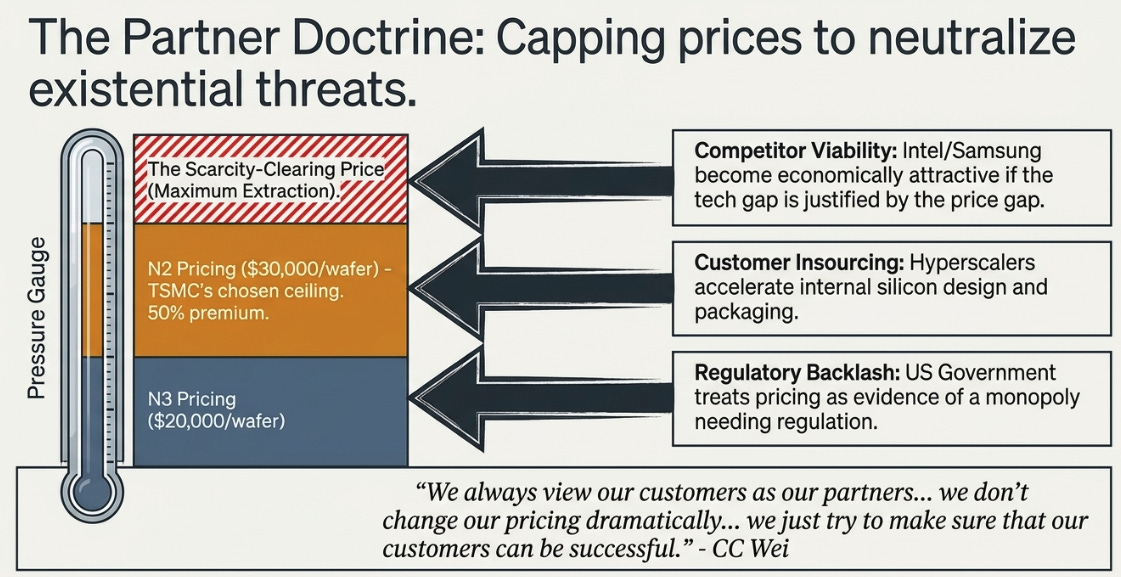

On pricing specifically, Goldman’s Bruce Lu pushed CC on whether the supply situation justified more aggressive extraction. The answer is what we have been calling the partner doctrine, and it is the most strategically important thing TSMC says with consistency:

“We always view our customers as our partners. Of course, we know our value. Of course, we know our position. But we also view our partner as a very important business partner. So that we don’t change our pricing dramatically or something like that. We just try to make sure that our customers can be successful in their market. Customer is our partners.”

N2 wafers are reportedly priced around $30,000, versus $20,000 for N3 at similar maturity. A 50% ASP premium for one node transition is very high in absolute terms, but it is only modestly above what the cost structure would predict. TSMC is not extracting maximum surplus from Nvidia, Apple, or AMD. They are deliberately leaving margin on the table. If TSMC priced at the actual scarcity-clearing level for N2, Samsung and Intel become economically attractive again because the price differential would justify the technology gap; hyperscalers accelerate internalization of design and packaging; the U.S. government treats TSMC’s pricing as evidence the company needs to be regulated or domesticated. The partner doctrine is the strategic equivalent of OPEC choosing to sit below the squeeze level, not because they cannot squeeze, but because they understand the second-order consequences.

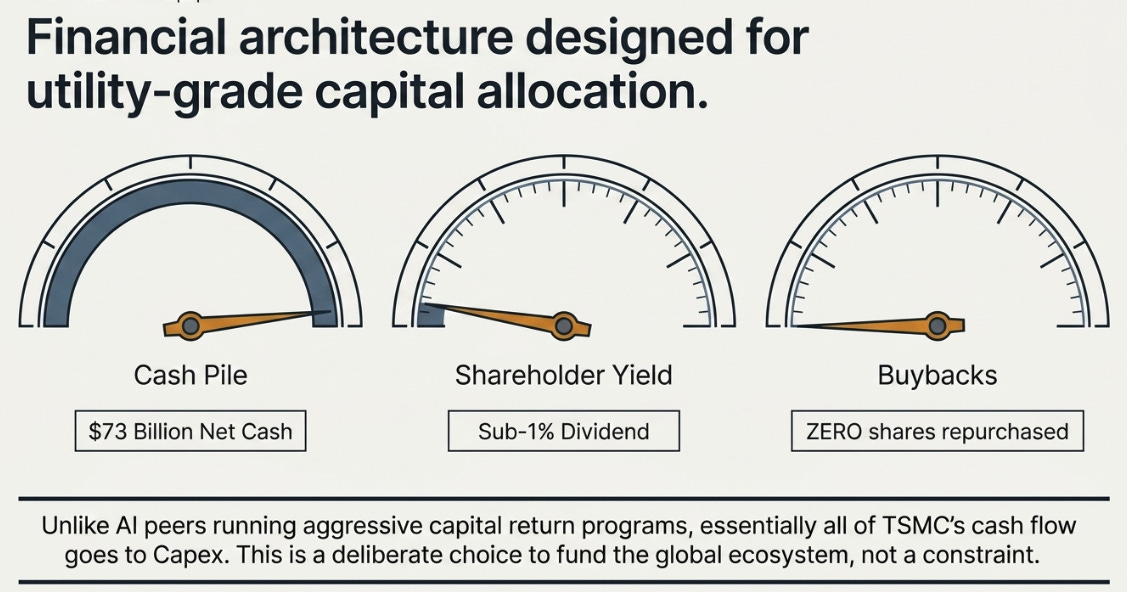

The capital allocation posture is consistent with this. TSMC has roughly $73 billion in net cash, pays a dividend yielding under 1%, and has never repurchased shares. Essentially all cash flow goes to capex. This is utility-grade capital allocation, not AI-infrastructure-leader capital allocation, and it is another deliberate choice, not a constraint.

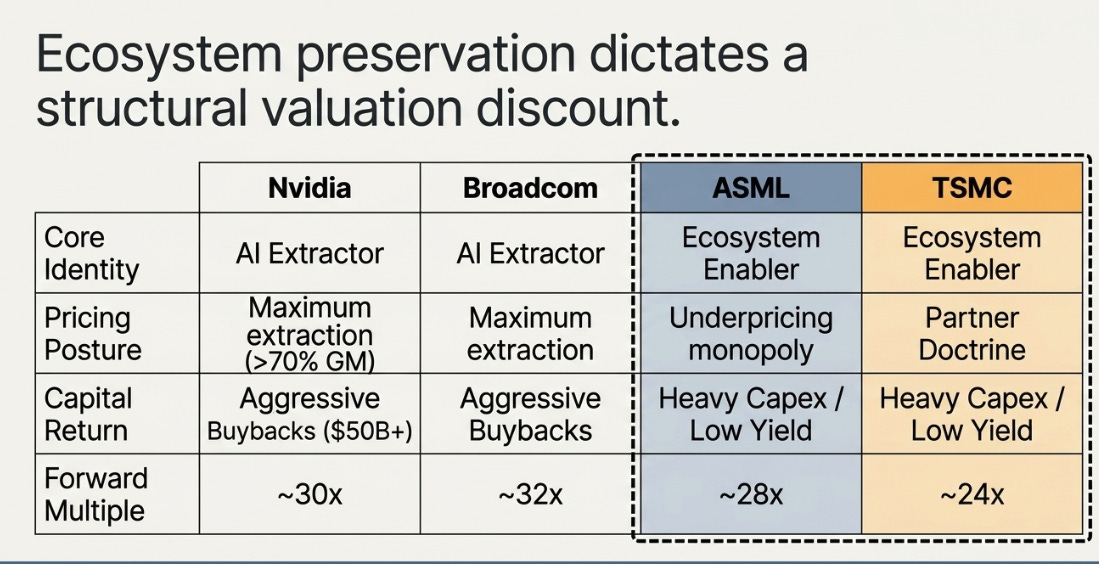

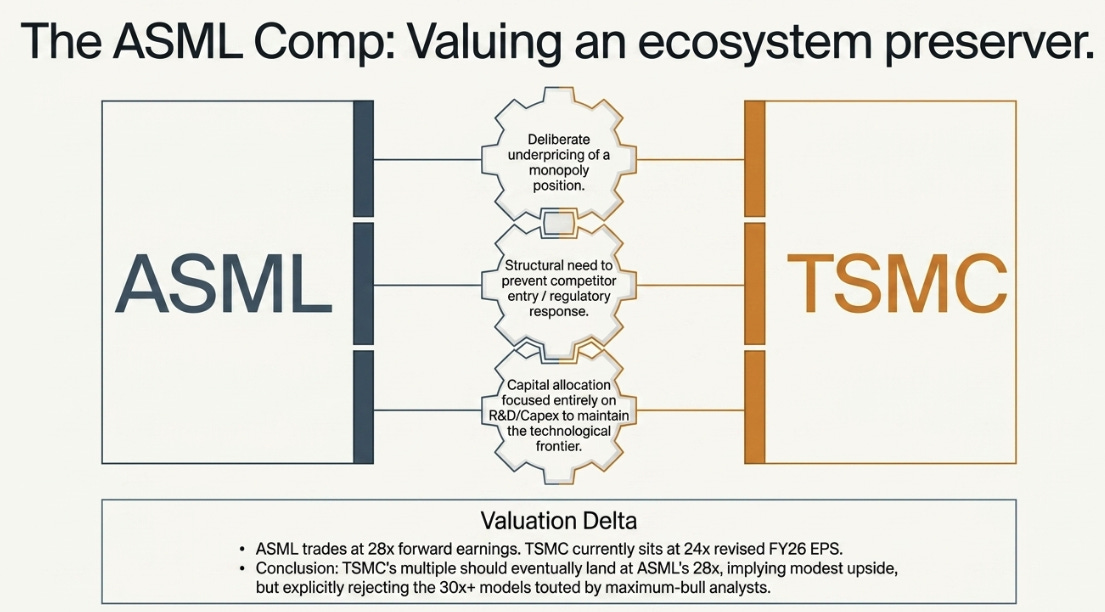

Variant: The Right Comp Is ASML, Not Nvidia

The consensus path from $380 is multiple expansion toward the AI infrastructure peer set, Nvidia at roughly 30x forward earnings, Broadcom at 32x, ASML at 28x. TSMC at 24x revised FY26 EPS sits at a 15-25% discount to that cohort. The implicit bull thesis, one we largely endorsed in January, is that the discount closes as 2026-2027 prints validate the durability of the capex cycle.

Our variant is that the discount is structural, not cyclical. It is also chosen. The partner doctrine on pricing, the conservative capital allocation, the deliberate underpricing of scarcity, these are strategic decisions that systematically cap how much of the AI economy’s economics flow through to TSMC shareholders. A company that chooses to leave margin on the table for ecosystem-preservation reasons should not trade at the same multiple as companies that choose to extract it. Nvidia has repurchased north of $50 billion in shares over the last three years and prices its Hopper and Blackwell accelerators at gross margins north of 70% because the market will bear it. Broadcom runs one of the most aggressive capital return programs in large-cap technology. TSMC has repurchased zero, pays a sub-1% yield, and sets wafer prices at levels chosen to preserve customer success rather than maximize TSMC margin.

The right comp is ASML, 28x forward, same strategic posture of deliberately underpricing a monopoly position to preserve a customer ecosystem, same structural reason for why maximum rent extraction would invite both competitive entry and regulatory response. ASML’s multiple is where TSMC’s should eventually land, not Nvidia’s or Broadcom’s. That implies modest further upside from the current 24x, maybe to 26-28x, but not the 30x-plus some bulls are modeling. The discount to NVDA and AVGO is not a mispricing. It is TSMC’s strategic posture correctly reflected in the multiple.

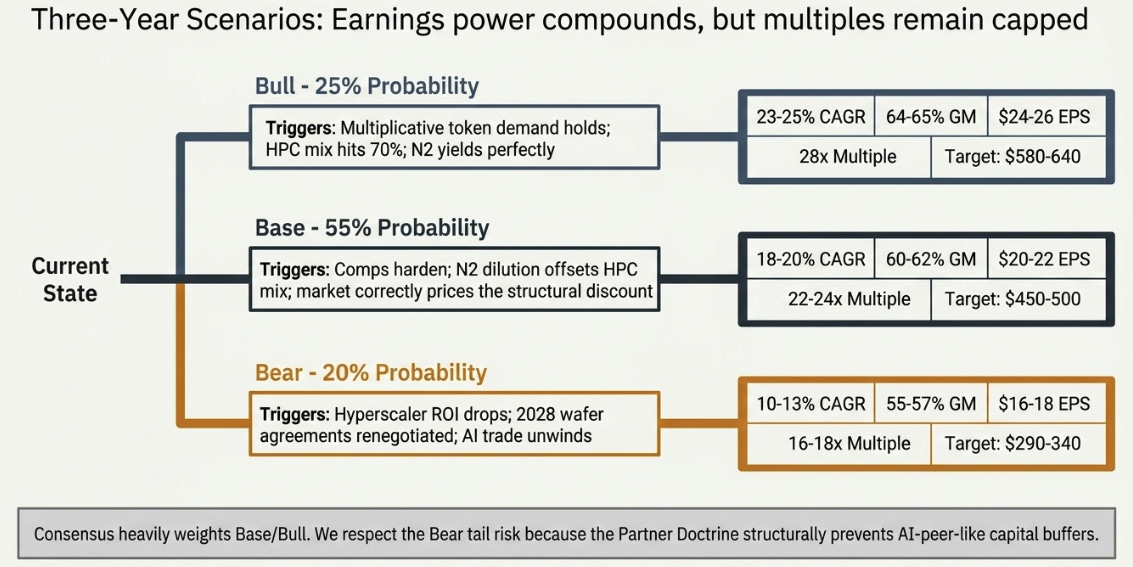

Three Years Out

Bull case: multiplicative token thesis continues (more users × more tasks × more tokens per task); closed-frontier centralization holds; hyperscaler AI commercial revenue compounds at rates that justify committed capex; N2 yields hit targets; HPC mix reaches 70%. The partner doctrine still caps the multiple at around ASML’s 28x, but earnings power is enough to drive the stock materially higher even without a full AI-peer rerate.

Base case: demand stays strong but normalizes. Revenue growth decelerates from 30%+ in 2026 to high-teens by 2028 as comps harden. Margins hold in low-60s as N2 dilution offsets HPC mix tailwind. Multiple stays close to current levels, the market correctly prices the structural discount. This is roughly where consensus sits, though consensus implicitly models a higher multiple than we do.

Bear case: not an AI collapse scenario. Hyperscaler ROI on 2025-26 capex disappoints enough in 2027 that 2028 wafer agreements get renegotiated, N2 dilution runs worse than guided, and the multiple compresses as the AI infrastructure trade broadly unwinds. TSMC retains its market position. The stock does not retain its multiple. Probability reflects that this is a tail scenario, not a base case, but one large enough to respect.

Consensus probability weighting is closer to 40/50/10. Ours is 25/55/20. The difference is that we think the bull case requires the partner doctrine to generate AI-peer-like capital returns, which it structurally will not, and we think the bear case is not as tail as consensus treats it.

What to Track

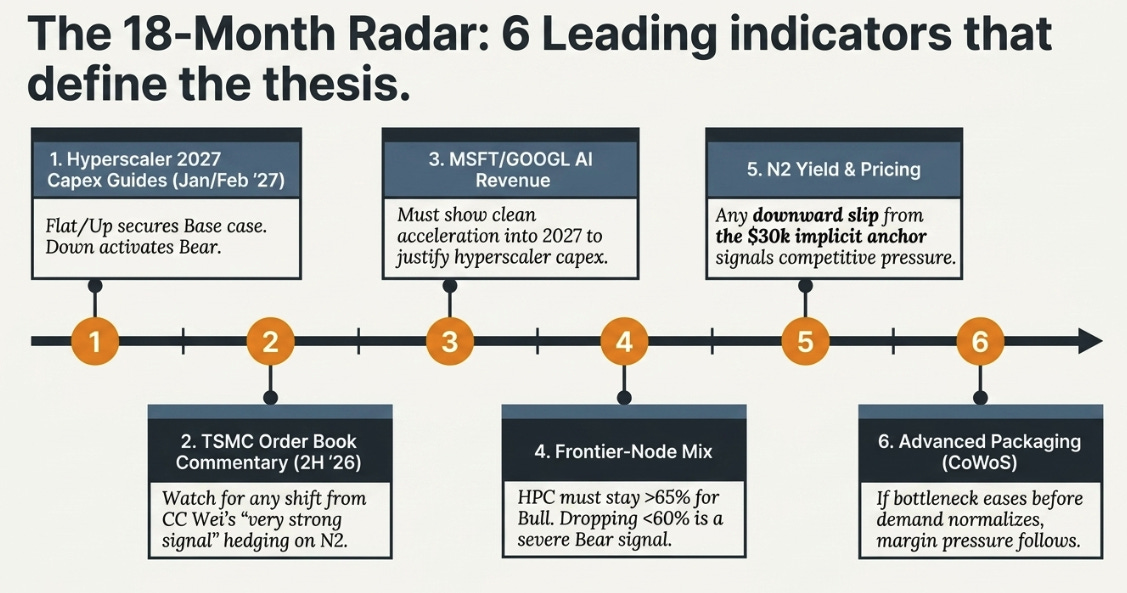

The thesis resolves on six specific observations over the next 18-24 months, in rough order of leading-indicator value:

Hyperscaler 2027 capex guides given on Q4 2026 prints (late January / early February 2027). If MSFT, META, GOOGL, and AMZN guide 2027 capex flat or up vs 2026, the base case holds. Guide down even modestly and the bear case activates.

TSMC customer order book commentary across 2H 2026, any shift from “very strong signal” language, any hedging on N2 demand visibility. CC has been using almost identical phrasing for four consecutive quarters; a change is a signal.

Frontier-node mix specifically. HPC mix going above 65% supports the bull path. Stalling at 60-62% supports base. Declining would be the strongest bear signal available.

N2 yield commentary and customer pricing. If ASP commentary moves off the implicit $30k anchor downward, competitive pressure is arriving.

Microsoft and Google AI-attributable revenue trajectories, not aggregate cloud, but cleanly AI-identifiable revenue lines. Needs to show continued acceleration into 2027 to validate capex.

Advanced packaging capacity. CoWoS remains the binding constraint on Nvidia rack-scale deployments. If TSMC’s packaging bottleneck eases before customer demand normalizes, margin pressure follows.

Closing

Morris Chang built TSMC on the rule that you do not add capacity to a mature node. CC Wei broke that rule today, deliberately, after personally verifying demand with the people writing the checks. That is the strategic event of Q1 2026.

The bullish story from here requires AI demand to validate on roughly the trajectory management has implicitly committed to. That trajectory is plausible, multiplicative token demand is real, closed-frontier centralization has held, hyperscaler capex commitments have not softened. But the path from there to shareholder returns runs through a partner doctrine that caps how much of the AI economy’s value TSMC extracts, and through a capital allocation posture that returns almost nothing directly. The operating story and the shareholder story have partly decoupled. The operating story is still excellent. The shareholder story at $380 is closer to fair than the prior arc implied.

Hold at current levels. Add on weakness toward $340. Trim above $500. The easy part of the trade is behind us, and the next leg requires something different from what produced the last leg.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.