TSMC 2Q26: The Cost of Building the AI Age

The bottleneck has become a construction schedule, and the partner doctrine may be what keeps it durable

TL; DR

TSMC’s latest guidance suggests the AI opportunity is expanding faster than even the company’s previous capacity plans anticipated.

The constraint has shifted from deliberate scarcity to construction: fabs, advanced packaging, power, equipment, and five-to-seven-year production timelines.

TSMC’s pricing restraint is not a weakness but part of the moat, leaving enough value with customers to keep their best designs, commitments, and future road maps concentrated at TSMC.

Morris Chang built TSMC around a simple discipline: capacity should follow visible demand.

That principle mattered almost as much as the foundry model itself. Semiconductor fabrication is a business in which enthusiasm appears years before revenue, while depreciation remains years after enthusiasm fades. The easiest way to destroy capital is to mistake every customer’s ambition for aggregate demand.

TSMC avoided that trap by moving methodically from one process generation to the next. It built a node, ramped it, improved yields, and directed the next wave of capital toward the following technology. Once a node reached its planned scale, TSMC generally did not return to add substantial capacity.

That rule was broken last quarter.

TSMC announced fresh 3-nanometre capacity across Taiwan, Arizona, and Japan even as 2-nanometre production was beginning to ramp. We argued then that the decision revealed unusually strong demand visibility: N2 alone would not satisfy what TSMC could already see through 2027 and 2028.

There was another interpretation. TSMC had spent several years benefiting from scarcity. Perhaps the political and commercial cost of remaining the visible constraint on AI infrastructure had become greater than the pricing benefit of preserving it. The company was choosing scale over maximum extraction.

Three months later, the N3 decision looks less like an exception than the first indication that TSMC’s model of the future had become too small.

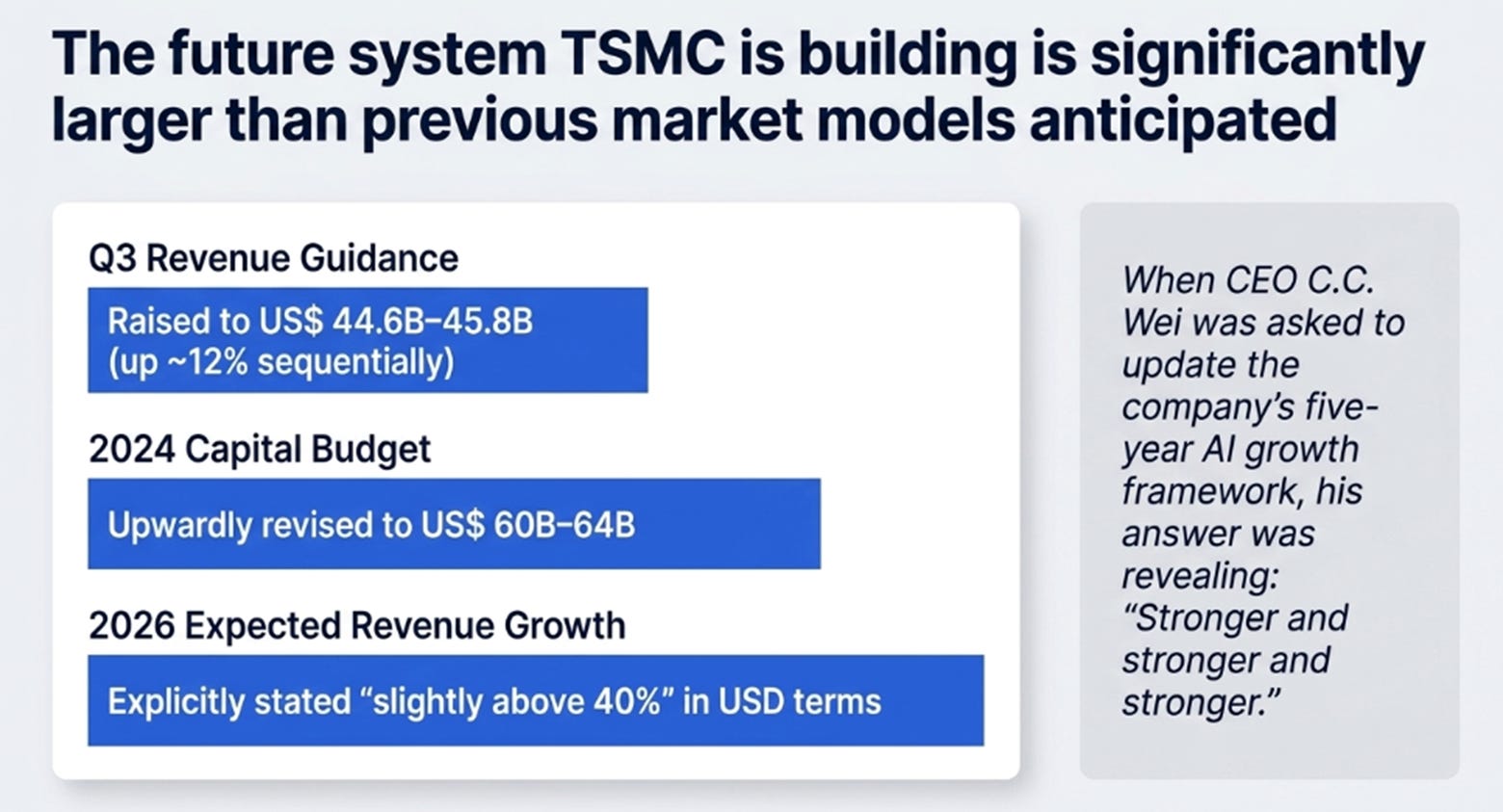

TSMC now expects 2026 revenue to grow slightly above 40% in US-dollar terms, has raised its capital budget to US$60 billion–64 billion, and says its previous N2 and N3 capacity assumptions are already “bigger.” When CEO C.C. Wei was asked to update the company’s five-year AI growth framework, he declined to provide another percentage. His answer was more revealing:

“Stronger and stronger and stronger.”

The question is no longer whether TSMC can make the bottleneck travel. It is whether the company can build the production system for the AI age without allowing the cost of construction to consume too much of the value it creates.

The Quarter That Changed the Forecast

TSMC’s second-quarter results were excellent, although the strategic event was the outlook rather than the quarter itself.

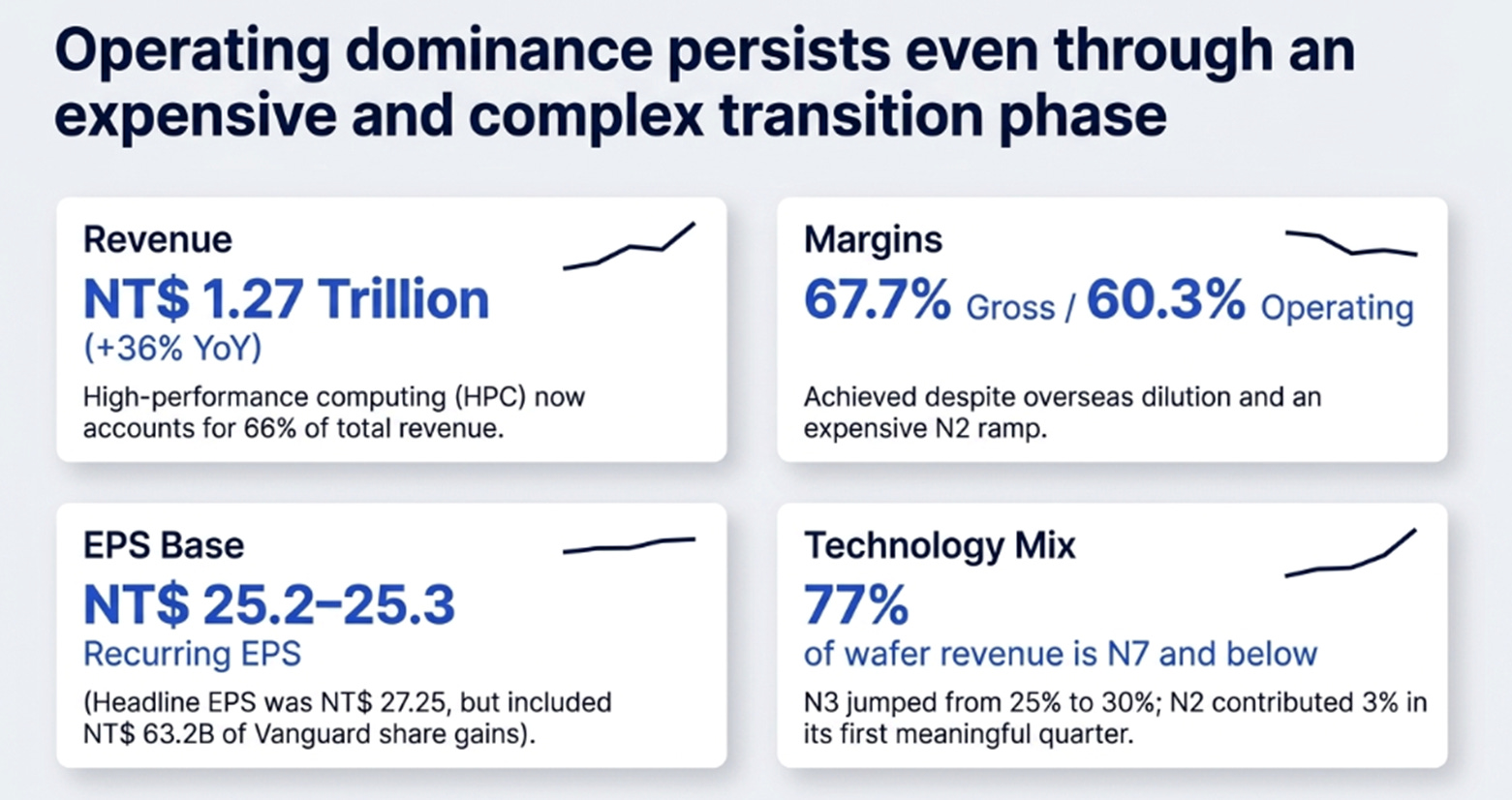

Revenue reached NT$1.27 trillion, up 36% year over year. Gross margin was 67.7%, operating margin reached 60.3%, and diluted earnings per share were NT$27.25. High-performance computing accounted for 66% of revenue, while technologies at 7 nanometres and below represented 77% of wafer revenue.

The headline EPS was somewhat better than the underlying result. Reported earnings included NT$63.2 billion of gains related to Vanguard International Semiconductor shares. After tax, recurring EPS was closer to NT$25.2–25.3: still a healthy beat, but not the 13% surprise implied by the headline.

The operating performance mattered more. Revenue had largely been known because TSMC reports monthly sales. The genuine surprise was that operating margin exceeded 60% even as overseas fabs diluted profitability and N2 entered an expensive ramp.

The mix showed how rapidly the company is changing. HPC revenue increased 20% sequentially and rose from 61% to 66% of total revenue. Smartphone revenue declined 4% and fell to 22%. N2 contributed 3% of wafer revenue in its first meaningful quarter, while N3 increased from 25% to 30%.

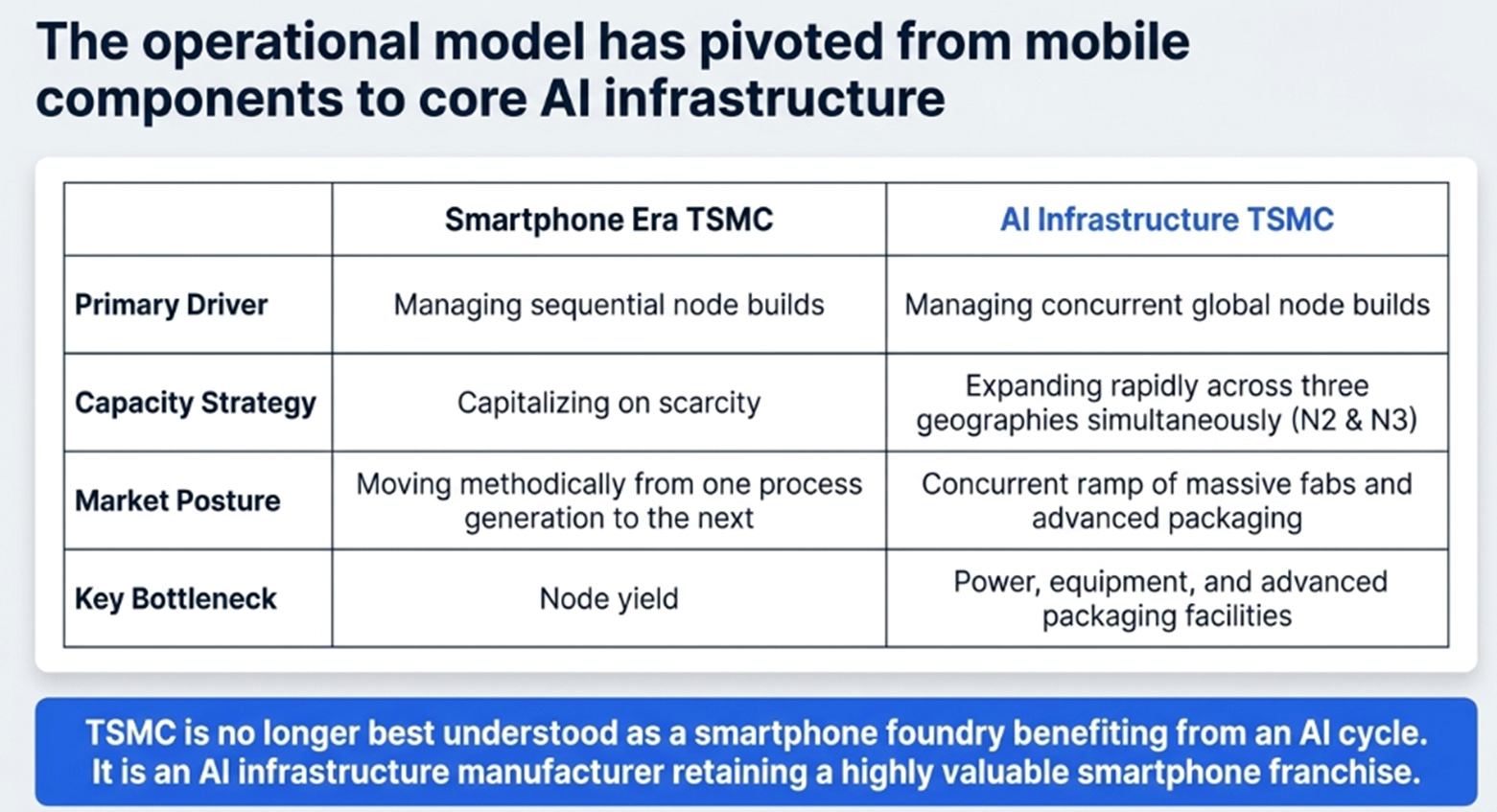

TSMC is no longer best understood as a smartphone foundry benefiting from an AI cycle. It is becoming an AI infrastructure manufacturer that retains a highly valuable smartphone franchise.

The larger change came in guidance. Third-quarter revenue is expected to reach US$44.6 billion–45.8 billion, up roughly 12% sequentially at the midpoint. Gross margin is expected to remain between 65% and 67%, while full-year growth has been raised far beyond the “above 30%” framework management offered only three months earlier.

Our previous view was that revenue would remain strong but normalize into the high teens, margins near 66% were probably closer to the top of the range than the start of a new one, and partner pricing plus overseas dilution would cap how much of TSMC’s operating strength reached shareholders.

That view was right about how TSMC behaves. It was too conservative about the size of the system within which that behaviour now operates.

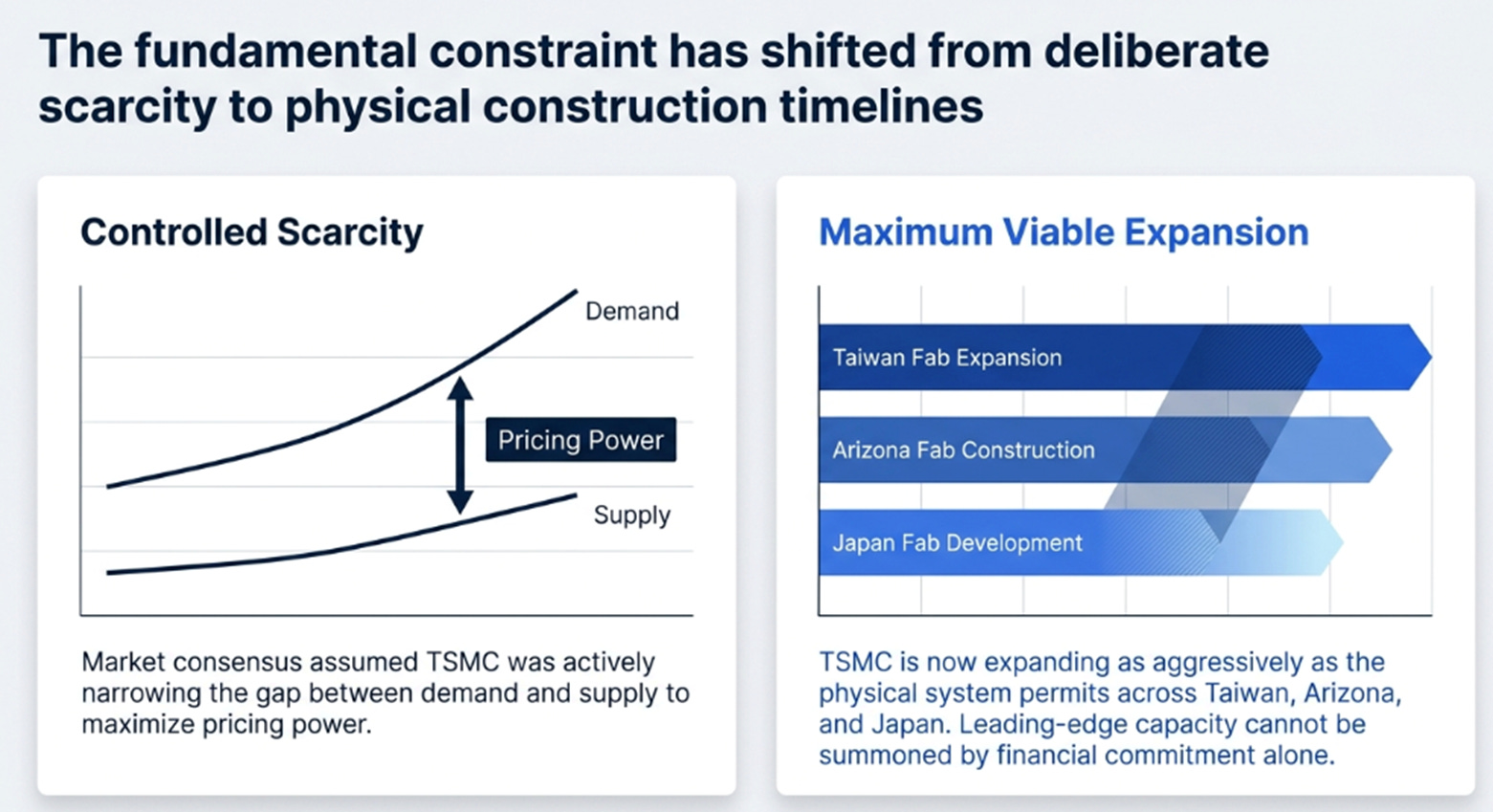

The Bottleneck Becomes a Construction Schedule

In earlier articles, we described TSMC’s posture as controlled scarcity. Management repeatedly said it was working to “narrow the gap” between demand and supply, not eliminate it. Persistent shortage encouraged customers to reserve capacity years in advance, accept higher prices, and deepen their dependence on TSMC’s road map.

That framework explained much of 2025. It is no longer complete.

TSMC is now expanding as aggressively as the physical system permits. It is adding N3 capacity across three geographies, rapidly ramping N2, converting existing tools, building advanced-packaging facilities, accelerating fabs in Arizona, Taiwan, and Japan, and welcoming third-party packaging capacity because its own back-end capacity is insufficient.

This does not look like a company deliberately preserving scarcity. A better formulation is that TSMC is managing the rate at which scarcity can be relieved without compromising technology, yields, customer trust, or returns.

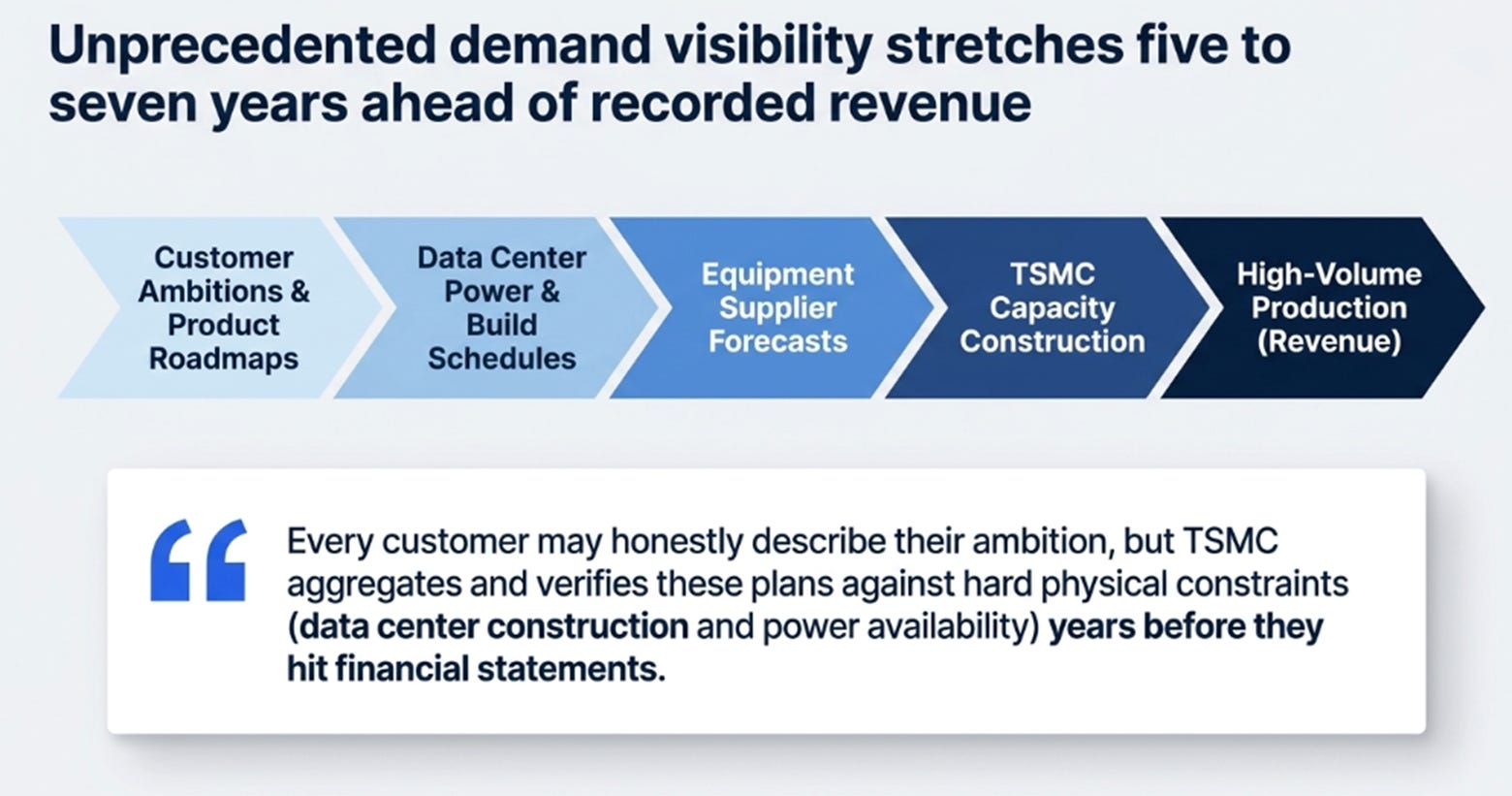

The shortage persists because leading-edge capacity cannot be summoned by financial commitment alone. TSMC says developing a new technology, preparing customer products, constructing capacity, and reaching high-volume production can now take five to seven years.

TSMC therefore sees something outside investors cannot: the industry’s plans before those plans become revenue.

Customers reveal product road maps. Chip designers reveal expected volumes. Cloud providers reveal infrastructure plans. TSMC checks data-centre construction, power availability, and deployment schedules. Equipment suppliers receive capacity forecasts years in advance.

Wei offered an unusually candid description of this process. Every customer may honestly describe its own ambition, he explained, but the sum of every customer’s forecast cannot be true. TSMC must apply its own judgement.

That judgement is becoming a competitive advantage. The most advanced customers reveal their futures to TSMC. That information helps TSMC decide which technologies and capacity to build. Successful execution deepens customer trust. More valuable designs move to TSMC. Those designs create manufacturing learning, supplier influence, and cash flow, which fund the next generation of technology.

The original TSMC flywheel was built around the density of Taiwan’s engineering ecosystem. The new flywheel is geographically distributed, but the informational and technological centre remains TSMC.

The bottleneck has not disappeared. It has become a construction schedule.

The Partner Doctrine Is the Moat

TSMC’s restraint on pricing has often been treated as a limitation.

Wei was again explicit. TSMC knows its value and understands its position, but it sees customers as partners. It does not want to impose sudden price increases that leave customers unable to succeed. Its objective is to earn enough to finance long-term expansion while allowing the ecosystem to keep growing.

The usual interpretation is that TSMC has extraordinary pricing power but chooses not to use all of it, thereby capping margins and shareholder returns.

That is true, but incomplete.

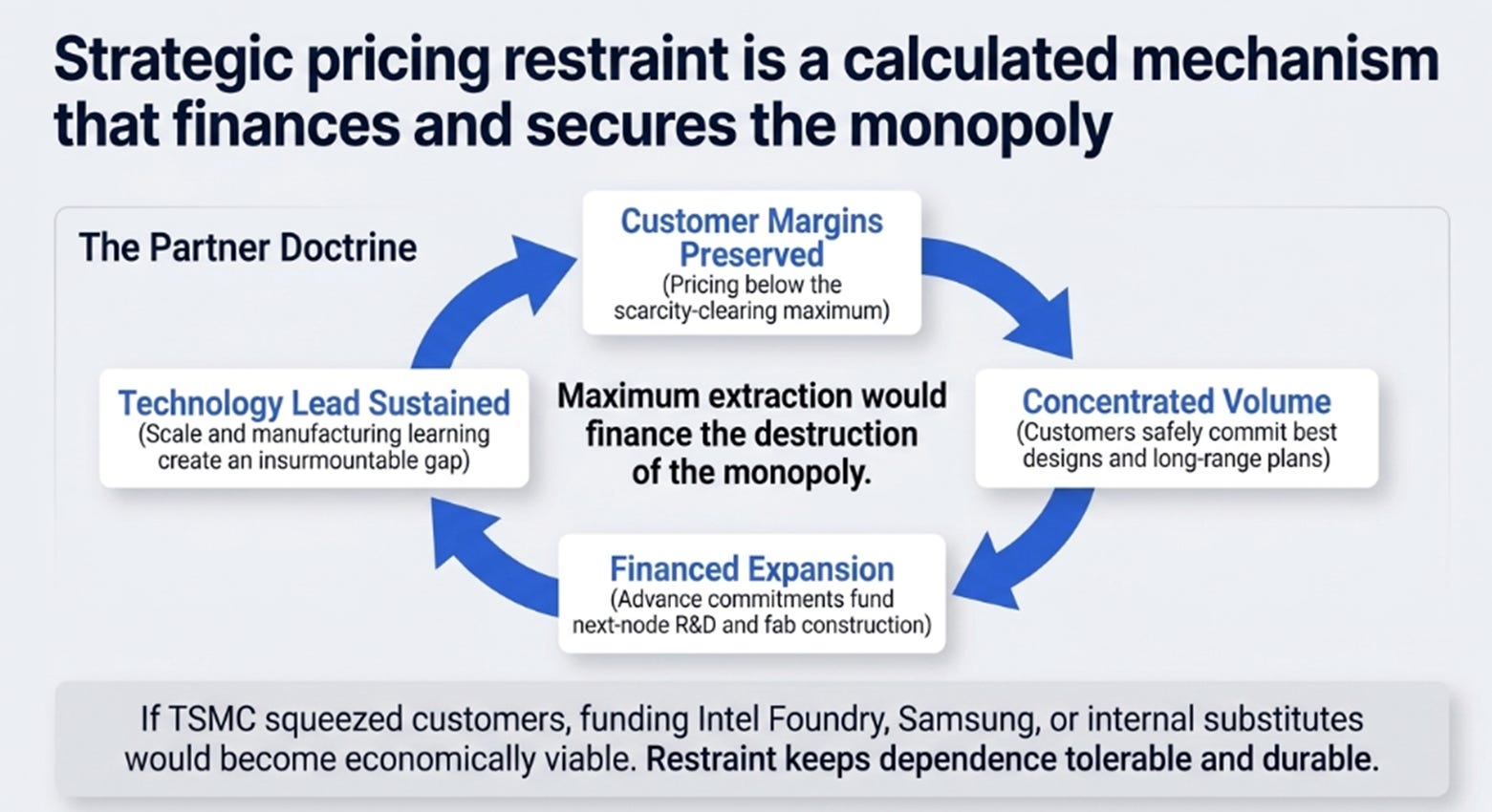

The partner doctrine is not a constraint sitting beside the moat. It helps create the moat.

TSMC’s technology lead is real, but it must be re-earned at every process generation. Leadership is a treadmill, not a fortress. What makes the treadmill durable is that customers continue funding it through concentrated volume, advance commitments, and long-range capacity planning.

Customers make those commitments because dependence on TSMC is economically safe: predictable pricing, no opportunistic squeeze during shortage, and no direct competition from the foundry itself.

If TSMC charged the full scarcity-clearing price, the calculation would change. Funding Samsung, Intel Foundry, Rapidus, or alternative packaging architectures would become more attractive. Customers would accelerate internal substitutes. Governments would have stronger reasons to intervene. Maximum extraction would help finance the destruction of the monopoly.

TSMC therefore prices below the level that would make alternatives economically compelling.

This resembles Amazon’s old “your margin is my opportunity” logic in reverse. Amazon kept its own margins thin to make competitive entry unattractive. TSMC preserves customer margins to prevent customers from funding competitors.

The chain is straightforward. Customers retain attractive economics, so they concentrate their best designs and capacity commitments at TSMC. Those commitments finance the next node and fab. Scale and manufacturing learning sustain the technology lead, which reinforces the next round of customer commitment.

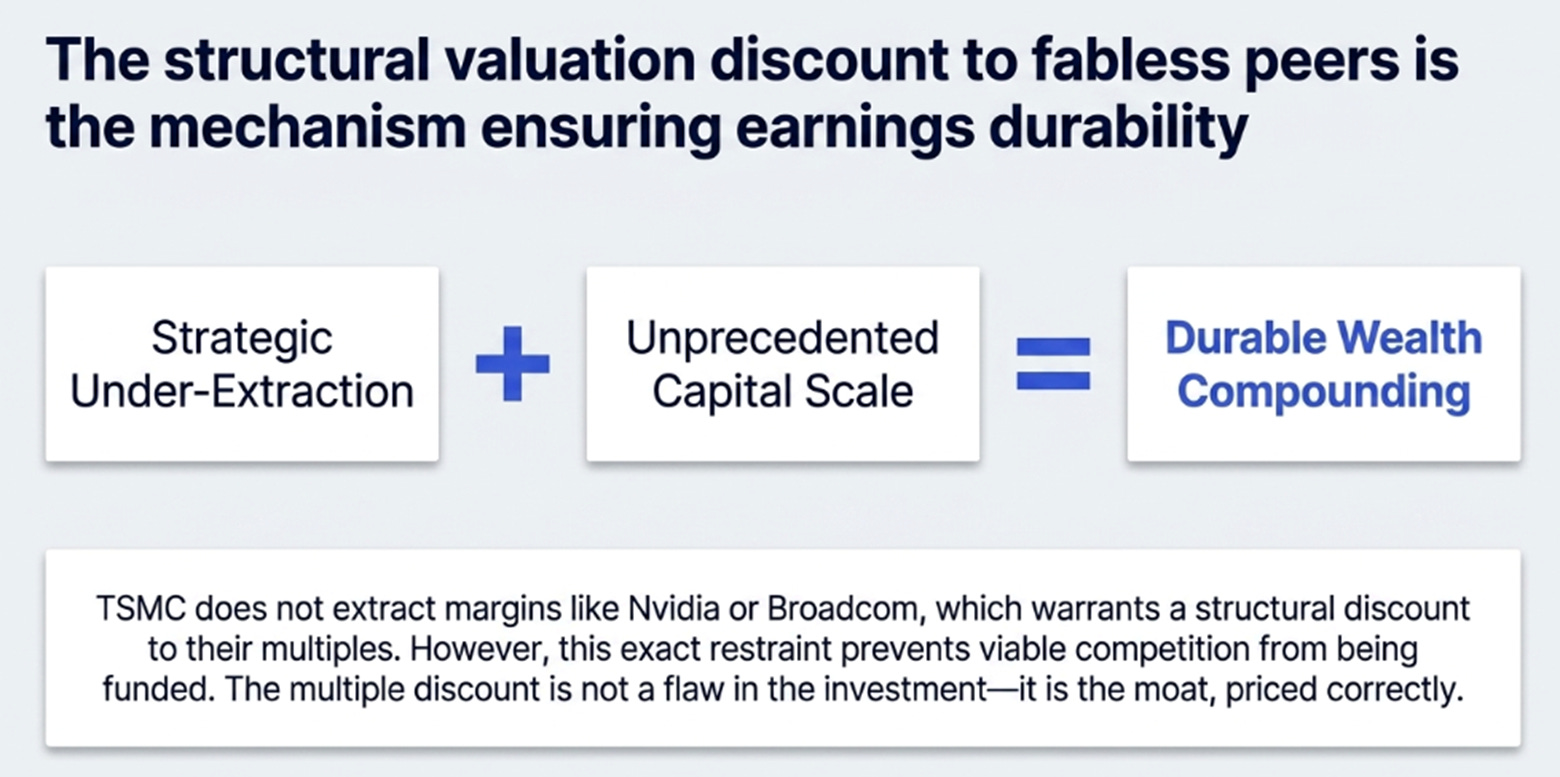

Under-extraction is not generosity. It is how TSMC keeps dependence tolerable enough to remain durable.

That is why the structural discount to Nvidia or Broadcom is not necessarily a flaw in the investment. TSMC does not extract like those companies, but its restraint may make the earnings stream more durable.

The discount may be the moat, priced correctly.

The Market Expands, but Margins Do Not Need To

The most important strategic disclosure in the call concerned agentic AI.

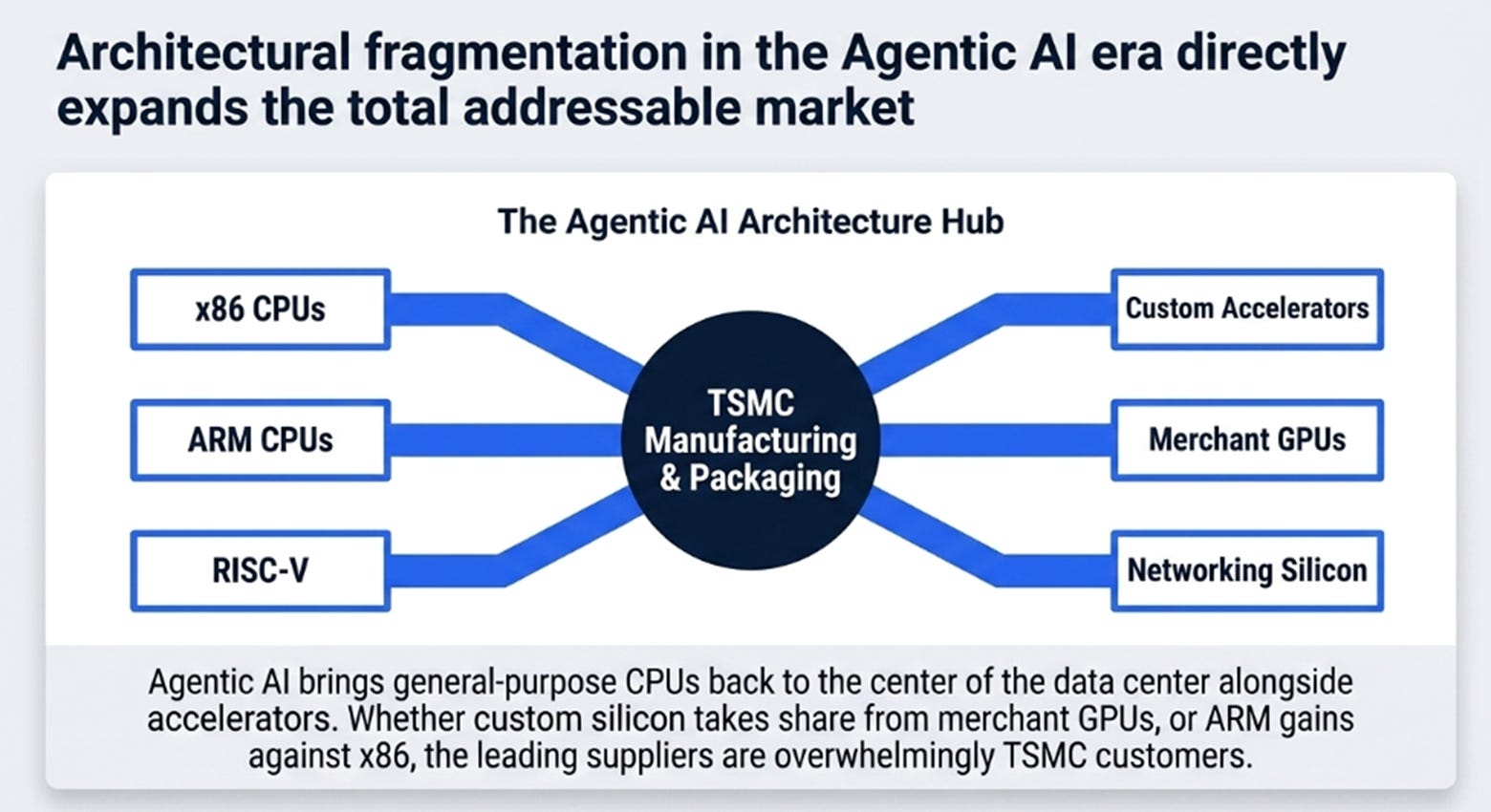

The first phase of generative AI was dominated by accelerators. Agentic AI broadens the architecture. An agent must retrieve information, manage memory, call tools, orchestrate workflows, and interact with conventional software. Accelerators remain essential, but general-purpose computing becomes more important alongside them.

That brings the CPU back toward the centre of the data centre.

TSMC’s position is unusually resilient because nearly every relevant architecture runs through its factories. Whether customers choose x86, ARM, or RISC-V CPUs, the leading suppliers are overwhelmingly TSMC customers. The same is true for most GPUs and custom accelerators.

The relevant product is no longer one accelerator. It is the compute system: general-purpose processors, specialised accelerators, networking silicon, and the packaging required to connect them.

Architectural competition can therefore hurt individual chip companies while benefiting TSMC. Custom silicon may take share from merchant GPUs; ARM may gain against x86. None of those shifts necessarily removes TSMC from the system. Fragmentation may increase the number of specialised chips requiring advanced manufacturing.

This broader opportunity does not require gross margins to rise indefinitely.

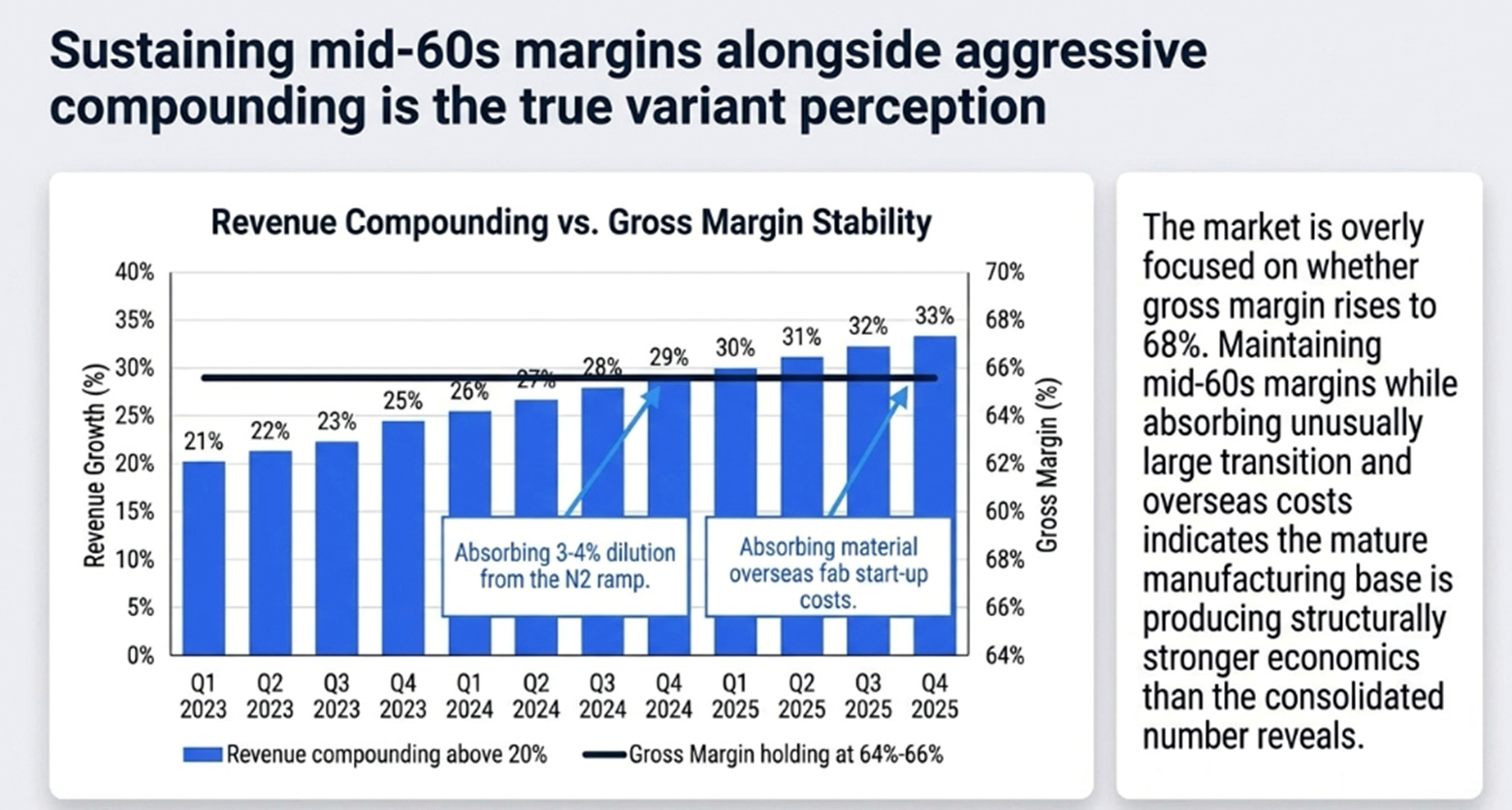

TSMC guided third-quarter gross margin to 66% at the midpoint, while expecting the N2 ramp to dilute second-half gross margin by three to four percentage points. Overseas-fab dilution remains another material headwind.

It would be simplistic to add those costs back and declare that TSMC’s “true” gross margin is 70%. New-node start-up costs are a recurring part of the business. Still, maintaining reported margins in the mid-60s while absorbing unusually large transition costs suggests that the mature manufacturing base is producing stronger economics than the consolidated number reveals.

The variant perception is not that margins must expand forever. It is that the market is too focused on whether gross margin rises from 66% to 68%, when the more important question is whether TSMC can hold the mid-60s while revenue compounds above 20%.

If it can, the earnings base—not the margin percentage—is being underestimated.

Three Paths from Here

The previous article argued that TSMC deserves something closer to an ASML-like multiple than a Nvidia-like one. That remains the right framework.

The update is not that the structural discount disappears. It is that the earnings trajectory beneath that multiple is now materially larger.

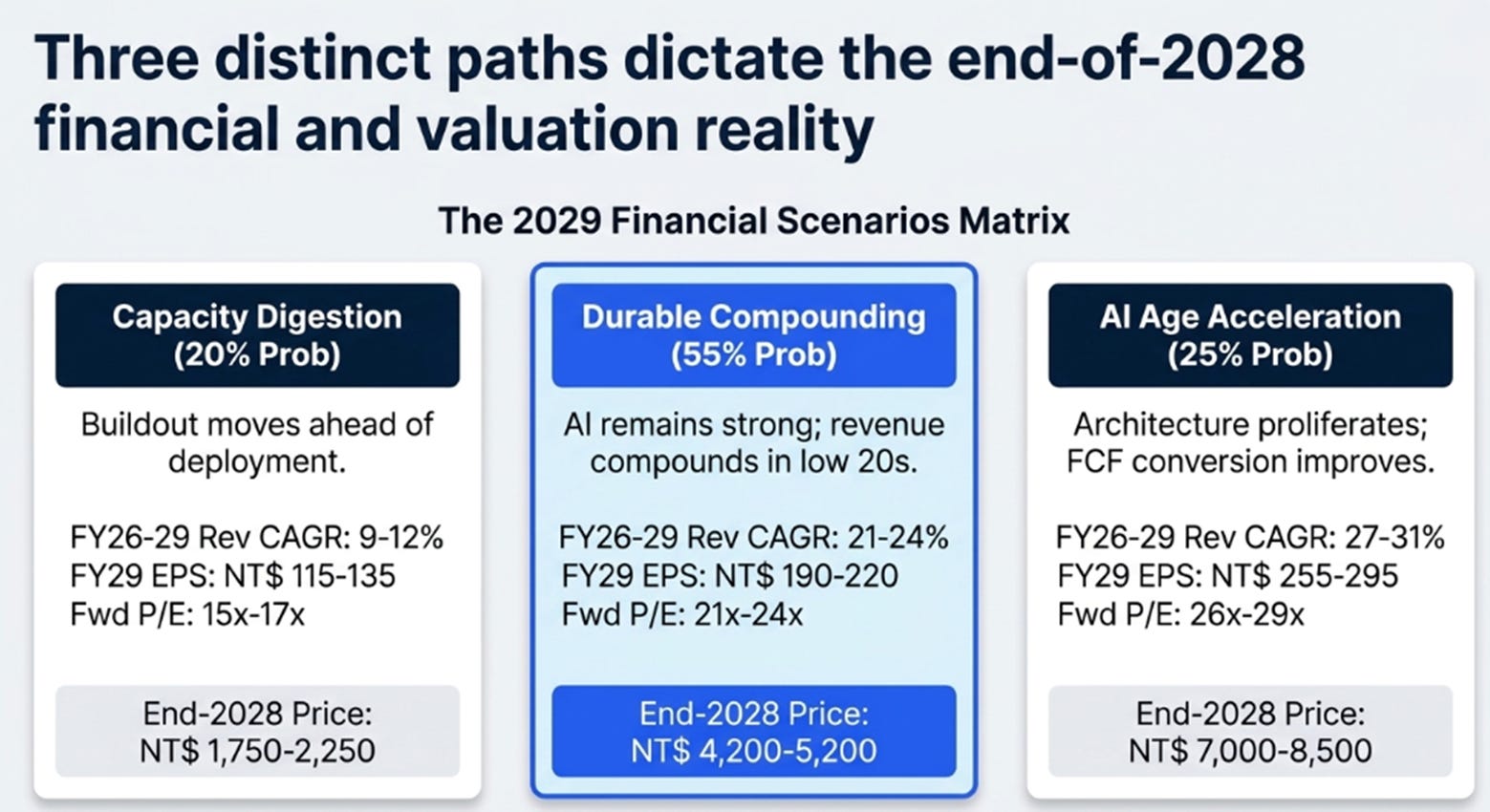

The scenario date below is the end of 2028, valued on forward FY2029 earnings.

Central values of approximately NT$1,950, NT$4,700, and NT$7,700 are reasonable representations of those outcomes from a current price around NT$2,470.

Capacity Digestion does not require AI to disappear or TSMC to lose its technology lead. It requires the current buildout to move ahead of deployment. Utilisation declines, new-node and overseas costs become more visible, and the market removes the AI-infrastructure multiple.

Durable Compounding assumes AI remains structurally strong, but TSMC continues leaving economics with customers and reinvesting most of what it earns. Revenue compounds in the low 20s after 2026, gross margin stays in the mid-60s, and returns come mainly from EPS growth rather than rerating.

AI Age Acceleration assumes architecture proliferates across accelerators, CPUs, networking, sovereign AI, and physical systems. Revenue remains above 25% for longer, pricing and mix offset overseas dilution, and free-cash-flow conversion begins to improve.

What Would Change the View

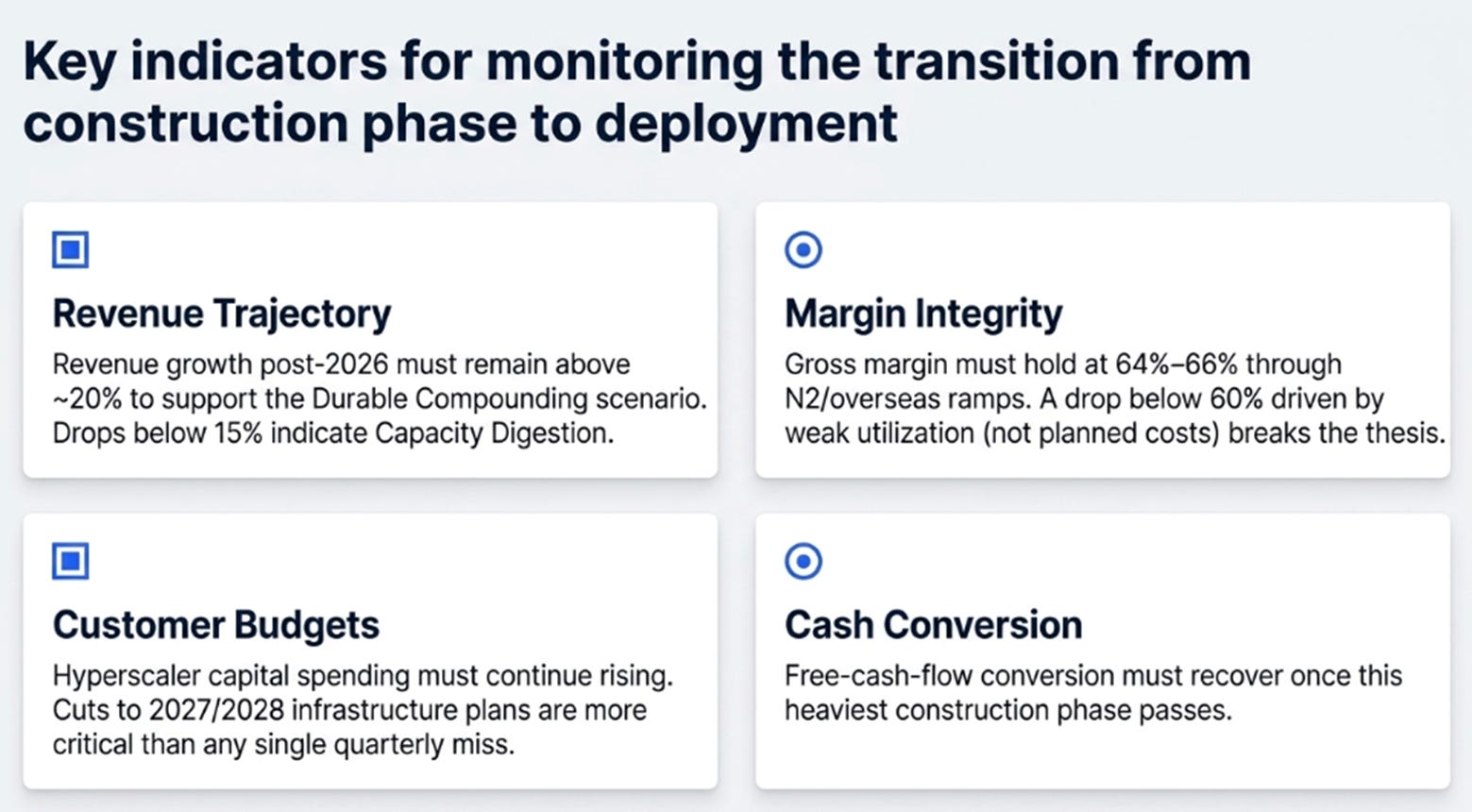

The thesis now turns on four observations.

Revenue growth after 2026 must remain above roughly 20% to support Durable Compounding. Growth above 27% suggests AI Age Acceleration; growth below 15% while capex remains elevated indicates Capacity Digestion.

Gross margin should remain around 64%–66% through the N2 and overseas ramps. A decline below 60% caused by weak utilisation, rather than planned start-up costs, would represent a material break.

Hyperscaler capital spending and customer commitments must continue rising. Cuts to 2027 or 2028 infrastructure plans would matter more than any single TSMC quarterly miss.

Finally, free-cash-flow conversion must recover once the heaviest construction phase passes. Weak conversion is acceptable while TSMC builds the system; persistent weakness accompanied by slowing revenue would show that the operating and shareholder stories are diverging too far.

Building the AI Age

Morris Chang built TSMC on the principle that capacity should follow visible demand. C.C. Wei has not abandoned that principle. He has changed the definition of visibility.

TSMC now sees product road maps, hyperscaler budgets, architecture choices, data-centre construction, and power availability years before those plans appear in reported revenue. It is spending more because the future it can see is larger than the one investor were modelling.

Last quarter, we argued that TSMC had learned to make the bottleneck travel, but that operating dominance and shareholder returns were beginning to diverge. That remains partly true. TSMC will continue to leave value with customers, invest before demand appears in financial statements, and carry the political and economic cost of building capacity across multiple countries.

What changed is our understanding of that restraint.

The partner doctrine does not merely limit what shareholders receive. It helps ensure that customers continue funding the technology, capacity, and learning that make TSMC indispensable. Under-extraction is part of how the moat renews itself.

And the opportunity on the other side of that restraint is larger than we previously assumed.

TSMC is no longer merely exporting scarcity. It is building the production system for a new computing era. The system is growing quickly enough that the company may not need to extract every dollar of value—or trade at every AI company’s multiple—to create extraordinary returns.

The risk remains that everyone’s ambitions prove collectively larger than reality. For now, the evidence suggests that the future is arriving faster than TSMC can build it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.