TL;DR:

V28 broke UnitedHealth’s old coding-driven profit engine, but Q2 suggests the infrastructure beneath it, claims, care delivery, pharmacy, workflows and data still has real operating value.

The recovery is partly restructuring, but falling hospitalizations, better care transitions and higher clinician capacity indicate UnitedHealth is improving actual healthcare delivery, not merely pruning unprofitable contracts.

The base case is now a durable integrated operator, not a return to the old premium compounder; the bull case requires Optum Insight to prove these internal capabilities can scale into an external healthcare workflow platform.

There is a particular danger in correctly identifying why a business has broken. The explanation can be so satisfying—so neatly aligned with the numbers—that it becomes tempting to assume it explains the whole company. When regulation eliminates an arbitrage and margins collapse, the obvious conclusion is that the arbitrage was the business; sometimes that is precisely right, as adtech discovered when privacy rules constrained surveillance, or investment banks discovered when regulation constrained leverage. But there is another possibility: the infrastructure assembled to exploit the old opportunity may be adaptable to a different problem, even if the original source of excess returns is gone for good.

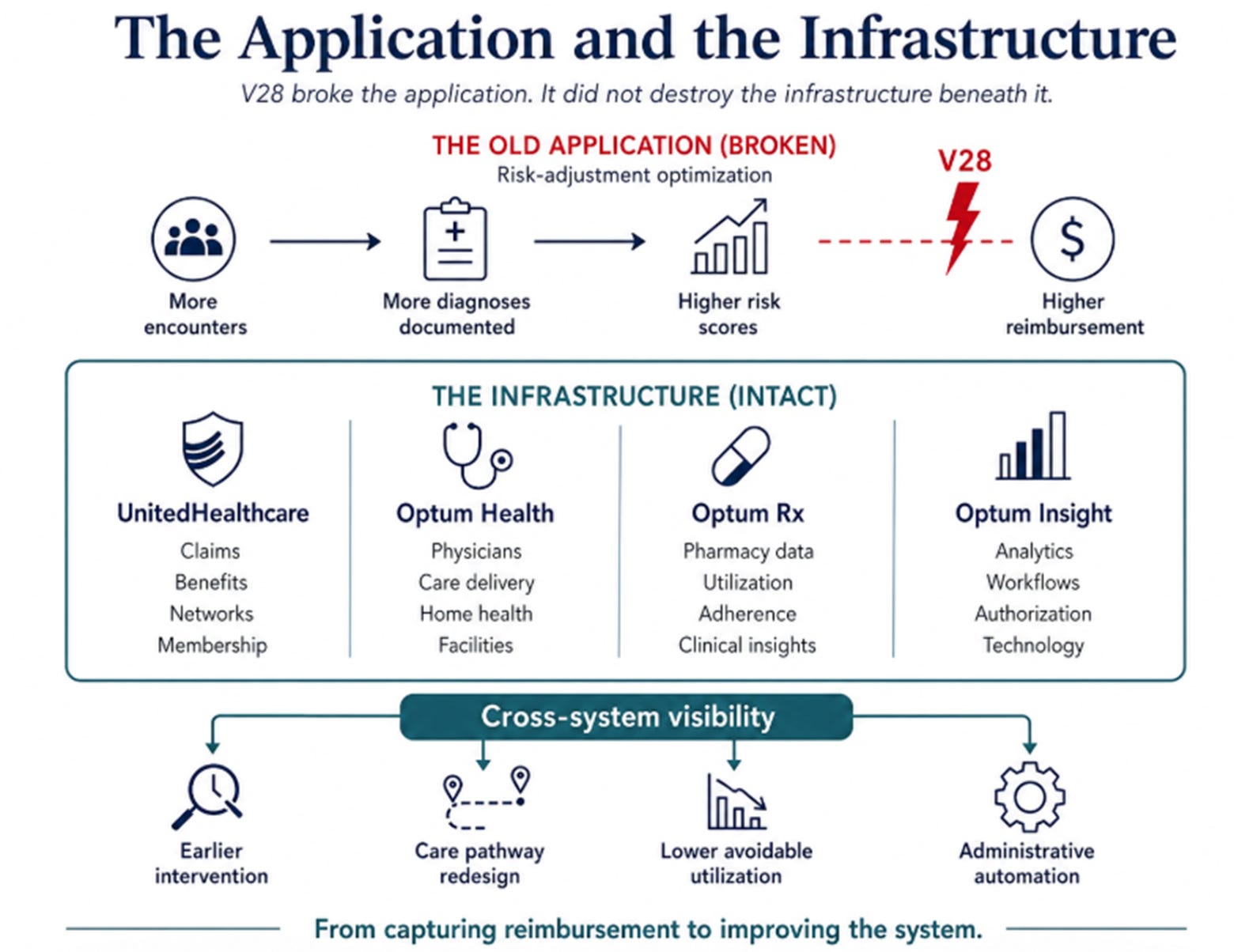

That was the possibility we underestimated with UnitedHealth. Our earlier work correctly identified Medicare risk-adjustment optimization as an important part of the company’s historical advantage. UnitedHealthcare supplied the members, Optum Health supplied additional clinical encounters, Optum Rx supplied prescription data, and Optum Insight supplied the tools that turned all of this activity into more complete diagnostic documentation and, ultimately, higher reimbursement. V28 weakened that loop, Optum Health’s margins collapsed, and management began describing contracts as structurally unprofitable. We concluded that the celebrated integrated model had been exposed as a coding machine and that UnitedHealth’s destination was a lower-growth, utility-like business.

That conclusion now looks too simple. UnitedHealth’s second-quarter results do not restore the coding economics that V28 eliminated, nor do they suggest that the old Optum Health margin structure is about to return. What they do suggest is that we mistook the most profitable application running on UnitedHealth’s infrastructure for the infrastructure itself.

The Application and the Infrastructure

The old mechanism was straightforward. More members generated more clinical encounters and more data; more data enabled more complete documentation; more complete documentation produced higher risk-adjusted reimbursement; higher reimbursement funded further expansion. The loop compounded because UnitedHealth was better positioned than competitors to observe diagnostic complexity across insurance, care delivery, pharmacy, and analytics.

V28 permanently weakened that loop. That part of the thesis has not changed. The old profit pool was not simply waiting for medical costs to normalize or for management to execute better. A regulatory change altered the economics of the system itself.

The analytical mistake was assuming that because coding optimization was a highly profitable use of the infrastructure, it was the only valuable use of the infrastructure.

The first quarter began to challenge that assumption. Optum Health returned to a margin above 5%, clinical reviews increased, skilled-nursing admissions declined, and patient-facing capacity improved. At the time, we argued that perhaps the coding API had been running on top of something more durable: a set of operational capabilities spanning claims, care delivery, scheduling, pharmacy, authorization, and provider workflow.

The second quarter gives that possibility more substance. UnitedHealthcare’s operating margin improved from 2.4% to 4.6%. Optum Health generated $1.2 billion of operating earnings at a 5.1% margin despite revenue falling 5% and the business serving roughly 700,000 fewer value-based-care patients. The reported medical care ratio fell to 86.7%, while full-year adjusted earnings guidance rose to $19.50–20.00 per share.

The headline medical care ratio was helped by $860 million of favorable reserve development, and it would be a mistake to ignore that. Adding the full amount back produces a rough normalized ratio near 87.6%, meaning the reserve benefit made the quarter look exceptional, but did not make a weak quarter look strong. Even on that crude adjustment, underwriting performance remained materially better than expectations.

More important than the financial result were the operating disclosures. Management said hospitalizations had fallen about 10% in selected regions after new transitions-of-care programs were implemented. Home-health initiatives improved timely care delivery by more than 20% while reducing acute utilization and shortening skilled-nursing stays. Patient-facing capacity expanded by roughly 200,000 hours, patient experience improved, and AI-supported clinical documentation reached 70% of employed providers.

These are not documentation outcomes. They are care-delivery and workflow outcomes.

That distinction matters because it changes what Q2 proves. The quarter does not prove that UnitedHealth has already built a new moat. It does establish that there is genuine operating capability underneath the coding advantage that once dominated the company’s economics.

Triage, Learning, and the Harder Problem

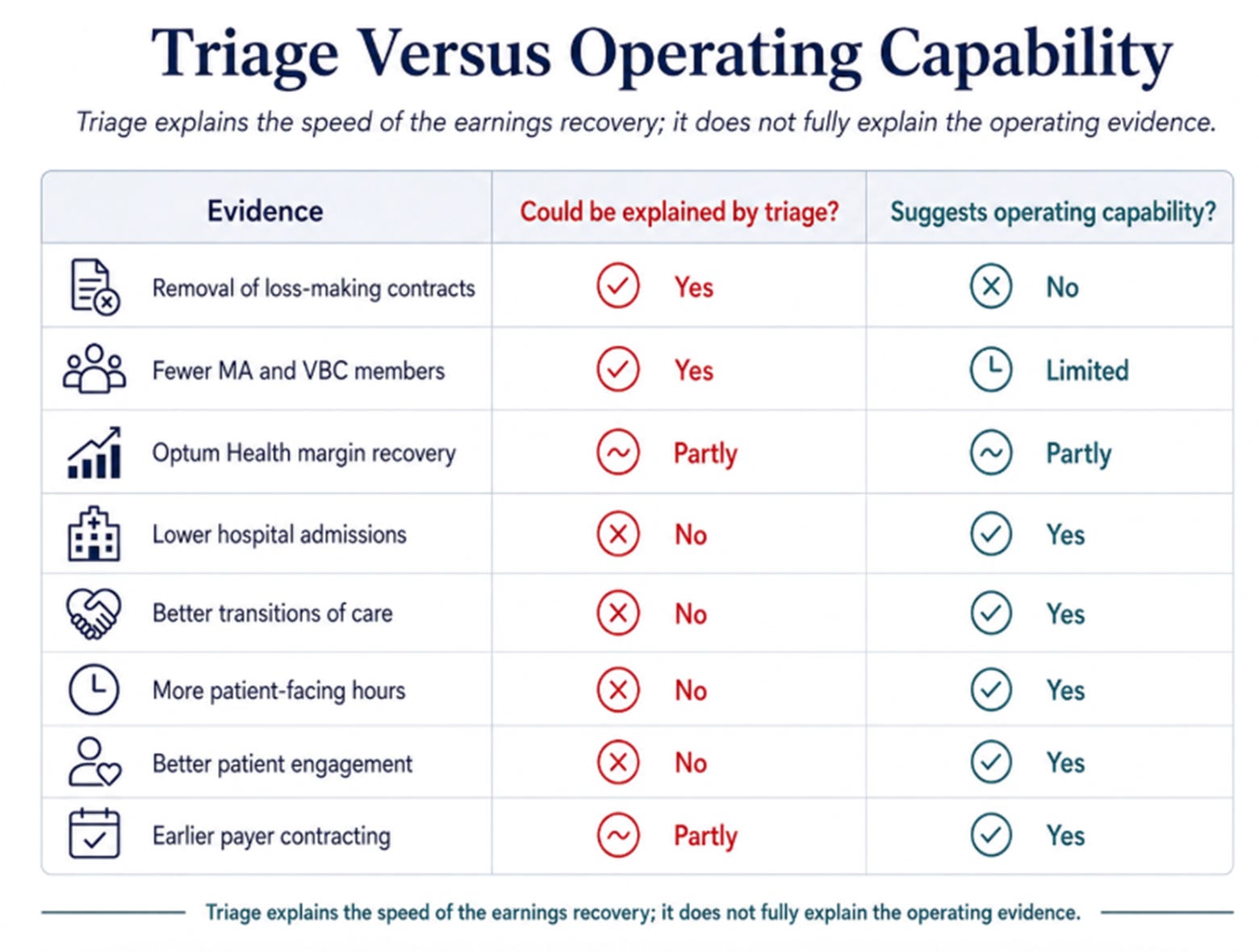

There is an obvious skeptical response: UnitedHealth did not produce this recovery while keeping the old portfolio intact. It shed risk members, narrowed affiliated networks, closed or sold hundreds of locations, exited poorly priced plans, reduced benefit generosity, and reserved against contracts it could not make profitable. Any competent management team should improve margins after removing its worst businesses.

A move from losses to 5% margins after aggressive restructuring may therefore demonstrate effective triage rather than a durable competitive advantage. That distinction is critical because triage is finite. Once the worst contracts and markets are removed, further improvement must come from better operations or renewed growth. Cutting away mistakes cannot compound indefinitely.

Much of the recovery is plainly attributable to this pruning. Yet triage alone does not explain why hospital admissions declined, why home-health transitions improved, or why clinicians gained additional patient-facing capacity. Those outcomes do not prove a new moat, but they suggest that the system left behind is capable of more than merely earning higher margins because its worst pieces were removed.

The deeper question is whether UnitedHealth can convert integration into a learning system.

The old loop used integration to capture more reimbursement. The emerging loop would use integration to reduce cost and friction: more claims, prescriptions, clinical interactions, and authorization activity create broader visibility; broader visibility enables earlier intervention and better workflow design; better workflows reduce unnecessary utilization and administrative expense; improved economics fund more technology and deeper integration.

This new loop is harder to build because it requires genuine operational improvement rather than regulatory optimization. It may also be more durable because its value does not depend on one reimbursement formula.

The surrounding environment makes that capability more valuable than it was before. UnitedHealth repeatedly emphasized that medical-cost trends remain well above historical levels. Medicare trends are below its deliberately conservative assumptions, but management explicitly rejected the idea that utilization has normalized and said its 2027 bids assume elevated underlying trends persist.

When medical costs were easier to manage, a competent standalone insurer could still produce acceptable economics; UnitedHealth’s most visible advantage came from navigating complexity better than peers. In a world of persistently elevated utilization, specialty-drug spending, provider intensity, and administrative friction, the ability to alter actual care pathways becomes more valuable.

The same environment that destroyed UnitedHealth’s first advantage may therefore have increased the value of its second.

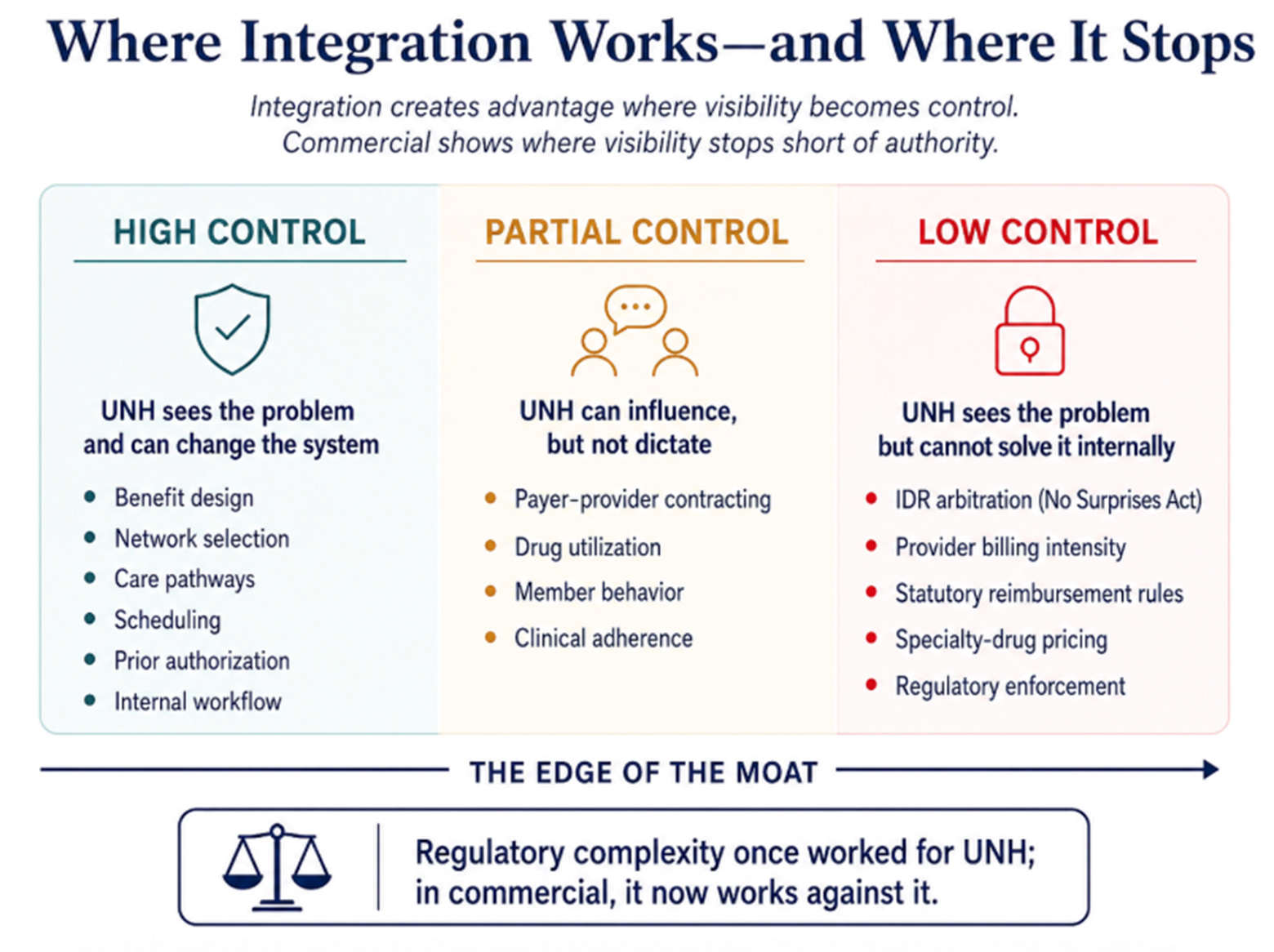

The limitation is that visibility is not the same as control. Commercial insurance illustrates the boundary clearly. Medical-cost trends are running modestly above 11%, driven by specialty drugs, provider coding and service intensity, and the Independent Dispute Resolution process created by the No Surprises Act. Management said IDR now contributes at least 100 basis points of commercial trend; around 60% of arbitration cases come from five entities, and awards when out-of-network providers prevail average roughly eleven times Medicare reimbursement.

The irony is precise: UnitedHealth once earned excess returns by navigating regulatory complexity in Medicare and is now being harmed by others exploiting regulatory complexity in commercial insurance.

More importantly, management has no obvious internal solution. Where UnitedHealth controls the levers—benefit design, networks, care delivery, scheduling, authorization, and clinical workflow—it can improve economics. Where the problem is created by external providers, drug prices, arbitration rules, or regulation, it may diagnose the pressure earlier without being able to solve it.

That is why commercial margin recovery has now moved beyond 2027. The company can fix the risks it owns; commercial will test whether it can manage the risks it merely intermediates.

What Kind of Company Is Emerging?

The post-V28 thesis can be understood in three layers.

The first is visibility. UnitedHealth sees a patient across claims, physician encounters, prescriptions, authorizations, and administrative workflows.

The second is control. It can alter benefits, networks, care pathways, scheduling, and internal processes in response to what it sees.

The third is monetization. It can retain those gains internally or sell the tools externally through Optum Insight.

Q2 provided meaningful evidence for the first two layers and only early evidence for the third.

UnitedHealth is using AI to summarize clinical cases, automate complex claims, improve scheduling, support real-time underwriting, and process prior authorizations. Its digital authorization tools are achieving 96% first-pass approval rates, while externally deployed products have processed roughly half a million authorizations and saved an estimated 69,000 administrative hours.

That is real traction. It is not yet a new business model.

Optum Insight revenue grew only modestly, some of the quarter’s strength reflected client activity moving forward from the second half, and management did not raise its outlook in a way that suggests external software demand has reached an inflection. There is also a strategic tension that should not be dismissed: many natural customers for Optum Insight compete with UnitedHealthcare. The more deeply those tools connect to customer data and workflows, the more those customers may worry about empowering a rival.

Until Optum Insight proves that external customers will adopt those tools at scale, UnitedHealth is best understood as an increasingly capable integrated operator rather than a healthcare platform.

That creates three possible destinations:

The bear case requires no renewed collapse. It only requires that the current improvement prove mainly a restructuring achievement. Optum Health stabilizes at modest margins, commercial remains pressured, and Optum Insight remains internal infrastructure.

The base case assumes integration becomes a durable internal advantage. UnitedHealth manages medical and administrative costs better, restores margins, and returns to mid-single-digit growth. It becomes better than a utility, but not the premium compounder of the coding era.

The bull case requires external proof. Optum Insight must grow materially faster, win named third-party customers and demonstrate that tools developed inside UnitedHealth can become products used across the healthcare system. The bull case is not the return of the old model; it is the emergence of a different one.

The next phase of the thesis will therefore be determined by what happens after the easy restructuring gains are exhausted. Optum Health must sustain acceptable economics and eventually grow again without recreating the same risk-selection problem. Optum Insight growth must move toward 8%, supported by named external wins rather than pipeline commentary. The normalized medical care ratio must remain below roughly 88%, while commercial trend must stabilize before it becomes a permanent constraint on group margins.

Most importantly, management’s claim that $19.50–20.00 is the base for renewed 13–16% earnings growth must eventually appear in reported results rather than confident language.

We correctly identified that V28 destroyed the profit mechanism that had made UnitedHealth exceptional. We incorrectly assumed that the mechanism was the whole company.

Q2 does not prove that the layer beneath is a new moat. It does show that it is more than wreckage. And in a healthcare system where controlling costs is becoming harder, that distinction may matter more than the coding advantage ever did.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.