UnitedHealth 1Q FY26: The Mean Moved Less Than We Thought

The old moat is gone. A new one is forming, if integration is becoming an operating system rather than a coding engine.

TL;DR

The break was real, but so was the recovery. We were right that V28 permanently impaired the old Optum model, yet 1Q26 showed enough operational improvement to suggest there was something real underneath the coding layer.

The real debate has changed. This is no longer about whether UNH can stabilize earnings; it is about whether Optum can become the operating-system layer for healthcare workflows, monetizing software, automation, and process control.

The key swing factor is Optum Insight. If external workflow/software revenue inflects meaningfully by late 2026, the stock can rerate higher; if not, UNH is probably just a recovering insurer with a lower long-term ceiling.

“UnitedHealth Group reported first quarter profit that blew past Wall Street expectations... Adjusted earnings were $7.23 a share, above the highest analyst estimate.”, Bloomberg, April 21, 2026

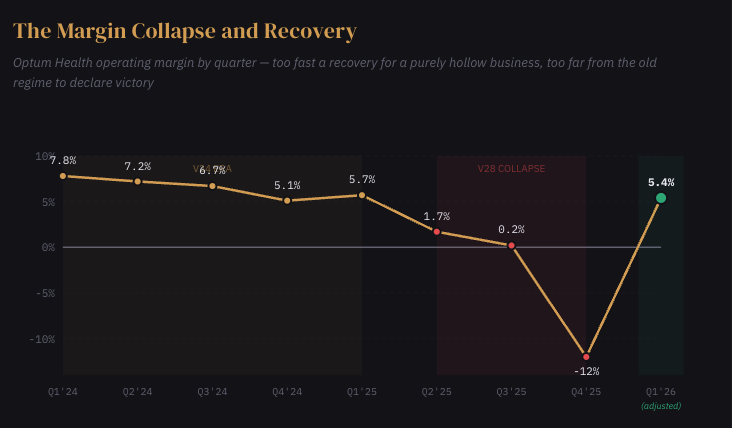

In January, after UnitedHealth posted its first annual revenue decline since 1989, we argued this was IBM 2011. The company’s celebrated integration wasn’t primarily about care delivery, it was about coding optimization. Optum had been built to maximize Medicare risk adjustment payments through comprehensive diagnostic documentation, and when CMS simplified the rules under V28, the margins that documentation produced evaporated. Optum Health went from 8.3% margins to an operating loss. Management reserved $623 million against contracts it described as “structurally unprofitable.” The cohort curve we flagged, negative margins in years one and two, 8% by year five, looked less like care management learning and more like the time required to complete a patient’s diagnostic profile.

We were right about the mechanism. The coding arbitrage is dead. V28 is permanent. The 20x multiple is not coming back. That part of the thesis stands entirely.

Where we need to update is the destination. We argued UnitedHealth was becoming a utility. Q1 suggests something more interesting might be happening, and the difference between “utility” and “something more interesting” is worth roughly $150 of stock price.

What the Old Thesis Missed

The most useful way to understand V28 is not as a regulatory event but as an architectural one. For two decades, Optum ran on a specific API: CMS’s V24 risk adjustment model, which paid more for diagnostic complexity. Every nurse practitioner home visit, every pharmacy data cross-reference, every Optum Insight coding tool was optimized for that API. When CMS deprecated it, the applications broke. Margins collapsed. That was our evidence.

But here is the question we did not adequately ask: was the API the product, or was the API running on top of something more durable?

Consider what happened in Q1. Optum Health posted $1.3 billion of adjusted operating earnings at a 5.4% margin, a recovery of more than 500 basis points from Q4 in a single quarter. If the entire business had been coding optimization in a trench coat, that speed of recovery is difficult to explain. You cannot operationally fix a segment that was structurally hollow. You can only fix one that had real capabilities buried underneath a layer of arbitrage.

The operational evidence is specific enough to take seriously. In UnitedHealth’s West region, clinical reviews increased more than 50%, and skilled nursing admissions dropped approximately 35%, in a single quarter, through what management described as data-driven clinical navigation around hospital admissions and discharge. Across the system, patient-facing hours rose 12% year over year after scheduling discipline was imposed across 70% of care settings. These are not financial engineering. They are process changes that either happened or did not, and if they happened, they suggest the integration contains genuine operational leverage independent of how CMS scores a diagnosis.

This does not mean the old thesis was wrong. It means the old thesis was incomplete. We correctly identified the layer of arbitrage. We underweighted what was beneath it.

The Operating System Question

If the coding game is dead, the question becomes what kind of company UNH is building on the remaining foundation. The sell-side answer is “a recovering insurer.” The more interesting possibility is that UnitedHealth is attempting to become the operating system layer for American healthcare administration.

That sounds grandiose, and I want to be precise about what I mean.

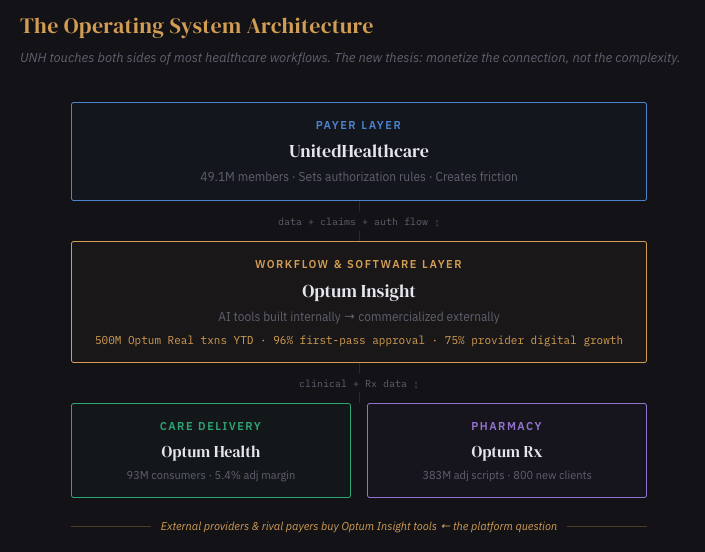

UnitedHealth occupies an unusual structural position: it touches more high-friction surfaces in healthcare than any other company. UnitedHealthcare sees the authorization demand. Optum Health sees the clinical fulfillment. Optum Rx sees the prescription. Optum Insight builds the software connecting all three. No other company has this degree of asymmetric visibility across both sides of the core healthcare workflows, claims, prior authorization, care navigation, scheduling, provider engagement, member experience.

In the old regime, that visibility was monetized through coding. In the new regime, it could be monetized through workflow standardization and software.

Listen to what Sandeep Dadlani described on the call: $1.5 billion of AI investment, one-third flowing into external Optum Insight products, two-thirds into internal process reengineering, routed through Optum Insight for potential commercialization. Optum Real, an AI-first platform, processed 500 million transactions year-to-date and expects 2.5 billion by year end. Digital Auth Complete achieved 96% first-submission approval rates with early payer and provider clients and over 50 in the pipeline. Meanwhile, 95% of prior authorizations are now electronic, 50% processed in real time, and provider digital transactions grew 75% year over year.

The pattern is familiar. Amazon built AWS to solve its own infrastructure chaos, then discovered it could sell that infrastructure to everyone else. UnitedHealth built workflow tools to manage its own administrative friction, and is now beginning to sell those tools to providers and rival payers who face the same friction but lack the data or scale to build their own solutions.

Critically, this is not the same thing as the old arbitrage. Selling workflow software to hospitals that need to get their claims approved is fundamentally different from gaming diagnostic codes for higher reimbursement. The first creates value for both sides of the transaction. The second extracted value from regulatory complexity. That distinction matters for durability, and it matters for whether regulators will eventually come after the new model the way they came after the old one.

I want to be honest about where this thesis stands: it is plausible, not proven. Optum Insight revenue grew only 2% year over year with declining operating earnings. The internal operating improvements are ahead of the external monetization. If Optum Insight does not inflect to meaningfully higher growth by late 2026, the platform thesis is just a narrative, and UNH really is a recovering insurer with a permanently lower ceiling.

But the evidence moved. Three months ago, the probability that integration itself, not the coding game played on top of it, was a real moat sat around 30% in our framework. After Q1, closer to 55%. That is enough to change the price. It is not enough to change the multiple.

Credibility Over Precision

One aspect of the quarter deserves separate attention, because it reveals management’s strategic priorities more clearly than any operational metric.

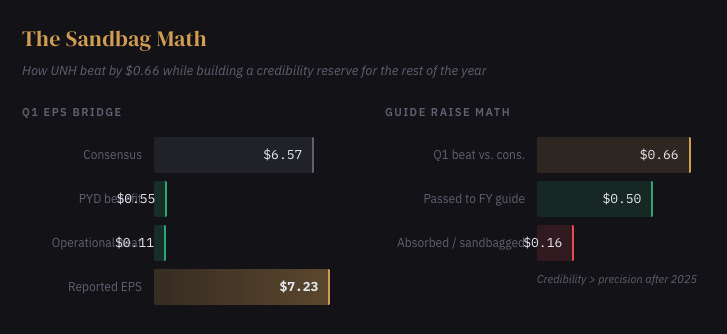

UNH beat consensus by $0.66 per share and raised the full year by only $0.50. Mathematically, that takes down the implied remainder-of-year run-rate. CFO Wayne DeVeydt confirmed approximately $500 million of favorable prior-year development, roughly $0.55 of the beat. The MCR benefited from a mild flu season. First-half earnings are guided at roughly two-thirds of the full year, with first-half MCR running “more than 250 basis points below” full-year guidance. Management also disclosed $900 million in Q1 incentive compensation against $35 million a year ago.

That is a company telling you three things simultaneously: the quarter was strong, the quarter had help, and credibility matters more right now than squeezing every cent into the guide. After the Witty-era guidance collapse, which destroyed more shareholder value than any DOJ investigation could, that is exactly the right posture. Hemsley’s playbook is clear: under-promise, over-reserve, deliver consistently, retrain the market to trust forward projections. Every quarter in 2026 is being structured to beat and raise, which means every quarter rebuilds the credibility that makes the multiple recovery possible.

Q2 is the informative quarter. If Optum Health holds above 5% adjusted margin without meaningful PYD help, the operational recovery is confirmed and the stock likely grinds toward $380-400. If it reverts to 3%, Q1 was a reserve-flattered head fake and the utility thesis reasserts.

What Consensus Misses

Consensus sees UNH as a damaged insurer recovering through better pricing and friendlier Medicare funding. Price targets cluster $370-400, implying a return toward 18-19x.

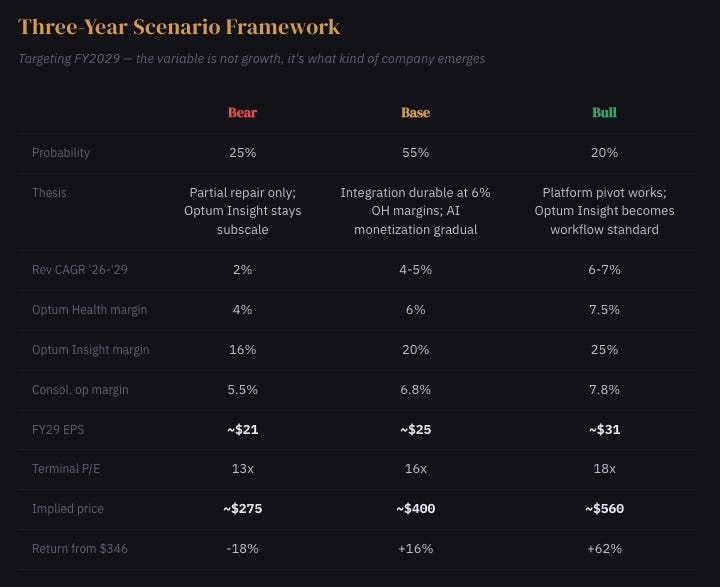

We think that framing is too shallow. The real question is not whether UNH recovers, it probably does, but what kind of company emerges from the recovery. If the workflow-and-operating-system thesis is right, the earnings that emerge are higher quality than what consensus models, because they are driven by software economics and process control rather than underwriting cycle. That supports a 16-17x multiple on genuinely better earnings. If the thesis is wrong, what emerges is a well-run but structurally diminished insurer, and 13-14x on lower earnings is the right frame.

The segment that resolves this is not Optum Health. It is Optum Insight. A segment growing 2% with declining margins is not yet evidence of a platform. A segment growing 8-10% with expanding margins would be.

Three Years From Here

The bear case is not disaster, it is partial repair that disappoints. Pricing helps but not enough. Optum Health stalls in the mid-single digits. The workflow pivot stays aspirational. The market concludes UNH is a good business, permanently less good.

What Resolves This

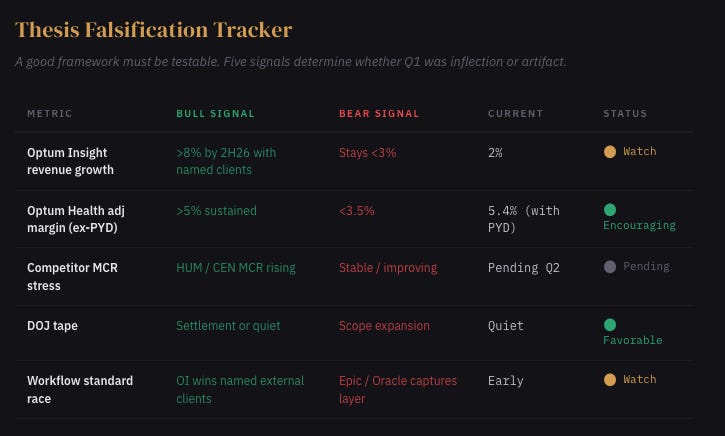

Five things determine whether Q1 was an inflection or just a good quarter.

Optum Insight revenue growth must inflect toward 8%+ by late 2026 with identifiable external customer wins, not pipeline commentary, revenue. Optum Health adjusted margin must sustain above 5% in Q2 without reserve help. Competitor earnings, Humana, Centene, CVS, must show MCR stress from absorbing the MA members UNH shed, confirming that intentional shrink was asymmetrically damaging. The DOJ tape must remain quiet; any structural-remedy signal invalidates the integration thesis entirely. And the workflow standard race matters: if Epic, Oracle Health, or a well-funded startup captures the provider operating layer before Optum Insight scales, the platform thesis dies regardless of how good UNH’s internal metrics look.

Where We Stand

When a company’s moat turns out to have been regulatory arbitrage, the instinct, ours included, is to conclude that nothing real was underneath. Sometimes that is right. GDPR revealed that much of adtech’s value was surveillance dressed as targeting. Sometimes it is not. Basel III compressed bank ROEs permanently, but JPMorgan adapted faster than competitors and compounded well from the new, lower base. Microsoft’s Windows monopoly ended, but the infrastructure Nadella inherited turned out to be deployable against an entirely different problem.

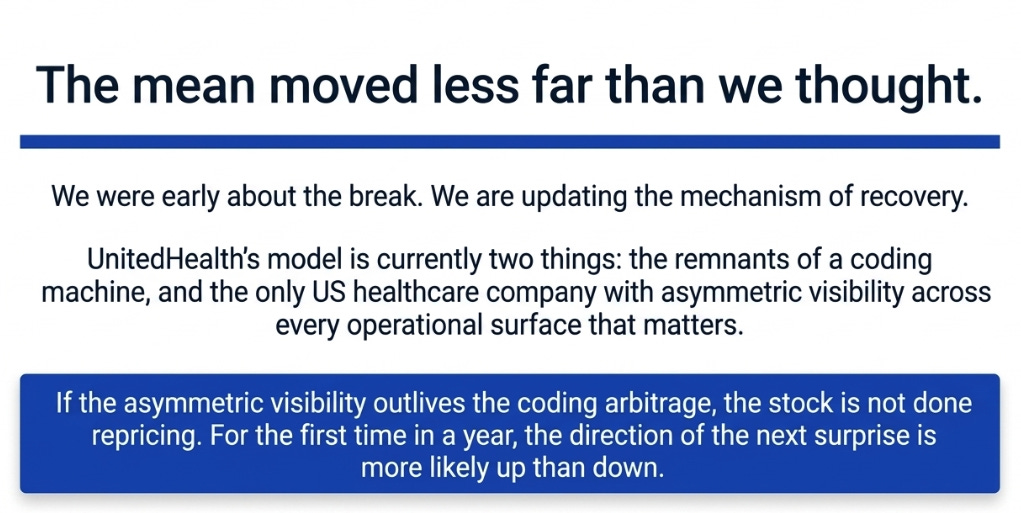

UnitedHealth’s integrated model may yet prove to have been both things: a coding optimization machine and the only American healthcare company with asymmetric visibility across nearly every operational surface that matters. If the second fact outlives the first, the stock is not done repricing. If it does not, if Optum Insight stays at 2% growth and the workflow thesis never materializes in the financials, then our January assessment was closer to the mark, and the stock eventually settles into the high $200s.

We were early about the break. We are updating the mechanism of recovery. The mean moved. It moved less far than we thought. And for the first time in a year, we think the direction of the next surprise is more likely up than down.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.