Vistra 1Q26 Earnings: Scarcity Is Not Enough

Power scarcity got Vistra noticed. Contracted cash flow is what gets it re-rated.

TL;DR:

Our original Great Energy Mismatch thesis was right, but it has matured. The market no longer needs convincing that AI needs power; it now wants proof that scarcity can become signed contracts, durable cash flow, and per-share compounding.

Q1 showed Vistra’s identity is changing. East delivered $801M of adjusted EBITDA versus $586M from Texas, while retail weakness from mild weather did not stop record Q1 EBITDA. The old ERCOT-weather lens is becoming incomplete.

The next leg depends on conversion, not narrative. Cogentrix, Meta, Helix, gas bridge power, new PPAs, hedge pricing, and buybacks are the signposts. The base case is attractive, but the stock needs signed duration to move from “AI power winner” to “AI reliability platform.”

A year ago, our argument on Vistra was not really about Vistra.

It was about the grid.

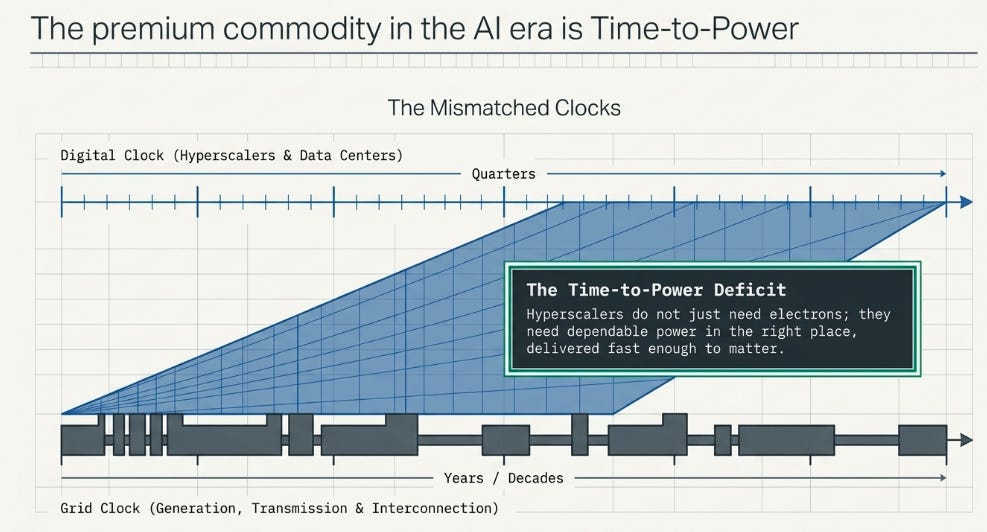

The AI boom, we argued, was creating a mismatch between two clocks. On one clock were hyperscalers, building data centers on digital timelines: quarters, not decades. On the other clock was the power system, where generation, transmission, permitting, and interconnection are still measured in years. The scarce commodity was not simply electricity. It was time-to-power — reliable, dispatchable, located power delivered fast enough to matter.

That thesis has aged well. Maybe too well.

The market no longer needs to be convinced that AI needs power. It no longer needs to be told that nuclear is scarce, that gas is useful, that transmission is slow, or that data centers are forcing a rethink of the utility model. Those ideas have moved from variant perception to consensus narrative. Vistra is no longer an undiscovered beneficiary of the Great Energy Mismatch. It is now a stock the market already knows, already debates, and in many cases already likes.

That changes the question.

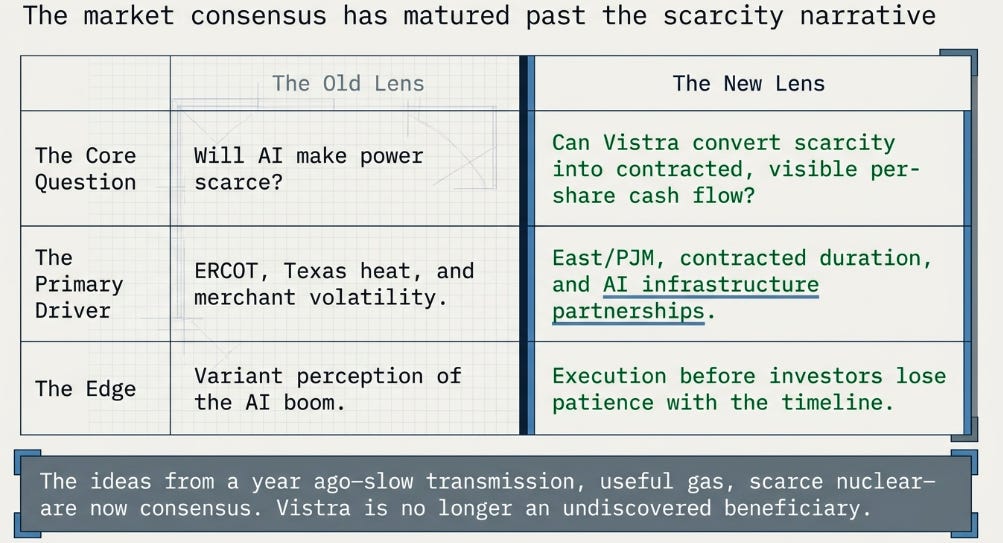

The old question was: will AI make power scarce?

The new question is: can Vistra convert that scarcity into contracted, visible, per-share cash flow before investors lose patience with the timeline?

That is the lens through which Q1 2026 should be read.

From Scarcity to Conversion

Our July framework was right about the direction of the world. AI demand was not merely adding load; it was exposing the inability of the grid to respond at digital speed. The four mismatches we highlighted — speed, scale, reliability, and location — are still the correct way to think about the problem. Hyperscalers do not just need electrons; they need dependable power in the right place, on the right timeline, with the right reliability profile.

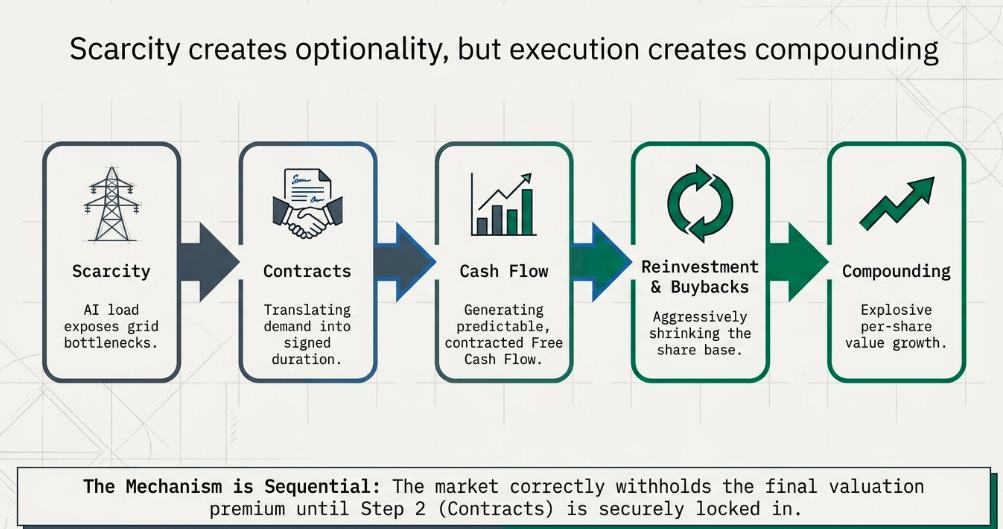

But our framework was incomplete in one important respect. Scarcity creates optionality. It does not, by itself, compound.

What compounds is conversion: scarcity into contracts, contracts into predictable free cash flow, free cash flow into buybacks and reinvestment, and buybacks into per-share growth. That mechanism is sequential. Each step requires execution. The market is right not to pay fully for the last step simply because the first step is true.

There are also things we underweighted. We grouped Vistra and Constellation too closely as beneficiaries of the same scarcity trade. We treated gas mostly as a volatility hedge, when it is now becoming a time-to-power product. And we did not fully anticipate how quickly Vistra’s earnings center of gravity would move away from the old ERCOT-only mental model.

Q1 matters because that shift is no longer theoretical.

The Inversion

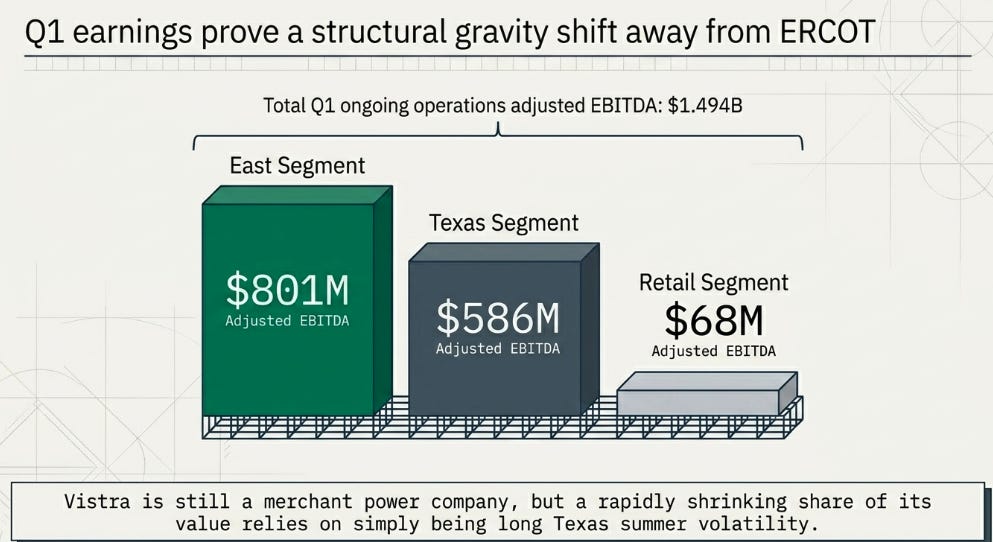

At first glance, the quarter looked straightforward. Vistra delivered $1.494 billion of ongoing operations adjusted EBITDA, up from $1.240 billion a year ago. It reaffirmed 2026 adjusted EBITDA guidance of $6.8–7.6 billion and adjusted free cash flow before growth guidance of $3.925–4.725 billion. The company also noted that the guidance range and the 2027 EBITDA opportunity exclude any potential benefits from Cogentrix and the Meta PPAs.

That is a good quarter. It is not, by itself, a thesis-changing quarter.

The more important detail was inside the segment table. Retail adjusted EBITDA fell from $184 million to $68 million, largely because Texas had an unusually mild quarter. Texas adjusted EBITDA rose from $490 million to $586 million. But East jumped from $514 million to $801 million.

For years, the simplest way to think about Vistra was through ERCOT: Texas heat, forward curves, retail margins, summer volatility. That lens is not wrong. It is just becoming incomplete. Q1 did not show that Vistra has stopped being a merchant power company. It showed that a smaller share of the value now comes from simply being long Texas weather.

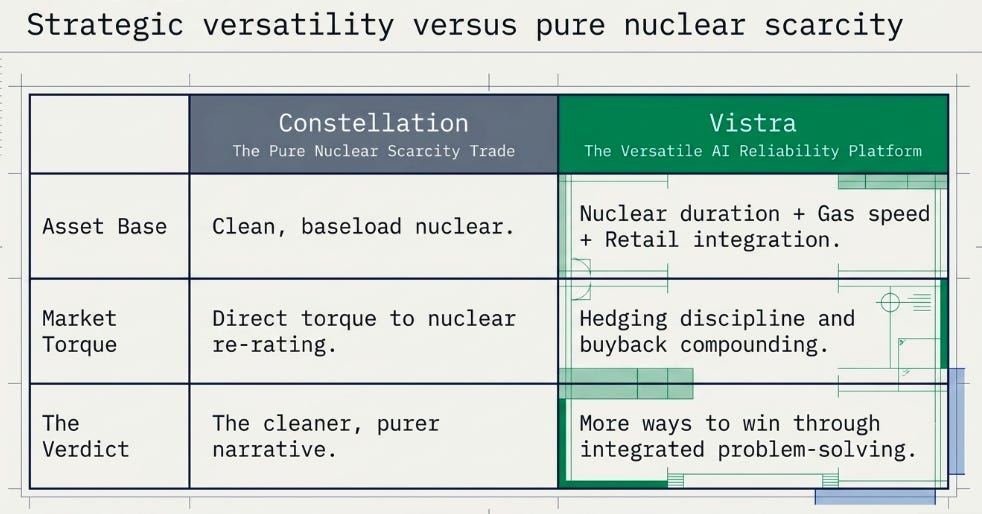

This is also where Vistra and Constellation begin to diverge. Constellation is the cleaner nuclear scarcity trade. It has more direct torque to the re-rating of nuclear assets and long-duration clean baseload contracts. Vistra is messier, but that messiness is part of the point: nuclear duration, gas speed, retail integration, hedging discipline, and buyback-driven compounding all sit inside the same company.

Constellation may be the purer story. Vistra may have more ways to win.

The East-over-Texas quarter does not complete that transformation. But it does make the old label harder to defend. The market still trades Vistra partly as an ERCOT-sensitive merchant generator. The income statement is beginning to say something else.

The Product Is Time

The most useful line from our original Vistra article was not about nuclear or gas. It was that the scarce commodity in the AI era is time-to-power.

That remains the right idea, but Q1 sharpened it.

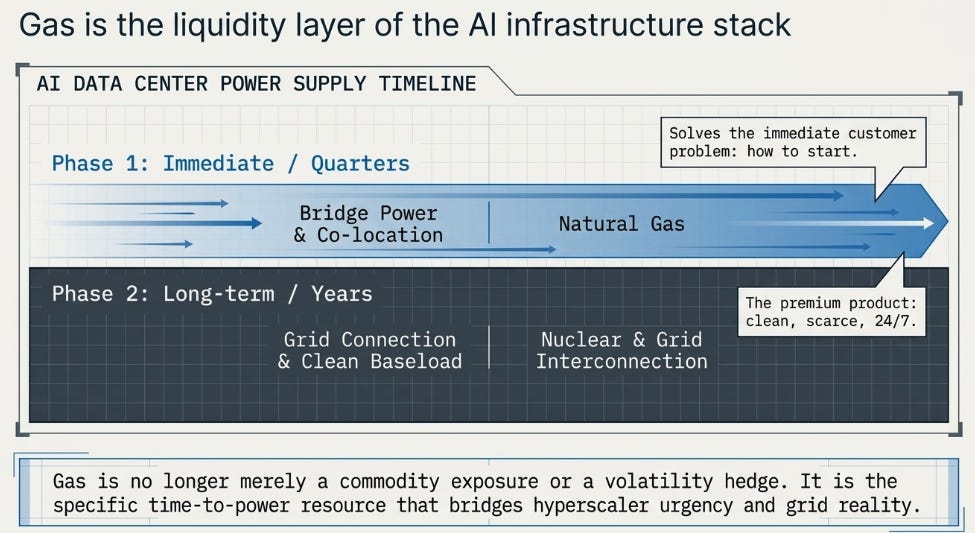

Nuclear is the premium product. It is clean, scarce, 24/7, and increasingly contractable over long durations. That is why the Meta PPAs matter and why investors naturally gravitate toward nuclear as the center of the AI-power story.

But gas solves the more immediate customer problem: how to start.

On the Q1 call, management repeatedly returned to bridge power, co-location, distributed generation, and customer flexibility. This was not an accident. Customers want grid connections, but they also want to energize projects before the full grid solution is ready. Jim Burke noted that the conversation has evolved toward bridge power, and that more of those conversations have been leaning toward gas.

That is a subtle but important update. Gas is not just a commodity exposure. In the AI infrastructure stack, gas is increasingly the liquidity layer, the resource that bridges the timing mismatch between hyperscaler urgency and grid reality.

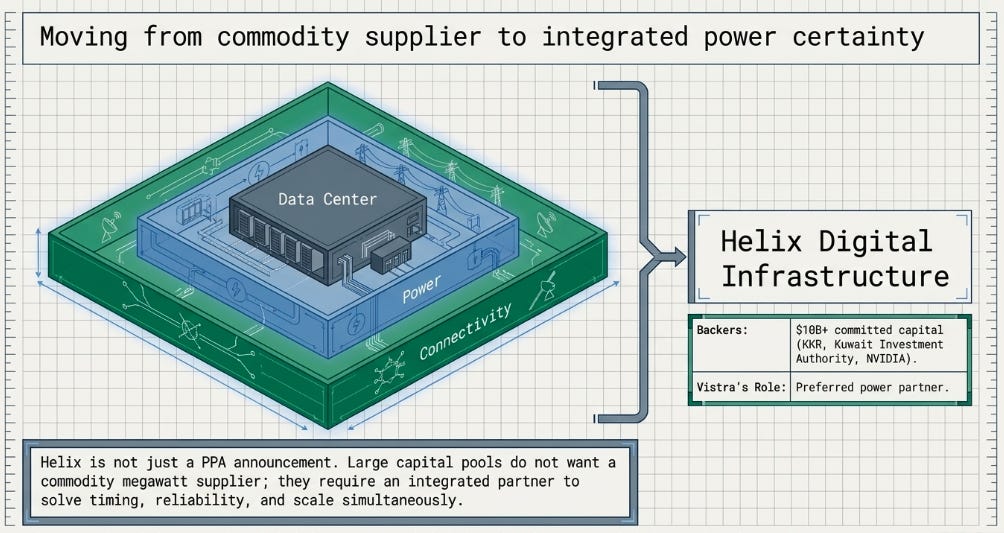

That is also why the Helix Digital Infrastructure announcement matters. KKR launched Helix with more than $10 billion of committed capital, alongside Kuwait Investment Authority, NVIDIA, and Vistra; Vistra is the preferred power partner. The point is not that Helix is already a new PPA. It is that large pools of capital and AI infrastructure partners are looking for an integrated solution to data centers, power, and connectivity. They are not looking for a commodity megawatt supplier. They are looking for a partner that can help solve timing, reliability, and scale together.

That is the strategic opening for Vistra. Not power alone. Power certainty.

The Market Is Not Wrong

The temptation after a quarter like this is to say the market does not get it. That would be too easy.

The market does get it. That is why the stock already re-rated over the last two years. That is why investor conversations around Vistra now begin with AI load, PJM, ERCOT, co-location, hyperscaler PPAs, and dispatchable scarcity. The market’s problem is not that it has missed the thesis. The market’s problem is that the thesis has moved from concept to execution.

There was no new major PPA in the quarter. Guidance was reaffirmed, not raised. Cogentrix has not yet closed. Meta is not yet in the guide. PJM rules remain complex. ERCOT forwards have been soft. Batteries have dampened volatility in some periods. Interconnection queues still include too much fiction and not enough committed load.

All that matters.

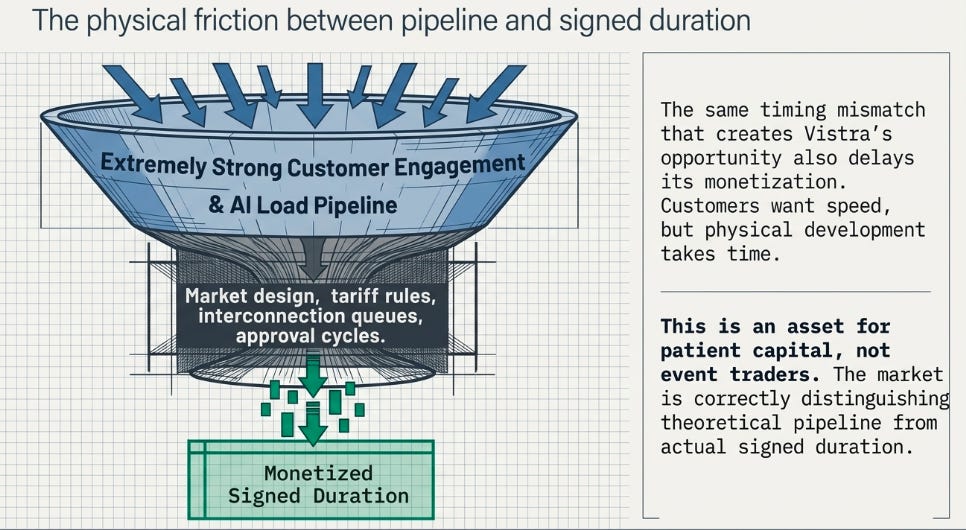

Management’s answer is that physical development takes time. That is consistent with our own original thesis. The irony is that the same timing mismatch that creates Vistra’s opportunity also delays its monetization. Customers want speed-to-power, but market design, tariff rules, interconnection processes, and approval cycles are still catching up.

The evidence suggests the pipeline is real. Management described customer engagement as extremely strong, and Helix supports the idea that Vistra is being pulled into the AI infrastructure stack. But the market is right to distinguish pipeline from signed duration.

This is a better stock for patient capital than for event traders.

The Compounding Mechanism

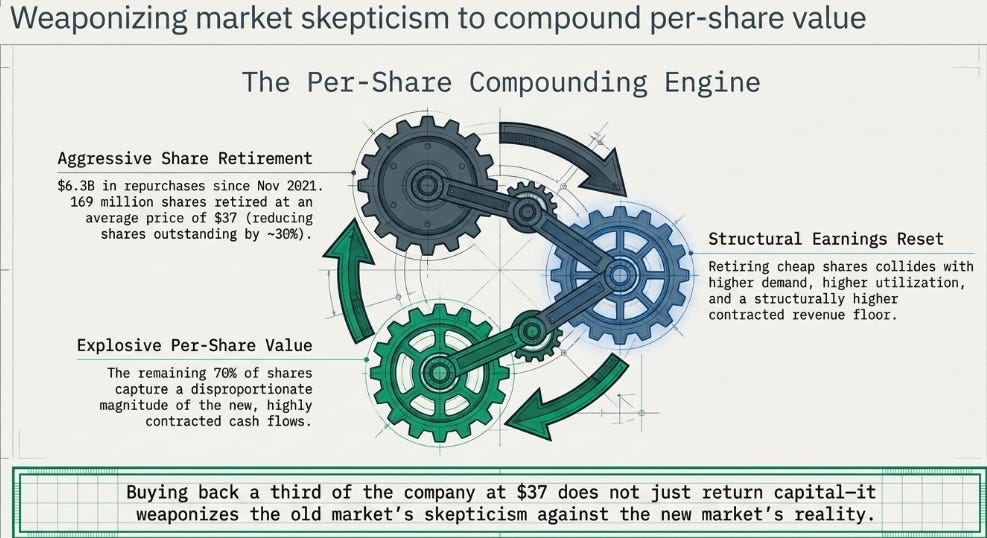

The buyback is not the thesis, but it is the mechanism that makes the thesis per-share relevant.

Since November 2021, Vistra has executed roughly $6.3 billion of share repurchases, reduced shares outstanding by about 30%, and still had about $1.5 billion of authorization remaining as of May 1. On the Q1 call, management noted that the program had retired about 169 million shares at an average price of roughly $37.

That math matters. A company that buys back stock at $37 and then sees its earnings base structurally reset has not merely “returned capital.” It has used the old market’s skepticism to compound the new market’s earnings base.

This is why the distinction between scarcity and conversion is important. If Vistra simply rides a power-price cycle, the buyback is nice but not transformative. If Vistra converts scarcity into more durable cash flows, the buyback becomes part of a flywheel: higher demand, higher utilization, more contracted revenue, more free cash flow, lower share count, higher per-share value.

That is the real bull case. Not AI demand alone, but AI demand converted into a per-share compounding machine.

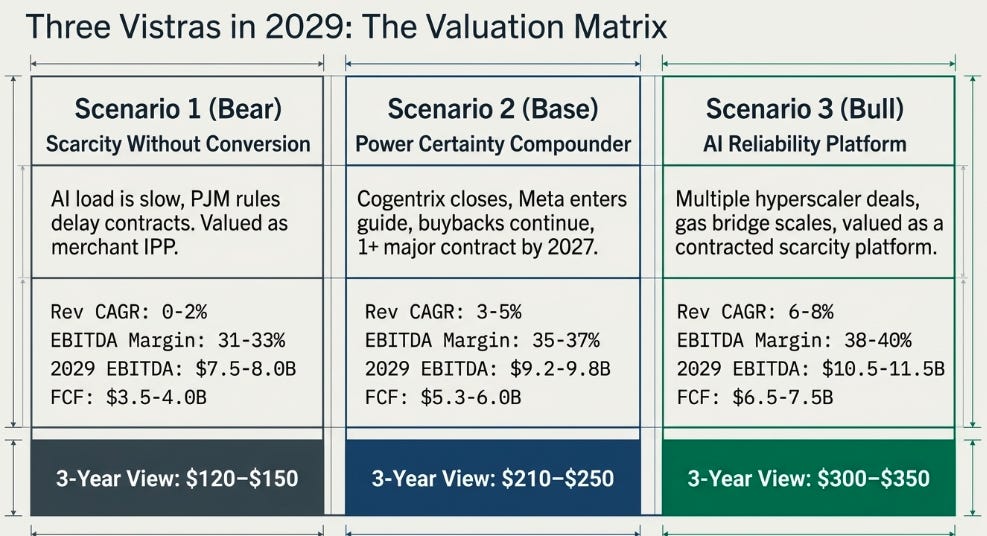

Three Vistras in 2029

The stock is not obviously cheap on current-year numbers. Based on Bloomberg consensus shared, Vistra trades at roughly 10x FY2026 EV/EBITDA, falling to around 9x FY2027 and 8.5x FY2028. That is not deep value. It is a bet that current estimates understate the durability of the earnings base and the upside from contracts not yet in guidance.

The base case is not heroic. It assumes the visible pieces gradually enter the model and that management continues doing what it has been doing: hedging intelligently, buying back stock, keeping leverage consistent with investment-grade ratings, and deploying capital only where returns justify it.

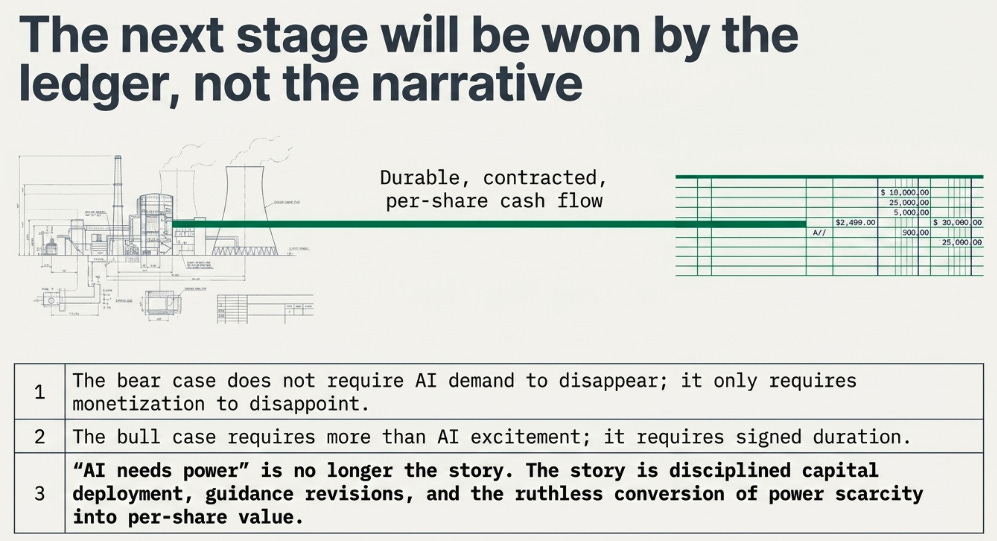

The bull case requires more than AI excitement. It requires signed duration.

The bear case does not require AI demand to disappear. It only requires monetization to disappoint.

What We Watch

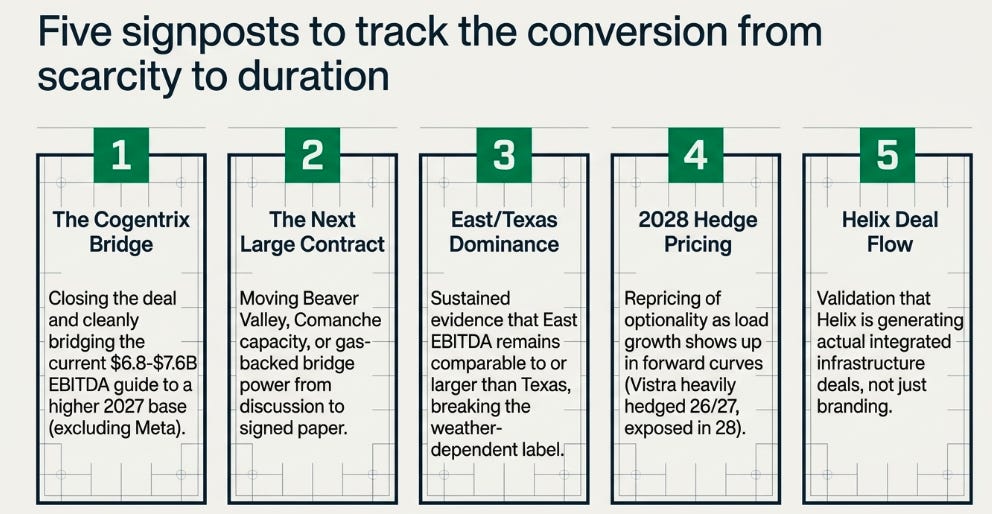

The first signpost is the Cogentrix close and the subsequent guide update. The current guide explicitly excludes Cogentrix and Meta benefits, so the market will want a clean bridge from today’s $6.8–7.6 billion EBITDA range to a higher 2027 earnings base.

The second is the next large-load contract. Beaver Valley, additional Comanche capacity, gas-backed bridge power, or a new-build arrangement would all matter, but the market needs to see one of them move from discussion to paper.

The third is the East/Texas mix. If East remains comparable to, or larger than, Texas, the ERCOT-weather label becomes less useful.

The fourth is 2028 hedge pricing. Vistra is heavily hedged for 2026 and 2027, but 2028 still leaves meaningful exposure. If load growth begins to show up in forward curves, the market will reprice that optionality.

The fifth is Helix. If it becomes a source of real deal flow, it will validate Vistra’s role as a full-stack AI power partner. If it remains branding, the market will discount it.

Scarcity Is Not Enough

Vistra’s quarter did not settle the debate. It clarified it.

The old question was whether AI would make power scarce. The new question is whether Vistra can turn scarce power into durable, contracted, per-share cash flow. Q1 gave us evidence that the earnings base is already changing: East over Texas, generation over retail, hedged cash flow over weather noise. But it also reminded us that the next stage will not be won by narrative. It will be won by contracts, guidance revisions, and disciplined capital deployment.

That is a less exciting story than “AI needs power.”

It is also the story that matters now.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.