Zhen Ding's 4Q25 Earnings: From Mobile Supplier to Interconnect Utility

The AI story is real. The question now is whether it is becoming large enough, fast enough, to change what this company is.

TL;DR

The debate has shifted. The old question was whether Zhen Ding had real AI exposure; the new one is when AI server, optical, and substrate become financially undeniable rather than merely strategically interesting.

“One ZDT” is the real thesis. The moat is not “PCBs,” but a manufacturing system that can absorb rising interconnect complexity across substrates, server boards, optical, and mobile, with Thailand turning geography into part of the product.

The proof points are mix, margins, and cash flow. If AI/server/optical/substrate mix keeps climbing and gross margins stay above the depreciation wave, the stock can re-rate; if not, it stays trapped in the market’s old mobile-PCB classification.

“Zhen Ding Technology’s sales growth is set to accelerate in 2026 as it enters a new expansion cycle... Gross margin should expand despite rising depreciation as high-end AI volume and improved utilization outpace expenses.”,

Bloomberg Intelligence, March 2026

Our January view was that Zhen Ding’s edge was not “PCBs” but manufacturing scale: the ability to turn increasingly exotic interconnect technologies into reliable, high-volume production. The key triggers were ABF yield parity, Thailand readiness, and the quarter when AI server plus substrate revenue crossed a credibility threshold of roughly 25% of mix. I still think that frame was right. What I would update now is not the direction of the thesis, but the burden of proof.

The company has done enough to prove the AI story is real. It has not yet done enough to prove the AI story is large enough to dominate the financials.

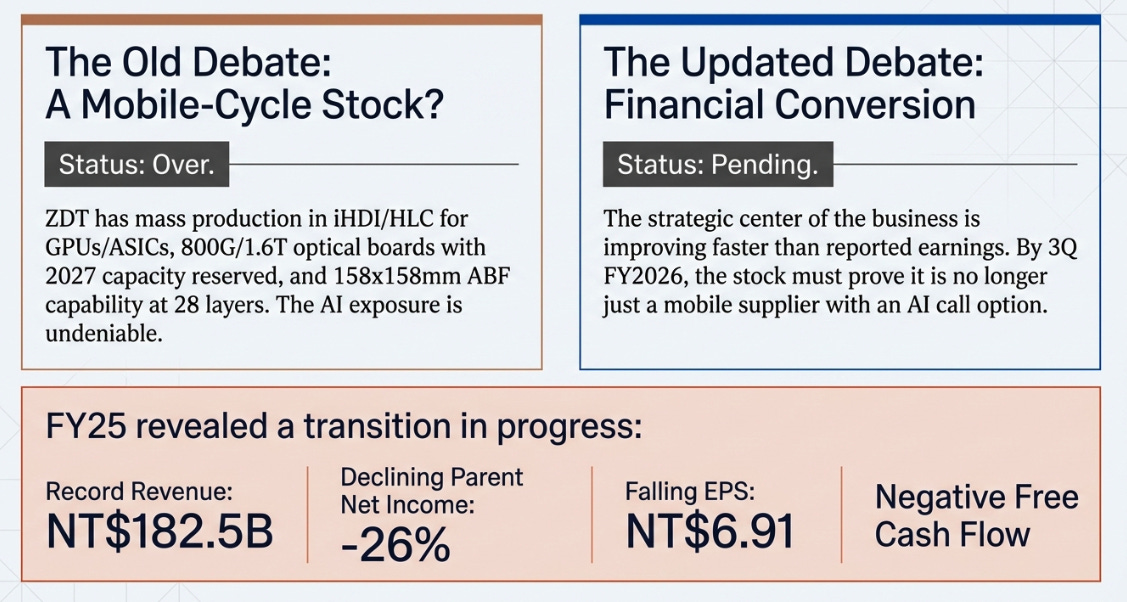

That distinction matters because FY2025 was precisely the kind of year that reveals a transition in progress. Revenue reached a record NT$182.5 billion, gross margin improved to 19.8%, operating margin improved to 7.6%, and Q4 gross margin hit 22.6%, expanding 220 basis points year-over-year in a quarter where revenue declined. AI-related applications accounted for nearly 70% of revenue. IC substrate revenue grew 31.3%. Management said 2026 would begin a “new high-growth cycle” and committed more than NT$50 billion to ten new facilities. But parent net income fell 26%, EPS fell to NT$6.91, and free cash flow turned negative. That is not the signature of a broken business. It is the signature of a business whose strategic center is improving faster than its reported earnings.

The Burden of Proof Has Shifted

The old debate was whether Zhen Ding had meaningful AI exposure or whether this was mostly another mobile-cycle stock with a nice deck. That debate is over. Management made a very specific case: iHDI and HLC products for GPU and ASIC customers are entering mass production; optical demand is driven by 800G and 1.6T boards with customers already reserving 2027 capacity; ABF capability has reached 158×158mm at 28 layers; and the company is spending at a rate that only makes sense if customer commitments are binding.

The updated debate is simpler and harsher: when does this become financially undeniable?

That is the real significance of the 25% credibility threshold. It was never a magic number. It was a way of saying the market would not reclassify the stock until AI server plus substrate revenue became too big to dismiss as interesting-but-immaterial. FY2025 reinforced that judgment. The strategic businesses are rising, combined server/optical/IC substrate reached 11.6% of revenue, up from 9.9% in 2024 and 6.2% in 2022. They are not yet the consolidated story. Mobile remained 61.3% of 2025 revenue. The company is still, financially speaking, what the market thinks it is.

By 3Q FY2026, the burden must shift from narrative to conversion. Not all at once, and not perfectly. But enough that the stock is no longer valued primarily as a mobile supplier with an AI call option.

The Metric That Will Settle It

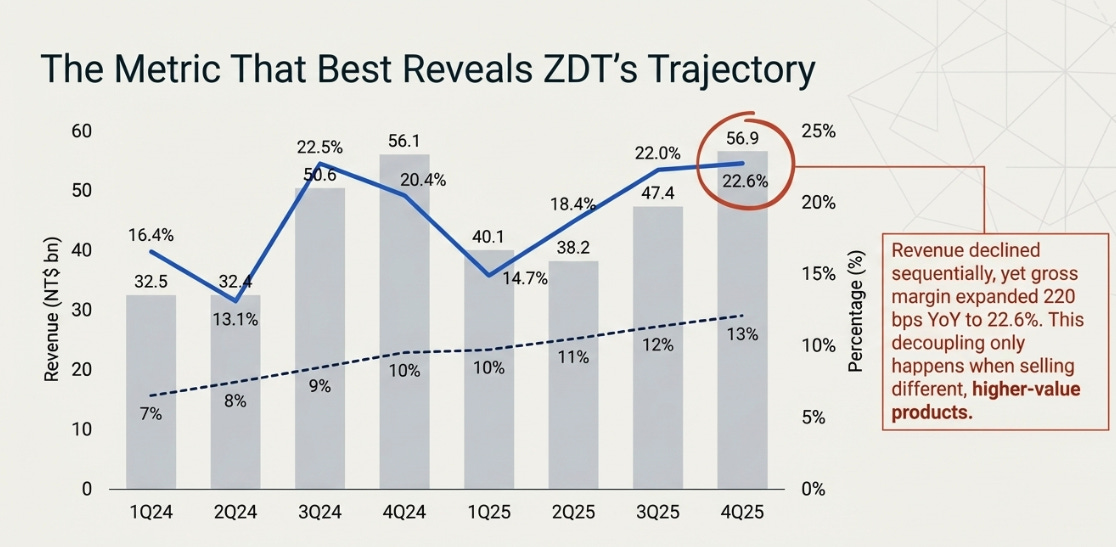

Source: Company filings. Quarterly mix estimated from annual disclosures. FY24 and FY25 mix figures are reported.

The metric that best reveals Zhen Ding’s trajectory is the decoupling of gross margin from revenue growth. In 4Q25, revenue declined yet margins expanded 220 basis points. That only happens when you’re selling different, higher-value products. The question for 3Q26 is whether that decoupling survived the seasonal trough of 1H26 and the accelerating depreciation from the NT$50 billion capex program.

If 3Q26 gross margin is above 24%, the depreciation wave has been absorbed by revenue growth and the margin expansion is structural. If it’s between 21-23%, the transition is working but the old business still dominates the margin profile. If it’s below 20%, the depreciation is winning and the bears are right to question the capex timing.

The competitor comparison sharpens this. In Q4 2025, Zhen Ding’s gross margin of 22.6% was nearly 700 basis points higher than Unimicron’s 15.8%, yet the market treated Unimicron as the “substrate pure-play” and Zhen Ding as the “mobile company.” The gap is classificational, not operational. By 3Q26, I want to see whether that gap has held, narrowed, or widened. If Zhen Ding is still running structurally higher margins than the company the market gives the AI premium to, the mispricing becomes harder to ignore.

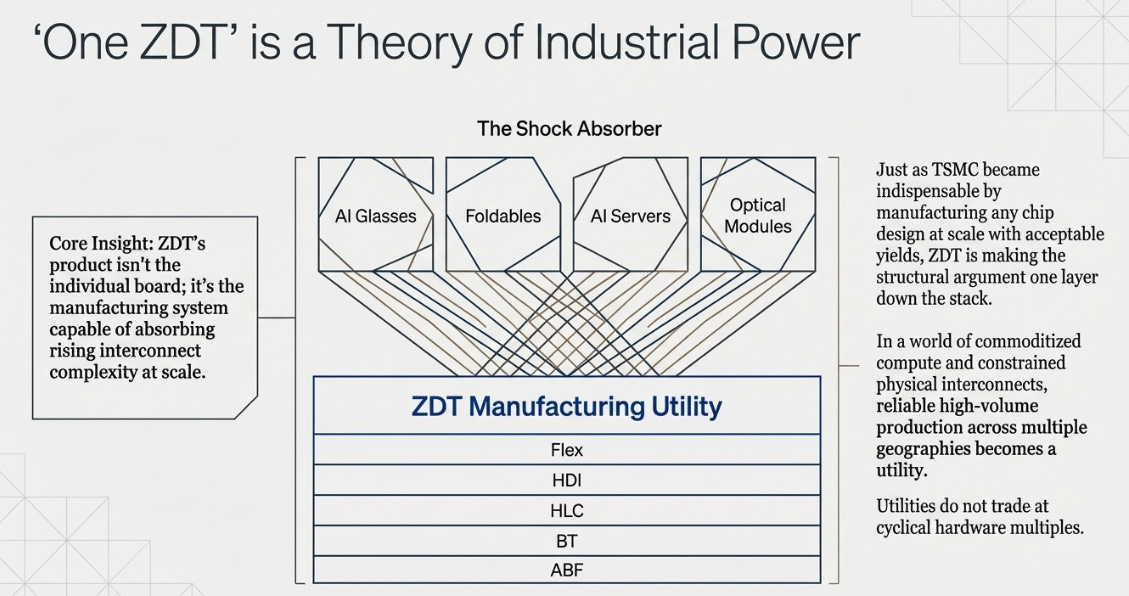

“One ZDT” Is a Theory of Industrial Power

The wrong way to hear “One ZDT” is as generic bundling. The right way is as a claim about what becomes valuable when computing fragments into more layers: flex, HDI, HLC, server boards, optical interconnect, BT, ABF, foldables, AI glasses, and eventually technologies that blur the line between substrate and board entirely. Zhen Ding’s product is not the individual board. Its product is the manufacturing system that can absorb that complexity.

This is the same logic that made TSMC indispensable, not because it designed the best chips, but because it could manufacture anyone’s design at scale with acceptable yields. Zhen Ding is making the same structural argument one layer down in the stack. In a world where compute is increasingly commoditized but the physical interconnect is increasingly constrained, the company that can reliably produce 28-layer substrates, 1.6T optical boards, and server backplanes across multiple geographies becomes a utility. Utilities that are essential and capacity-constrained do not trade at cyclical hardware multiples.

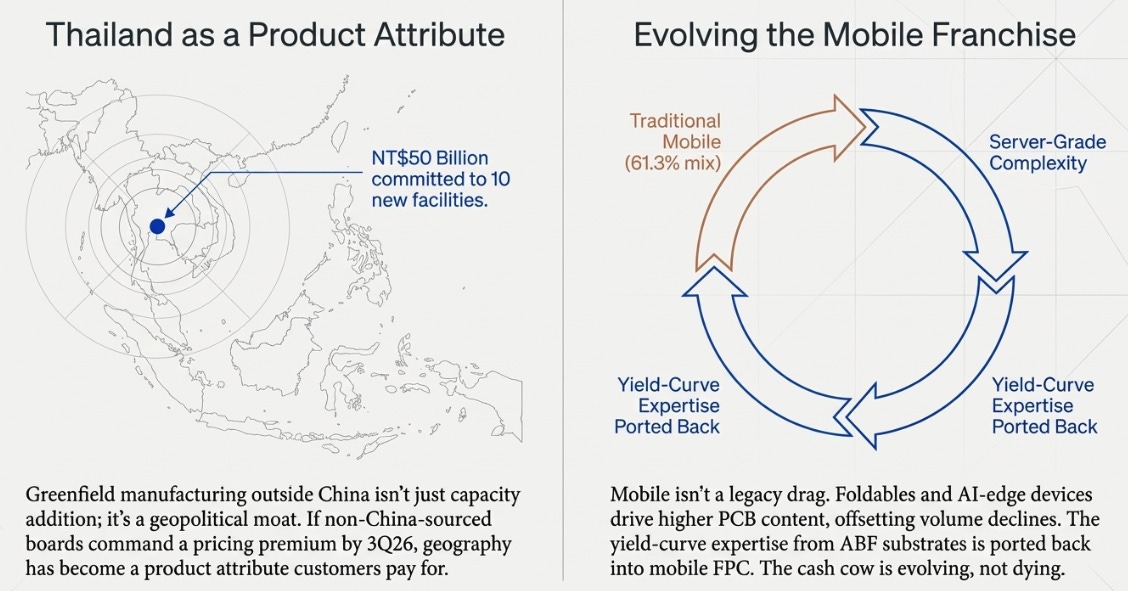

Thailand is the proof that this argument is landing with customers. Building greenfield manufacturing in a new country is not adding capacity. It is building a geopolitical product attribute, something customers pay for, not just a cost of doing business. By 3Q26, we should know whether Thailand is at meaningful utilization and whether non-China-sourced boards command a pricing premium. If they do, geography has become a moat. That’s new for PCBs.

The mobile business, meanwhile, deserves a reframe. The memory squeeze was supposed to be the headwind that sank the legacy base. But if foldables and AI-edge devices are driving higher PCB content per unit, enough to offset the volume decline, then mobile isn’t a “legacy drag.” It’s a high-precision manufacturing franchise whose technical requirements are converging with server-grade complexity. The same yield-curve expertise developed for ABF substrates gets ported back into mobile FPC, widening the gap against second-tier players. The cash cow isn’t dying. It’s evolving.

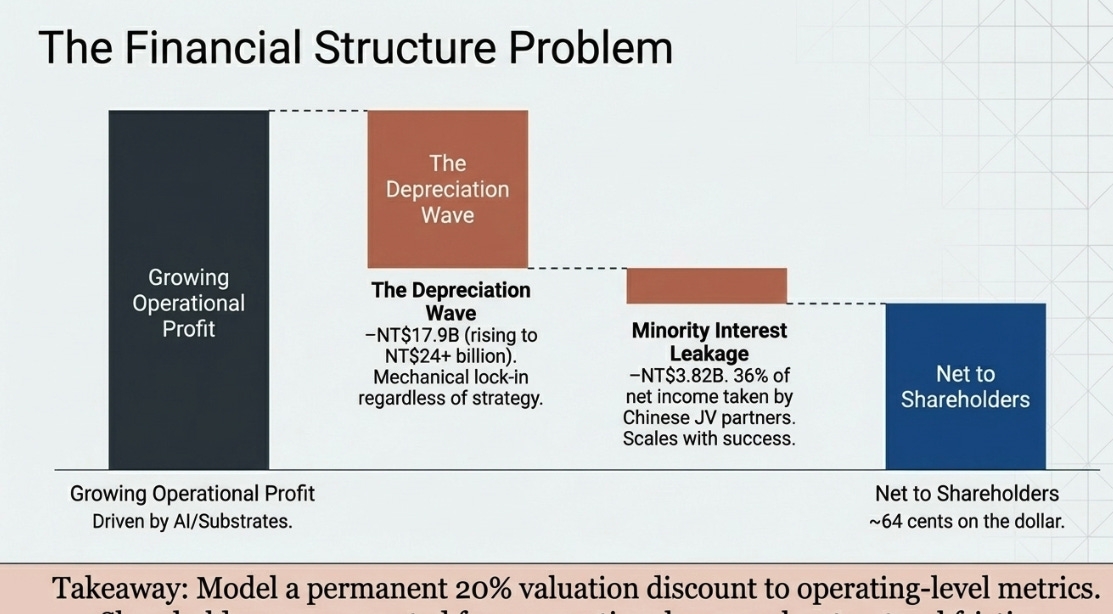

The Financial Structure Problem

Even if every operational thesis is confirmed, there is a gap between what the business is becoming and what equity holders actually receive. This is the part of the Zhen Ding story that bulls tend to skip and that I want to be explicit about.

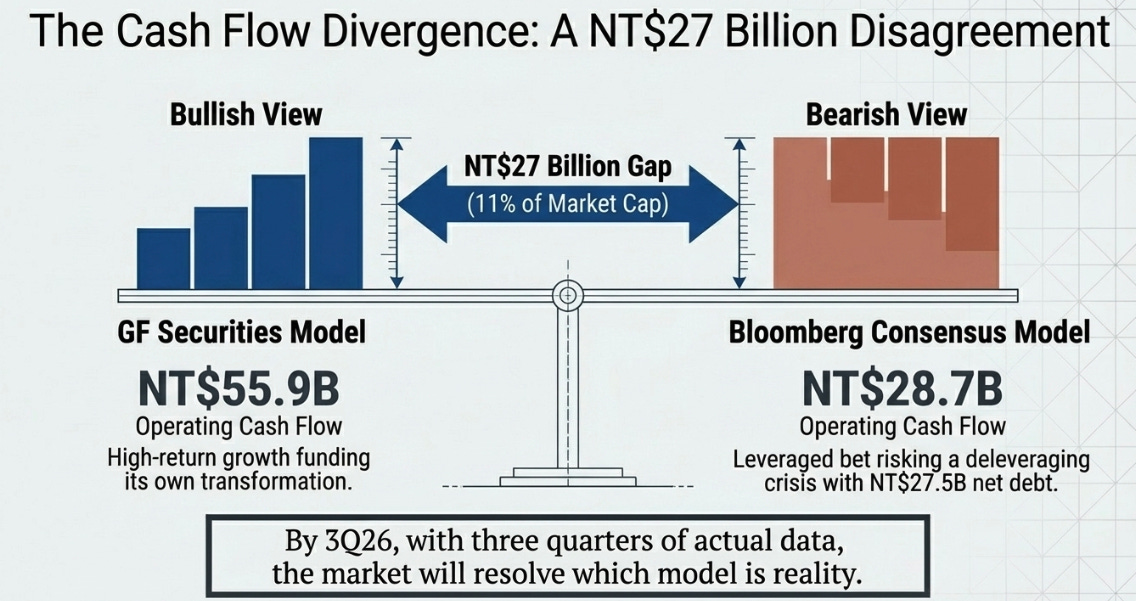

The cash flow trajectory is the most important resolution by 3Q26. In March, the biggest analytical disagreement wasn’t about revenue or margins, it was about cash. GF Securities modeled FY2026 operating cash flow at NT$55.9 billion. Bloomberg consensus modeled roughly NT$28.7 billion. A NT$27 billion divergence, about 11% of the entire market cap. GF saw a company funding its own transformation. Consensus saw a company levering up to NT$27.5 billion net debt. By 3Q26, we have three quarters of actual data. The answer to this question determines whether the thesis is “high-return growth funded by operations” or “leveraged bet that requires perfect demand to avoid a deleveraging crisis.”

The minority interest problem is exactly as structural as I warned in March. In FY2025, minority partners in Chinese subsidiaries took NT$3.82 billion, 36% of net income. For every dollar of operating improvement, shareholders receive roughly 64 cents. This isn’t changing. It won’t change. The JV structures provide political cover and local government relationships essential for operating in China. The leakage scales with success: as the Chinese operations become more profitable from AI and substrate production, the absolute dollar amount grows even if the percentage holds. I now believe this should be modeled as a permanent 20% valuation discount to operating-level metrics.

The depreciation wave is the mechanical test. D&A was NT$17.9 billion in FY2025 and is rising toward NT$24+ billion annualized. If revenue ramps fast enough, depreciation is invisible, absorbed into a growing base. If revenue growth disappoints while the depreciation schedule is locked in, the margin expansion reverses mechanically. The depreciation doesn’t care about your strategy. It shows up every quarter regardless. By 3Q26, the early evidence should show which path the company is on.

The point is not to be bearish. It is to be honest about the distance between “the business is transitioning” and “shareholders are getting paid.”

Variant Perception

Consensus still tends to see a smartphone-heavy manufacturer with a better story than its financials. Bloomberg Intelligence makes essentially this argument: growth accelerates, but high-growth segments remain limited in contribution and margins stay below peers because of depreciation.

The better framing is that Zhen Ding is not becoming an AI pure-play. It is becoming an AI-era manufacturing utility for the interconnect layer of computing. If you expect substrate pure-play margins, you will be disappointed. If you recognize that the moat is the ability to industrialize difficult physical systems across multiple categories, and to finance that with a still-large mobile base, then the company starts to look less like a cyclical component maker and more like infrastructure with a lagging valuation framework.

The classificational arbitrage remains the most concrete version of this argument. If Zhen Ding still runs higher gross margins than Unimicron while trading at a lower multiple, and the only explanation is Bloomberg database tags, then the mispricing is real and the catalyst for closing it is knowable: mix crossing 20-25%.

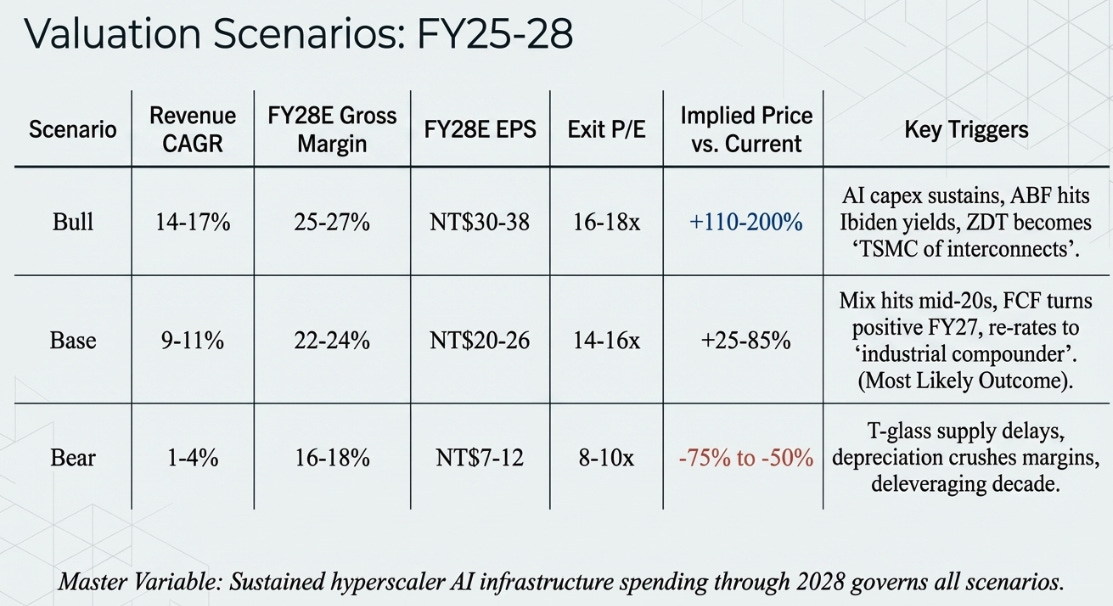

Three Years, Three Prices

Bull requires AI capex sustaining through 2028, ABF yields reaching Ibiden-adjacent levels, Thailand commanding a geopolitical premium, and server/substrate mix exceeding 30%. Zhen Ding becomes the TSMC of interconnects.

Base assumes the transition is real but incomplete. Mix reaches mid-20s%, margins improve but stay below Ibiden, mobile stabilizes through premiumization, and FCF turns positive in FY2027. The stock re-rates from mobile-PCB multiples to “industrial compounder with AI upside.” This is the most likely outcome.

Bear requires AI capex to decelerate before new capacity is utilized, or T-glass supply constraints from Nitto Boseki (whose Fukushima expansion doesn’t arrive until early 2027) to leave factories idle. Depreciation crushes margins, net debt climbs past NT$40 billion, and the company spends the late 2020s deleveraging. This is trackable: watch Nitto Boseki’s timeline, NVIDIA’s platform guidance, and hyperscaler quarterly capex disclosures.

The single variable that governs all three scenarios: sustained hyperscaler AI infrastructure spending through 2028.

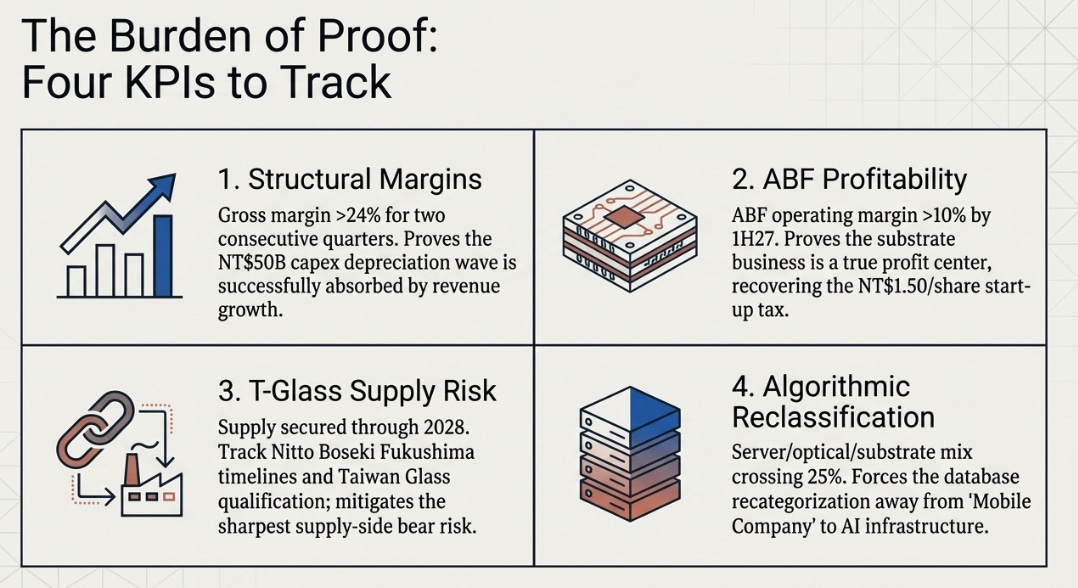

What Confirms It, What Breaks It

Four items. Not eight. Stated plainly.

Gross margin above 24% for two consecutive quarters. Confirms the depreciation wave has been absorbed by revenue growth. We got one quarter at 22.6% in 4Q25. We need to see it sustained above 24% as the NT$50bn capex comes online. Structural confirmation.

ABF operating margin above 10% by first half 2027. Confirms the substrate business is a real profit center, not just a strategic initiative that breaks even on a good day. The start-up tax was NT$1.50 per share. The return on that investment needs to be visible in segment profitability.

T-glass supply secured through 2028. The single most concrete supply-side risk. If Nitto Boseki’s Fukushima expansion arrives on schedule and Zhen Ding has allocation, the bear case loses its sharpest edge. If it slips or allocation is insufficient, the factories sit idle regardless of demand. Track Nitto Boseki timelines and Taiwan Glass/Fulltech Fiber Glass qualification progress.

Server/optical/substrate mix crossing 25%. The mechanical threshold for algorithmic reclassification. Not analyst opinion, database categorization. At 11.6% in FY2025, the company is on the right trajectory but needs another 12-18 months. The pace of that climb through 3Q26 will tell us whether the 2028 bull case is realistic or aspirational.

Our January view was that Zhen Ding’s second act would become obvious when the market stopped seeing a PCB company and started seeing an interconnect platform for the AI era. My updated view is only slightly different, but more demanding: that second act is real, but by 3Q FY2026 the argument must show up in financial conversion, not just strategic coherence. The margins must hold. The cash flow must inflect. The mix must keep climbing.

The story no longer needs belief. It needs proof.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.